Transfer to General reserve have no impact on cash flow. It is just a reserve appropriation. The balances in general reserve is a part of share holders fund - company can even pay dividends out of this reserve.

Additionally all reserves are generally profit appropriations(other than security premiums received which is direct cash accrual received on issue of shares etc) and can be used for payment of dividends(debenture redemption reserve, capital redemption reserve etc are exceptions to this, and are created for specific purposes and cannot be used for payment of dividend). Hope you find this helpful!

Out of curiosity - what is stopping ITC from de-merging and listing its hotel, paper and FMCG businesses? Is their a regulation/ share holder agreement which is stopping the company from listing these business stand alone?

If ITC demerges and list these as stand alone entities - that would be one among India’s biggest value unlocking exercise. If any of you have access to the board of ITC - you should raise this question. Currently the foreign investors are not allowed to invest additionally into ITC due to its presence in cigarette business and this can easily be circumvented by a demerging exercise. This exercise will additionally give opportunity to the shareholders to decide which business they should stick to and which one to exist. This will additionally create a new set of investors who have stayed away from this due to its presence in cigarette business.

Q 1) If General reserve is not a cash transaction , then how can General reserve be used to pay dividends, this confuses me a lot. As HUL used thier general reserve of around 2400 Cr and moved to P&L statement.

I have read a lot of people complain about this and I would like to add my thoughts on this topic.

While there is some merit in the argument that a de-merger would help, I agree with the management that ITC is much stronger united and it should remain that way. The reason for this is -

The cigarette business is the cash cow for ITC. Most of the PAT and all of the CFO is generated from it. The money from there is used to grow the FMCG and other businesses. Currently FMCG is still in a growth phase where it will require sufficient capital for marketing as well as acquisitions. Being together will give ITC the strength to fight competitors as well as acquire them if needed. This is a unique advantage which only ITC has and it doesn’t make sense to take that away right now. There could be scenarios in the future where heavy capital is required to build a new product and the high CFO will come in handy then.

ITC has also invested heavily in backward integration and that has provided it a source of cheaper raw materials. Such an exercise would not be possible without the cash from the cigarette division and the existence of a united agri division.

The FMCG business is still growing and the margins are yet to expand. At such a critical stage, it would be unwise to make it a standalone entity. Let’s not forget that the FMCG division exists only because of the cigarette business

The focus of the management should be to grow their revenues and bottom line. If these things continue to happen, the PE re-rating will happen eventually. The de-merger of FMCG is a question to ponder when the margins are in double digits and it is self sufficient. Until then, a united ITC is a stronger ITC.

“The lockdown did help in the sense that the brands I like were not available easily, and so I was less likely to buy smokes.” With the lockdown’s restricted supply of cigarettes, smokers went into withdrawal. In many families, people would not smoke at home out of a sense of respect for their elders, or because of the absence of social cues of parties and post-lunch tea breaks with colleagues.

Quite a few will permanently give up smoking during Covid-19. And given continuing social distancing norms for quite some time and lack of gathering/partying, there will be limited new additions.

You have to remember that even nascent FMCG companies building brands and with low margins and huge debt are priced at PEs above 30 to 50 and higher. The risks involved in buying those companies are huge… what if their brands don’t end up being built? What if their cashflows cause issue and lead to overwhelming debt? What if their margins don’t improve? With ITC they’ve already built huge brands and are now the 3rd biggest in India for FMCG other revenue. Their margins are improving every year. There is no worry about debt whatsoever… infact if ITC goes bankrupt it will be because world war 3 has started. The cigarette business is a dying business… taxes/health consciousness etc are are universally accepted to destroy the tobacco industry…however, even if the profits from cigarettes drop by half ITC will still be better placed than other FMCG companies due to having some sort of a cash cow to dip in for any emergency expenses and brand building. At the end of the day if anyone is buying it as a cigarette company then news like this should panic them. For the rest of us this is just a long term buying opportunity we can SIP in safely for a few years at a low PE of 15 or so

which already covers the loss in profitability from cigarettes but hasn’t yet accounted for the increase in profitability from Fmcg others. There is an opportunity cost of missing out on other stocks with tailwinds while investing here. That’s the only main issue I find. However, capital protection, a good dividend yield(even with lower cigarette profits) for the next few years seems a good investment with the current unsure situation with the markets due to Corona while we patiently wait for a re rating in a few years. Also, I’ve learnt you can’t time the market. The re rating could happen anytime…look at reliance. All it takes is a margin increase in a quarter(with their backward integration it could happen faster than normal) /inorganic growth with a few company acquisitions (they have huge amounts of cash in waiting) and it could happen. Entering at the ground floor for what looks like a value investment opportunity ie low downside, huge upside… is something we rarely get with safe large caps.

All such companies clearly understand what they are doing. These are just tactics to pull consumer base and make Inroads in segments dominated by competitor. Until they loose legal battle, work is already done.

Above is just my assessment and I maybe wrong.

Some actual good news for tobacco maybe? Im not sure how to interpret this for ITC.

Edit: just checked and when FDI was banned on November 18 2016 the market reacted badly and ITC fell By about 10 percent in the following days and the last time there was some positive progress ie discussions about allowing FDI on April 11 2018 ITC rose the next few days by about 10 percent. Don’t want to make assumptions though. This was the first announcement of a possible ban back in Jan 2018… ITC fell that day too:

Edit: Done a bit more studying. Few things that popped up

BAT wanted to buy more stake in ITC but weren’t allowed to. This may allow them too?

Foreign companies know that their cigarettes are being sold here illegally and don’t stop it since they benefit. By doing this maybe they could start setting up here itself and selling hence maybe it’s a step in the right direction to curb illegal cigarettes?

Could be a signal it’s safe to invest in cigarette companies since this shows the government isn’t going to ban cigarettes anytime soon… infact it shows the opposite?

Could improve exports and ITC agro could benefit from it?

Trying to figure it out. But I’m not sure. Could be bad for ITC due to increased competition. But increased legal competition and less illegal could be a good thing?

In my limited reading from release on your link, I think this is more for exports of Tobacco and does not at least in my reading, providing any information about relaxation in FDI in cigarette sector. Secondly, in agri business, ITC also involved in tobacco exports. So it may mean more competition from other players in case modifications are allowed. In my view, in case this approved, it would have marginal negative impact, too the extent competition increase from export based tobacco firms.

Discl: my view may be biased as ITC is now my largest holding and I have added during last one month. Not a SEBI registered investor, not recommending investment.

I think we need to see growth on advertisement also during period which is also function of product portfolio. Since no one is likely to increase usage of shampoo, washing power and hair colour; the advertisment spending on such categories ad spendings would report muted growth.

If you read data in details, we find that 3 of top 5 advertisement spender on television have shown negative volume growth while only RB and ITC have shown positive growth.

Company

Jun-20

Jul-20

Aug-20

July/June %

Aug/July %

Aug/June %

HLL

257

280

206

9%

-26%

-20%

Reckitt Benckiser

63

91

137

44%

51%

117%

P&G

33

29

30

-12%

3%

-9%

Godrej Consumer

27

26

22

-4%

-15%

-19%

ITC

23

25

26

9%

4%

13%

Partially, it would also attribute to products as RB has Dettol and toilet cleaner which were expected show better growth during lock down and limited mobility, followed with ITC (with savlon, sunfeast, bingo and ashirwad). At least, I am not able to read much positive or negative from this article. We also need to note that TV advertisement account for around 45% advertisement budget while Print/Film/Digital /Radio/ OOH account for balance. So extending just one part (although largest) may not lead us to any meaningful insight in my view.

Appreciate your efforts to share relevant link along with your view. Thanks for that.

Discl: My largest holding, have purchased share in last 30 days, Not a SEBI registered advisor, Not recommending investment in the company. My view may be biased due to my holding.

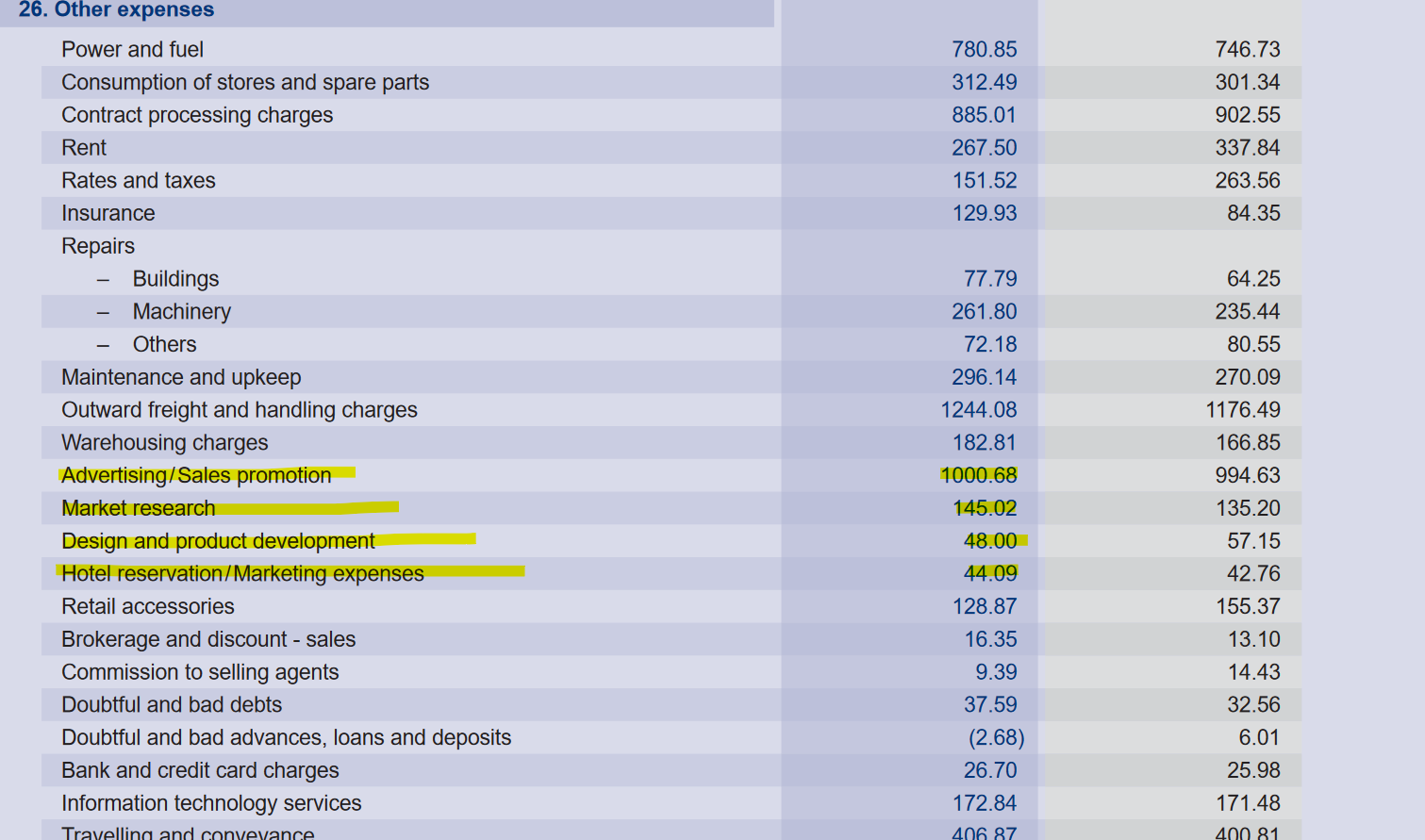

I have a basic question with respect to the amount that is spent for Marketing and Advertising. From FY20 annual report, I found that this is roughly ~1200 cr ?

Now if we exclude the cigarette business and assume that all of this marketing is spent toward M&A for FMCG then it would mean that M&A/FMCG sales would be ~ 10% for FY2020. This seems to be in line with what HUL & Marico are spending today. Is this assumption correct? If so, going further what should the strategy for ITC to gain further market share?

This is ITC’s chart from 1990s; they were growing well till 2015; Then this fall happened; now what has changed since 2015 is nothing : FMCG is growing leaps and bounds, reduced captial allocation on low ROE businesses like hotels,paper etc and now more focus on FMCG (with the great scope for margin improvement- currently 2-3% for ITC vs 15 to 20% for nestle)…i think more than anything, it is the patience and temparament which is the key in ITC.

I was not part of that investing journey but people would have similar views for Unilever as well when it went sideways for good 7 to 10 yrs.people cite that example quite often .

It’s not that cigarette business was growing well between 2005 to 2015- it was a mature business then also.If u think cigarette business as well in today’s context, legal ciggies are just 10% of overall pie;So, for an optimistic ITC shareholder, there is still light there at the end of the tunnel

One more important point: change of guard: Sanjeev puri may be different from YC Deveshwar…looks like he is FMCG bull as I could make out from his interviews.Look what happened to Tata consumers with Sunil D’Souza and to Britannia with Varun Berry.

Disclaimer: May be biased since ITC is 6% of my portfolio.

Please let me know if the post is redundant as there is a lot of similar debate often in ITC thread

After reading your writeup, I bumped on two articles :

&

Interestingly both of them talks about ITC as more of a Cig business, as other business lines have yet to generate substantial Profits.

Money they have put in other business segments in last decade is huge. May be the reason of slow growth.

After reading your analysis & the above article, ITC would be considered a Sin Stock because of Cig. business and I think, I would consider & have it in my portfolio as Dividend Stock then a growth story for the time being.