Valuation report is out

NAV per unit at INR 100.49. Does not include Vadodara Kim. WACC cost of capital for most assets over 10%

Valuation report is out

NAV per unit at INR 100.49. Does not include Vadodara Kim. WACC cost of capital for most assets over 10%

Oct Toll collection. 6% up QoQ

and here is the half yearly report. Looks a nice compendium of every kind of info

PS - invested

Nov’22 toll collection, in line with the figs of Oct’22. This came out, post market yesterday

a869ffeb-c63b-46d4-8723-842c20500caa.pdf (421.2 KB)

Toll collection stopped again and the revenue gets shifted to end of concession. Not bad for long term investors but may be sentiment dampener for short term traders of Invit.

Curious about this. Is there any potential risk of non revenue recovery at the end of concession? If yes, would it impact the IRR and distribution appeal?

No impact as concession period will get increased by same number of days. In fact NAV gets improved based on past similar instances as revenue is only deferred to a future period with benefit of annual increase as per WPI and traffic growth well compensating the time value of money.

Thx much Amit, this helps

These 2 news items are a week and 3 weeks old

Recommencement of toll collection in Amritsar- Pathankot Jan 16 news

Dec’22 toll (Given it is 31 days month, a tad higher than Nov) 9th Jan news

Here is the fine print in today’s budget

Budget fine print ![]()

Tax avoidance through distribution by business trusts to its unit holders

Finance (No.2) Act, 2014 introduced a special taxation regime for Real Estate Investment

Trust (REIT) and Infrastructure Investment Trust (InVIT) [commonly referred to as

business trusts]. The special regime was introduced in order to address the challenges of

financing and investment in infrastructure. The business trusts invest in special purpose

vehicles (SPV) through equity or debt instruments.

2. Keeping in mind the business structure, the special taxation regime under section

115UA of the Act, inter-alia, provides a pass-through status to business trusts in respect of

interest income, dividend income received by the business trust from a special purpose

vehicle in case of both REIT and InvIT and rental income in case of REIT. Such income is

taxable in the hands of the unit holders unless specifically exempted.

3. Sub-section (1) of section 115UA of the Act, inter-alia, provides any income

distributed by a business trust to its unit holders shall be deemed to be of the same nature

and in the same proportion in the hands of the unit holder as it had been received by the

business trust.

25

4. Further, Sub-section (3) of section 115UA of the Act, inter-alia, provides that if the

“distributed income” received by a unit holder from the business trust is of the nature as

referred to in clause (23FC) or clause (23FCA) of section 10 of the Act i.e., is either rental

income of the REIT or interest or dividend received by the business trust from the SPV,

then, such distributed income or part thereof shall be deemed to be income of such unit

holder.

5. It has been noticed in certain cases that business trusts distribute sums to their unit

holders which are categorised in the following four categories:

(a) Interest;

(b) Dividend;

(c) Rental income;

(d) Repayment of debt.

6. As has been stated above, interest, dividend and rental income have been accorded a

pass-through status at the level of business trust and are taxable in the hands of the unit

holder. However, in respect of the distributions made by the business trust to its unit

holders which are shown as repayment of debt, it is actually an income of unit holder

which does not suffer taxation either in the hands of business trust or in the hands of unit

holder.

7. It may be noted that dual non-taxation of any distribution made by the business trust i.e.

which is exempt in the hands of the business trust as well as the unit holder, is not the

intent of the special taxation regime applicable to business trusts.

8. In view of the above, it is proposed to make such sum received by unit holder taxable in

his hands. However, provision is also proposed for a situation when the sum received by

unit holder represents redemption of unit held by him. Hence it is proposed to amend the

Act by way of,-

(i) insertion of clause (xii) in sub-section (2) of section 56 of the Act to provide that

income chargeable to income-tax under the head “income from other sources”

shall also include any sum, received by a unit holder from a business trust, which-

(a) is not in the nature of income as referred to in clause (23FC) or clause

(23FCA) of section 10 of the Act; and

(b) is not chargeable to tax under sub-section (2) of section 115UA of the Act;

(ii) insertion of a proviso to the said clause to provide that where the sum received by

a unit holder from a business trust is for redemption of unit or units held by him,

the sum received shall be reduced by the cost of acquisition of the unit or units to

the extent such cost does not exceed the sum received;

(iii)insertion of sub-section (3A) in section 115UA of the Act to provide that the

provisions of sub - sections (1), (2) and (3) of this section, shall not apply in

respect of any sum, as referred to in clause (xii) of sub-section (2) of section 56 of

the Act, received by a unit holder from a business trust;

(iv) insertion of sub-clause (xviic) in clause (24) of section 2 of the Act to provide

that income shall include any sum referred to in clause (xii) of sub-section (2)

of section 56 of the Act.

9. These amendments will take effect from 1st April, 2024 and will accordingly apply to

assessment year 2024-25 and subsequent assessment years.

Discussion points

There was no panic in the counter, unlike the REIT like Embassy but wanted to know various view points…

If the return of capital becomes taxable, its yield will fall significantly

I think it affects both REITs and INVITs broadly however REITs more. As the majority of distribution of INVITs was primarily thru interest which was anyways taxable unlike REITs. Curious to hear from others

not true…IRB was different with good RoC

0.8 Rs ROC 1.25Rs as interest. Now the entire 2.05 Rs (last distribution as an example) is taxable. Still think even at 30% tax bracket it is reasonably okayish at 8.7% post tax yield. However looks like it will also take a hit in stock price due to its risk profile

at 30% tax, it is actually almost 34% tax because of surcharge …so, at 65 price, it is more like 8% for the above 2.05 taxable…but, who else is giving post tax 8% !! obviously, it is still respectable and that is why, perhaps it did not tank, in comparison to the horror tale in REITs and even the ever reliable Indigrid.

With one HAM project, I expect some minor uptick in distribution in coming quarters…Look at ever increasing auto sales…people will drive, even if the roads are choked…with replacement policy coming (it is for Govt vehicles but will slowly happen for everything…and people will be on roads)…all said, who can forget the free fall from 100 to 27 between 2017-19…so, risk is always there !!

PS - Holding

Yep agree. My biggest concerns are two:

Additionally the model is such that they constantly need to include more assets in the INVIT as the old ones will go back to the Govt?

Agree with you the yield is attractive and traffic volumes are on a secular uptrend.

PS: Holding as well

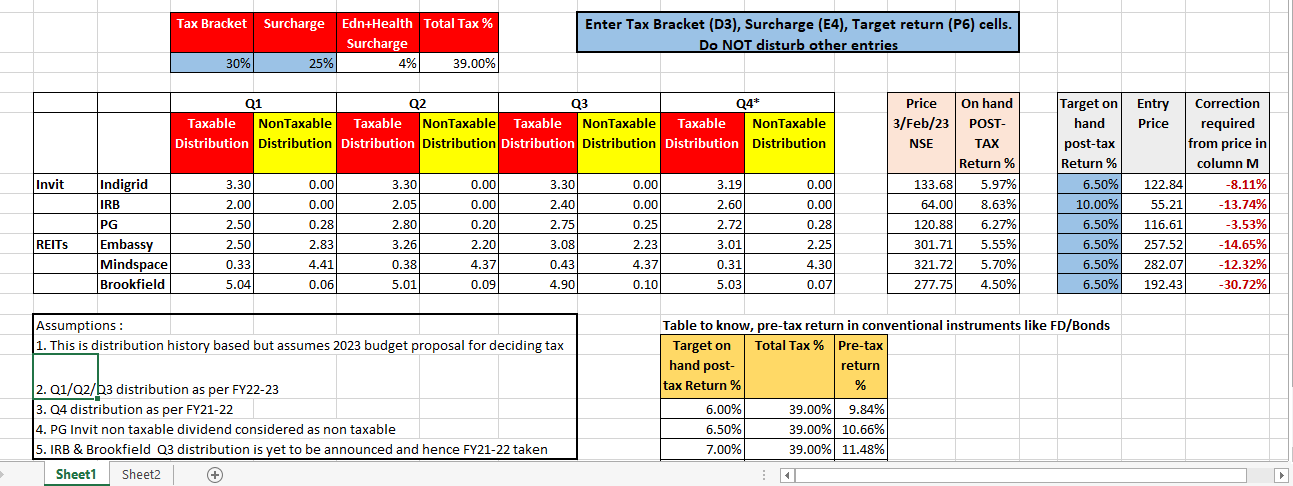

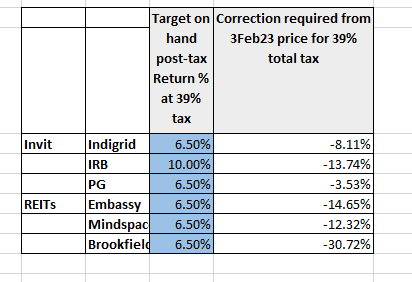

I have attempted to come out with a calculator that depicts the ravages of the 2023 budget taxation ![]() Target entry price for a target return and current return %

Target entry price for a target return and current return %

All the assumptions are in the spreadsheet and they are self explanatory. A very point is that this is historical distribution based and assumes that if this distribution is continued as such, what will happen with the new budget proposal.

I have also included a table for comparison with conventional instruments like FD

The only input cells are tax bracket, surcharge and target return (all in blue accent)

Pl give feedback and I am open to correct the excel

[InVit_REIT_Target Price_Target Return.xlsx|attachment]

InVit_REIT_Target Price_Target Return.xlsx (15.8 KB)

What shocked me was the amount of correction needed in Brookfield, post the budget change…how did it escape? is it held by entities who don’t have tax? or they taxed differently?

In budget proposed is tax for debt repayment part of income to be taxed in individual – why this would be taxed at 39%? I understand there is some change is taxation for international investor but individual investor from India is this tax rate valid?

Not a good worksheet. Only return of capital is taxed at the hands of investors - < 30% of the distribution is return of capital in these invits/reits. you were getting pre-tax yield of 9%+ in INVITs, now it is 12%. Markets are overreacting.

@Girish_Kolari Here are the tax slabs and surcharges

And Yes - with 30% tax bracket and 25% surcharge - you will get 39% …not much of a change in that…and YES…I have pasted the link above for tax on return of capital

Pl READ POST number 289 above

You might be in a different tax level and the spreadsheet has the input for the same…Pl Xcheck what you are saying, before questioning

@Srini_Narayanan

You don’t have to commend anything but instead of condemning what is not good…tell me, what is the error in the spreadsheet?

Return of capital is now taxed…and that means, in the case of IRB everything is taxed…the calculator captures that…what is wrong in the calculator? My assumptions stated in the excel makes this absolutely clear. Don’t jump to conclusion, without reading properly You may conclude whatever but don’t say it is not good, without absorbing the details

PS - The very reason, the average investor in INVIT and REIT is unable to understand is that , the aspects of taxation is not properly understood…It is your understanding that is incorrect. Post the changes in budget, the entire distribution in case of IRB (and Indigrid) will be taxable for the unit holder and in case of PGINVIT, except a small non-taxable div, the rest are entirely taxable. Please X check anything before typing something as NOT-GOOD