Quite an interesting development, Indigo is looking at different ways to raise fund.

some news and trends in airline industry

disc : Not invested , this is not any recommendation to buy sell or hold

INDIGO reports a loss of 2800 crs. It took them 10 yrs to build a reserve of 5600 and just 60 days lockdown wiped off half the networth. Airlines is indeed a tough business.

Indigo is going to raise 4000 cr. by issuing equity through QIP.

How this is supposed to add value to the shareholders ( mainly to retail investors ) ? . What I learned from investing is that the rise of debt / dilution is equity in long term is not beneficial for the investor it added additional risk parameter as another variable ( I may be wrong in my perception as having limited knowledge )

disc: watching not invested .

Concall highlights:

- Yield is up by 9% but load factor is down by 18.5% leading to reduction in RASK of 5.4%

- Before going for equity fund raise of 4000cr., want to explore all debt options. On the basis of current revenue improvements deferring the decision for QIP until the end of 2020

- Stable liquidity condition as of now and have made all the lease payments (fixed cost) without any deferrals

- Current domestic capacity operating at 60% and should go up to 80% by end of year (depending on government approvals)

- Average cash burn was 25cr/day this quarter (vs 30cr/day last quarter)

- Sold and leased back 4 ATR and 3 CEO planes to raise liquidity; plans to sell and lease back more aircrafts

- Plans to return all the CEO planes and replace them with more fuel efficient NEOs

- Pre-covid corporate travel was ~50% of total travel

- International operations: Only focused on narrow body planes; will not go into wide body until see positive numbers from it (although prices have come down for wide body planes)

- Residual values have gone down for wide body planes, but the prices of narrow body planes have been largely stable

- Until 2023, will accept new planes and continue retiring CEOs decreasing overall fleet count slightly. After 2023, fleet count will increase

- Cargo revenues doing very well YOY; don’t give revenue breakup into cargo and passenger; most of the ancillary revenue comes from cargo

Disclosure: Invested (position size here)

Any question/comment in the concall regarding the impact of the current fare cap by the Govt? Looks like its extended till Feb end of next year.

Q3FY21 Concall update-

- Co operated @ 70% of its last years domestic capacity in Q3 & is currently operating at 80%. International capacity deployment stands at 28% as on date.

- Co seems to be operating at 70% of its overall pre-covid capacity.

- Daily Cash burn has reduced from 40cr in q1 to 15cr in q3.

- Co expects to reach 50% of its pre-covid international capacity by mid CY & 100% by CY end. CEO mentioned strong chances of important markets like saudi,bangladesh, srilanka etc opening up soon , these would have opened earlier had it not been for the fear around the UK & South African strains.

- Co seeing strong profitable demand domestically in Tier 2 & 3 cities. Metro to metro routes continue to be challenged though.

- Co intends to ramp up capacity as soon as possible as it currently is able to only fly its aircraft on average 7 hours a day , it used to be 13hours earlier. While IndiGo has been circulating & maintaining its fleet the cash strapped competitors were forced to ground some aircraft for months. These will need maintenance & repair before they can be re-inducted in their fleet. Supply from competition would be ‘muted’ in the short term.

- Co doesn’t intend to go in for the QIP.

- Co sees strong revenue from Q1FY22 as a lot of the routes co has launched would have had the necessary booking window to optimise revenue.

- Co is seeing strong cost savings in fuel thanks to its more fuel efficient NEO fleet. 65% of its total A320 family aircrafts are now NEO.This should become 100% by Dec22.

- Cos strategy is to ramp up capacity at the earliest & become profitable. Co believes in low fares & does not believe in a high yield environment sustaining in a cost conscious market like India.

- Co is seeing strong diversified demand from across India in non metro markets & believes the market in metro should improve soon.

- Corporate travel has been doing well in the SME side & co has seen corp travel from core industries return to 30% of earlier levels. Travel from the IT , consultancy remains subdued. Based on its interactions mgmnt believes corp travel should return to 70-80% levels by Q1FY22.

Board approves QIP worth 3’000 cr.

Disclosure: Invested (position size here)

Not directly related to indigo. This post is about SpiceJet.

Also found that author of above post has site dedicated for aviation industry content.

discl - not invested in any aviation stocks.

This here is BS of Indigo.

The reserves have been wiped out.

Finance exp is around 560 cr and Depriciation is almost 1200 cr which may keep increasing.

Sadly coz of Omicron this qtr may also be a washout.

The market cap of this company is at 73,700 cr…

The stock price recently in Nov made an all time high. Who is buying at these levels and whats there rationale.

Does any of this makes sense…

Disclosure: Ofcourse i am not invested. ![]()

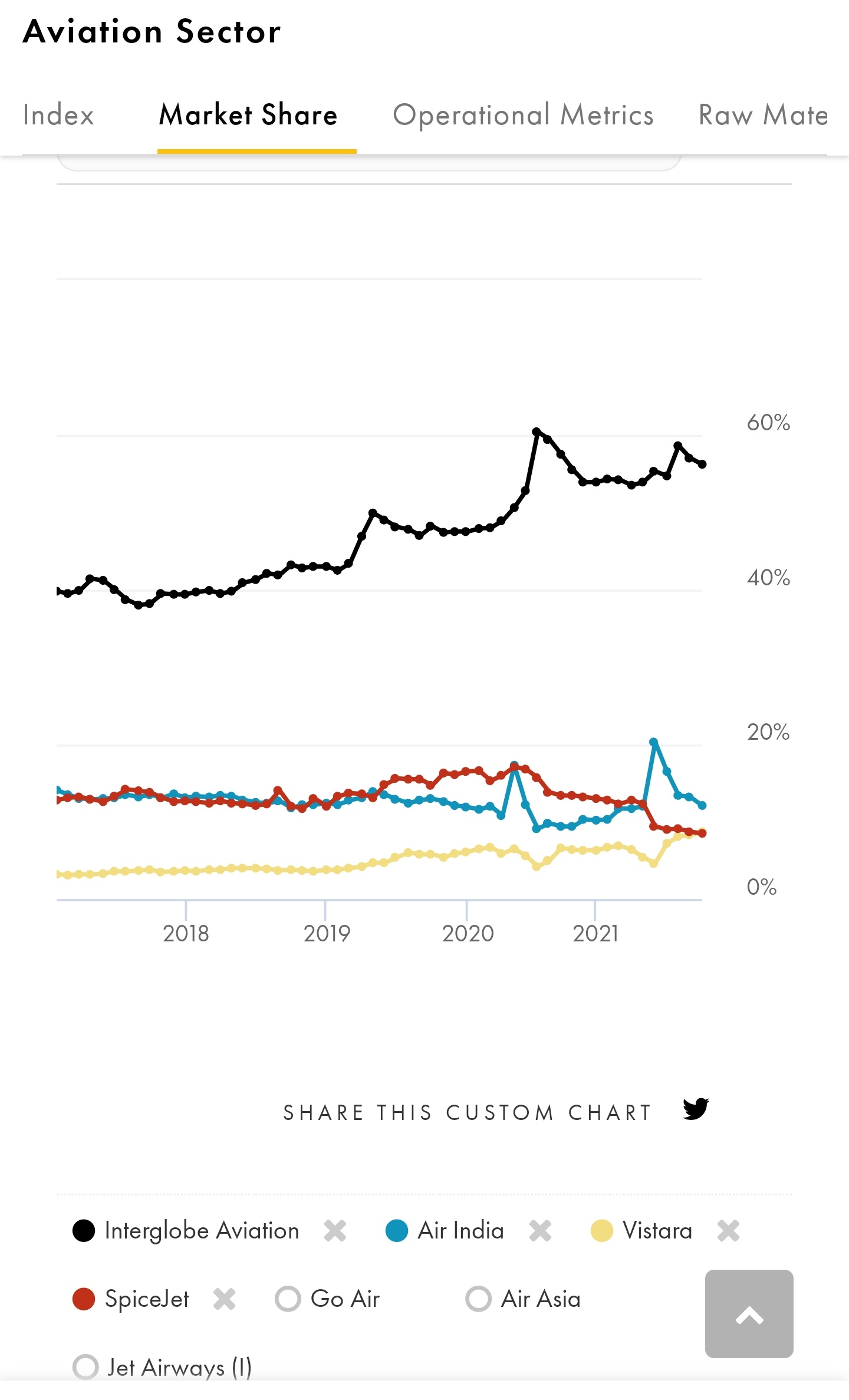

Indigo’s valuation is supported by its competitors weakness & not solely it’s balance sheet strength.

It is clear that air travel is here to stay & Indigo will be the last man standing.

Poor show from Interglobe Aviations (Indigo). Loss of 1500 crores? What happened here? I thought they’d be profitable with such an amazing quarter for tourism… I sense some massive beating.