Great results from itc, imo:

For me, the key monitorable is that the PBT from FMCG has tripled from 92cr to 282cr (YoY)

Great results from itc, imo:

For me, the key monitorable is that the PBT from FMCG has tripled from 92cr to 282cr (YoY)

ITC Q2 PAT at 3519 cr vs 4119 cr yoy, In Q1 PAT 2424 cr

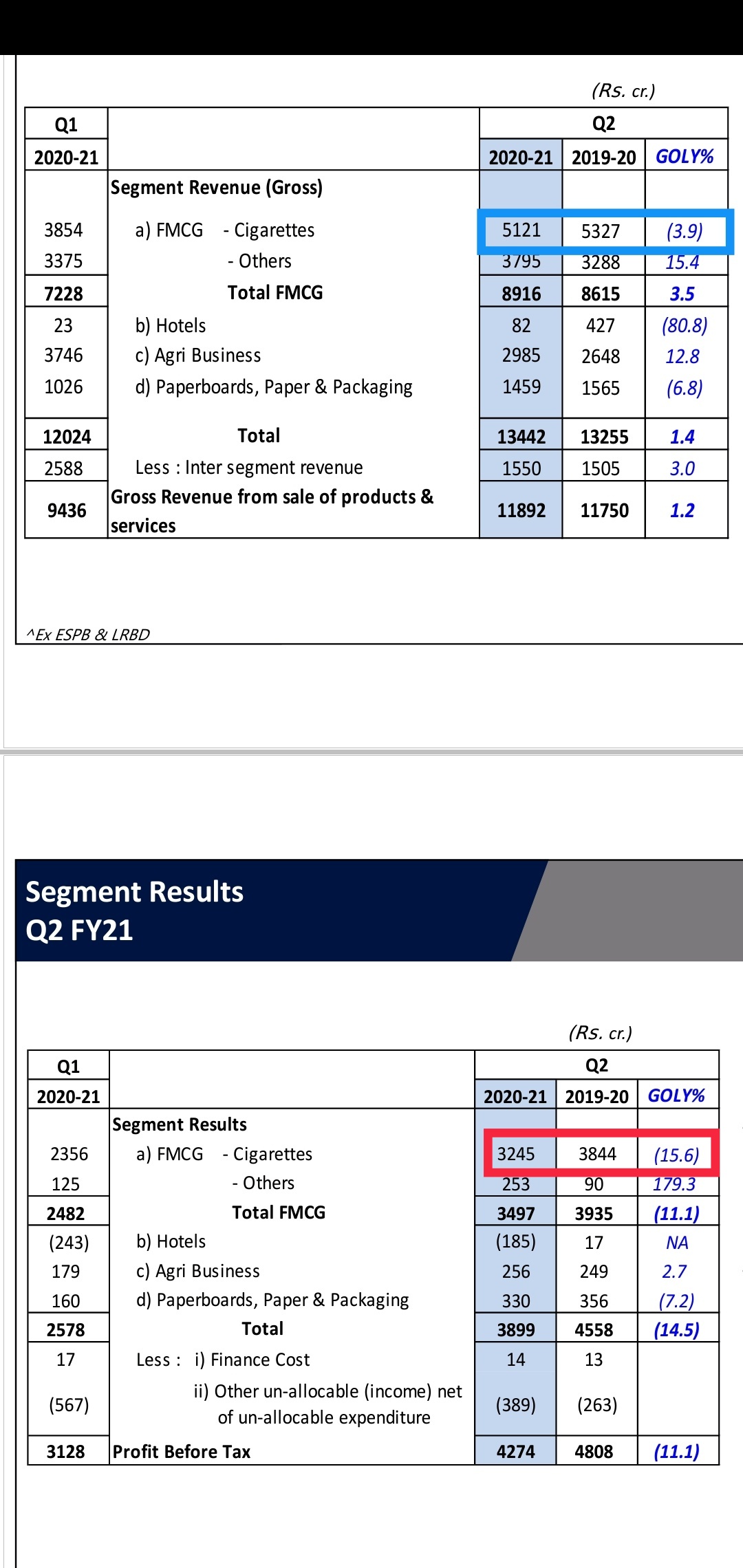

FMCG sales at 3930 cr vs 3296 cr yoy, In Q1 FMCG sales were 3378 cr

FMCG- PBT at 282 cr vs 92 cr yoy, In Q1 FMCG PBT was 129 cr

Major re rating may follow on back of FMCG turnaround

Disc : invested

Although would be good to have this rerating but not sure if there will be anything major over medium term yet. FMCG sales growth of 20% is somewhat comparable to peers, PBT is indeed good but still profit from FMCG is miniscule in the scheme of things…Would be interesting to see how market behaves…

Views welcome

Disc: Invested

Hotels loss narrows to 184 cr vs 282 cr in Q1

In Q3, that too may turn around.

Heard the commentary from Indian Hotels management. They have recieved record bookings for Nov, Dec.

Hi…

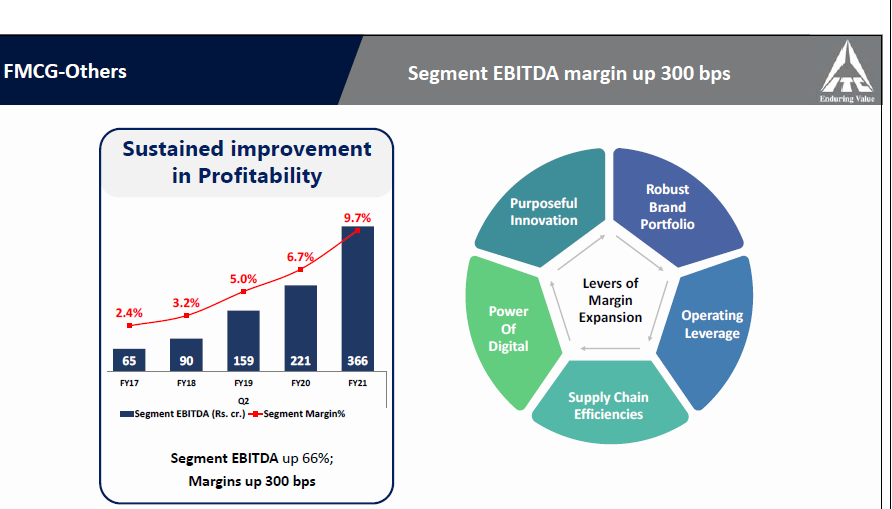

Q2 FMCG EBITDA is 366 cr , Margins at 9.3 pc.

Q1 FMCG EBITDA was 257 cr, Margins at 7.6 pc.

In Q2 last yr, FMCG EBITDA was 221 cr, Margins at 6.7 pc.

Good improvement in Margins. That got me a little excited.

Or…am I missing something??

fmcg others profit margin increase from 2.7% in Q2 2019 to 6.6% in Q2 2020. Profit margin more than doubled. Hopefully the market share gains made during covid is retained post covid

Agree that all is good for FMCG as expected and on lines with tailwinds for other FMCG companies as well. What I meant is that as you said major rerating, for that still FMCG profits are very less as compared to overall profits and hence for street to look at ITC as an FMCG company maybe sometime ahead. So for immediate/medium term movements of stock, we need to focus on cigarettes performance as well. The revenues for that are down approx 4%. So overall the subsegments performances may balance each other.

But you never know, street is very forward looking, more that we can imagine…you never know what it likes and plots for years ahead. For me, for ITC to be valued as an FMCG would start when its FMCG profits are at least half of cigarettes, for then the growth in FMCG would start to meaningfully offset the decline in cigarettes (if decline) QoQ. Pls note these are just my thoughts and I maybe wrong. Thanks

Also, if anyone has any thoughts on why the Agri business, which many vouch for and we speak about e-choupal etc. and ITC agri business as one of the next level businesses it has invested in - has a decent revenue growth of 12.8% but EBIT growth is only 2.7%. Would be good to know why EBIT growth is below par with a business of such strength?

Thanks

Disc: Invested hence concerned

One optimist perspective for YoY quarterly views

Outside cigarettes and hotels business, rest of ITC biz ( fmcg, agri, paper, others) have reached closer to 1000 cr profit over 9000 cr revenue, YoY comparison would be 800 cr profit on 8000 cr revenue. That’s 13% revenue and 25% profit growth with margin expansion.( numbers are approximate and grouping them for simplicity)

Cigarettes in same period is marginal decline on revenue of 5 % to 5600 cr and profit dropping by 15% to 3500 cr. Expect them to recover to normalcy.

At growth rate of #1 FMCG+agri+paper+ Other could reach to 2000 cr profit over 3 years at 25% CAGR - now that is something market can’t ignore as it is clearly catching up with cigarettes profitability numbers over next few years and ready to shoulder future growth as main engine.

As they say mkt is future focused, hypothesis has more substance with every passing quarter than before and if it is of any credentials, PPFAS has ITC as largest holding

Also sunrise food numbers when added from next quarters, will strengthen FMCG pie and accelerate journey

At best mkt may wait to see 1-2 qtrs to see consistency and slowly react.

Any further developments on Hotel biz drag impact on profitability as hindrance will seal the fate further, mgmt has acknowledged issue and assured to keep it capital light and so on…

Invested

Margins for all companies have increased on account of Covid related cost cutting. So need to see if this margin improvement is a secular trend that can be sustained, or has one-off cost cuts.

Also, inspite of the margin improvement, share of FMCG (non-cigarette) margins to overall margins is still a measly 7%.

ITC is a great business to be honest, but the turnaround into an FMCG-focussed player will take quite a bit of time.

Hello all,

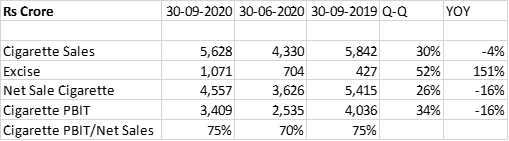

I have a question regarding Cigarette business. While the YOY revenue fall in cigarette business is only 4%, the YoY profit fall for the same is more than 15%. Can someone please explain the reason for this?

Investor presentation with lot of information on the results and the demand scenario

Few guesses …

Agri business also has decent tobacco business domestic + exports … These are higher margin business as compared to wheat , soya , mustard etc , This would have declined with lower Cig consumption across the world .

Agri businesses are highly seasonal and one should look at trend over 3 /5 years rather than QOQ or YOY …

ITC - FMCG others @ 18%+ Gr seemed to performed better than other FMCG companies like Nestle ( 9% Gr YOY) , HUL ( 14% YOY inspite of Glaxo brands addition ) , Britannia ( 11% YOY) …

The key part is how crisis has been used by ITC to gain market share & mind share in Personal Care and Noodles category .

The another gem that has emerged is Paper division … Inspite of loss of paper print and stationery business - The division performance is very interesting … It is getting some serious structural adv by improving access to Local Low cost Raw Material and tailwind toward paper packing from plastic packaging …

Product Mix is an issue .

Top end bars , restaurants and events are closed or semi operational wherein both liquor and top end Cig brands are consumed … This has higher impact on ITC vs VST kind of product Mix . You can see impact on United spirits and Breweries sales

Hence ITC has launched as per Investor ppt lot of lower end brands … This will help you maintain revenue , but at lower Margins …

But the good part is ITC in second quarter has been able to deliver near flat Cig revenue inspite of loss of sales due to closure of major HoReCa chains … This might help them when HoReCa reopens

In my limited understanding, we need to deduct excise duty on cost from Cigarette revenue. Post GST, Cigarette is one of few item which carry excise. There was major jump in excise duty payment, which was passed on form of higher sales realisation. I have noticed same in VST industries as well. Find enclosed my wokring for Cigarette business. While PBIT margins are maintained at around 75%, same was lower due decline in Cigarette revenue.

My takeaway from ITC Q2FY21 results is one slide:

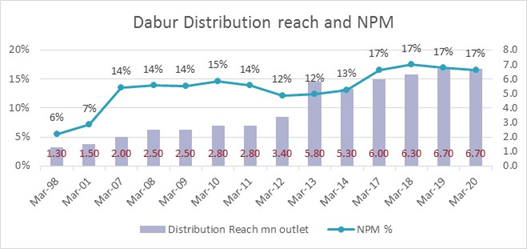

I am also enclosing relationship in NPM and Retail reach sourced from annual report of Dabur India over the years. Not that increase in margin in Dabur was only due to increase in distribution reach, nevertheless, high penetration in distribution do provide good operating leverage to the company for sure.

Please note that during FY1998 to FY2001, the net profit margin increase only 100 bps for Dabur, however same increased to 14% by FY2007 (which was 700 bps) over next 6 years. Ideally, one would like to have yearwise information, but same was not avilable in annual report. I have collected whatever was available and represented in graph. This is my investment thesis in ITC (non-cigarette FMCG business revenue and margin enhancement).

The issue here is more that just excise pass on …otherwise in Q1 we would have seen Cig PBIT/ Sales of 75% as ITC has not taken significant prices hikes in Q2

The Metro market and HORECA channel has opened in some fashion in Q2 vs Q1 that might have improved Product Mix Margin in Q2 , but still it is not at its historical favorable mix

In Q3 we will see as Hotels , events open up more and Metros like Bangalore , Mumbai etc are fully open … Product Mix improves further and hence leading to better EBIT margin

Thanks for highlighting this aspect. Pls correct me if wrong, so cigarette revenues are in essence down by almost 16% rather than 4 if we remove excise from revenues? True picture would come from volumes…could not find details on volume decline overall and sub categories…anyone has data in volumes?

Considering how sales of United Breweries and even United spirits were impacted, a 16% drop is revenues is not alarming but point is , is cigarettes and liquor comparable based on how they are distributed and consumed? Thoughts welcome

I have gone through the report but unable to find anything related to the recently acquired brand Sunrise foods deal, how did this segment performed ?

Q2 results state:

" During the quarter ended 30th September, 2020, 1,28,05,310 Ordinary Shares of 1/- each were issued and allotted under the Company’s Employee

Stock Option Schemes. Consequently, the issued and paid-up Share Capital of the Company as on 30th September, 2020 stands increased to

1230,50,36,551/-. "

What would be the impact of such dilution?

AXIS Research Report

ITC-Ltd-Q2FY21-RU-09112020.pdf (932.4 KB)