Source - ITC Annual Report

1 Like

ITC has out paced it’s competitors in the terms of growth and will soon be the leading FMCG brand in India

2 Likes

I feel now they’re also beginning to realise thr undervaluation and mrktg themselves accordingly. Every second day thr’s news regarding ITC’s FMCG plans, products etc. etc. ( Doosro se pehle apni izzat khud karo…  )

)

Dont knw how far this impact vl be, bt value investors wd hv preferred longer period of undervaluation to acquire quietly.

Disc :- Invested.

1 Like

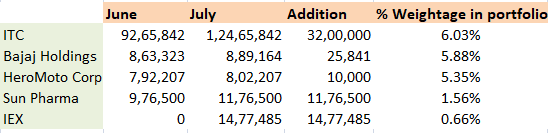

PPFAS Long term Value Fund update:

- Added 3,200,000 shares of ITC, second largest domestic holding in their portfolio, (6.03% weightage)

4 Likes

Hi,

ITC pretty rapidly increasing their non tobacco business.

Another article signifying that.

Thanks,

Deb

The Black horse in the stable which you missed out is agri business, and e choupal , with change in APMC act and corp farming, ITC is best geared to lead the race

3 Likes

~~ this is like a permanent problem with ITC…everytime things starting to look normalised…there is some additional cess

Extract from above article…Center is likely to push for GST compliance, collections and widening base…Delhi has acted on it…

According to Manish Sisodia, deputy chief minister and finance minister, nine sectors namely auto, electronics, e-commerce, insurance, pharma, financial services, consulting, security and healthcare had not been affected by the COVID-19 pandemic.

Also read: Delhi govt sends notices to 5,584 cos for not filing GST returns

Sisodia has written to the GST department that around 935 companies under these nine sectors have paid zero tax and 2,017 companies have paid 50 percent tax. He said the Delhi government will strictly scrutinize the reasons behind not filing tax returns by these companies from unaffected sectors.

He has asked the companies to immediately deposit the taxes and warned of stringent action against the companies which failed to do so.

Thus, Centre feels, similar exercise can be conducted by all states, individually which can help in augmenting state revenue collections, which can help reduce the burden on the compensation requirements.

I think if you are a long term serious holder of ITC you have to just expect tax increases and use it as your yearly method to add more in dips. I, for one, am buying it for its future in FMCG others and agro business. Cigarettes have such huge margins and price flexibility that ITC have managed to increase their revenue and profits almost every year even with continuous government interference. Plus they’ve finished most of their capex and have enough cash flows(more than enough) for whatever expenses and spends and acquisitions they need to do. So If there is an increase in tax(not even confirmed may I add) all I can see it doing is stalling dividend yield for some time (its already high anyway) but in the long run all everyone is looking at is FMCG Others margins and growth… and if anything the continuous taxation will force ITC to maybe even pursue inorganic growth to get FMCG others to start taking most of the load off cigarettes and make growing it as quick as possible their main priority and could lead to a faster re rating.

Note: please flag if deemed an opinion piece or inappropriate. This is a reply to the post regards the GST article above

4 Likes

@Malkd Thanks for your feedback. Will look deeper into the agri and paper business. Although the fmcg business is average now but if you see my valuation i predict a growth in both its margins and return on invested capital. I expect it to become an established fmcg player. Thanks again.

1 Like

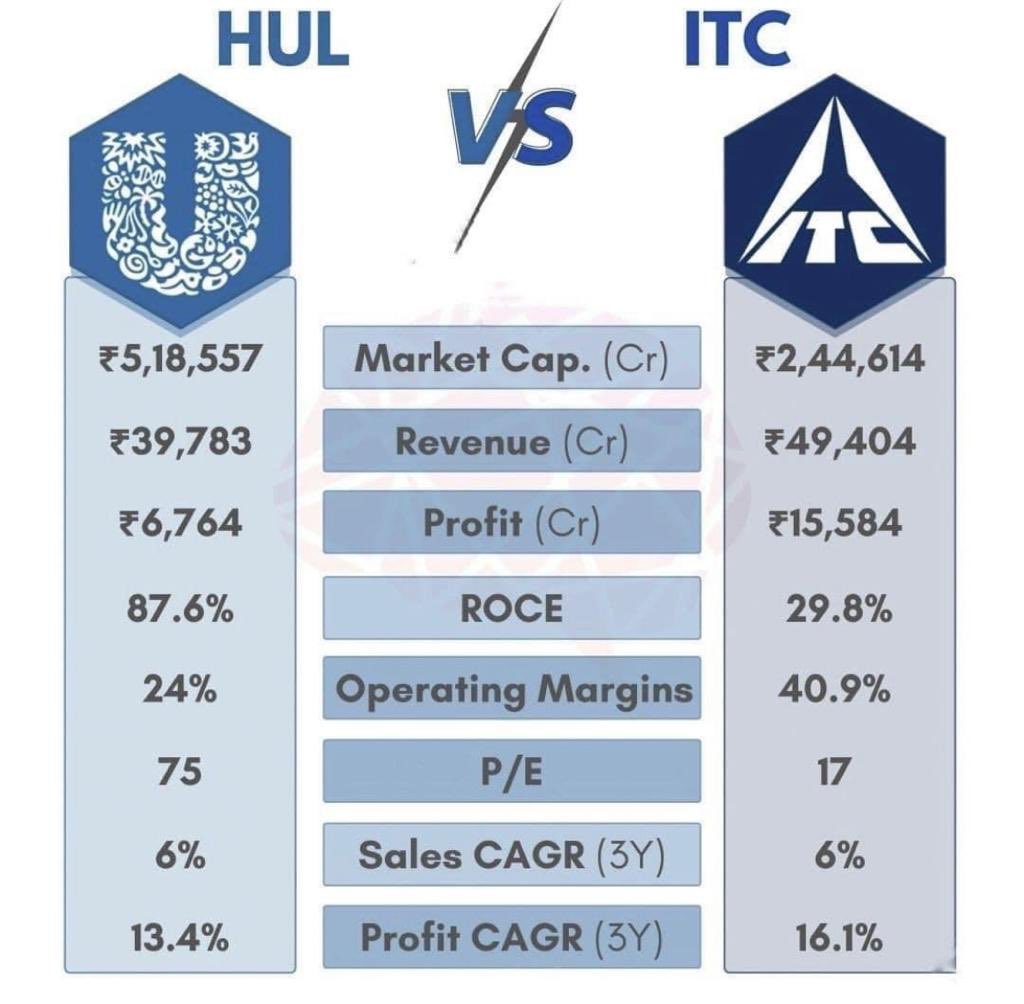

With all due respect to your views, I am surprised by seeing above line. ITC, infact as on today, is already an established FMCG company. I am not saying this because I am an investor in ITC. I am saying this because I have seen this homegrown FMCG company grow their brands, most of which I have been using since long and have complete trust on when I buy them. It (along with the likes of Tata Consumer) have the capability to take on top MNC FMCGs in times to come - not only in India but globally as well.

So, yes - ITC is already an established FMCG player, not highly profitable in FMCG for obvious known reasons.

Disc: Hold Tata Consumer since long term in core portfolio. ITC is a new addition.

3 Likes

This topic is temporarily closed for at least 4 hours due to a large number of community flags.

This topic was automatically opened after 16 hours.

ITC thread is constantly getting locked, some directions and things to ponder

Please avoid one liners which add no value to the discussion. If you have to put up anything meaningful even on small things post with relevant data and source of data. There are lots of garbage being piled up. These kind of posts disturb the smooth flow of reading useful stuff as these one and two liners tend to clutter the threads.

If one is interested in a company for purpose of investment, read the thread completely before posting any comments. Most of the times, the concern and query is already addressed earlier. If not, and if you feel your post adds value to the thread, then only add the post.

At valuepickr, we encourage democratic participation from all forum members, new and old. But whatever we put up, whether its a piece of information news or a query, it should be value accretive to you and others. Otherwise it holds no meaning.

PS:

I just (re)posted what @hitesh2710 has written in other thread with some modifications. Let us learn and earn together.

19 Likes

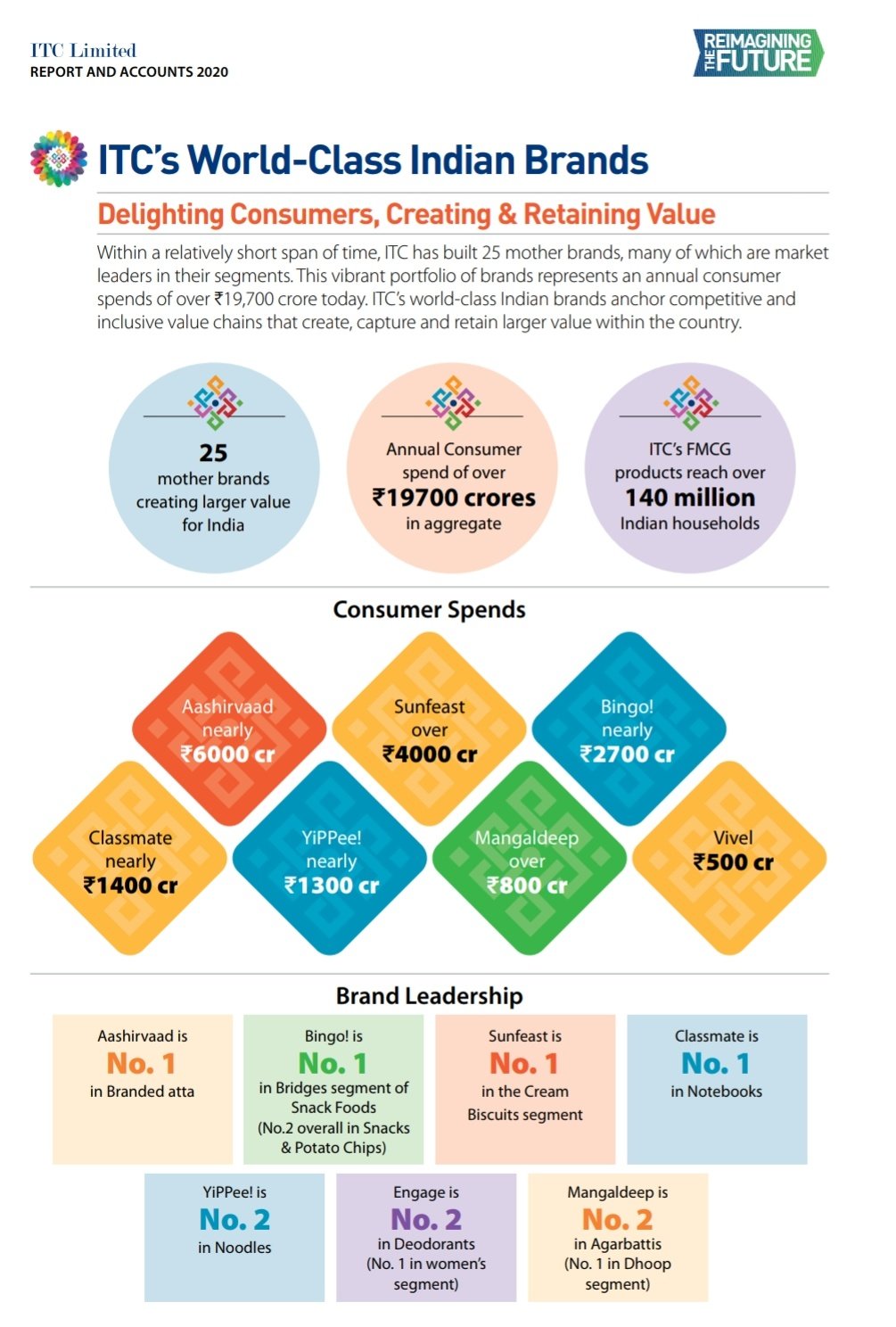

Hi Amit,

I have one doubt here in the FMCG part.

So revenue from FMCG business is 13000 cr. But when we look into brand wise revenue it is more than 13000 crore.

so total is 6000+4000+3000+1500+1300+800+500 = 17100

So what I am missing here.?

Thanks,

Deb

Good question, 13000 Cr is revenue for ITC, the numbers projected per brand totalling 17100 Cr, is the final value of the products sold to customers.

The difference goes to the distributers and retailers.

8 Likes

it’s a classic case of Mr market telling us one thing and our own value investing philosophies telling us another.

guess we should allocate to both.

4 Likes

Suggestions for increasing tax burden on Tobacco products (esp. Bidis and Cigarettes) appearing in Media:

The more they increase taxes on legal cigarettes the more the price increases and more people shift to the cheaper illegal cigarettes. So overall the government ends up collecting less than they would if the taxes on legal cigarettes were lower. If anything the government should impose stringent measures to prevent illegal cigarettes being imported and sold but for some reason they just take the easy way out and increase taxes. At some point they’ll realise this hopefully. What I’ve never understood is…

- How are the stats regarding illegal cigarettes even present considering they are illegal. Keep reading about how sales of those are increasing at X growth etc… If this can be calculated then I’m sure it can be tracked and stopped too. Unless this whole illegal cigarettes thread is a red herring . Can someone explain how they calculate this? Is it just by doing a reverse calculation on less legal cigarettes being consumed equals more illegal being consumed(taking the probably inaccurate assumption that overall cigarette demand has not dropped over the past few years)?

- Also right now the government benefits from ITC due to dividends and taxes. Once their stake is sold will their priority towards ITC change? For eg just last year the entire vaping industry got destroyed to protect their interest in ITC and cigarettes so just wondering what would happen if they start collecting less tax overall and less dividends too from the same.

Note: Honest questions. Flag and delete if inappropriate

2 Likes