Capital allocation – was never as bad as perceived; will get better from here on

Three things essentially decide at what rate a business compounds wealth for shareholders – 1) how much return you make on the existing business 2) what is the sustainability of that return 3) how you use that return (OCF) – re-invest profitably , redistribute, hoard cash, re-invest unprofitably (best to worst in the order listed). ITC always rated high on the first metric thanks to is monopolistic position in the cigarette business but rated poorly on the third metric as a bulk of the cash was being re-invested unprofitably in FMCG and hotels. That is changing for the better now.

From FY08-20, the cigarette + Agri + paper business generated a cumulative FCF of Rs930bn. Out of this, 6% or Rs60 bn was invested into hotels and 8% of Rs80bn was invested into the FMCG business. It should come as a surprise that only 15% of the FCF was indeed spent on FMCG plus hotels. Hotels infact, has taken just 6% of FCF and has unnecessarily drawn more than its share of criticism.

The reaming 80% of Rs750bn was paid out as cumulative dividends (average payout of 70%). ITC has hardly done any large ticket M&A. While less than ideal, ITC of the last 12 years already scores higher than companies such as GCPL which have paid out 30% of profits as dividends and invested more than 50% of FCF cash unproductively in far flung endeavors outside India.

What is changing going ahead? – the FMCG business was in a hyper investment stage and now is reaching scale with visible improvement in margins. Bulk of the capex here is behind and future capex can be funded with its own P&L. The FMCG business is thus changing to a cash additive (like all FMCG companies are) from being cash dilutive. Segments such apparel retailing which were loss making have been wound down – shrunk store count for Wills Lifestyle and sold John Players to Reliance.

In Hotels – ITC has acknowledged that capital has not be deployed productively. That said, they have built brands (ITC, Welcome, Fortune, Welcome Heritage) and have built in-house expertise in running luxury hotel chains. They are now pivoting to an ‘asset right’ model where they will enter management contracts with property owners and earn royalties on running the hotel chains. Simply put, they will get people like Chalet hotels to own the assets while they will play Marriott’s part. Bulk of the incremental room addition will happen via management contracts. This is a major change and means that hotels will no longer be a major cashflow drag for ITC.

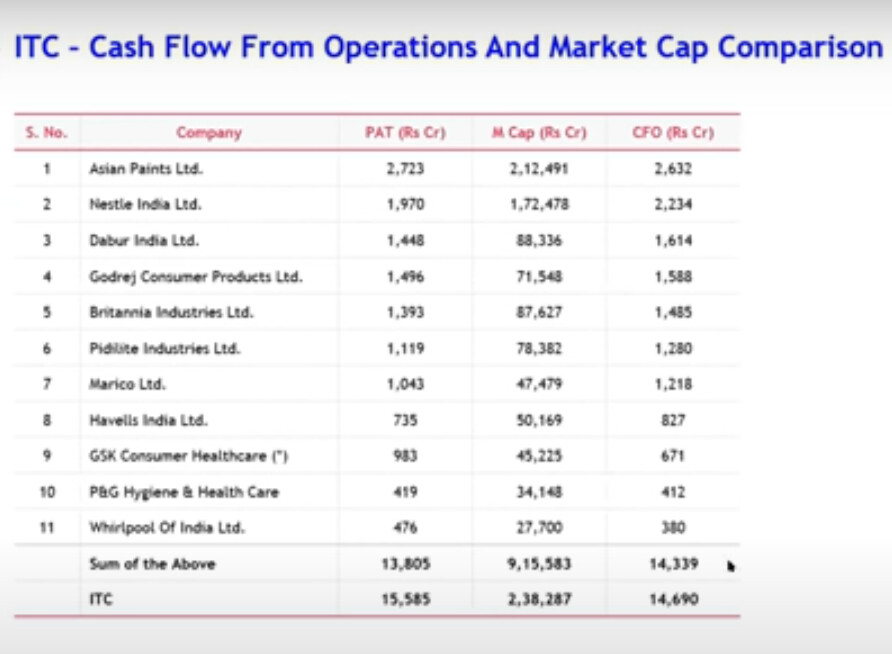

What this means that 100% of cigarette business cashflows now can be paid out to shareholders. In that direction, ITC has increased its dividend payouts to 80-85% of profits from an average of 70% over the previous 10 years. At current price of 225, ITC’s FY22 dividend yield is 4.5% and FCF yield is 5.5%.

What I admire the most is a clear stated prudence on M&A. Sanjeev Puri has made it clear in media interviews that despite the large cash balance and annual accretion, ITC will be conservative in ‘paying up’ and only focus on small deals where they can acquire brands and substantially scale them up (like Savlon). The recent Sunrise Foods acquisition is a good example. There will nothing outside India and in unrelated categories outside of FMCG.