It is barely 1% of ITC. Not very bright future as most of the top executives earlier were from tobacco business and not sure how aggressively they can drive infotech business.

3 Likes

Already ITC is known for their capital misallocation.Its not in the shareholders interest when they are investing money out of their core business.IT,hotel etc are not their core business.FMCG and cigarettes must be their sole focus.Investment in IT should be used for improving operations and efficiencies in FMCG and cigarattes rather than trying to develop it as separate vertical.

3 Likes

ITC is already runnning numerous verticals. It has the penetration and reach. Why should it not Invest in and grow ITC infotech? even at 1% of ITC pie, it is bigger than many mid cap IT companies which are growing at a hefty pace and providing a good dividend.

Also, ITC infotech can be a supplementary supporter of other businesses leading to better efficiencies within the organization.

1 Like

Yes ITC is running numerous verticals,thats why i said ITC is known for capital misallocation and that is one of the reasons I believe ITC stock has been under performing.Any company must focus on business what it is good at and outsource jobs where others are better than you.Companies cant be superstar who wins all the sectors.If company is trying that its nothing but burning away shareholders money.

One of the recent good decision taken by management is to return 80% of free cash to shareholders.That means lesser cash available for reinvestment which will force the management to make prudent capital allocation rather than trying hands on everything out there.

12 Likes

When to invest\diverse in multiple businesses and when to concentrate and focus on profitability should be dependent on business cycle and management’s discretion. At certain times, its only logical to diversify, allocate capital to certain different business propositions. Following this is the call on which businesses to grow and which ones to be milked as cash cows.

It amazes me why ITC’s diversification is seen as capital misallocation and for other trendy cos. its labelled as ‘disruptive’ or ‘visionary’. E.g. The great Amazon has tried its hand and failed in many businesses, to get few big winners they had to try few different things. Its just the nature of things that 1 or 2 successful ideas will come to dominate a cos. earnings and profits. As long as management is intelligently trying out these things, no harm in that.

In fact, an opposite and disturbing view seen in this market has been that few cos. which were not allocating capital at all and were hoarding investments in debt mutual funds have got those marked down. So in the hindsight, that didn’t seem a prudent capital allocation to me either.

Disc. Invested in both ITC and Amazon. My views maybe biased.

12 Likes

Similarly, with Reliance. Whenever it enters a new sector, people laud them. It is not about diversification. It is about execution. ITC may have failed in some of it’s ventures, that doesn’t mean they are not capable. We are all praising the FMCG sector in which ITC diversified into.

3 Likes

Totally Agreed.

Before these posts get marked for being bit off-topic, the only point of view that I wanted to share was to not look at diversification as mis-step always. Some cos. do diversify and diversify for good. Yes, but the very act of diversifying throws up occasional failures from time-to-time. So, these have to be taken in stride by long-term investors. As Buffett puts it - “Think of it as a dividend check that got lost in mail”

The difference between ITC and reliance is that reliance has Mukesh ambani who sets ambitious short term(2-3 years) and long term targets. ITC leaders lack ambitions to speak out their short term targets and hence market is not believing in them.

Disc:: Invested in ITC

1 Like

My objection is not to ITC’s diversification itself but the manner in which they are diversifying. They already are into more fmcg categories than any pure play fmcg company in India (not sure but can’t think of another company which is into matches, stationery, dairy products, coffee, milk, chocolates, personal care, incense sticks, juices, floor cleaner, gum and candy, pre cooked food, atta, noodles, biscuits, salty snacks…).

Even before consolidating their position in a category, they are eager to enter into new categories, eg they supply to lacs of pan shops throughout the country but you wouldn’t find their gum, candy or salty snacks at any of these shops.

Isn’t the range already too diversified esp when you consider that fmcg (excluding cig) is itself a diversification.

My only grouse with ITC. It looks a bit like a portfolio with a hundred stocks AND counting. Would love to hear them say that they are not going to enter into new categories and focus on existing ones.

3 Likes

I dont know why everyone is keep saying ITC is misallocating the capital with out any numbers to substantiate the argument. @ashwinidamani had done the quantification and shared in this thread.

ITC has very well interconnected business. Paper business was started as a backward integration for producing cigarette packages. Agri business was developed because they need to deal with farmer to get tobacco leafs for cigarettes. Hotel business was started to gain some foreign exchange. In 2001 packaged food was started ( ready to eat gourmet food) because chefs at their restaurent wanted it, and ITC expanded it. Actually most of the master chef FMCG products comes from ITC restaurent chefs. Infotech was started to serve ITC IT needs as the congloromate was big enough. Of course each business took off and shaped in to a different business with more products when the opportunity rose as any other company would do. if you read ITC history one will realise how each business was started and rational behind it.

Requesting everyone to add value, information, number crunching, products and its opportunity size.

Anyone followed up the ICML construction status recently ? I was away due to personal reasons and did not do any due diligence on it. They had 11 operational I think and others were at different stages. This is very crucial as they would drastically increase the margin for FMCG products.

11 Likes

In 1975, the Company launched its Hotels business with the acquisition of a hotel in Chennai which was rechristened ‘ITC-Welcomgroup Hotel Chola’ (now renamed My Fortune, Chennai). The objective of ITC’s entry into the hotels business was rooted in the concept of creating value for the nation. ITC chose the Hotels business for its potential to earn high levels of foreign exchange, create tourism infrastructure and generate large scale direct and indirect employment. Since then ITC’s Hotels business has grown to occupy a position of leadership, with over 100 owned and managed properties spread across India under four brands namely, ITC Hotels - Luxury Collection, WelcomHotels, Fortune Hotels and WelcomHeritage.

3 Likes

Sorry to sweep in the conservation, but as shareholders, we should all trust the management and most importantly, their decisions.

Just because the stock hasn’t performed for a couple of years, doesn’t mean that the management is incompetent and/or misallocating shareholder’s money.

Also, about misallocation of capital towards FMCG etc, I guess the management knows best about which vertical could be scaled the largest and become most profitable.

We all have seen in how in a decade or so, ITC’s FMCG is competing with the largest names in the industry. This wouldn’t have been possible if the mgmt didn’t know what they were doing.

They are a cash-super-rich company, with BAT and GoI as shareholders, so creating shareholder value must be their priority focus, even if it takes a decade.

Or, you know, maybe they are trying to take the “weak hands” for ride.

Warren Buffett’s quote comes to mind - "No matter how great the talent or efforts, some things just take time. You can’t produce a baby in one month by getting nine women pregnant.”

9 Likes

The reasons I can think of are the following:

-

They are big enough to consolidate in select segments and become top 3 in those segments and still have enough profits from FMCG to become a FMCG-profit-heavy company. To become a FMCG-profit-heavy company of ITC’s size you want them to become top three in many categories.

-

ITC is a relatively new entrant to FMCG and built most brands from scratch. Brand building in FMCG takes a lot of time and not all ventures become successful. So, it makes sense to go all out in many categories and try to make brands in each. Some will become successful, some will be less successful and some will not succeed at all. So, at the end of sustained brand building tenure (still ongoing), they are expected to end up with a decent number of good brands.

.

Now, most companies which started with such aggression have not succeeded, some because of leverage-fueled aggression and some because of the lack of brand building (Patanjali). However, ITC’s aggression were funded through internal accruals and they are continuing to build brands with enough persistence.

18 Likes

The important point which nobdy’s analysis ever addresses is this : -

What will stop the company to increase its FMCG margins in near future?

And the answer to this question is key to evaluating whether ITC is an investment-worthy candidate or not.

I’ve seen very brilliant analysis posts ( including the above one) which have dissected ITC’s business segments beautifully. In fact, these reports are suffice to provide you a considerable investment thesis for ITC. Commendable job

But the above question is where I find every thesis comes up short.

4 Likes

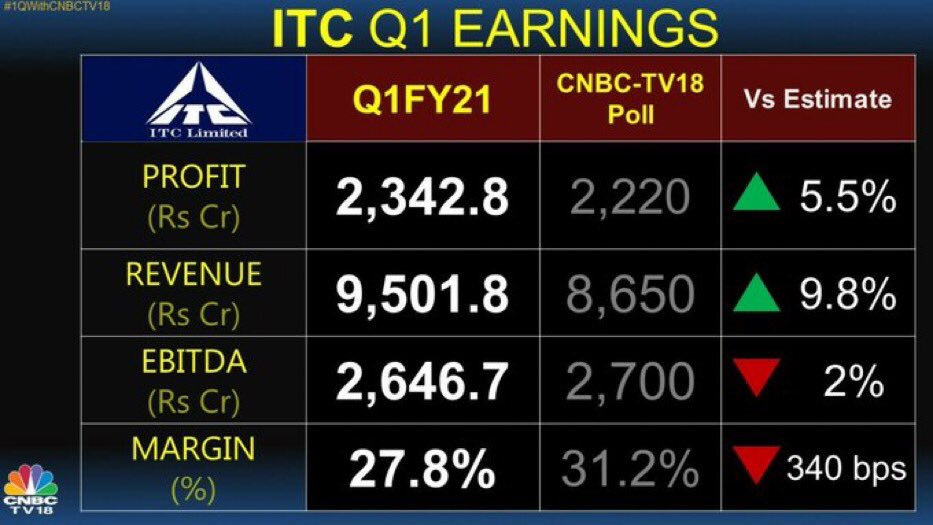

Results are out. Overall profits and revenue are down as expected due to hotels and the lockdown affecting cigarettes. Paper and packaging down too. However, FMCG Others up and Agri up which is all I was looking for. Can see the market reacting positive due to this. Results here:

a2da0a20-a0c0-4f76-a5df-014cdd09f474.pdf (611.0 KB)

2 Likes

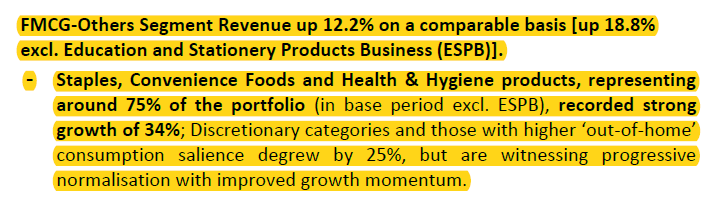

For me, highlighted statement was key highlight of Q1FY21 results:

Other details are provided in press release related to FMCG other business are as under:

Aashirward: Significant value and volume growth

Yippee Noodle: Substantial growth driven by “at Home” consumption

Bingo: Growth slow down during Lockdown due to limited mobility, but normalised after lockdown lifted

Sunfeast Biscuit and Cakes: Robust growth driven by Surge “At home” consumption

Chocolate and Confectionery: Severely impacted due to subdued demand for discretionary products, now witnessing progressive normaalisation

Engage: Witness a tepid quarter due to decline in demand

Savlon and Fiama handwash: Production increased multifold, Perfume planin HP was repurposed in quick time to manufacture hand sanitizer and increased demand for Savlon. Several new launch in Savlon family:

Nimyle floor cleaner: Strengthen market leadership in Orissa and West bengal

Nimwash: New vegetable wash product received encouraging response

Stationery/Agarbatti/Match box adversely affected by Lockdown

Refer to enclosed release for other segments details:

https://www.bseindia.com/corporates/anndet_new.aspx?newsid=0281edc2-86fd-4f31-9220-226f5d7a7bef

Discl: Among my Top 3 holdings. My view may be biased due to my holding, Not A SEBI registered advisor, Not giving any recommendation in stock.

18 Likes

Standalone Financial Results for the Quarter ended 30th June, 2020 - Media Statement

7a26b0d7-29f8-489d-bd00-862ba250ed6b.pdf (1.1 MB)

Unaudited Financial Results for the Quarter ended 30th June. 2020

a2da0a20-a0c0-4f76-a5df-014cdd09f474.pdf (611.0 KB)

2 Likes

True

Hotels , Education/ Stationeries were hit card

Classmate is 1500 crore brand and chunk of sales happens in Apr-jun quarter …

Inspite of this they have done pretty good in FMCG others

2 Likes

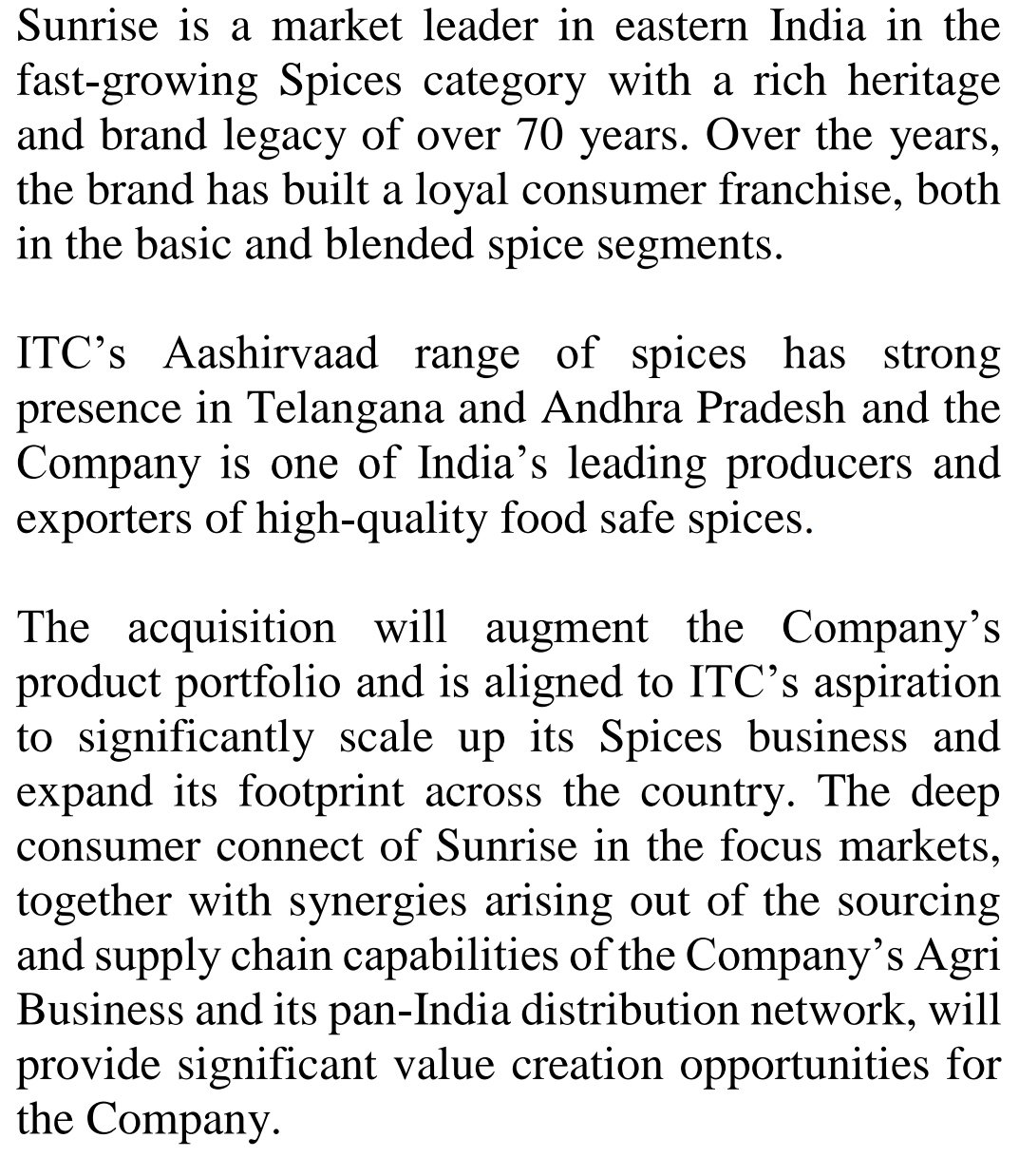

ITC completes 100% acquisition of Sunrise Foods.

The upfront consideration is 2,150 Crores. With a contingent consideration not exceeding 150 Crores if Sunrise achieve certain milestones within 2 years.

ITC aims to be a FMCG giant by 2030 and it’s a step in that direction.

6 Likes