analysis by Vijay Malik

10 Likes

Very indepth analysis by Dr. Vijay Malik. Highlights the continued problems of capital allocation. Merger/amalgamation of loss making group companies has been a recurring event, in many cases resulting in increase in promoter stake in Ion Exchange. The company has also transitioned into a majorly promoter driven company from being a professionally driven company earlier. The new promoters have been gradually working on increasing stake through various direct and indirect means, not void of conflict of interest in some cases. The legal challenges of the past remain an issue and are likely to result in a ~50 Cr. impact on P&L sooner or later.

Today, government launched Atal Bhujal Yojana.

The water treatment segment has a lot of focus from the government but the listed companies in this segment are throttled by their own issues. Va Tech Wabag also has been suffering from debtors collection for Govt projects. Thermax has only ~10% of its business in this segment.

Any cleaner well managed companies in this segment which will be able to leverage the upcoming opportunities?

3 Likes

I will try to respond to the analysis made by the Dr. without any bias. But I do hold a considerable stake in Ion Exchange, so please consider my views in that light.

1. Susceptibility to Economic Downturns: Maybe true in the past, when the government had little to do with water management and all the projects originated from the industry. But this is changing now. In fact currently when there’s a pronounced slowdown in the Indian economy, Ion Exchange is doing very, very well (Even if you ignore the Srilankan order, their Sales from other orders and the Chemicals division has been impressive).

2. Margins may fall back after Srilankan Order: Impossible to guess. But I honestly do not mind even if the Margins shrunk. The company had good RoIC even before this project. Now if both Sales and Margins shrunk, we’ll have a real problem on our hands. But according to management commentary, this seem very unlikely.

3. Entry Barriers are Low because of high NFAT: True generally for most businesses. But I think Opportunity Size is too high for this to matter (Remember, the GOI’s budget estimate for EPC projects is Rs. 6,30,000 Crores). Plus, beauty is in the eye of the beholder. High NFAT also means higher FCFF conversion. Presenting a high NFAT as negative-only seems a little contrived.

4. High Receivables Days: We have already discussed this in this thread. Looking at Receivables Days alone can be misleading. Cash Conversion Cycle is the one that should be looked at. Historically, Ion Exchange has been able to maintain a CCC around 30 days. If you don’t trust me, compare the Debtors Days in Screener for Ion Exchange and VA Tech Wabag. VA Tech Wabag actually has better Debtors Days than Ion Exchange. So then why is VA Tech Wabag facing the heat and Ion Exchange not? You’re right. VA Tech Wabag has had almost double the CCC of Ion Exchange for some time now.

5. Large ESOPs / Share Allotted to the Management/Employees directly/indirectly: This is a legitimate concern that we have already discussed in this thread. This was done until 2012-13. Currently, with the clean up going on with the convoluted holding structure, we can hope that this won’t repeat. Of course, we should keep an open eye should it repeat again.

6. Low SSGR in the past: Again, true in the past. I don’t see this happening in the future. But let’s see.

7. Debt not Repaid despite Cash: I think this was a direct question to the management in one of the concalls. In fact, since I hold a couple of B2B businesses, I can assure you that all of them are more or less protective about their Cash balances. It’s just the way the B2B business rolls. You can’t be caught with a Cash crunch during a down-cycle. It will wipe you out.

8. Transition from Professional Management to Family-based Business: True observation. I don’t see the problem, however.

9. Convoluted Holding Structure started by Permutit’s handover: Discussed in detail in this thread. I believe the clean up is happening now. But it was definitely a bad move in the past.

10. Legal Disputes / CI Scheme: Legitimate concern. I had highlighted this as a primary concern in my presentation. You take any company as old as Ion Exchange is and you will find some legal dispute with the Tax authorities in most of that. I don’t think this is out of place. But the one observation about delayed payment to the government is legitimate. Regarding the CI Scheme case, it should be over within a year. The management indicated a positive ruling, but we shall wait and see.

11. Capital hand-outs to Subsidiaries: I had highlighted this as a minor Risk in my presentation. It should be noted that in a Holding company structure, the better-placed Parent company often takes loans on behalf of the subsidiary and then hands it over to them. This gives better Credit terms than if the Subsidiary itself applied for a loan. Despite the losses in 2-3 subsidiaries, the overall Growth / RoIC from both the Engineering and the Chemicals divisions has been fantastic.

12. Consumer Division: Legitimate concern. We all have it. But funny that he mentioned the % for the above point, but failed to mention that Consumer Division constitutes only 10% of Sales.

13. Remuneration in Excess of Statutory limits: I believe this was a single standalone instance. Someone posted a historical analysis of Management Salary Vis-a-Vis Sales Growth in this thread and I believe it is in line.

In my eyes, the biggest concerns are only regarding the Legal Dispute and the convoluted holding structure. If we are to believe in the management, both of these are getting addressed. But if you are really someone turned off by even the smallest capital allocation slip up, then it is true that Ion Exchange may not be the best investment for you.

18 Likes

1 Like

Management interview on CNBC. Would have loved if they had discussed more on the business and sales aspects. But it appeared to be more about projecting.

Regards

Divyansh

Disc: invested from lower levels

1 Like

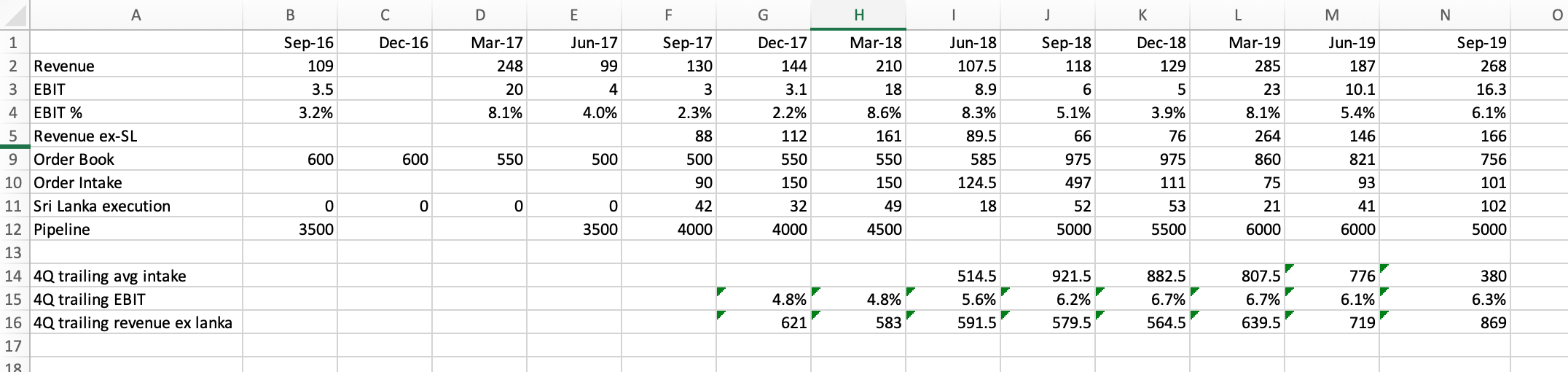

There are a lot of useful numbers reported for the engineering segment in the Ion Exchange concalls. I have created a tracker of some of the metrics I thought were important - order intake, bid pipeline size, S. Lanka executed, etc

Few insights:

- Increase in bid pipeline has not led to increase in intake

- EBIT margins of engineering division have shot up as 4Q trailing revenue has increased beyond 500 cr. Conversely, a fall in engg revenue will be a double whammy - lower revenues as well as lower margins

- 12 month trailing order intake is at its lowest point in 4 years in the Sep-19 quarter

- The big Vedanta order in Sep-18 is started contributing from Mar-19. However, it will not last more than a couple of more quarters.

Given the big run up, the engg division needs to land at least 200cr of orders per quarter if ION Exchange is to continue its dream run. The chemical division cant do all the heavy lifting.

Disc: > 5% of PF

5 Likes

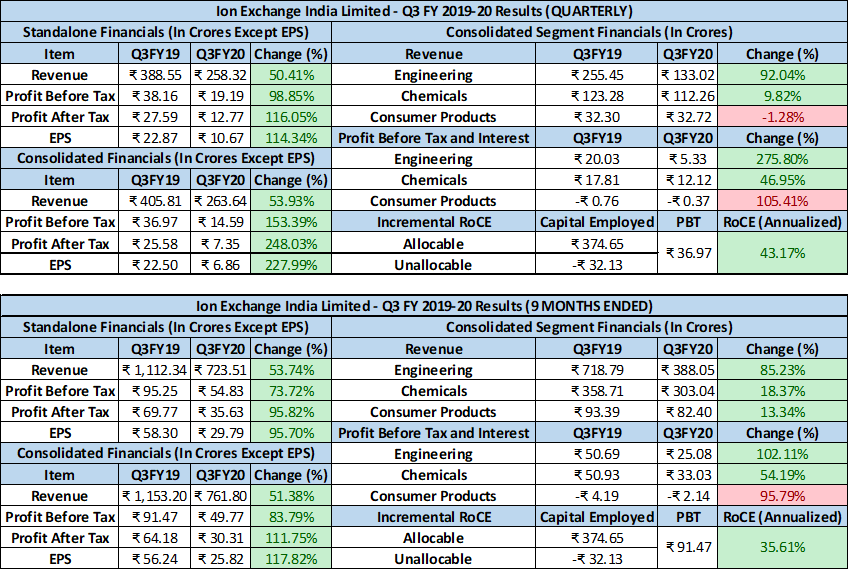

Results

https://www.bseindia.com/xml-data/corpfiling/AttachLive/08bada5f-71f3-4039-a98a-115c4b859f1f.pdf

Consolidated

Revenues up ~54%

PBT up ~153%

PAT up ~248%

EPS up ~228%

Edit: In case you haven’t already noticed, “Q3FY19” and “Q3FY20” are swapped. Pardon the error.

Investor Presentation

https://www.bseindia.com/xml-data/corpfiling/AttachLive/5671fee0-c47c-4b0d-a42b-4542b08d3398.pdf

12 Likes

what does the order pipeline look like after srilanka and vedanta?These were big ticket orders and I believe were the major reason for the increased interest in this company in the last 6 months.After the completion of these if there are no big orders,the growth might taper down.

Currently there are no new big orders. We will get to know the Order Book details on the upcoming concall: https://www.bseindia.com/xml-data/corpfiling/AttachLive/1d9d297f-29d7-4686-8b79-cb8768aa4280.pdf

there is capacity CAPEX done when net-fixed-asset-turnover (NFAT) ratio is not looking good … could you please clarify

When company has done the CAPEX, new capacity addition won’t be optimally utilized thus because of lower net sales for the same plant,equipment which normally company does, NFAT will be lower than normal and if everything is alright then it will reach to normal levels or even better in due course if CAPEX was done to improve the efficiency.

1 Like

Concall Transcript - Q3 FY20

Guidance: High Double-digit Growth guidance maintained for Q4FY20. Guidance for FY21 to be shared next quarter.

Order Book: Rs. 766 Crores (Ex-Srilanka) + Rs. 588 Crores (Srilanka).

Bid Pipeline: Rs. 5,000 Crores (Expected conversion 20%. Conversion will happen within the next 2-3 Quarters or so). The composition is more towards Zero Discharge / Waste Treatment.

Engineering

- Enquiries are going on for a large orders, but large orders take a lot of negotiation and gestation period before they get confirmed. The management did not want to commit any information as of now.

- Economic Growth directly impacts the Engineering Business. So the pickup in the Indian Economy (Which the company expects to happen next year), should impact the Engineering Business positively. The lull in the Order Book can be attributed the slow growth in the economy.

- Ex-Srilanka order, the 9-month Engineering YoY Growth is 41%. Growth is attributed to faster execution of the Order Book.

- Majority of the Srilankan order will be completed by the contractual date of May 2020, but some extension may happen based on mutual agreement with the Srilankan Water Board. Completion for Q4FY20 to be likely ~Rs. 200 Crores.

- Management in touch with Municipal organizations. But they are very specific about the terms of the agreement.

- Scale enables the company to bid for larger projects. Executing large orders like the Srilankan one improves their chances of converting such large projects. But eligibility criteria will differ from order to order.

- Engineering projects don’t need any specific capacity / plants to be put in place. The investment is more on manpower / engineers, which is what the company has spent on recently. The Srilankan order team consisted of some of the top management from IEIL, but mostly Contract Workers from Srilanka.

Chemicals

- Resin Capacity Utilization is close to 90%. Resin constitutes 60% of overall Chemicals Revenues.

- The Opportunity Size for Resins abroad could run into more than $1 Billion / ~Rs. 7,000 Crores and the market is ever-expanding. Domestic Opportunity Size is only Rs. 300-400 Crores. Some major competitors for the Domestic Market are Thermax and Octel.

- Regular Capex of Rs. 50-60 Crores for Resins to continue. A big Capex (A new greenfield expansion) is in review, but no decision as yet. Some of the new capacities should go live soon.

- Growth guidance for Chemicals division is 15-20% going forward.

- Membranes potential is promising (Opportunity Size is “pretty large”). Capacity utilization is 40% and to reach 50% by the year end. But no specific guidance.

- Chemicals Margins have increased (Recent Quarter number is 16%). The management expects this Margin level to be maintained.

Consumer

- Turnaround guidance maintained. They are focusing on “specific market segments”.

Others (Actually just my questions)

- Confirmed that the transfer of shares from Trusts to Promoters is because of the SEBI re-classification.

- No comment on whether all such shares will be transferred completely. Decisions to be taken from time to time.

- The loans given to Ion Exchange by Permutit when the former was set up in India still exist on the Books of the company, but they are small in size. Some of the loans have been repaid.

There were a lot of boring questions on specific numbers from the P/L or B/S, which I have taken the liberty to not transcribe.

14 Likes

Hi Dinesh, always been an admirer of your analysis and writing. Any idea why the promoter stake has gone down sharply?

It has not. SEBI reclassified shares held by Employee Trusts from Promoter to Non-Promoter.

4 Likes

Positive development for most water players. But it remains to be seen how the terms of the business / contracts will be for the Jal Jivan mission.

3 Likes

Con call transcript for Q3 Fy20 results:

I see concern about sustainability of current momentum.

Resins growth is constrained by capacity and will be around 20% till the greenfield project gets planned. Revenues of 100 Cr per quarter is a good estimate.

Overall chemicals (incl. resins) contribute 150 Cr with 15% CAGR expected.

Engineering wise they can hit 400 Cr per quarter.

So overall decent enough projection, if they can exceed in margins or revenue wise, would be pretty good.

Consumer biz would add 50 Cr, with optimistic mgmt outlook.

Disc: 5% of portfolio, since a month ago.

1 Like

Hi, I was looking at screener for Ion exchange and observed promoter holding reduced to 27%. Does anyone know something going on with the company. Screener shows Promoter holding has decreased by -17.03% over last quarter

1 Like

refer this just 3 posts above:

3 Likes

Hi,

Please refer to further analysis by Dr. Vijay Mallik

5 Likes