IREDA launches its retail subsidiary -receives Govt approval

The wholly owned subsidiary to focus

on the retail business B2C under PM-Suryaghar (Rooftop Solar), PM-KUSUM schemes and B2C segments in RE and Emerging RE sector including EVs, Energy Storage, Green Technologies, Sustainability, Energy Efficiency,

It’s one of the stocks where there is always some promising new development. Fortunately or unfortunately we are now in the phase of market where easy liquidity seems to be peaking and now valuations are in driving seat. We have already seen sharp corrections in many overvalued but darling stocks without any meaningful bounce back.

At 7 times book, those investing in IREDA now will have to brace for a long slog to get any meaningful return. Ireda might be a great company but so was (and is) Bajaj Finance in its heyday in 2021 commanding 12 times book and now at 6 times book stock still has very few takers.

The jump in Gross NPAs is a bit concerning? Any idea what asset slipped.

Didnt find any management interview either post the results explaining the jump in NPAs.

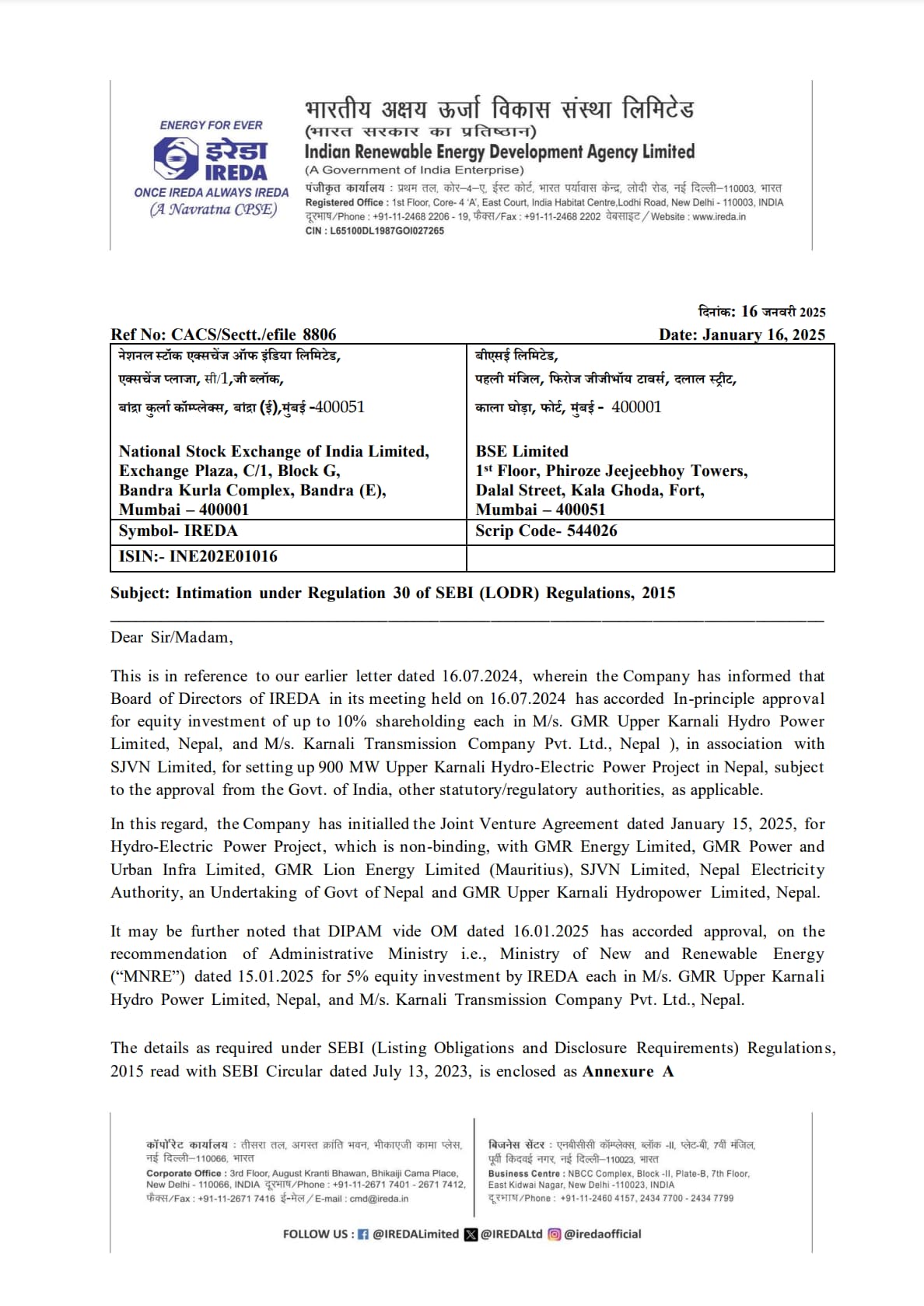

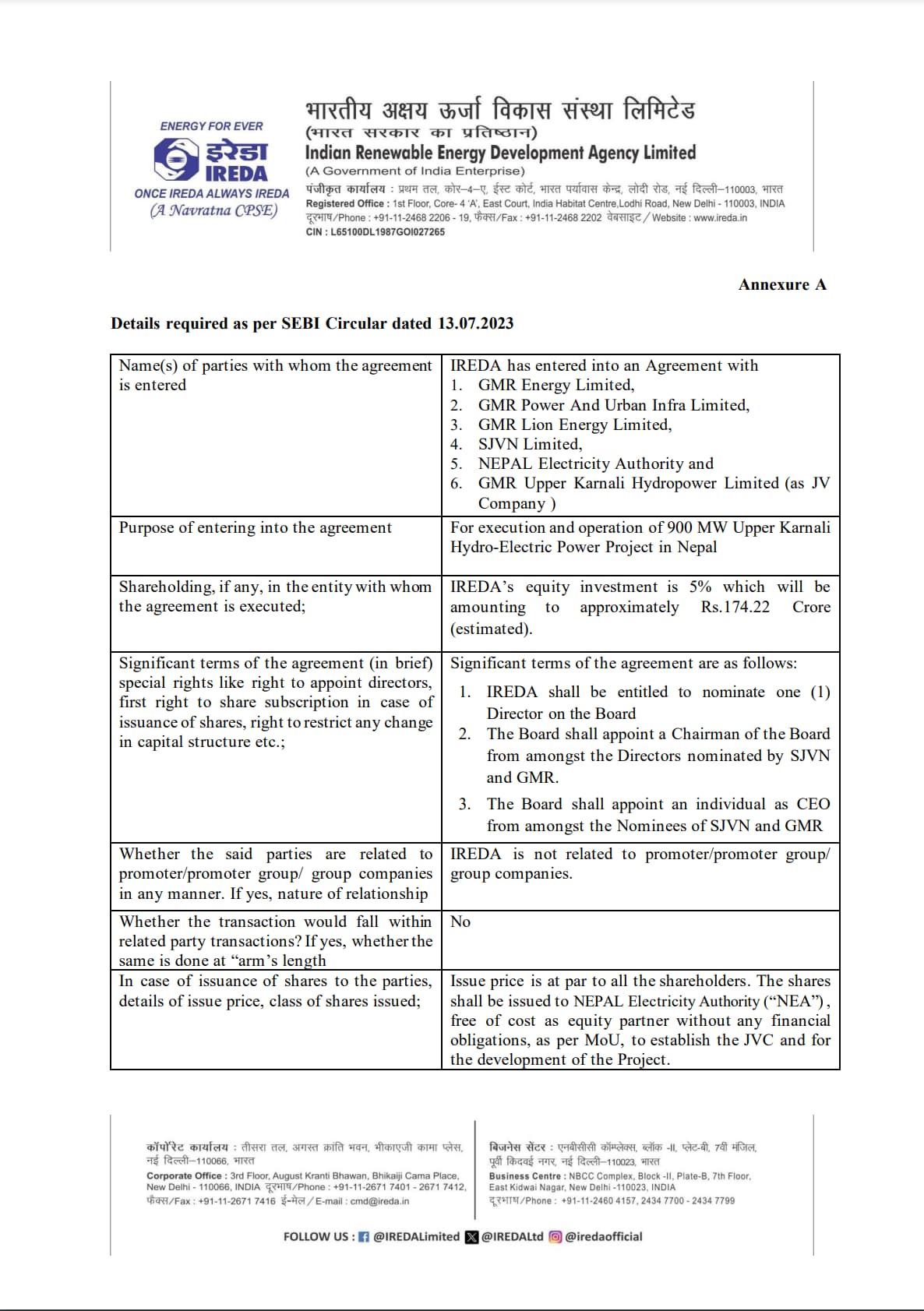

IREDA entered into a non-binding Joint Venture Agreement (dated January 15, 2025) for the development of the 900 MW Upper Karnali Hydro-Electric Power Project in Nepal.

This project involves collaboration with entities like GMR Energy Limited, SJVN Limited, and the Nepal Electricity Authority.

Good results. But equity dilution is a concern and so EPS is lagging. Any views

May appear a naive question, but aren’t IREDA and IRFC just another NBFCs? Why should they be valued differently?

Price to book is the metric that we are looking here . its expensive in my opinion

Has anyone analyzed the impact of Gensol issue on its books or NPA.

It seems the IREDA investors are in for a cruel awakening. The question is did IREDA alert the public or any other institutions about the default?

The Mint says:Gensol: The Jaggi brothers made smart moves. So, why did they need a ‘piggybank’? | Company Business News

"Between FY22 and FY24, Gensol raised ₹664 crore from the Indian Renewable Energy Development Agency Ltd (Ireda) and the Power Finance Corporation (PFC) for buying 6,400 electric vehicles (EVs). The loans were meant to fund 80% of the cost of the EVs, with Gensol expected to put up another 20% in equity, taking the total corpus to ₹830 crore.

The vehicles were then meant to be leased to BluSmart, which is an EV-only ride hailing company started by the Jaggi brothers.

However, Gensol bought 4,704 EVs at a cost of ₹568 crore. The remaining ₹262 crore was unaccounted for, even after a year since the last tranche of financing was received from the lenders, Sebi noted. The two promoters siphoned this money from the company through multi-layered transactions for personal benefit, the regulator alleged.

ey? Sebi found that ₹43 crore went towards paying for an apartment in The Camellias, an ultra-exclusive housing complex developed by DLF in Gurugram. The promoters also spent on a golf kit ( ₹26 lakh), Titan watches and jewellery ( ₹17 lakh), credit card bills ( ₹60 lakh) and in Emirati Dirhams (over ₹2.5 crore)."

I am a lay person, but how did the fraud go on? I have just found a 2010 headline. Loan end-use tracking to begin soon: ICAI - The Economic Times

But you know what? Adanis are also accused of circular movement of funds. May be not entirely similar, but if they had done it in the US, they would have gone to jail for 30 years like Gupta did.

So, other businessmen also take a hint.

Gensol started defaulting only in december 24 and according to IREDA , the default amount/ time has not crossed the threshhold yet where the entire loan be marked as NPA so that question of notifying others does not arise.Till now the default amount is only 56 crores out of a loan amount of 640 or so .While it looks likely that the money would remain in limbo for sometime, still ,the money is traced mostly so most of it would ultimately end up in the books of Ireda .

IMHO, its not a thing that changes the fundamentals too much for Ireda ..its not going to sink or even stutter since even total loss would mean only 4 months profit down the drain .

Vulnerable portfolio

However, the broking firm expects Ireda’s return on assets to drop to 2.3% and 2.2% in FY26 and FY27 from 2.5% in FY25, as credit costs rise. The lender’s borrowing costs may increase due to higher exposure to the private sector and a high proportion of the vulnerable portfolio, according to the report.

This includes its exposure to Gensol Engineering Ltd, barred by the Securities & Exchange Board of India in its 15 April interim order. As per an ICRA rating action report dated 4 March, IREDA has a total exposure of ₹470 crore to Gensol, including ₹216 crore towards working capital. Ireda had unpaid dues of ₹56 crore from Gensol as of 15 March, according to Sebi.

The exposure, with a high probability of default, can significantly affect Ireda’s profitability ahead. Further, its provisions coverage ratio for stage-3 loans at the end of Q4 was 45.3% against 58.8% a year ago, although it was marginally better than 44.5% in Q3.Ireda posts strong growth momentum in Q4, but ₹470 crore Gensol loan is a concern

There have been serious lapses in monitoring the end-use of the loans given to Gensol/Blusmart.

https://www.livemint.com/companies/gensols-missing-evs-a-262-crore-question-mark-for-lenders-ireda-and-pfc-sebi-loans-nclt-blusmart-anmol-jaggi-11745238381293.html

Another good reason why retail investors should stay away from government PSUs where there’s no accountability at the top level.

Boom bust, the lending space itself goes through a series of boom (where loans are given out left and right boosting revenue), and bust (when bad actors don’t pay them back).

No PSU concept here, same thing has happened in many NBFC’s.

I’d be interested again below 3 P/B at such growth rate.

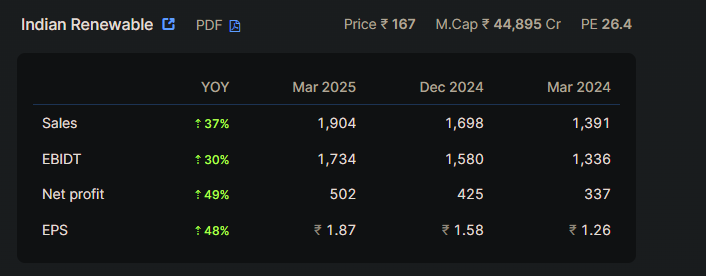

Some Material update from Q1FY26 Result:

-

Although reveune is flat QoQ, Profit almost halved. Reason: Spike in impairment provision–> driven by Gensol downgrade and AP legacy NPA reclassification

-

Update about AP NPA reclassification:

• Borrower had challenged NPA classification since FY20 citing non-payment from APSDCL.

• Court had earlier restrained IREDA from declaring it NPA.

• On July 2, 2025, the interim stay was vacated, and IREDA immediately classified ₹783.34 Cr as NPA (Stage III) in Q1 FY26.

• Adequate impairment provision had already been created earlier under ECL method.

• Visible impact on Gross NPA %, but fresh heat of PAT is negligible as provision was created earlier -

The hedge reserve gain of rs 24.89 gave some positive cushion, otherwise the result would have been worese.

-

Regarding Gensol:

• Borrower loans:

GEL: ₹510.01 Cr

Gensol EV Lease Pvt Ltd: ₹218.95 Cr

• Both downgraded to NPA; insolvency (IBC Sec 7) proceedings and DRT cases initiated.

• however some secuity is there: Collateral of project assets + corporate & personal guarantee + 20% equity stake pledge.

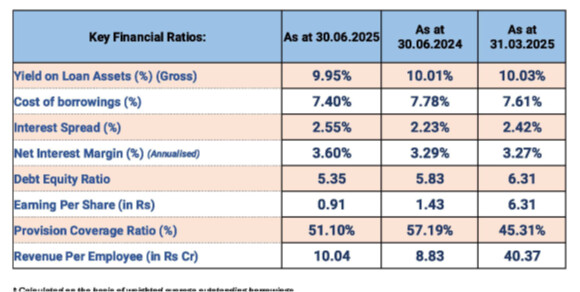

Key Financial Ratios:

In my view, IREDA should immidiately start Concall and address these issues and provide future guidance.

point of concern for me: cases like Gensol and the AP saga raises serious trust issues and implementation of monitoring tools of end usage of loans given

some positive points: as on 30-06-24, interest spread has widen to 2.55% from earlier level of 2.22% on 30-06-24. With recent introduction of tax exmption bond, cost of borrowing is supposed to decrease furtehr.