Not a big amount (~INR 43 lac), but always good to see promoters buying on the market.

2 Likes

For those , who are keen and yet to listen to Q1 FY23 concall, here is the link

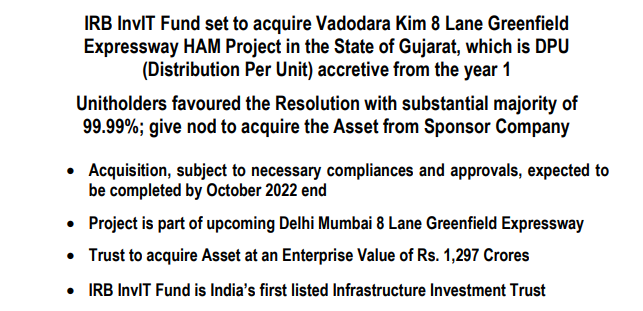

My key takeway from yesterday EGM

- Management declaration of DPU accretive nature of new project indicates their intention for this asset and future asset additions

- Management if following more predictable/accurate timelines now as compared to last few years where they were giving vague answers in Concall

- Shareholder response to the resolution has been passed with great majority and same will push management to onboard more new assets in coming years

- Market Price differential from book value will merge soon and last few days price movement is quite indicative.

P.S: Invested and biased

8 Likes

Aug’22 toll collection figures are here

About 2 crore less than July’22

1 Like

Thx for pointing …corrected it

1 Like

I have attended EGM of IRB InvIT to acquisition of New assets. On the thread @VijayJ has raised various point about valuation of assets and discount rate (WACC) applied in valuation.

While I agree with most of the comments, Still find that acquisition of HAM assets may not bad for investors in the long term. Find enclosed positive points in acquisitions:

- Stability in cashflow: Currently all 5 assets IRB holds have uncertain cashflow, which depend on toll rate and traffic. While Toll rate is determined by WPI, tarffic is function of economy actiivities. Hence, adding an assets wtih annuity income from NHAI would significantly improve diversity in portfolio in my view.

- Distriubtion acretive: As per EGM transcript, the management has given guidenace of additional distribution of Rs 0.50 (50 paisa) per unit from new assets in FY24. Given that toll assets portfolio reduced by 2 major road assets, addition in assets along with positive contribution to cashflow shall add confidence in IRB InvIT, if they manage to walk the talk.

On negative side, in past, the management has failed mutiple times over their past assurance. In my opinion, the Q2FY23 distribution, would be very critical for investors. In my understanding distribution of Rs 1.5/unit is normal, Rs 1.25/unit would be negative and anything above 1.5/unit may be treated positive. This is my undestanding and it may be completely wrong.

Current toll collectiion from existing assets increase my optimism for distribution. I have increased by holding by around 50% during May 2022 to August 2022 in IRB InvIT, mainly switching from India Grid InvIT investment (I have reduce India Grid holding by 27% and same being invested in IRB InvIT). The high wholesale price index and cyclical jump in road traffic are main factors which give me confidence to increase allocation in IRB. Whether my investment decision is correct or wrong, only time would confirm.

Discl: My view may be biased due to my investment. Not a SEBI registered advisor. Not offering any investment advise.

5 Likes

To all you investors of IRBInvit, I had a question around recording the distribution from IRBInvit. As per the distribution, it is split between interest and repayment of capital. Further in the FAQ on the IRBInvit website it doesn’t clearly state how should one treat the “capital repayment” part. I understand that the interest component is taxed at the tax bracket of the investor. How should capital repayment be treated? As per my understanding based on the link below repayment of capital is supposed to be a pass through and not taxed at tax bracket of investor.

Any help of the same would be appreciated. Thank you.

1 Like

Capital redemption shall be reduced from your acquisition price. For instance, you purchase IRB InvIt today at Rs 60 per unit. In next one year, IRB InvIT distribute Rs 2 as capital redemption. After 1 years, the market price is same at Rs 60 and you sold your holding in market. Despite no change in price, you would still be subject to capital gain, as your acquisition cost would be adjusted (deducted) with capital redemption. Hence, you adjusted purchase cost would Rs 58 (Original purchase cost Rs 60- Capital redemption of Rs 2 during the holding period), while selling price Rs 60. So you need to pay 15% Short term capital gain (holding of 3 years is required for InvIT to be consider as long term) on Rs 2.

Disclosure: This is my understanding and it could be wrong. I am not a qualified chartered accountant. You may consider advise of tax expert on the subject.

2 Likes

Thanks for that information. But this is alright if I have done purchase 1 time or so. I have purchased shares over few months and at various price from 52-55. So how should one consider the price adjustment?

My expectation is that of Rs 8 annual dpu this year. I do know that they were holding cash for maintaining this DPU after 2 assets going out and same was communicated by management in last Concalls. Use of cash in current acquisition and its impact on dpu and revenue for remaining months will be key monitorable. In any case DPU of 6 for this year is also not bad as I feel IRB Invit investment may be slow n steady debt exposure in portfolio considering their availabilty at significant discount to book value.

Please refer to this article if it helps

“All other cash flows received by the investor would be exempt from tax. In any case, the cash flow attributable to the debt repayment by the SPV represents return of capital of the investor, and would not be taxable.”

3 Likes

Thanks. The article in Mint is helpful.

1 Like

problem is people don’t look through the detail and this has been discussed in detail. Yes. Return of capital is not taxable.

I had also put calculators that simulate everything in this thread

1 Like

Hey Kayan sorry for that but I understand that return of capital is not taxable. So under what heading is one supposed to account for that in the investors book ? How is it used ? Also I am unable find a link to your calculator. If you could please include the same here it will be very helpful. Thank you and sorry for any inconvenience.

Post 237 above has the calculator.

Capital reduction needs to be shown as the adjustment to the Investments value in the books of accounts.

1 Like

“Although tax-free SPVs and trusts will remain, unitholders of InvITs and REITs will no longer be exempt. They will also be subjected to be taxed at the applicable income tax rate for the dividend income under the finance act 2020.”

1 Like

Thanks. I think this is applicable to REITs/INVITs that have opted for concessional tax rates.

So dividend is taxable in the hands of investor if the trust has opted for concessional tax regime. If not dividend is exempt with the investor?

To my knowledge none off the REITs/INVITs listed have opted for concessional tax regime

The aim behind such imposition seems to be convincing as it was to apply one advantage – either exempt the dividends or offer a lower corporate tax rate to the SPVs.

3 Likes

Sept’22 toll collection is almost same figure as Aug’22

Share purchase agreement for VK1 (Vadodara-Kim) project is complete

Earnings release is tomorrow (17th) and the call is on 18th

2 Likes

Quarterly earnings came out at 2.45 PM today… so, as the saying goes, ‘it is all in the price already’ since market got to see the results for 45 mins before close

(read the fine print in point 9 about the operating expense)

Looks a good result at 1st glance but will double down on details later

No surprises on the distribution front and it is on expected lines… If the Q3 and Q4 distribution and its break up is similar to last year, then anyone buying in now at say 60 Rs price, will take in 15% pretax distribution…(read the fine print of Q3/Q4 expectation)

Declared 2nd Distribution of Rs. 2.05/- per Unit, for the financial year 2022-23. The

distribution will be paid as Rs. 1.25/- per Unit as Interest and Rs. 0.80/- per Unit as Return of Capital, subject to applicable taxes, if any.

Please note that October 21, 2022 has been fixed as the Record Date for the purpose of Payment of this Distribution and it will be paid / dispatched to the eligible Unitholders on or before October 31, 2022.

3 Likes

My key takeways from Concall:

- Rs 8 DPU for current year is reiterated and possibility of 8+ depending on next half traffic flow

- 50 paisa DPU addition due to VK-1 addition.

- 150cr approx. cash used in current acquisition and 200 cr approx debt. Around 40 cr cash balance in books and 50cr approx in Escrow account(One toll project)

- Debt position still comfortable and management expects 2 new toll project additions in coming one year(mostly third party )

- Valuation report likely in coming few days

6.More details on balance debt repayment at SPV and Invit levels expected in next quarter results. This will give more transparent cash flow projections to investors/analysts.

Disclosure: Invested for long term

6 Likes