I think, one of the most intrsting updates by company in recent times :

Disc. : Invested.

Wonder how much of cost savings this will generate?

Also wonder whether Nicotine production is coming under any “ESG” bans worldwide, which is shrinking the production.

Disc: Invested

Very Interesting.

One company that I have seen making aggressive strides in the choc space has been Amul. I have seen a lot of “cadbury” families making a shift for Amul. ITC is still very premium. Wonder, if they have plans to compete in the segments that Amul is competing in. Will be interesting to see their brand and product positioning.

Even in Noodles, after careful research, they introduced Yippee targeting kids who liked non-sticky and longer noodles. It was a slight change but paid out huge dividends.

Their pricing and positioning is more at the premium end, competing against Bournville and Dairy Milk Silk. The starting price is around ₹70 which puts it out of the ambit of the average impulse shopper in India (these are usually ₹5 or ₹10 packs that are either bought on impulse or for birthdays). How well Fabelle scales down in price and scales up in volume will determine this play.

I have tried all their chocolates over the past 3-4 months and loved most of them. The mouth feel is more in line with premium brands and not the mushy dairy milk of childhood memories. How well this will play with people who grew up on dairy milk and never outgrew it (99% of us) is the question.

And they don’t have a play in the “healthy” chocolate segment of 80% and more cacao beans. Amul’s strength lies in the super wide range of chocolates they have (I know of and have tried 24).

Another observation is that in the 4-5 (non-chain) supermarkets that my family frequents, we have not seen Fabelle at all. Even Karachi bakery’s chocolates and other new brands have gained shelf space but Fabelle is invisible. As an investor this remains an area of concern - only one of the store owners even knew about the brand.

This topic is temporarily closed for at least 4 hours due to a large number of community flags.

This topic was automatically opened after 8 hours.

Good interview that gives some insights into Fabelle’s Business and the future plans. Really waiting to try it out.

Disc : Invested.

Don’t think Fabelle can compete with likes of Cadbury or Amul. They are super premium even than Ferror Rocher I think. The only way they can enter the mass market is by reducing the cost of chocolates sold which in turn would require a change in overall Fabelle brand image and company input cost in making these chocolates as currently high premium cocoa are only used.

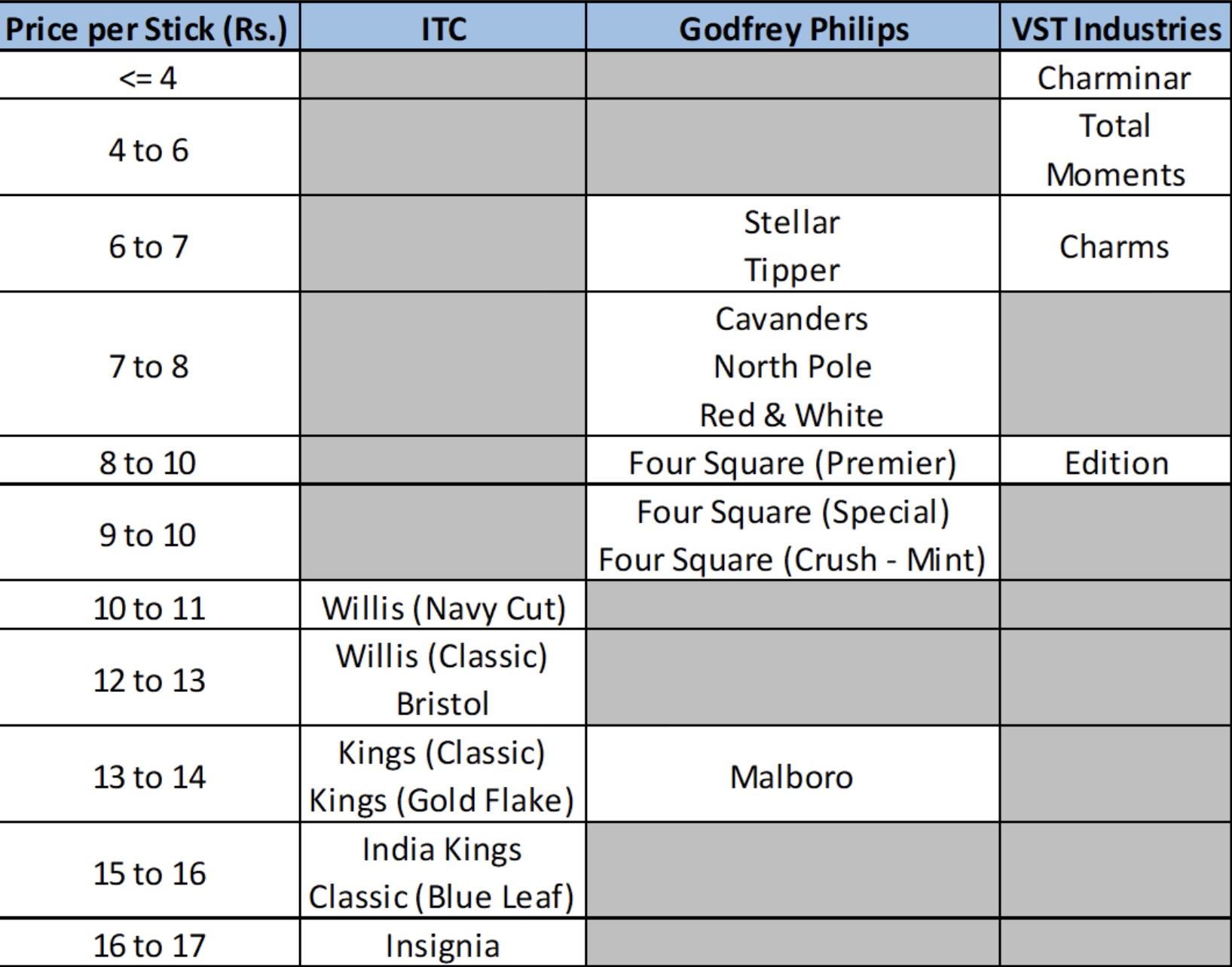

Quite interesting insights into who’s selling what in the 69 mm cigarettes market along with prices. Good to see ITC is at least not stagnant to the prospect of them losing market share.

Hello,

Been reading alot here lately and I think I could help.

First I believe some people are interpreting ITC’s business incorrectly

So I will try to paint a picture with some points

-

Hotel business.

Many people just want them to sell their hotel business. Although I understand the sentiment but long term value creation does not happen by taking decisions on short term.

So why does ITC needs it hotel. Well I believe it will be a key ingredient for almost all the future growth. How?

They are not limiting themselves and want to take over the food industry.

If you see the process of how ITC launches a food product can see hotel playing a big role in it.

They first launch their product in all their hotels. Taking inputs from all the top chefs in the country and trying those things out on customers before starting to sell it in the open market is a huge advantage and people studying management and strategy will agree that this gives them an edge over others.

If you listen to previous AGMs you can see Mr. puri talk about incubating prawns product or some other food product. Hotel helps them incubate products and all the future food products are currently incubating in those hotels.

I’ve seen alot of companies talk a lot about synergy. But this maybe one of those few instances where synergy works.

Me personally, I dont mind hotel not contributing to profits or revenue (its just me being conservative here) because I think they will be of big help in the future. -

Pricing of products.

I think some news article wrote something about ITC’s chocolate product and somehow that started a discussion over here and people are suggesting that they should lower their prices.

First of all ITC always asks for a premium

Cigarette:

Biscuits:

The same goes with chocolate. They are not here to compete with cadbury or other chocolate brands. They want to compete internationally. And if you have tasted those chocolates you will agree that they do deserve the premium they ask for. So I dont they should punish shareholders because majority of indians cant afford their chocolates. As people will get richer they will be able to afford and they would win the war without competing with its competitors.

So I dont mind many of my friends not going for fabelle. If they have tasted it once they will come back.

I think people here need to stop looking ITC as a 200 rupee stock and start thinking of the company as a luxury brand.

While I appreciate people backing the investment thesis with logic but being blind to facts is not an investor work.

just to get the food taste etc they have a complete hotel business … Why can;t Nestle etc do that then if that is so successful. Why Yipee despite having free run for years and Maggi in controversy can’t be NO 1 noodles … Lets support investment but not get blind.

Having said that …

ITC is a company where downside is almost capped given the cash flow visibility and trading volume liquidity but the upside is UNKNOWN. They need to perform in FMCG and get on to better ROIC for it to be at par with best.

Always remember if someone is thinking himself intelligent buying at a price, someone is equally thinking himself intelligent on selling at a price. The only thing that separates BUYER and SELLER at this price point in ITC is only INVESTMENT HORIZON and RETURN EXPECTATION.

Hello my friend,

If I may speak freely I still prefer having nestle over yipee. I don’t know why it is but I have tried and the taste of nestle has just settled in for me. I’ll be stupid if I assume thats the case with everyone, but when put in a place where even I wont prefer ITC I wont defend ITC. Where its bad its bad. No need to hide.

I do have something to say though. This 29% market share they pulled it out of thin air. They didn’t go from 100 to 29 they went from 0 to 29. All I can do is close my eyes and believe that future generations won’t be so rigid in their taste preferences as me and things MAY look up in the future.

I appreciate your comment on hotel. I am not saying what they are doing or did is so out of the box that no one else can do it. I just happened to be impressed by the idea that instead of investing their capital which does not produce any accountable return they invested it in hotels which may produce something.

And at last the return on capital employed. What I have been lead to believe is that accounting is the language of business but it does have its limitations.

As I indicated in my reply that hotels incubate products. And now they have started entering the market. And now all of a sudden they have positive return on capital. Isnt that strange?

As these products are incubated they incur all the cost but they add almost nothing to the revenue / profit.

So what I believe is that their margin is not that low. It looks low because it accounts for costs of products which they are incubating.

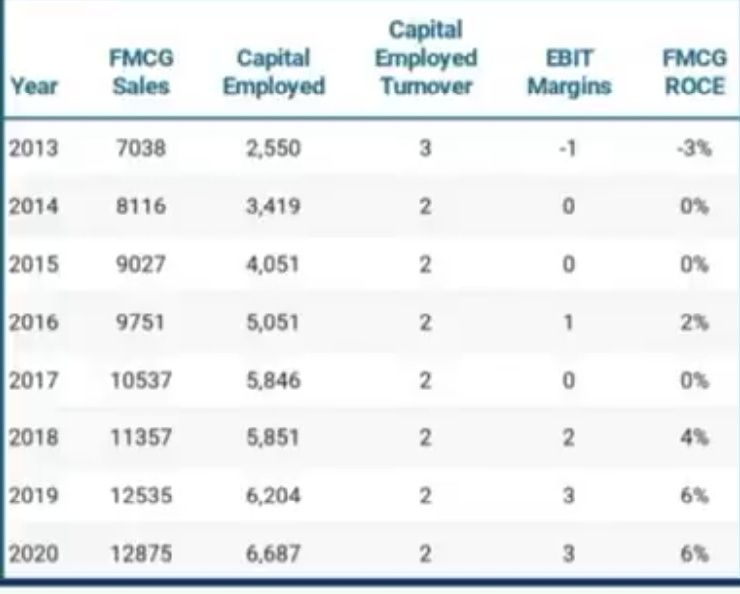

As they start releasing more products the margins and the returns will improve ( as suggested by the table given by you ).

And as I already showed that they ask for more premium than market average. I do believe their profits are above average on the products they released. You can’t charge the most and have least margin among your competitors.

It is the limitations of accounting which businessmen like you and me have to understand.

I do believe market is always forward looking. So if market had all these facts with them they might value ITC differently.

And lastly, I would never tell anyone how to do their job. I wont tell modiji how to run a government, if I think i can do better i will do better. I wont tell tim cook how to make phones, if I believe I can make better phones I will make better phones. The same way Mr. Y C deveshwar picked Mr. puri and Mr. puri promised to make ITC into a fully fledged FMCG company. I have no reason to doubt otherwise. But I would prefer to check regularly his words against the results. So after checking results I would say he is delivering on his promise.

Thank you

I just want to quantify the “something”. Just for comparison sake, ITC has over 100 hotels so do the Indian Hotels Ltd(Taj Group). ITC generates approximately around 60-70 crores in annual profits while the Indian Hotels Ltd in its best year generates about 400 crores in net profits. Lets say you make a far fetched speculation that it someday will generate 450 crore annually. Still, is that number relevant in any way? I don’t think so. ITC as a whole today generates about 15000 crore net profit. Adding that 450 crore to that number today itself doesn’t even make ITC’s overall growth flinch by even 3%. For me, if I am looking forward, hotels are not even relevant.

I guess ITC management also acknowledges now that Hotels will not have focus anymore. Hotels we talk about are legacy decisions. Now Mr.Puri has only two options, one is to find a buyer for Hotels and sell them off. The market will be more convinced if that happens but as a owner, one will not sell during Hospitality sector downturn as the valuations are very depressed. The other option is to put your assets to best use like what Hitendra had explained, like using your capital intensive asset to help incubating your growth areas. I won’t say this should be their long term strategy and there might be better cost effective ways. As a manager, one would make decisions with options on hand and trade offs. ITC management is trying to extract best use of their Hotel business for their FMCG launches. ITHL is more of a specialised Hotels business so comparing them would not be right.

I feel we should trust the management and track the result and see if they walk the talk and going in the right direction to create more value for the shareholders. If not, one can always sell and move to greener pastures.

An interesting investment thesis on British American Tobacco (BAT) and nuances of tobacco industry, must read for those interested in understanding dynamics of Tobacco industry better:

Few excerpts from the blog:

Is ITC thinking of growing this business for outside clients as well, from now where it is mostly for internal work?

Could not find any info with regard to this

A counter point with ITC governance issues, from a well know investor

Quite an interesting step by ITC. I think, this engagement drive would give more eyeballs than an Ad spend on TV.

25k retailers across India is quite a number, am sure, they would target more than this in this drive.