The subsidiaries are held by Ion Exchange and hence, indirectly by the Promoters themselves. So, they are Promoter Shares.

It clears up the clustered holding structure. That’s all I want. It helps to reduce any shareholding of the Trusts regardless of whether the Sharmas buys it or Mr. Abhiram Seth.

Since the subsidiaries are owned by Ion Exchange, the Ion Exchange shares held by the subsidiaries belong to all the shareholders of Ion Exchange, not just the promotors. The 3.33% stake must be divided amongst all the shareholders in proportion to their shareholding, hence I said that the net shareholding of the Promotors when it comes to subsidiaries portion would be less than the stated 3.33%. Subsequently, the total promotor shareholding would less than the stated 27.1%. This is what I wanted to convey.

That’s true and whatever % the Promoters don’t indirectly hold in the subsidiaries / trusts, those are held by the other Shareholders of Ion Exchange, like you pointed out. This makes them Treasury Shares, which is good.

If your contention is only on the fact that the Promoters don’t hold a lot of Stake in the company, then yes, I agree.

Surprisingly decent results, without any change in Working Capital position. It seems like they have also reduced Debt by a fair amount.

On the flip side, the management had promised that the legal dispute will be resolved this year. But it seems like the case is still going on. Not sure if COVID19 had caused any delays in this. As I remember, legal fees were a good chunk and doing away with the case will increase the Cashflows.

Decent results (see consolidated earnings) - although sales have declined a bit profitability is strong. EPS of 25 for latest quarter compared with EPS of 80 for entire FY2020.

Interestingly, one particular investor (RJ) seems to have exited after holding this stock since 2007-08. He used to have around 5.3% stake till recently. He has either exited completely or reduced stake below 1% by March 2021. Just for your information as observed.

I for one believe, the results will be good; as the demand for heavy engineering has been on a rise, due to the capex plans by 100s of companies. If you hear GMM Pfaudler’s Concall, the management has pointed out a huge demand for Heavy Engineering goods, the same is the case with Anup Engineering, Thermax, and ISGEC.

Being a strong player with strong margins in the heavy engineering segment, it seems as if Ion Exchange India Limited will give out great results this time.

Furthermore, since the government has been on the neck of a lot of companies for pollution management, the companies will have to strengthen their waste-water plants, and install new ones when and where the capex will be done.

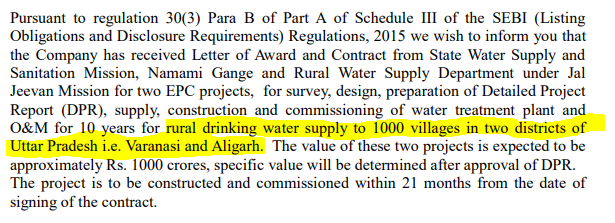

Excellent. More attractive than the contract size is the fact that they won it under Namami Gange and Jal Jeevan. Hopefully more projects similar this to come in the future.

In fact, I believe one of the asks will fall under the Consumer Division (Highlighted below), unless I am wrong.

Right, there may be involvement of consumer division in this.

The document shows that both are end-to-end EPC projects, with IEL involved from surveys to DPR to execution to O&M (for 10 years). The project has to be completed and commissioned within 21 months from date of signing of contract, assuming lead time of signing contract, this should reflect in the numbers within next 24 to 36 months. Also, these 2 projects only covers 1000 villages in 2 districts in UP - Varanasi & Aligarh, so as you rightly said, hopefully, more such projects would come in future - the potential can be massive.

@dineshssairam thanks for the wonderful work you’ve been doing on analysing this company for so long, it really becomes so much more simple for others like me. Since you have tracked them for so long, I have a specific question - are they capable of scaling quickly if there is a steady flow of projects under programs like Namami Gange & Jal Jeevan? They have handled large order from Sri Lanka govt in the past, but the opportunity from the Indian govt could be of a much higher magnitude.

The Sri Lankan order was the first one of such magnitude, unless I am mistaken. So there’s no telling how efficiently they can scale. We only have the reference of how they executed the Sri Lankan project - and rest assured, it went well.

Company guided for 20% revenue growth and stable yearly margin

• The company had a revenue of Rs. 445.2 Cr in Q4FY21 which grew by 27.5% YoY

• The geographical breakup for FY21: Domestic sales are at 58% and exports are at 42%

• The engineering segment (63% of total revenue) witnessed steady flow of orders during the quarter. Order book for engineering projects up to 31st March’21 is at Rs. 662 Cr

• Recently The company has been awarded a contract under the Jal Jivan Mission for the rural drinking water supply to 1000 villages in two districts of Uttar Pradesh namely Varanasi and Aligarh

• The value of this project is approximately Rs 1000 Cr and details regarding it will be out post approval of the detailed report and the project should be constructed and commissioned within 21 months of signing of the contract

• The execution of the Sri Lanka project improved during the quarter but frequent COVID related restrictions in the country continue to pose execution challenge.

• Order execution of other on-going Engineering orders further picked up pace resulting in improved sales and margins. The Bid pipeline project as of 31st March’ 21 is at Rs. 6000 Cr

• In the chemicals segment (30%), sales and dispatches showed continued improvement and margins improved due to higher turnover coupled with operational efficiencies

• In the consumer products segment (7%), volumes increased but was constrained due to certain segments continuing to remain affected due to restrained economic resumption in key consumer sectors and after effects of the COVID lockdown measures and continued social restrictions.

• In the chemical segment, the company had planned a capex of Rs. 100 Cr which will increase in the coming quarter for a new plan with higher capacity and details should be out in the coming quarter

• The company expects margins to be sustainable

• The chemical business has an asset utilization of 70% for the year