has there been anything in the news about falling production and/or logistics issues for last quarter?

1 Like

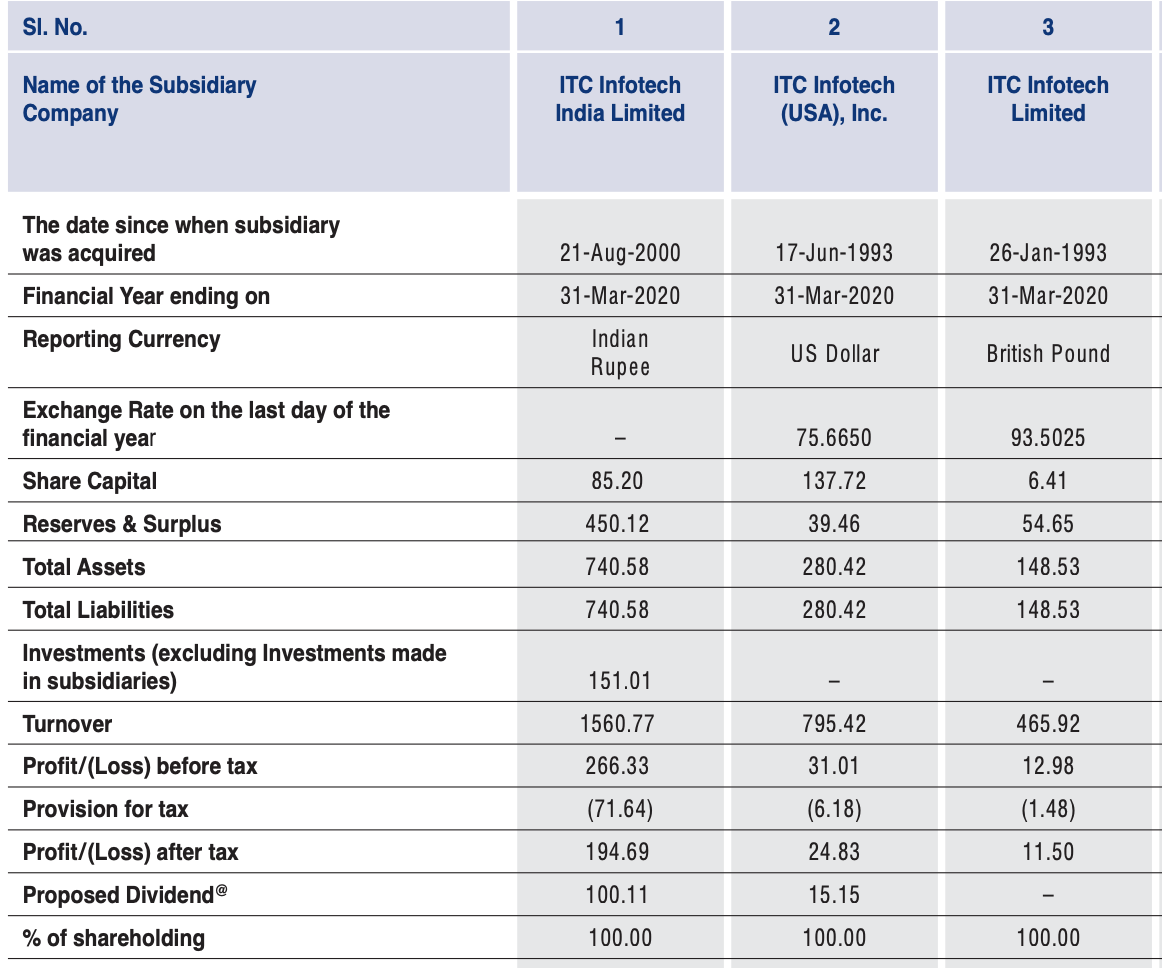

Hello VPs. I have below question regarding ITC Infotech:

- Is there any meaningful contribution from this arm in terms of both revenues /profits and offering its competencies to the group as a whole?

- What plans does the management have regarding ITC Infotech?

Can someone throw some light regarding above questions?

Regards.

Is there any reason why Infotech doesn’t get as much attention as Cigarettes, FMCG, e-Choupal? Even on the company website, it’s listed under “Group Companies” and not as a stand alone business. AFAIK, ITC Infotech has clients other than ITC group companies. So, it should be considered a full fledged business?

7 Likes

One more question on the valuation side- the company paying 10 rs. dividend and assuming 3.5% growth in dividend, and using 10% DR, we get a value 154rs. This is still 30% lower than prevailing price (208rs). Given that dividends are sustainable, because of cigarette business, doesn’t it sound like heads I win, tails I don’t lose much opportunity ?

Open to criticism.

ITC’s plus point is its Valuation, its negative point is Growth. Almost nobody says its expensive, the only issue is the Earnings growth is not that much. To make things worse, ITC had capital allocation issues in the past and there is a consistent Regulatory overhang due to Cigarettes business. That is why street is divided and most big investors are not ready to take the plunge.

Infotech is as core as Agri business and paper board … It support primary business and does competitively business across the world but at much smaller scale .

ITC is not known as paper or agri business or IT services company … It is FMCG company …

Hence management speak with that emphasis …

ITC on wishlist since last two years . Even though reasonable valuations still I’m not fully convinced to buy .

The company’s hospitality business has burnt a significant amount of the company’s cash-flows generated from its most cash generative business segment – the cigarettes business.

The fast-moving consumer goods business launched in 2000 generates just 3%-5% of pre-tax profit and 6% of return on equity compared to 35% by others. even though the FMCG business brings in a quarter of the company’s total revenues, it only contributes to ~3% of ITC’s profits.

It recently acquired Sunrise at around 3.7 times its FY19-20 revenues of Rs591 cr, at a P/E (price-to-earnings ratio) of 37. ITC itself hasn’t been able to sustain its P/E of 15.

Over the past 12 years, the company’s employee costs have shot up by 3.26 times, yet its revenues have only grown by 3.12 times

ITC’s stakes in EIH and Leela have been suffering tremendous losses; just in FY18-19, it lost Rs.1250 crore.FY 20 is worst due to covid.

Still it’s cash cow is cigarettes . Which always comes with regulatory issues and Taxation

But valuations are good… n it’s a value play plus dividend…But I firmly believe ITC can create value for its shareholders only by demerge of it’s FMCG . Only time will tell if that’s happening.

3 Likes

And nothing wrong with that. As long as there is addiction in terms of Tobacco, liquor and other stuff, there’s a market for the ‘fix’. In terms of ITC, we know the rest of the biz is for ‘derisking’ from single revenue source; Most seem to have revenue growth(hotels excepted) which makes me want to believe the management is first looking at market expansion and growth before focusing on profit on noncig areas.

If anything, if they’re not good at managing accrued cash, they seem to be giving dividends, so not complaining on their prudence part too. Personally, trilateral ownership is a good thing, management cannot do some silly ‘moon shot’ and crater themselves in boring business areas

6 Likes

Disc - Invested.

That is true. In fact, two things are puzzling.

- ITC cannot leverage it’s cigarette distribution to push its bingo chips. Sadly,all we see at pan shops are balaji wafers and parle/ Britannia biscuits. Why?

- While sunfeast dark fantasy, aashirvad atta and yippee noodles in eatables and savlon in soaps have more availability, same cannot be said about other ITC products. Why?

Why is the management not able to leverage their existing channels to push other products?

The above fact is more glaring to the eye considering how The current management is solely focusing on FMCG.

9 Likes

With all due respect ITC’s Capital Misallocation Narrative isn’t as bad as people portray it to be if you take into account the the entire picture into play.

Read this article to find out more

Also as per last results Presentation the Margins have gone into double digits when Sunrise is taken into account as well. Even ex Sunrise it is within striking distance of double digits.

A lot of people also constantly are very vocal about how the company’s distribution and availability of a product isn’t very strong. Guys, this FMCG division has been in business for only 3 decades, please cut them some slack before comparing them to Nestle, HUL who have been in business for more than 10 decades

And imagine if with this kind of availability and distribution if this company is clocking 12000 CR+ of Revenue what’ll they do when they soon strengthen it

Just my 2 cents.

Disc : Invested.

6 Likes

Frankly speaking three, four years down the line, the moment we may see that the balance or the distribution is in favour of the non cigarette business over the cigarette business, then it will have a much better valuation to command.

It a good company with a great balance sheet, good dividend payout, clean management.

At present I’m neutral. Still not convinced .still in doubt if it’s a value investment or value trap . Finally market knows better. So respecting it .

A trigger could be the demerger of fmcg business

Hi Chinmay, resonate with your thoughts, but will not excuse the weak distribution in ITC. I have checked this weakness out, at the ground level.

They have created a number of verticals and they drop them just like that… Minto is a very strong brand and is a case in point.

The opportunities for ITC are huge in the Foods side of the consumer biz. they have hotels and the Agri biz for supporting this Foods Biz.

Frozen Foods, Ready to eat is a very big area and its restaurants in the Hotels is a rich area for identifying items from

Similarly, the RM cost for the foods part of the FMCG biz should get support from its E-Choupal biz. Its not visible

distribution is not the only angle, lays and balaji and lots of other fmcg products ae way ahead in taste and quality, and give better margin to retailers, who prefer to keep what sells ,rather than locking up capital.

ITC needs to get that edge

2 Likes

@Vego Your preference is noted. I actually prefer Bingo to Lays. What I am curious about is the more definite and objective data like “better margin for retailers” that you state.

Is the phrase your guesstimate or is it objective information? What is the margin difference?

Regards

3 Likes

Balaji scores on Larger volume to price for end users, and lays offers better margin MRP 5CP 4.5/4.2 . MRP10 9/8.4 , tried checking for Bingo but cant get any retail bedi shops selling this

3 Likes

Can you please throw some light on what happened with Minto or point me to an article about the same ? Would love to know what went wrong.

2 Likes