My understanding of Aviation accounting is a work in progress.

Would seniors with better understanding shed some light on the following query.

The (non cash) forex losses in IndiGo’s $ lease liabilities are expensed from the P&L on a quarterly basis , is this a good accounting practice?

As the Average tenure of these lease is 6 years, should’nt the forex adjustment be spread over the lease cycle? The fall in currency anyway gets passed on to the consumer as higher ticket prices. The Rs. has fallen by a third since 2014. Although IndiGo flourished during this time frame , if someone had only read its P&L(as per latest standards) they would be utterly confused.

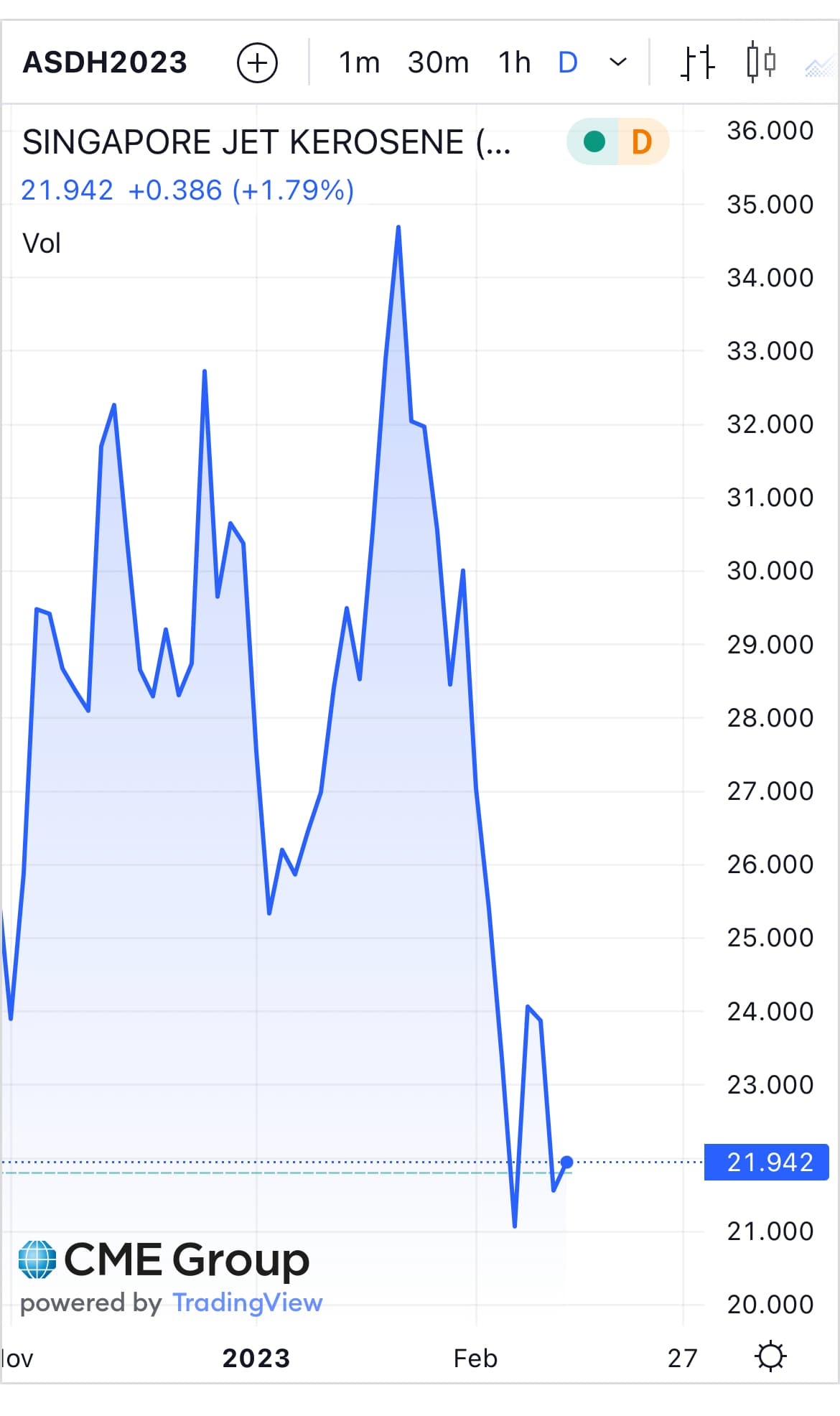

The first chart shows the feb 2023 data for Singapore benchmarked ATF crack spreads & the second chart is for march.The MOPAG pricing that India has recently adopted for pricing ATF domestically follows this benchmark & is a big change from the previous opaque PSU cross subsidised pricing mechanism.

ATF prices in india have been trading at 120$ crude equivalent till last month since crack spreads for middle distillates(ATF) have been abnormally high due to “supply chain” issues. A reversion to mean as indicated by the charts can mean a big boost for Indian aviation.

Heavily consolidated market,Cost leadership,Order book visibility till 2028(while everyone else is buying expensive planes in a Sellers market),Most competition has impaired balance sheets, with all this , a reduction in fuel cost !!

Looks like a Lollapalooza for IndiGo?!

Discl- InVested. Would love any feedback which wrecks this “theory”

Hope they don’t remove the crucial manuals that are necessary in case of emergencies. No matter how wonderful and easy the electronic gadgets are to work with, we cannot deny the possibility of them stop working, and these are planes we are talking about, only they can help themselves up in the air, in extreme scenarios.

I am sure people who run airlines know about this, just saying, because it is one thing to remove or make things weigh lighter to conserve fuel and make some profits, but news like these don’t sound good.

No investment, not following, had a position in the past.

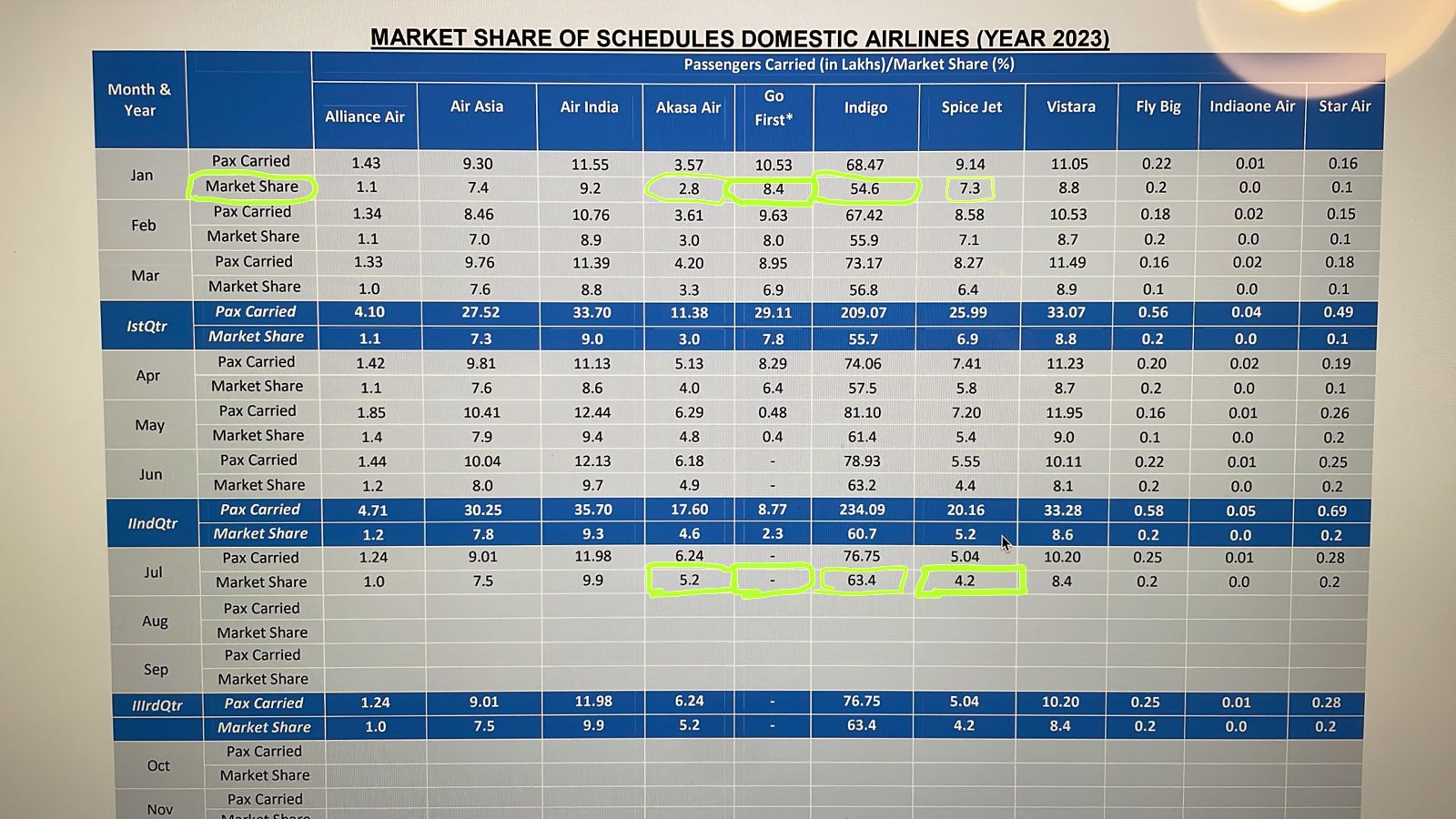

Before GO, GOing , GOne happened 4.5 Lakh passengers flew daily(domestic). Industry capacity was at 4.9Lakh which now stands reduced to 4.6L . Prices have sky rocketed naturally & daily passenger count has fallen to 4.25L . Meanwhile ATF prices in india which are tracking MOPAG have fallen 18% this CY. Stars seem to lining up for another record quarter.

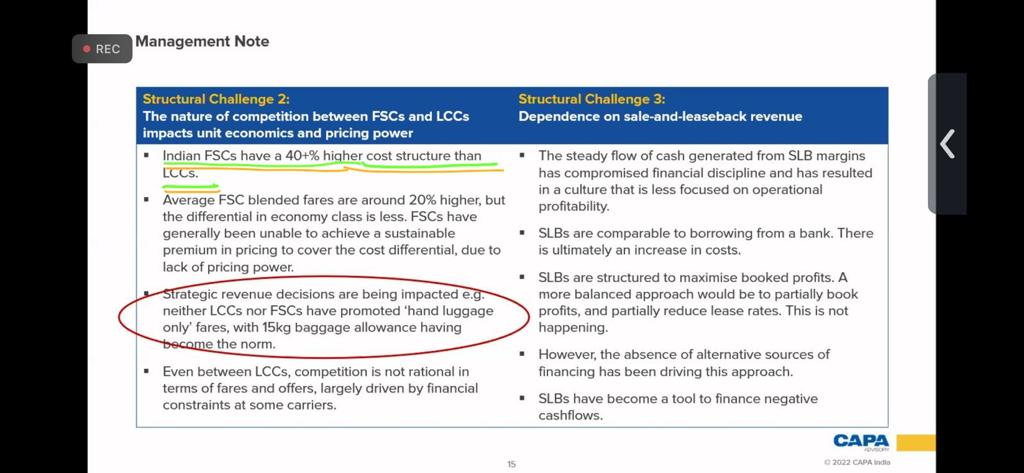

The difference seems to be blurring between LCCs and FSCs in terms of fares. How is IndiGo different there? We have a fully automated process, which doesn’t need human intervention and knows how much inventory we have. Flights get opened several months in advance and the machine decides how the inventory is to be sold the day it gets opened. As you get closer to the day of departure, the machine determines what the fares would be. The machine develops artificial intelligence over a period of time. Say, for a Delhi-Baroda flight, which has been in operation for five years and flies at the same time, the machine knows what the flight looks like every single day. So the machine looks at December 1 and, what is sophisticated is that the machine will determine by looking at the data of the past five years how that plane has performed on that day every year. So the machine might like to hang on to a little bit of inventory close to the departure and sell it later for a higher price or may sell all tickets on a cheaper price in advance thinking that there won’t be an opportunity later.

.

…

…

…

…

The article is dated 2011

Agile Airport Services Ltd , IndiGo’s sub that takes care of ground handling did 512cr sale & made 11cr PAT(9cr last year)Interesting how a cost centre has become a Profit centre.

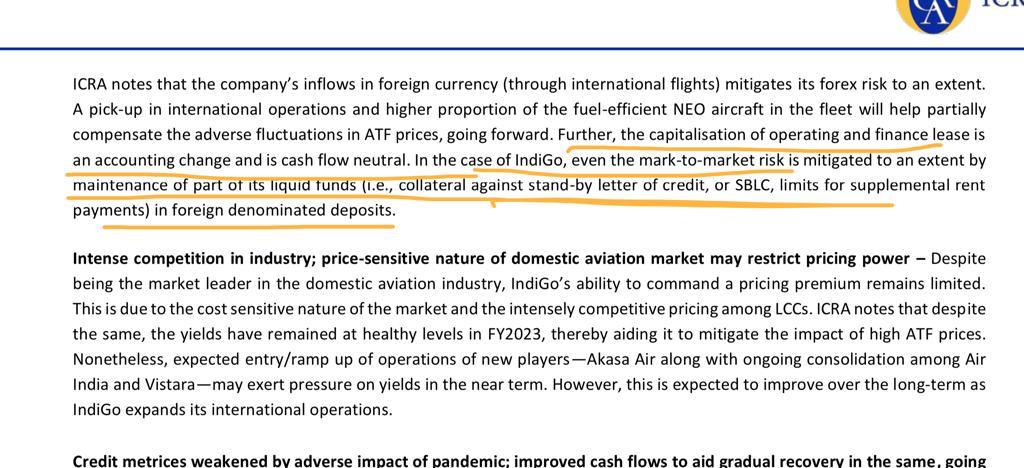

Forex Earned = Rs. 8,138cr & Forex spent= Rs.19,172cr , As the International contribution to sales increases The Forex volatility(Non cash item) will get hedged naturally to that extent. PFA ICRA’s rating upgrade which mentions this point in detail.

Operationally company continues to build on its efficiencies thereby increasing the gap between it & the next best player. All the new planes are coming with CFM engines , latest PW issues will not affect growth going forward.

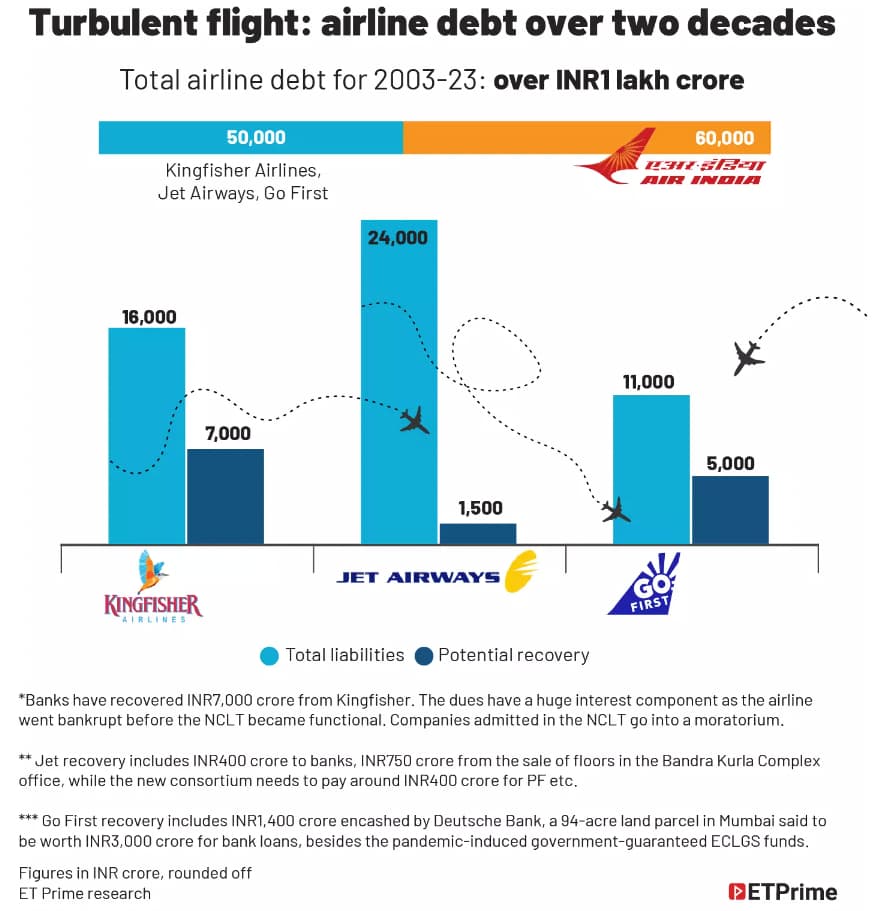

Recently, Akasa Air stated that it is in a state of crisis and might shut down

after 43 pilots left the airline to join a rival group. Well there is nothing new in Airlines shutting down in India. With poaching of pilots to a huge pile of debt overhead, lets take lessons from the demise of India’s private airlines.

Sanjay Kumar Ex-CRO IndiGo on the CAPA call also mentioned that the Cost difference between IndiGo & the next LCC is 25%. In Aviation , being the lowest cost provider is the only MOAT there is ! Ask the many billionaires who thought otherwise