Coke has a unique and closely guarded secret to its taste which its competitors cant reproduce(dont know about wrigleys).But that doesn’t hold for biscuits ,juice etc.

People go to shop for buying juice not real juice

People go to shop for buying biscuits not Britannia biscuits.

When buying books getting a book is priority rather than Classmates

For pooja getting agarbatti is important part not getting mangaldeep

but

If you are buying Coke you get a bottle of coke or nothing

I agree your cult brands theory to some extend like Maggi whose taste cant be reproduced by competitors

When you are bombarded with options from multiple brands as of now mostly you go towards non itc brands because of the brand image existing in mind.But that will change for the next generation (with all these ads in cartoon channels).

Efficient and country wide distribution channels also helps.

If you are saying that biscuits, notebooks, juice are very easily substituted, then these would be commodities. If this is the case then, ITC will never be able to command margins and their advertising money will also go in vain.

I do not agree with this thesis. Let me illustrate: There is a company that sells noodles in India and there are concerns over it related to it causing health issues (poisonous lead). And, the company has to stop selling this noodle product. Yet, its competitors are not able to permanently take away market share from the leading brand. And, soon the leading brand solves its health issues and the customers are ready to buy. I am sure that you can guess which brands I am talking about.

Yes, I agree that there are some commodity like products eg. Agarbatti but I doubt that these will ever contribute meaningfully to their bottomline.

Again, I am reiterating my thesis that ITC will remain a cigarette company unless it understands how to create superior products and not just roll out any “me too” products and label them as FMCG. Brand differentiation and creation is the only thing that can increase FMCG’s contribution to their bottom-line.

All ITC FMCG verticals are like startups. The mandate is to capture market and mind share with high quality products. Profits would always follow later.

The VC who does this unlimited funding is cigarette business.

No other FMCG company has invested for future like ITC.

Till 2017, ITC was ranked amongst top in long term consistent compounders. Nobody was then questioning it’s relatively high PE. In the previous 25 years, it has outperformed HUL by 10% ( ITC CAGR 19% versus HUL’s 9%). It was best Nifty performer in 2013.

ITC has created brands which are now very much recognisable in the market.

I strongly disagree with you regarding second rated products produced by ITC.

From my childhood I used to buy maggie (Eventhough topramen was in the shelf). Still top ramen is not able to garner the market share which yippee garnered in this short time. (Reason which i understood in lockdown time, I tasted yippee for first time since I thought nothing will equal maggie in my 27 years of life. Frankly speaking noodles(only noodle part) are far superior compared to maggie. But masala is personal preference (if you like tomato taste, you will like yippee). I didnt become a fully yippee fan. Now thinking of buying both maggie and yippee because i used to get bored of maggie/yippee if i consume long time) . You can argue that its your personal taste/biased opinion. Yippee capturing market share is a testament to this opinion.

In cream biscuits segment, britannia and parle missed the bus( Dark fantasy). They became the copycats like Hide & seek choco rolls and britannia chocolush. I accept that mom magic is not as good as good day.

I never knew about navneet notebooks. But for my fair copy I always used to buy classmate or TNPL. Classmate is costly yet its quality is really good.

Aashirvad: People were saying they are not able to get aashirvad MP atta in lockdown times. Brands are nothing but consistency. Any number of times I buy atta it should have same taste and quality. Thats why people long for aashirvad atta. So ITC can charge few extrabucks for that (as buffett says).

Wheat is commodity yet they created a brand out of it. Pillsbury not able to do it which aashirvad did.

Consistency is maintained by backward integration like e-choupal.

I can cite recent example like savlon disinfectant spray which is huge hit compared lifebuoy spray ( savlon gave more quantity than lifebuoy).

Finally ITC is marketing as truly indian company which HUL and neslte cant ( BAT is 30% but indians own 70%)

Conclusion: ITC products are of very good quality. They are no 1 in new segments/products they enter. Merely saying their quality is second rated is not in good taste. I accept that fabelle cant replace the cadbury, mom magic not the good day. Savlon handwash - lifebuoy. When market gives them a chance like disinfectant spray they capture the whole market share (https://www.amazon.in/Savlon-Surface-Disinfectant-Spray-Surfaces/dp/B086WQK1GK). Yippee need not replace maggie but it will become complementary.

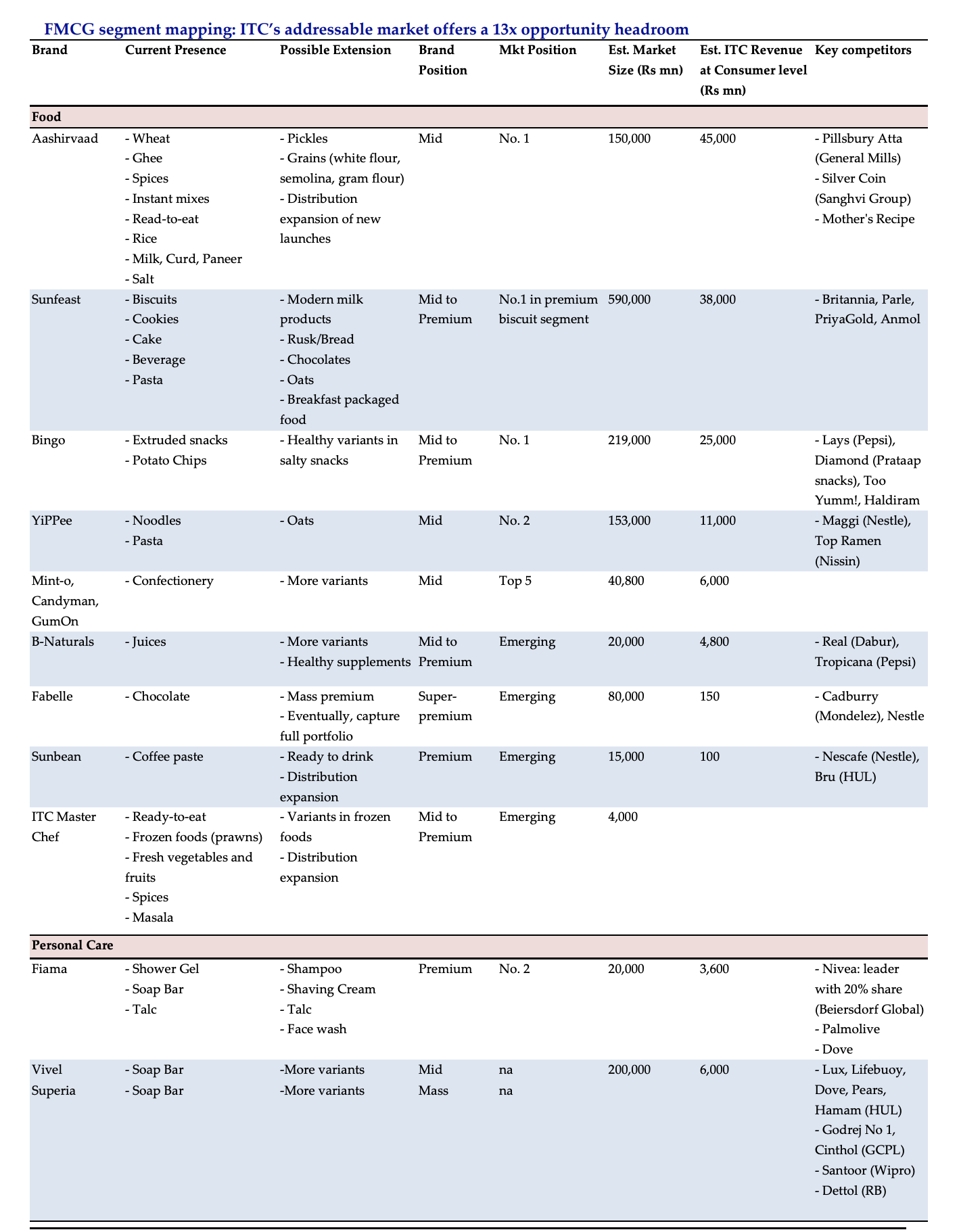

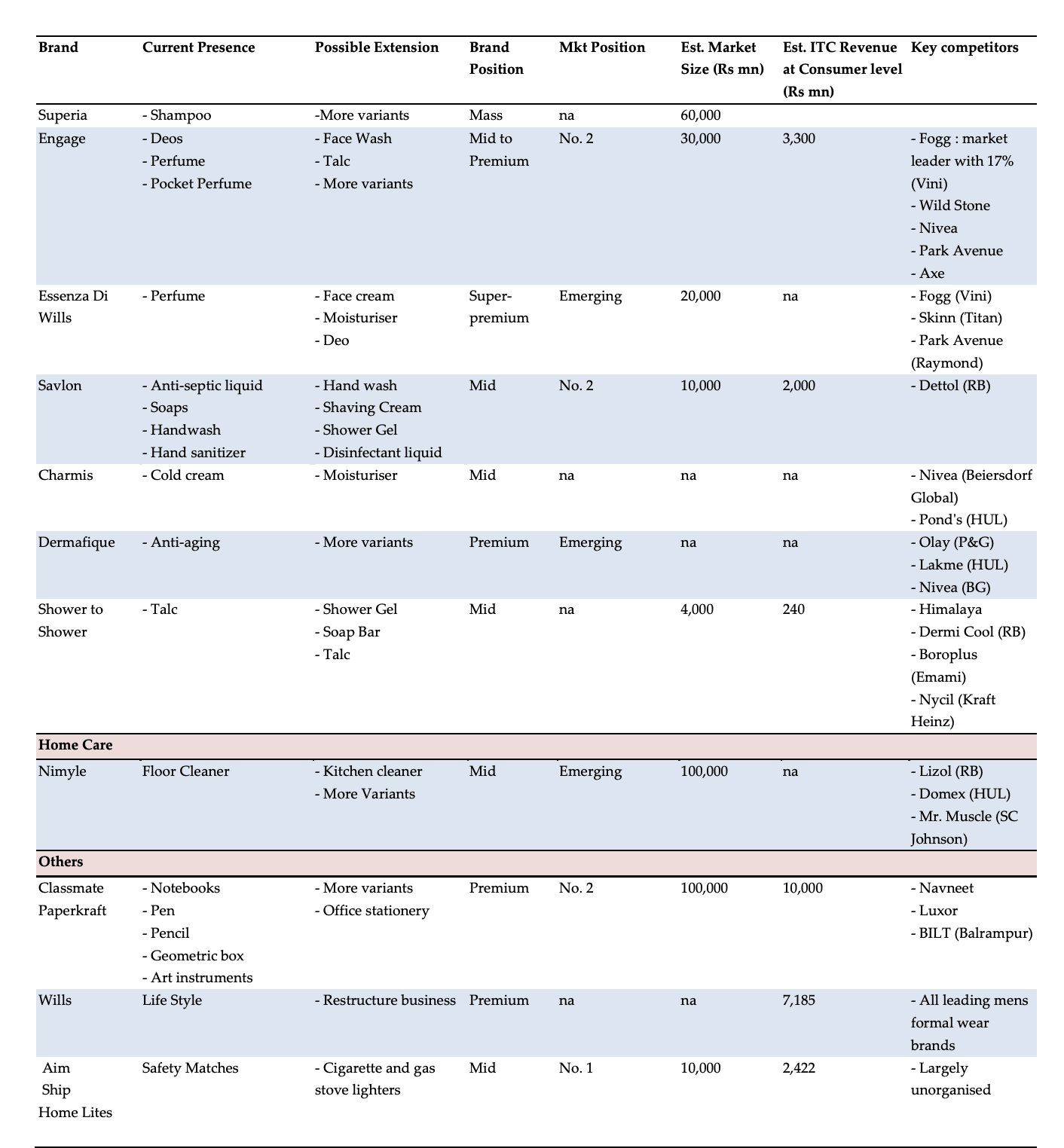

Here’s a compiled list of a nice tweets by Prashant Pandarathil on Twitter ( @prashant_mrch16 ) of how ITC has a known history of entering strong monopolies and penetrating themselves. Agreed they might not be the best in each category but they have caused some considerable damage !

This is from the latest report from HDFC which shows all the categories ITC is present in and its position in the market. We should not judge the products on our anecdotal individual likes/dislikes. The discussion can go on and on but is mostly useless. Most of our taste habits are formed in the childhood, so someone used to Maggi will likely not like Yippee but present children who are introduced to it may stick to it life-long.

Even though Hotel business contributes every less towards their revenue I thought of sharing this video which I came across on how they will be operating during COVID crisis.

Well, everyone knows that their cash cow is Cigarettes, but with govt coming hard on tobacco industry + cigarette volumes declining, its pretty obvious that those free cash flows are going to reduce significantly over the coming years.

In VST Industries thread, I did cover about Cigarette being cockroaches among the listed companies. US and UK sector wise data in CSFB Global Wealth study only show Cigarette being a major sector which continiue to exist in 20th century. Having said that, lot of changes have happen. My wish is ITC can maintain its cashflow around 5-10 years from Cigarette and after that Other FMCG sector shall become sufficiently large to provide for future growth territory. This is my wish and market environment is not obliged to fulfill my wishlist

There can not be clear cut answer to such question when there are mutilple moving parts. However, being addictive business, ITC cashflow from cigarettes, are least volatile in my opinion. How long that situation can persist, I do not know. One has to look at once risk profile and decide for allocation after developing conviction in investment idea.

Discl: Among my top 5 holding and with small addition last month, my view may be biased. Not a SEBI registered advisor, Not Recommeding investment in the company, Please do your own due diligence before investing.

Link for Cigarette Industry Market cap globally over 20th century

If u look at the margins of FMCG they r improving over the last four years… Further the demand for cigis r inelastic in nature n thus easy to pass on the price… Cigi prices for milds has moved from 3 to 15 Rs over last 7 years I guess.

I was observing advertisments in 3 Malayalam channels . In between prime shows majority of advertisments are from itc brands . Mangaldeep, savlon hexa , vivel soap , fiama handwash , savlon handwash, candyman ,nimyle ,aashirvad atta, engage perfume. In terms of competitors only hul , dabur and jyothy lab are there but with fewer brands when compared to itc. Any data to compare FMCG companies advertisement spend ?

in all the noise, we rarely hear about news on ITC infotech. Shouldn’t it be in the focus right now when IT companies are able to grow with ‘work from home’?

Why is ITC Ltd not providing it enough wings to fly? FMCG sector also has a huge requirement and potential globally for IT services.