This analysis is by @Karan_Dattani and not me, he was told to post these in the original thread but he didn’t, so doing on his behalf

Ion Exchange

Summary:

Ion Exchange (India) Ltd is into Water and Waste Management business. With shortage of fresh water and stricter environment norms the Industry can grow significantly. Company have strong footing in international markets particularly Oman and USA. Company has been expanding its Chemicals Business and is earning significant RoCE from the same. With segment details mentioned below you can see that company looks like a great capital allocator and have been increasing returns on Capital Employed.

As per my valuation model fair value per share of the company turns out to be in range of Rs. 600 – Rs. 900

CMP = Rs. 705 which falls under my fair value range

But there are some significant red flags for me to buy this stock. These are mentioned towards the end of the report.

Company Overview:

Ion Exchange (India) Ltd is an Indian Company into Total Water and Environment Management:

Purifying drinking water for homes communities, urban and rural areas.

Treating water for industrial process.

Removing pollutants from waste water.

Recycling and recovering waste water.

Recovering energy from waste.

Macros:

Global as well Indian Economic Growth will be severely impacted by Corona Virus Pandemic. IMF projects contraction of 3% followed by a partial rebound next year, whereas Moody’s Investor Services expects 0% growth for India followed by more optimistic 6.6% in FY2022. Investment in Infrastructure will be significantly reduces with negligible new projects and slowdown in existing ones.

Industry:

India is one of the largest consumers of freshwater in the world today, accounting for about 750 billion cubic meters annually. For a country which accounts for only 4% of the world’s water resources despite hosting 17% of the world’s population, the water crisis is looming large. The Central Pollution Control Board (CPCB) estimates that by 2030, India’s water demand is expected to rise to 1.5 trillion cubic meters. It is estimated that less than 30% of domestic and less than 60% of industrial wastewater is treated.

FY 2021 will see slowdown in capex spending, after that Industry is estimated to grow at 12% CAGR driven by strict directives issued by CPCB regarding proper disposal and reuse of sewage, necessitating construction of new sewage treatment and recycle plants in the country.

Company:

IEIL offers complete range of solutions for water, waste water management, solid waste management and waste to energy to industries and municipal corporations.

The business of your company can be segmented into:

Engineering

Chemicals

Consumer Products

Engineering is one of the key segments for the company. In this segment, the company meets the requirements of medium and small scale industries such as F&B, pharmaceutical, automotives and chemicals etc through its predesigned, pre-engineered product range for water and waste treatment. For the heavy segments in core sectors like power, refinery, steel, bulk chemicals and municipal infrastructure, it offers technologically advanced innovative and customized solutions for total water and waste management.

Chemicals: Company is engaged into manufacturing and sales of conventional and speciality resins and various Industrial Chemicals. Their products have tremendous opportunity in both domestic and international markets. Company is under continuous process of developing newer products and different applications under Chemical purifications and separation area.

Consumer Products: This segment caters to needs of Individual homes, institutions and commercial establishments. Company has a wide range of products in the market to provide safe and pure drinking water to homes, communities and institutions, under brand name ZeroB. Company has installed INDION water vending machines on number on South Indian Railway platforms.

Segment Results vs Capital Employed:

Consumer segment seems to be doing worse but once can observe that not much additional capital has been employed to the same. On the other hand Chemicals segment has got excellent RoCE and can produce exponential results for incremental capital employed. Engineering Segment is seeing raise is RoCE and PAT margins and company is increasingly focusing on “Services Segment”, being capital intensive business Engineering segment seems to require significant Capital Employed and much of the incremental capital can be deployed here as long as the company keeps generating satisfactory returns on capital employed.

Key Managerial Personals:

• R. Sharma – Chairman & MD

• Dinesh Sharma – ED

• Aankur patni – ED

• Milind Puranik – CS

R&D:

Company spends about 0.7-0.8% of its revenues in R&D activities and is quite active in bringing in new technologies and products. Some significant developments include:

Reduction of wastage in home RO from 80% to 30%

Microcarrier beads (high potential in export market) and fine grade polymeric absorbent resin (pharmaceutical chromatographic applications)

Developed a resin for separation of rhodium (potential in precious metal ind)

Polymer based antiscalent, maleic copolymer and evaporator antiscalent (cooling water treatment)

UV purifier with online and storage facility (prevents recontamination of water in storage tank)

Fluoride and germ removal

Solar based units for removal of ground water contaminants (application in rural area)

Water Vending Machine

Customised RO purifier for railway pantry car

Automatic chlorine dioxide system with acid and chlorite technology can help to penetrate disinfection market in F&B industry

Advanced membrane bioreactors for municipal and industrial waste water treatment

Subsidiaries:

Company is having 17 national and international Subsidiaries:

Aqua Investments (India) Ltd

Watercare Investments (India) Ltd

Ion Exchange Enviro Farms Ltd

Ion Exchange Asia Pacific Pte Ltd, Singapore

Ion Exchange Asia Pacific (Thailand) ltd

IEI Environmental Management, Malaysia

Ion Exchange Env Management Bangladesh

Ion Exchange WTS Bangladesh

Ion Exchange LLC, Oman

Ion Exchange LLC USA

Ion Exchange Projects and Engineering Ltd

Global Composites and Structurals Ltd

Ion Exchange Safic (Pty) Limited, South Africa

Total Water Management Services (India) Ltd.

Ion Exchange Purified Drinking Water Pvt Ltd

Ion Exchange Environment Management Limited

PT Ion Exchange Asia Pacific

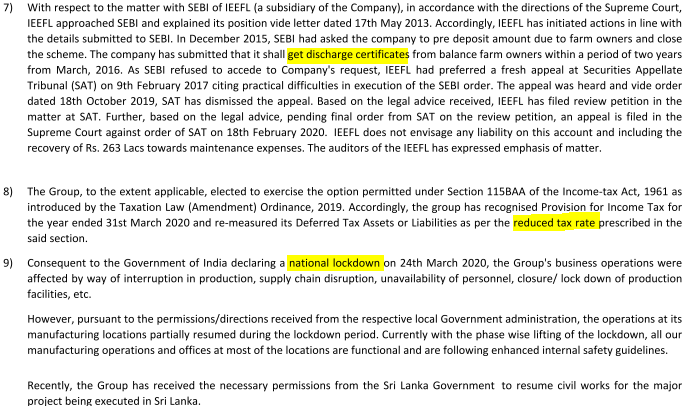

Some of the red flags I came across while studying this company

Top 3 Executive Directors salary is equal to 15.57% of company’s consolidated net profits.

Ongoing case in SAT with regards to Collective Investment Scheme ran by one of their subsidiaries Ion Exchange Enviro Farms Ltd (IEEFL).

No provisions have been created for the same.

Maintenance Expense worth 2.68 crore is considered fully recoverable by IEEFL.

No provisions have been made against the same.

All the subsidiaries combined have Accumulated Losses of Rs. 99.54 crores.

From 2018 company changed method of EPS calculations and have excluded shares held by Employee Welfare Trust which resulted into artificial jump in EPS.

Significant amount of Trade Receivables, Trade Payables, Advances Received from Customers, Loans given etc., belong to their own subsidiaries.

Aqua Investments (India) Ltd and Watercare Investments (India) Ltd have no Operating revenues. They are just carrying Investments in Fixed Deposits and some Inter Corporate Deposits.

I do not understand need of having 2 subsidiaries just for carrying investments and then charging administrative expenses against the same.

Almost all of the revenues from ‘Global Composites and Structurals Ltd’ & ‘Ion Exchange Environment Management Ltd’ and most of revenues of ‘Total Water Management Services (India) Ltd’ comes from parent itself.

Again, can’t understand need of local subsidiaries to deal with parent company itself.

Doubtful about sales of 73.81 lacs (more than 100% of its revenues) from IEEFL to Parent as IEEFL is engaged in farm produce.

Loans of 76.34 crores given to subsidiaries most of which have eroded their entire net worth but kept in business by the Company just to deal with itself and give them loans?

In year 2014-15 1 of the subsidiaries defaulted in repayment of loans and interest to banks in case of repayment of interest on various term loans aggregating to 45 lacs.

Statutory Auditors, M/s S. R. Batliboi & Co resigned in 2014-15.

Financial statement of 1 branch and 60 trusts having Assets = 76 cr, Rev = 104 cr and NP = 8.2 cr not audited by same auditors.

Financial statements of 13 subsidiaries having Assets = 126cr Rev = 130cr, PAT = 74 lac, and associates having net profit share of 57.25 lac not audited by same auditors.

This might be an opportunity, company consumer products lost ground to RO purifiers which have been declared unhealthy by NGT. They have to add back some minerals, do not know if they can do that. RO is banned in Delhi, and wherever TDS in water is below limits/piped water is supplied etc.

People are maybe taking ‘early’ announcements of results as a good sign in this bad season!

About the ban of RO, some negative effect can happen on IONEX also, but overall positive. The final notification of MoEF did come out in February but apparently the NGO which filed the case in the first place is not happy.

This may take 1-2 years before any strong action is visible which benefits IONEX.

Also, stock was trading at PE 8 which is a historic low of sorts, it has to catch up to the median of around 15.

I feel this is a good move by SC as RO leads to water wastage, plus we don’t actually need this much pure water to drink, so RO should be considered a requirement only in high TDS water areas and not as a fashion trend to follow by looking at Tv ads.

now how this is going to affect the company that we have to see. coz I see two trends here:-

People who think RO is a necessity for good health(mostly because of Tv ads) will go for RO.

People who understand RO is not necessary and leads to water wastage will go for UF+UV systems.

I have personally used Zero-B from IONEX, majority of my life, small and can use anywhere you go, no electricity required and the water still contains enough Iodine ions to be used to disinfect other things.

I don’ t think SC move on RO will affect IONEX or even Thermax, It will surely going to affect to the likes of companies in to household RO’s.

Yes RO is required based on the input TDS.

i am sharing my views and observation :

when I come to know about company : I was working with DS Group in setting up Catch natural water plant in Kullu in 1998-2000. A fresh stream of hiil spring fall of water was taken in to catchment area from there water was stored in SS 304 vertical tanks than it is lifted to first floor where we have filtration unit plant of Ion exchange In that unit we have only carbon filter sand filter and sedimentary filters . Piping is done by third party . Ozonator is supplied form third party , Fine micron filter was supplied by third party in essence only 25% of the plant is supplied by Ion exchange .

Theme of water Purification and investing in the related companies is good but what I feel that the opportunities are more but there is major share in the pie for the SME companies .

if we talk about Ion exchange from last 10 years there is no major increase in capital block I wonder how they able to rise the revenue . If they are only trading or supplying the equipment by making them from third party or importing than there are low margins and that is what reflected from the OPM .

It has lot of subsidiaries I am not comfortable with that .

ESOP is double edged sword

Trade receivables are piling up in balance sheet and are huge if one compare with the cash flow statements .

if one add up gross block in balance sheet and compare the cash flow under cash from investing subhead fixed asset purchase that is not telling the same story

Since 2017 advance taken from customer are more than the cash reserve showing in the balance sheet ??? Does it means all the surplus they are showing are actually the advance taken from the clients ??? I am confused .

Order book doesn’t mean that it is guaranteed sale or the cash realised so one should be vigilant on this issue.

disc: not invested these are my view and does not binding on individual .and this is not any stock recommendation to buy or sell or to hold . I am not any sebi approved broker or analyst

Hi @dineshssairam ,

Your research on this company is truly commendable.

After reading this thread, Dr. Vijay Malik’s analysis and doing my own research I like the company but there are some clear non trivial risks involved:

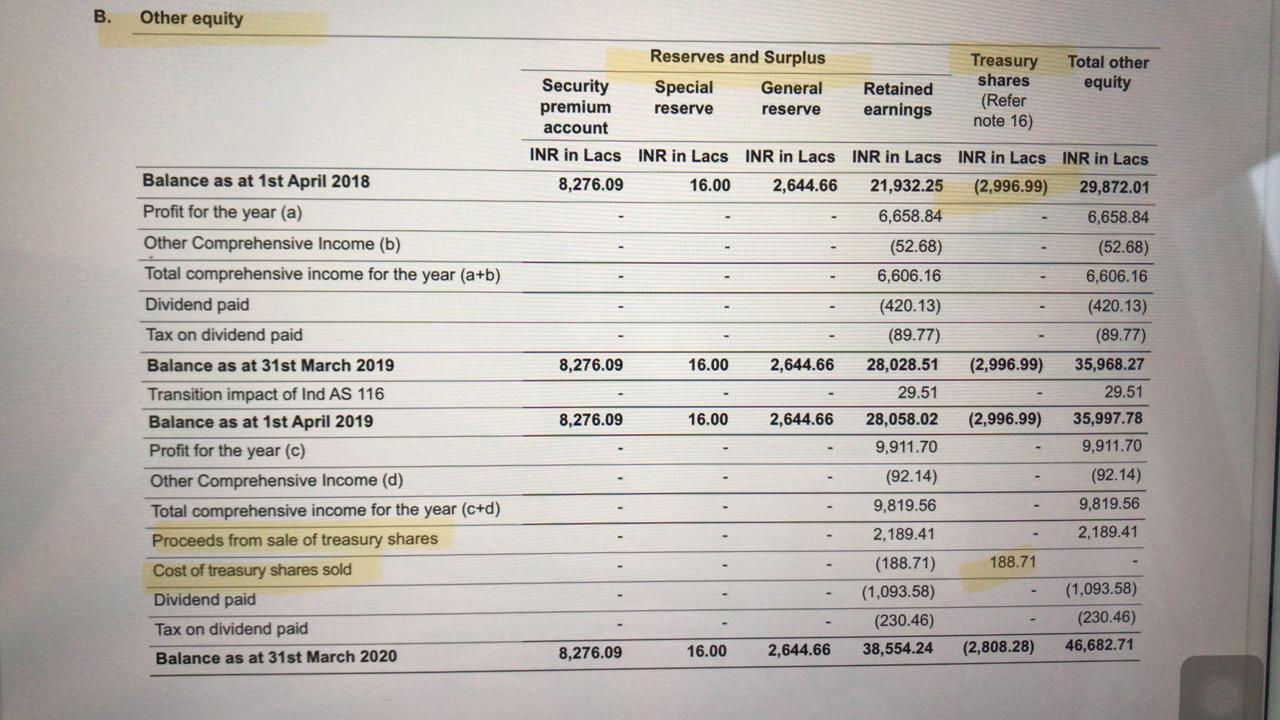

The whole issue of shares in the trust is very confusing. The outstanding shares have decreased in FY20 compared to FY19 resulting in an artificial jump in EPS. This is a bit fishy. No clear commitment from management to resolve this completely soon.

Why did the management take special permission from Govt. to go above the remuneration limit ? They already have equity. They should be interested in increasing their wealth by increasing market value of their equity. I saw the graph of the increasing trend of remuneration with sales in the thread, but even then the absolute values are still higher than standard regulations.

How is the management positive on a favourable CIS ruling ? The company has failed to convince SEBI, twice; SAT, twice; and Hon. Supreme Court, once about its position over the last 16 years. Recently, in Oct. 2019, SAT has dismissed the appeal of the company. Close to 6% of their PAT income can be affected by this

EBIT margins have temporarily increased due to Sri Lankan order. You implied margins don’t matter if sales keep increasing. Well, I think the market may want to see higher consistent margins if we want this stock to be re rated to higher multiples.

Overall, I’m still bullish on this sector so the stock can be a good bet at lower valuations but there are some clear big risks in the future.

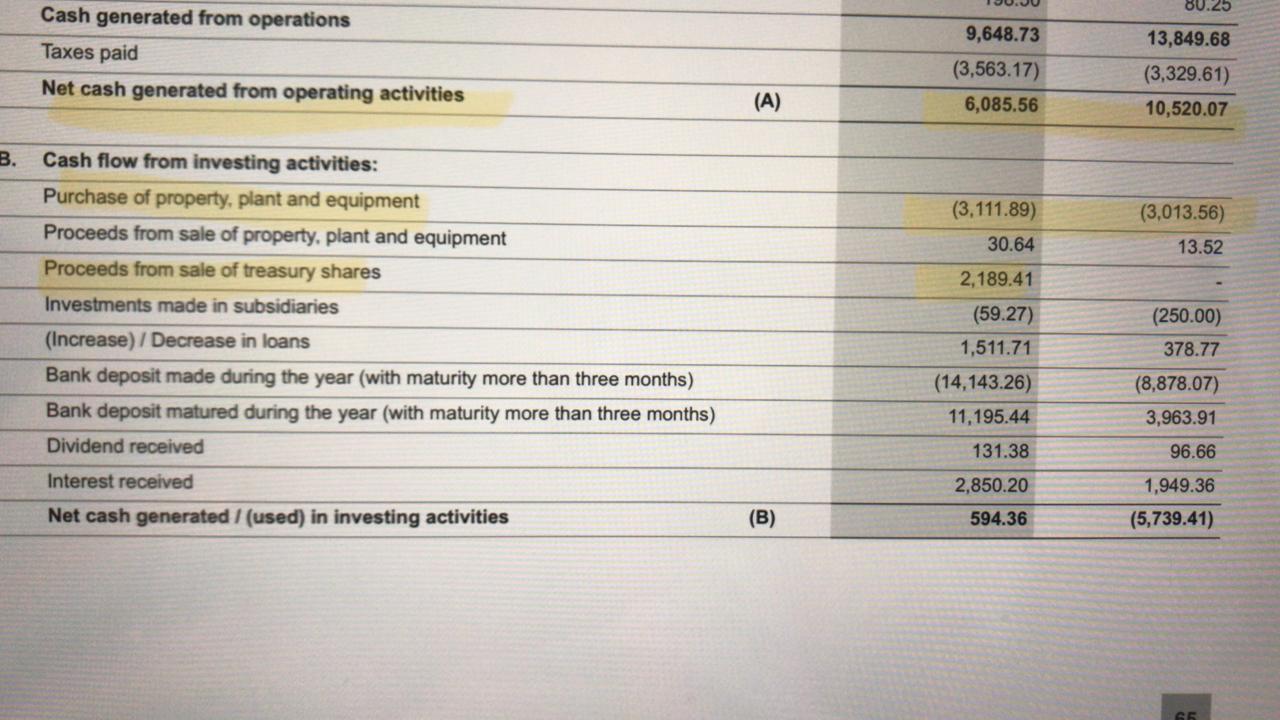

The reduction in Treasury Shares is a legitimate Accounting move. I don’t think that was a problem. The problem is in the convoluted holding structure. Once again in the latest concall, someone addressed it.

No arguing here. They screwed up once. It’s up to you to decide if you’ll allow a one-time slip up.

This is again a one-time thing. I don’t think it’s uncommon for a company as old as Ion Exchange to have Income Tax Cases against them (VST Industries comes to mind immediately for comparison). I don’t care if the company wins or loses. If the case gets over, they can redirect that energy towards the business - which is more fruitful.

I didn’t say they will increase or decrease. The Engineering division has volatile Margins. It depends on the size, length and quality of the project being executed. Executing a high-Margin, low-Revenue project is the same as executing a low-Margin, high-Revenue project. It’s ultimately about Allocation of resources. Although, sure, high-Margin, high-Revenue projects like Srilanka could help - but they’re rare.

I wouldn’t call these big risks. But Risk is personal and I won’t stand on judgement here.

I stand corrected. The Tsy shares (owned by trusts) have been marked as ownership of iON Exchange and the cash (~20 crores worth) due to the sale of some shares last FY have flowed in the company (attached screenshot). Thus, the promoter bought shares last FY via their own money and not trust’s. This clears a huge overhang.

As far as I know, they don’t. In fact, a while ago, they were talking about new Opportunities coming to them from clients looking to switch from Chinese companies. But there has been no update after that.

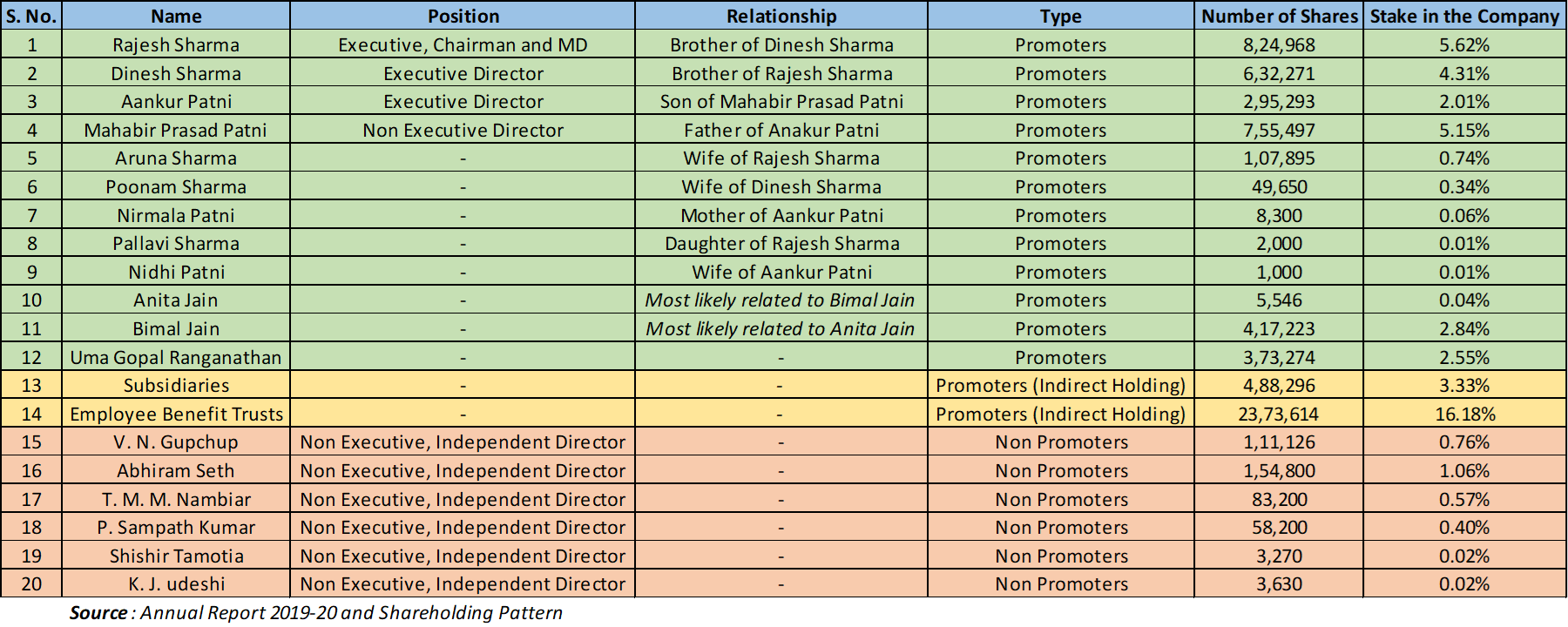

Another question: The independent directors hold a significant number of shares in the company. I have not seen this any other company as far as I remember. Is it good or bad?

The total holding of Non Executive, Independent Directors is close to 3%. Some of this 3% was to clear up the indirect holding structure, for instance Mr. Abhiram Seth’s purchase last year.

But yes, at least half of these holdings, I assume, were also allocated until 2013-14, when they were issuing massive ESOPs to themselves. Definitely a bad practice. We have discussed it multiple times in this thread.

This is the total Shareholding of all Promoters and Key Managerial Persons. About 46%.

I do know regarding the ESOP issue with the promotors but didn’t know that they allocated them to the Independent directors as well. The ESOP issue along with the fact that the company requested SEBI to exceed the 10% of PAT limit on the compensation of EDs has been a major issue for me when deciding on investing in IEIL. To top it off, the shares owned by its subsidiaries is also classified as Promotor shares in AR. So actual promotor share holding is less than 27.01%.

How would buying the shares of the trusts (which are held by the promotors indirectly) by an Independent director help the promotors? As far as I know, the money received from the sale of those shares flowed into Ion Exchange and didn’t end up in the hands of the promotors. Ideally, the promotors would want to get those shares reclassified as their own.