IREDA, is a non banking financing company which provides financial assistance to renewable energy projects like power generation, equipment supply and fuel source projects including wind power, solar power, hydro power, biomass.

The Company’s primary sources of funds include domestic and foreign borrowings, internal resources and Government of India support.

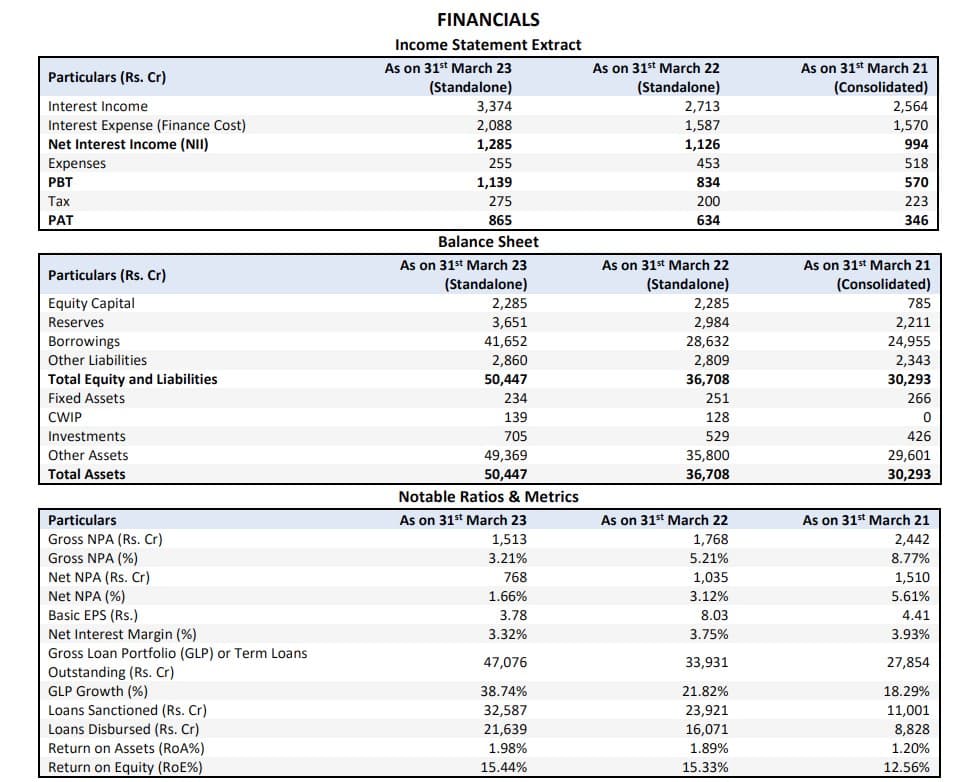

Keep monitoring few metrics like: GNPA, NNPA, NIM, ROA which are important to track in case of financial companies.

Many listed players are funded by IREDA (like websol i know of)

Can anyone explain would it not be safe for the company if it lends to psu or govt backed projects mostly? It too would have low or no NPAs like IRFC? How much safe is it to lend private players? I am a newbie here and trying to understand and learn. Thanks in advance.

With ROA/ROE of 1.2% / 9% , a 4+ P/B multiple is unjustified. Haven’t done extensive research on this. Is there any fundamental trigger which can improve the return ratios?

Folks invested in the company please share your rationale behind the investment thesis.

I don’t think we are in euphoric market as far as banks/NBFCs are concerned. Most banks/NBFCs right now are reasonably valued. They are slightly above historic valuations but reasonable compared to the current return ratios.

Most banks like top private sector banks, NBFC like Bajaj Finance (basically large caps), would be reasonably valued. But for smallcaps there is definitely euphoric market.

Coming to IREDA, imo it is overvalued.

Reason for these valuations maybe

Newly listed Popular company, hence multiple domestic mutual funds have started building positions.

The SIP inflows are at all time high (every month a new ATH), and the mutual funds need to buy new companies.

PSU, Renewable theme, previous stock returns of PFC/REC.

Things I will watch out for before increasing position:

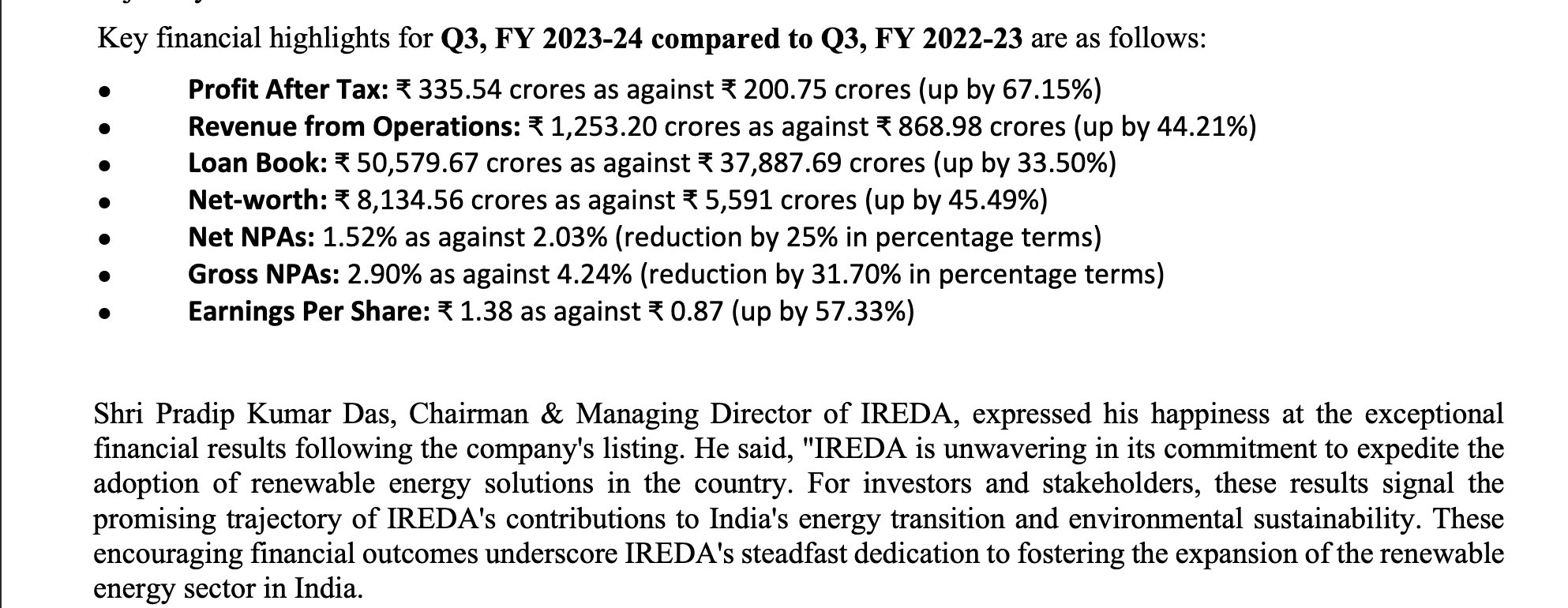

Ireda upcoming results. Even though the market has already discounted the previous 55% Profit growth.

Ireda get’s approval for Navratna. Which again has been promoted by the MD multiple times since the IPO.

X,Y,Z Ace small cap investor enters IREDA. Quarterly Mutual fund holdings revealed.

Has anyone looked under the hood for the various loans they are giving ?

It is really weird , they are giving high loans to small companies against their company shares .

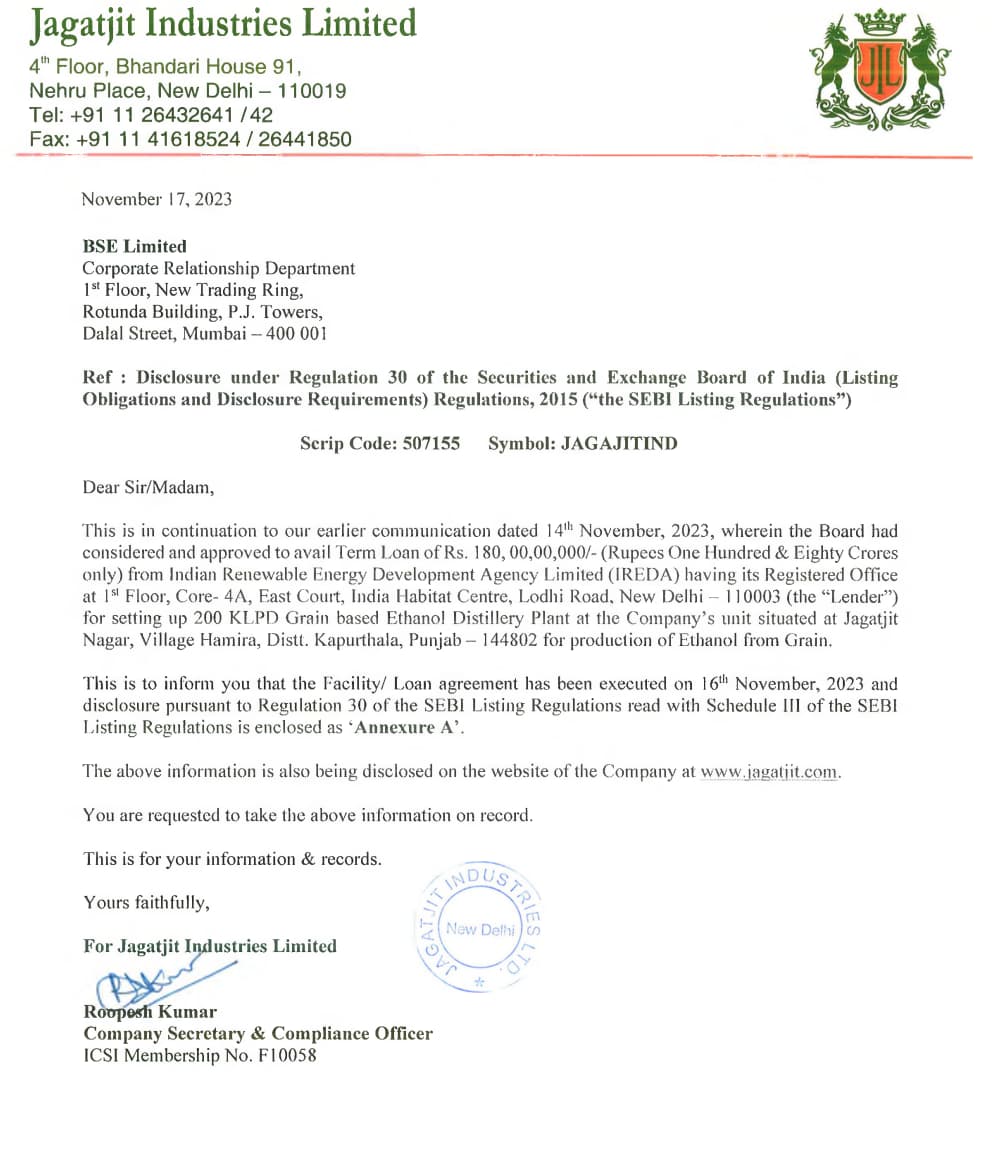

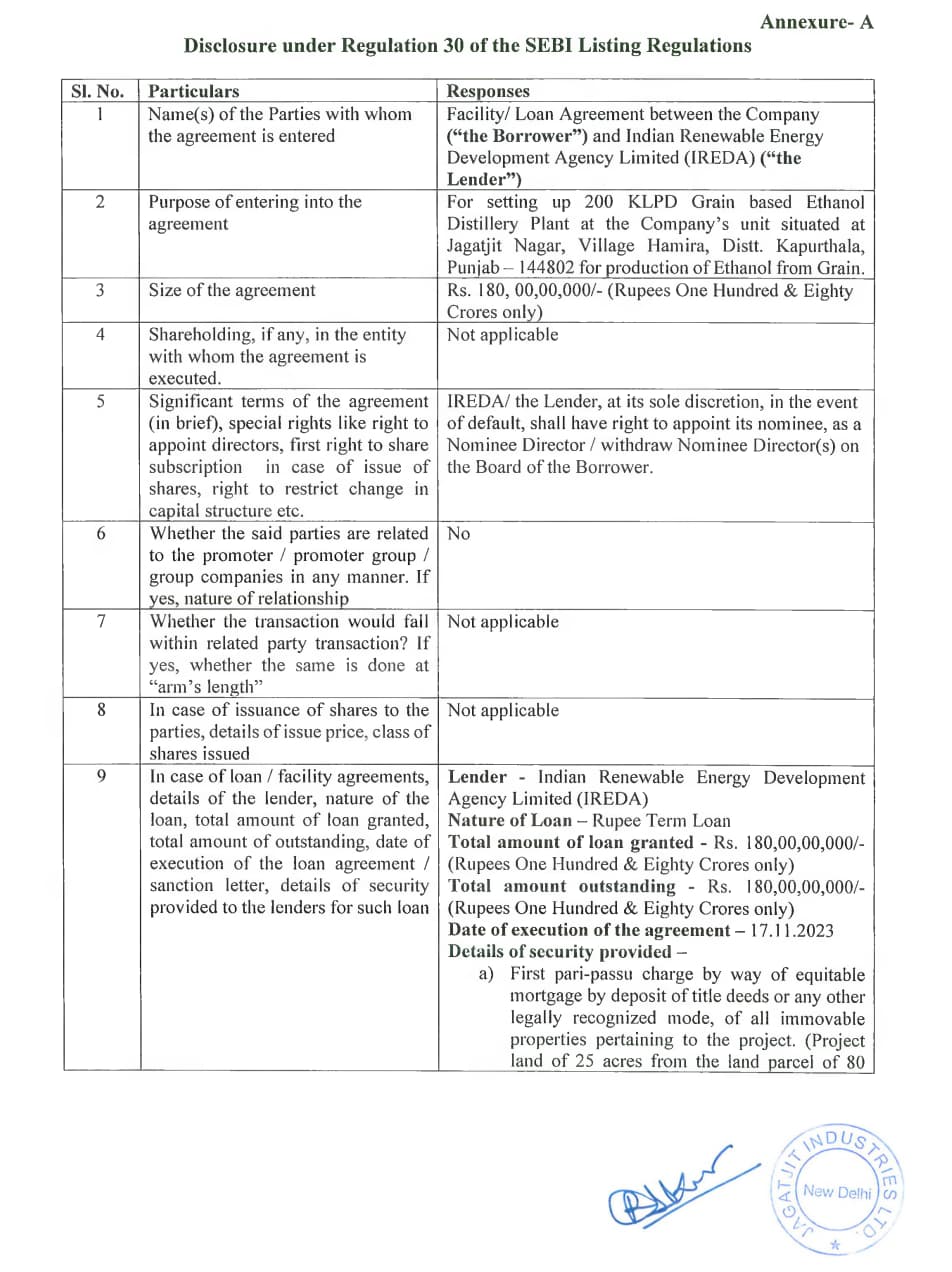

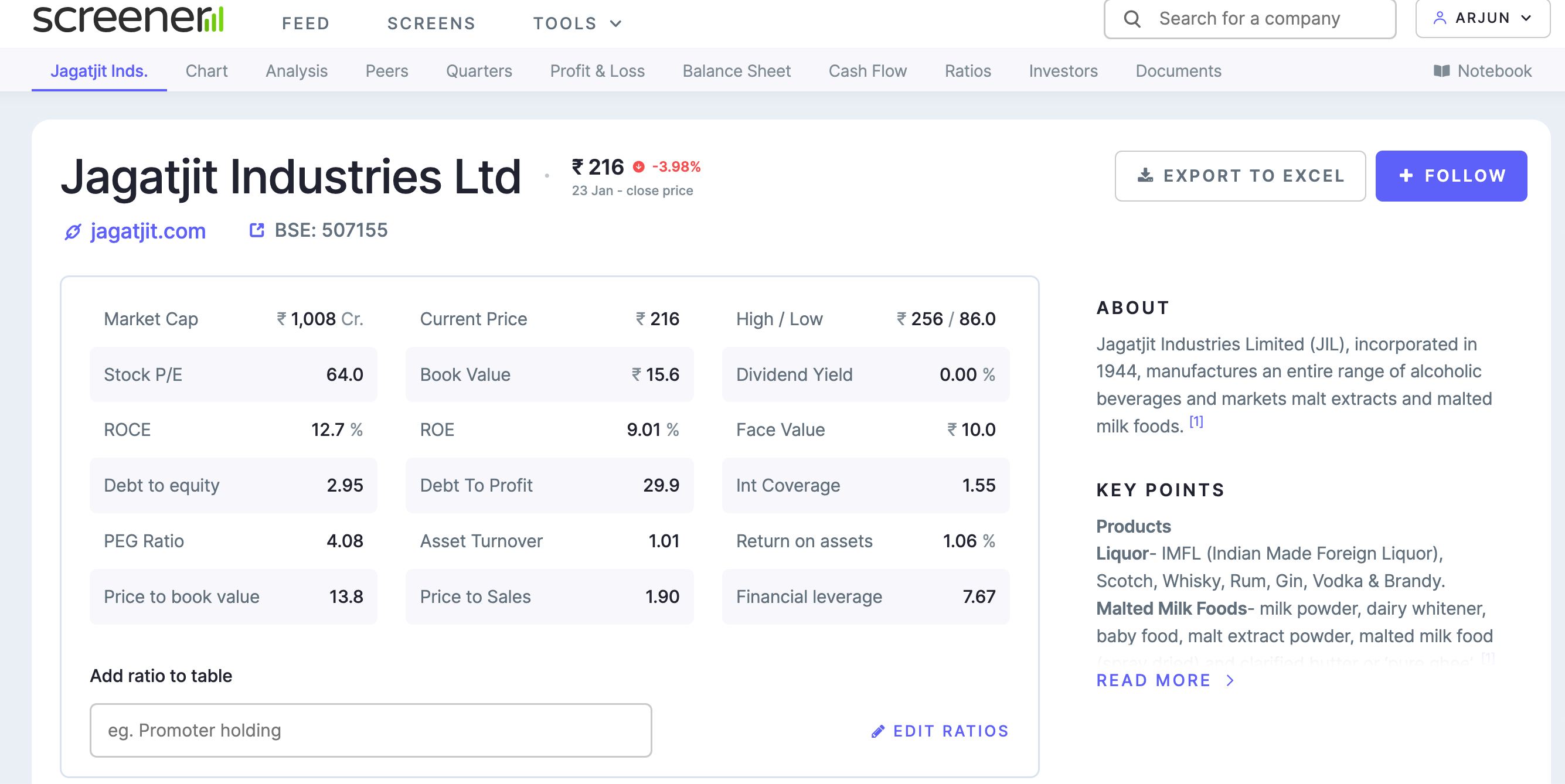

They say they have collateral but against a companies shares is not exactly good , also doesn’t help these companies are at very high PE valuations already. Case in point Alpha logic and Jagatjit industries . 05abca1f-1b1d-40a3-b224-92f049080fff.pdf (163.8 KB) aa2afee7-2f3d-43dd-947f-03b698a4034b.pdf (3.1 MB)

Most of the way they are disbursing loans is done in a similar way .

If one searches IREDA on screener you will see quite a few loan sanctions like this , in which the value collateral seems unsound. Not from a loan or banking industry, but seems like a red flag .

Not invested, studying for now .

India’s is an early stage of credit cycle and many finance companies are giving loans like these. In the initial years NPA’s would be low, but most of the businesses will fail anyways, and slowly NPA of NBFC will increase and profits tumble.

The numbers of JagatJit Industries, are of the present, but the loan of setting up of Ethanol plant is given keeping in mind the future. As long as JagatJit as enough cash flows to pay off it’s short term debt, it won’t become an NPA for IREDA.

You can also track the working capital ratio for an individual company, to see it’s ability to pay debt.

Anyways, all these concerns are for IREDA’s management, and as a shareholder I will be more concerned about growing profits and valuations of the company.

NPAs, higher provisions, risky loans & advances will dampen the valuation of the Company of which you are the shareholder. Whatever is Management’s concern, should be your concern too buddy!

I agree, but as an investor in 20 companies, it is quite draining and not fruitful to dive into such details. Maybe for an SME or Microcap you can do that to identify corporate governance issues, but no need to worry about a PSU like IREDA with top quality management.

As I mentioned, in the start of the credit cycle the loans are dispersed quite freely, and initially NPA’s are low. When the non payment begins (At the end of the credit cycle), it would be wise to get out of all PSU.

In IREDA, I am tracking Earnings Growth and Valuations.

Before you would realise the cycle has turned bad and NPAs are going to grow, your majority of the profits would have been wiped off.

Polycab is not an SME and still we saw what transpired there. Corporate governance issues do not happen because of the size of a company.

PSUs’ major risk is governmental control and overnight shift in the policies/ rules/ stance.

Anyway, everyone has their own style of treading along in the market.

Good luck!

Holding IREDA since listing day. Would book partial profits before budget.