ITC - comments of Cigarette performance and Industry as a whole -->

A punitive and discriminatory taxation and regulatory regime along with a sharp increase in illegal trade in recent years, especially at the premium end, continue to pose significant challenges to the legal cigarette industry in the country.

Towards the end of the year, the COVID-19 pandemic caused operational disturbances even before the nation-wide lockdown. During the initial phase of the lockdown, unprecedented disruption was witnessed across the value chain. However, all factories are currently operational and sales & distribution operations are progressively normalising.

Immediately upon receipt of permissions, the Company was able to resume operations and swiftly ramp up production and availability of its brands across markets. This is a testimony to

the extraordinary resilience and deep commitment of the Company’s workforce and business partners.

Several new variants were introduced during the year to cater to the continuously evolving consumer preference and ensure the future readiness of the Company’s product portfolio. Key market interventions during the year include the launch of innovative and differentiated offerings at the premium end such as Gold Flake Indie Mint & Gold Flake Luxury and the extension of Gold Flake Neo & Classic Rich & Smooth to other markets. The Business also deployed focused offers under the ‘American Club’, ‘Wave’, ‘Player’s Gold Leaf’, ‘Pall Mall’, ‘Navy Cut’, and ‘Flake’ trademarks in strategic markets towards bolstering and strengthening its market standing.

It is pertinent to note that since 2016-17 i.e. pre-GST, taxes on cigarettes have increased by 40%, i.e. at a compound annual growth rate (CAGR) of about 12% (on a comparable basis) - over thrice the rate of inflation during the same period.

Discriminatory taxation on cigarettes, has caused progressive migration from consumption of duty- paid cigarettes to other lightly taxed/tax-evaded forms of tobacco products, comprising illegal cigarettes and bidi, chewing tobacco, Gurkha, Zarda, snuff, etc. Consequently, while the share of legal cigarettes in total tobacco consumption in the country has declined considerably from 21% in 1981- 82 to a mere 9% (against global average of 90%), aggregate tobacco consumption has increased over the same period.

Illicit cigarette trade in the country has been growing at an alarming rate. Euromonitor International ranks India as the 4th largest illicit cigarette market globally.

While legal cigarette industry volumes have declined by about 20% between 2010/11 and 2019/ 20, the illicit duty-evaded cigarette segment has grown by 36% during the same period , accounting for about one-fourth of the domestic industry and making India one of the fastest growing illicit cigarette markets in the world.

The regulatory framework for cigarettes in the country is one of the strictest in the world.

The large and rapidly growing illicit cigarette trade also has a deleterious impact on the millions of farmers and farm workers engaged in the tobacco value chain. Since smuggled international brands of cigarettes do not use Indian tobaccos, in addition to revenue losses, the growth of the illegal cigarette trade has also resulted in a severe drop in demand for Indian FCV tobaccos in the domestic market.

It is pertinent to note that several other major tobacco producing countries, including the USA have framed regulatory frameworks for tobacco taking into consideration the economic interests of their tobacco farmers. The inadvertent and unforeseen consequence of the stringent Indian tobacco regulations and discriminatory taxation continues to adversely impact the livelihood of Indian tobacco farmers with corresponding gains to tobacco farmers in the countries that have opted for moderate and equitable tobacco regulations.

It is estimated that since 2013-14, Indian tobacco farmers have suffered a cumulative drop in earnings of appx. Rs.5,175 crore

Stability in taxes on cigarettes will have the salutary effect of enabling the legal cigarette industry to claw back volumes thereby engendering domestic demand for Indian tobaccos. This will also help cushion the impact of volatility in international markets.

So, they are trying to play the farmer card for stability in rules and laws in the industry.

According to them, the illicit cigarette segment GREW 36% in the past decade, so if they were to tap into this market, cigarette volumes would grow handsomely.

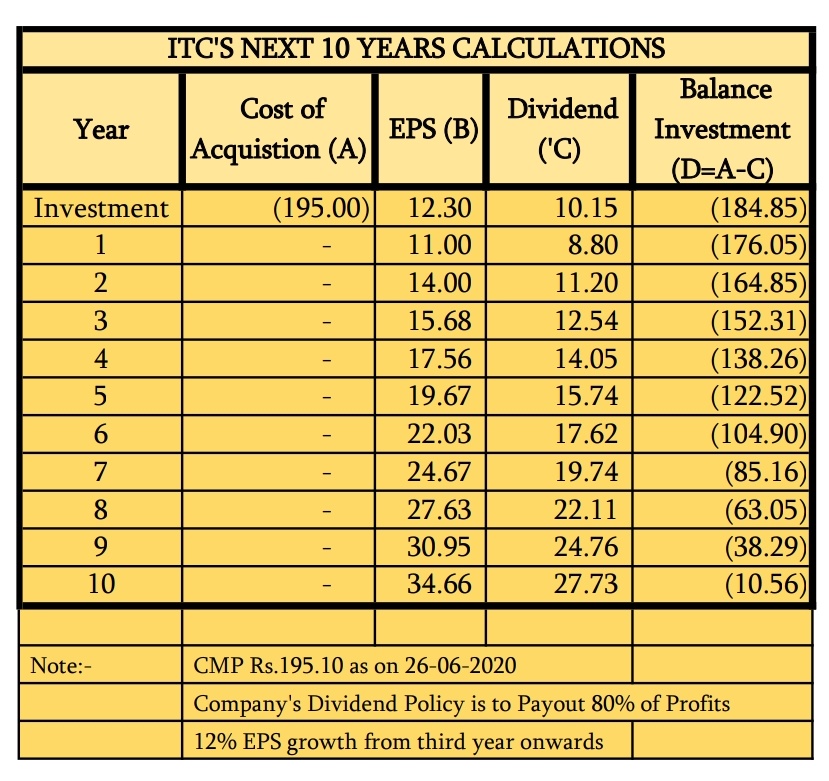

( maybe just sonata and rites (albeit a psu) belong to this category of growth + dividend stock). I don’t see any issue at all with the payout

( maybe just sonata and rites (albeit a psu) belong to this category of growth + dividend stock). I don’t see any issue at all with the payout