Happy to check again my understand if I have some missing information in my understanding.

In above comment you have mentioned POST number 289 – with respect to the link you have posted I could not understand what is it, would you please give me more information.

One more clarification is above mentioned detail talk about individual tax slab or REIT tax consideration change?

My understanding of change is following - in case you are referring different change please do let me know.

"The amendment proposed for REIT/InVIT related to distribution by manner of repayment of debt to the unitholders is now covered under the ambit of taxation as other income

The heading itself is clear. Double non taxation is addressed, which means that it will be taxed atleast once and that will be in the hand of the investor.

With this change , amortisation ( REITs) and Return of capital ( Invits ) are under tax now.

DDT is not applicable if the reit spv claims tax deduction as per old income tax regime…and if I recall right these REITs (When I say, these, I mean only Embassy and Mindspace),do use the old regime.Let me check in IRB

Also, this budget is very specific about killing the loop hole of tax avoidance in both ends (as in the case of Return of capital or amoritsation)…and not about double taxation

Chill - my aim was not to troll…interest portion (which is the dominant component of the return was always taxable). Now the return of capital is also taxable (it is < 30% for most INVITs on yearly basis). Price reduction and increase in yield does not justify this change in taxation. There are not many instruments with AAA sovereign rating with this yield arbitrage (> 500 BPS in case of PGINVIT). Disc: I am buying for this yield

You are free to decide on what suits you and I guess, everyone has a risk appetite that suits them. But, if I were you, I won’t call others work as ‘not good’ without solid reason

In my opinion, more correction has to take place and a slow decay has already started. Once the ex date hits in IRB, you will see an after effect here too. IRB gives the best yield among all the 6 instruments (refer my excel) and hence the correction may not be much. In any case, retailers don’t dictate the price, and it is the biggies/fund houses that decide it and some of them have different or no taxation at all.

Taking EVEN your 30% RoC affected as taxation as the base figure, for 39% tax on this is 12% decay (and that is the kind of approximate correction my table reflects). I don’t find any reason, to condemn that without further reasoning

I was a witness to the free fall in 2017-19 and hence I will approach it all with a tinge of caution (this is not a like for like comparison but DHFL, months before it folded up was AAA. Franklin ultrashort MF was the top debt fund, almost in every ranking for 5 plus years, before it was shut down, abruptly. So, I take everything with not a pinch but ton of salt), My attempt here is to educate the average retail holder and he must know, how much he will be getting post the taxation change, for his specific taxation bracket.

My premise is likely to hold true - already my 2 INVITs are back to small adjusted price (IRB at 65-only dropped 1 rs) and PGINVIT (back to 124 dropped 3-4 rs but will recover) I bought a truckload of PGINVIT when it dropped to 115 (a yield of ~13% for a regulated AAA biz) Now recovered to 124. Mkts overreacted to tax implications

you are correct - i was thinking 13.4 which is by Indigrid nit pginvit. My main point is at ~11% when risk free sovereign is at 6.5, 550 bps arbitrage is quite high (at pre-tax level)

“ “Declared 3rd distribution of Rs. 2/- per Unit, for the financial year 2022-23. The distribution will be paid as Rs. 1.75/- per unit as Interest and Rs. 0.25/- per unit as Return of Capital, subject to applicable taxes, if any”

Jan 2023 traffic decline is normal due to lower car trafffic following holiday season. There is nothing unusal in traffic

FY24 distribution would be around 8 per unit (Rs 2 per quarter) Maximum amount would be in form of Interest. During FY22, the two major project were near completition of concession, which resulted in larger share of principal, which is not case in FY23. Hence, distribution is mainly coming from interest flow and same shall continue

Management view about represenation to Min of Finance of application of income tax on capital redemption is as under. The investor shall be allowed adjust repayment of capital against acquistion cost and after appropriation of total acquisition cost, balance amount shall be taxed. The meeting of Representative body of InvIT and REIT has not held as most of REIT/InvIT were busy with quarterly results. Same is expected to organise in shortly as most have now completeed their quarterly reason.

Vadodara Kim would be contributing Paise 30-40 per unit in FY24. The final distribution would be subject to movement in interest.

WPI for DEcember 2022 was around 4.95% provisionally. In case same remain in final esitmate for WPI in Dec 2022, during FY24, InvIT shall expect toll hike of around 5%, (3% fixed+40% WPI (~5% in December), giving the toll revision rate,

Pathankot toll closure would result in increase in concession agreement by 30 days and cash compensation of Rs 6-7 Cr for closure of toll collection, InvIT has filed arbitration for same expect award within period 12-18 months period.

Amravati Talegaon, traffic continue to adversely afffect due to Metro work. However, now traffic shall improve as most of work is complete (Not sure on the second statement)

FY24 total repayment would be Rs 105-110 Cr (55-60 Cr for Vadodara HAM Assets and balance for old assets).

Exploring to add one more HAM assets from third party. Still at early state. InvIT can raise further Rs 6,000 Cr from debt.

Approached SEBI for buyback of units However, since nearly 90% of NCDF is distributed as distribution, SEBI sought source for funding buyback. SEBI was also against allowing NCDF for buyback as same would result in many investors missing out of buyback due to small amount. Hence, in my view, very difficult to anticipate management to do buyback to reduce discount between fair value and market value.

Disclosure: My view may be biased due to my holding in IRB InvIT and also IndiaGrid InvIT/Embassy REIT. Not recommeding any investment action. I am not SEBI registered advisor. I may take investment decision to buy/sell without informing forum. No trade in last 90 days.

Thanks DD. How would one keep a track of adjustment of repayment of capital against acquisition cost? Also in which tax assessment year would this be adjusted? Looks to be a cumbersome process?

This is suggestion. I am personally following same. Not sure whether same get approved or not. So wait for change. If government agree to change the tax law, it would worth that efforts. Personally, see very low probability of same being accepted.

Posting this as EDITED REPLY (RATHER THAN NEW POST, since VPr doesn’t allow 3 consecutive postings by the same user)…but I thought that this is time relevant info and hence putting it here

March toll collection news came on 10th April and it is a good 9% increase YoY and almost similar one for MoM too

The distribution is on the expected lines (Declared 4th distribution of Rs. 2.00/- per Unit, for the financial year 2022-23. The distribution will be

paid as Rs. 1.70/- per unit as Interest and Rs. 0.30/- per unit as Return of Capital).

On a rolling 4 quarters basis, the Post tax yield (at 30% tax bracket and 31.2% total tax) will be 8.59%, at closing price of 72.26 and pre-tax yield will be 11.14%

=======================================

While commenting on the occasion, the Spokesperson, IRB Infrastructure Pvt. Ltd. said, “The InvIT has well managed to continue with this distribution, despite certain odds like handing over two concessions duento completion. 26% rise in toll collection across all assets despite these odds, along with FASTag toll collection around 95% is noteworthy. Adding a HAM Asset, the first one for the Trust, which would

ensure consistent periodic revenue inflow, is another feather in the crown.” He further added, “Trust will continue to explore opportunities to acquire assets.”

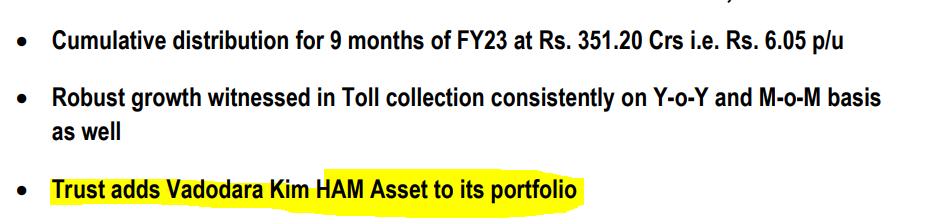

To re-iterate, the Trust acquired its first Hybrid Annuity Asset, Vadodara Kim Project from the Sponsors, in October 2023, which is the first stretch to achieve COD on the prestigious Delhi Mumbai 8 Lanes Greenfield Expressway.

Cumulative Distribution since IPO crosses 57% to Rs. 3,387 Crs

Good recovery in revenue over FY22 despite completion of 2 Concessions

First HAM project added to the Portfolio

FY23 Toll Revenue rises 26% Y-o-Y

Electronic Toll Collection is now ~ 95% (Fastag) The Trust has set 12th May 2023 as a record date for distribution and the same will be paid to the unit holders on or before 22nd May 2023.