Hi,

Any response from the management?

Hi.

None as yet. 3 emails have been sent and no reply as yet. Quite putting off I would say!

Right… This does not give confidence on the company’s CG

Innovative Tech Pack Ltd has informed BSE about “Intimation regarding change of Corporate Office of the Company”. Could that be a fallout of the mail sent by v31?

Wow Amazing…  it still does not clear the corporate governance red flag raised, though it does in a way vindicates our research. Well done everyone

it still does not clear the corporate governance red flag raised, though it does in a way vindicates our research. Well done everyone

3 Likes

According to AR16, the promoters earned salaries to the tune of 39 lakhs and 15 lakhs which, as a percent of PAT, are 11.5% and 4% respectively. Aren’t these numbers very high?

As per company’s law, a promoter can draw salary upto 10% of PBT. So the metric has to calculated with respect to PBT. PBT as per company’s act includes director’s remuneration to the reported PBT. So basically you need to add back the promoter’s/director’s remuneration to the reported PBT and then calculate the take away salary of that PBT. If it is less than or equal to 10%, it is a legal take-away

new plant operational in baddi

http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/7a4af148-33e8-4fed-8f1e-1000dfb2640e.pdf

1 Like

Company has won order from bisleri to make caps…

Will add considerable revenue to the toplline for next 5 years

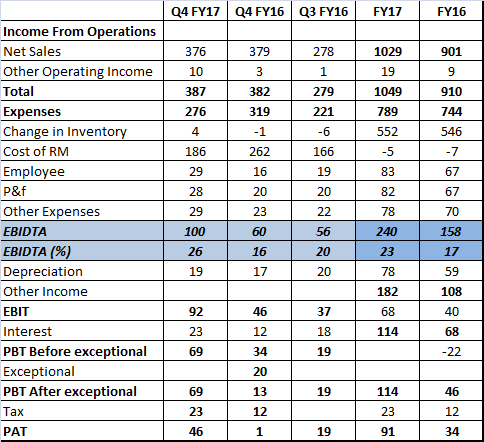

Financial Table

-

Top line has grown 36% qoq and 63% yoy in Q4 FY17 (yoy is adjusted for Rs 14.81cr turnover reported in Q4 FY16 as trading turnover. Same was classified as trading turnover apart from normal business activity in notes to result) . Similarly, Sales grew 54% yoy in FY17 (adjusting for same one time trading activity)

-

ITPL registered highest ever EBIDTA margin at 26% in Q4 FY17 and 23% for the year as a whole. EBIDTA has grown 68% yoy and 78% qoq in Q4 FY17 and 52% yoy in FY17.

-

This year was finally without any exceptional item (which was the norm earlier :-)).

-

Fixed assets have grown from Rs 24cr in FY15 to Rs 59cr in FY17. LT debt in the same period increased from Rs 7cr to Rs 27cr. Thus capex has been well funded. Sales are likely to be robust going ahead with ramping up of capacity utilization.

-

Net working capital continues to stable (with higher sales).

Company has put in good capex without stretching balance sheet, while core numbers continue to be impressive.

Disc - Invested

2 Likes

Hi Nirav,

Yes, very good nos! Finally the positive outcome of expansions and several orders wins by the company are bearing fruits. Like you have mentioned the best part is that all of this has happened without stretching of the balance sheet.

The margins of this quarter look quite high from the norm and may not be sustainable. Lets try to dig more on the same. Couple of the possible reasons for expansion of margin could be - 1. Reduction in trading business which would not be giving much margins 2. they have shifted 2-3 factories to one self-owned premises and perhaps this could have led to better planning and production, saving on rentals etc?

Also, have they hit the maximum possible utilization?

Regards,

Ayush

6 Likes

Hello Sir,

Its true that the current capacity and subsequent orders from players like - Dabur, Marico, Bisleri, INBISCO place INPACK at a very sweet spot, especially the proximity between the Baddi & Guwahati plant and Dabur’s 16/29 manufacturing units in Baddi.

But it would be very interesting to know what is the revenue contribution by Top 3 or Top 5 supplier, before 2016 and later after the company starts to realize these contacts into revenue - which it expects to do in 2017.

Sir did you have any idea what that might be (if you had a chance to talk to the management)?

In addition, with the kind of structure of contracts that the company has established with its customers (most of them) - the company has the ability to transfer any rise and fall in PET prices to its customers, hence what really is at focus is the ability of the company to increase revenue by executing existing contacts, and get new ones.

Also the company has majority of its presence in FMCG, followed by Pharma, FMCG as an industry is the most dynamic in its packaging - with requirement of continuous change in its packaging with a large variety of small quantity selling goods bearing different packaging. In view of the importance of packaging for FMCG Industry, many packaging players who were earlier in packaging for Industrial and Heavy Goods are getting attracted to FMCG packaging - one such example is Mold-Tek Packaging Ltd. which earlier was focused on packaging for paints, lubs, chemicals … and is now trying to get its grip better on FMCG.

INPACK’s complete focus and existing experience also gives it an upper hand on such competitors, however it would beneficial to keep track of developments of such competitors.

In a recent conversation with CS, I got to know that along with INPACK one more company won the Dabur PET supply contract - the company’s name is Varahi Ltd, this company was then taken over by Manjushree Technopack (got delisted in 2015). Manjushree Technopak is a very big incumbent in the industry (Revenue of around 800 Cr) - and has focus on FMCG and Pharmaceuticals. The company earlier has its main foothold in Southern India, but with Varahi the company has started to compete in Northern Part as well.

Dabur currently contributes 40% of INPACK’s revenue and the top 3 clients contribute 65% of the revenue, I think revenue concentration will increase once the big contracts start contributing to revenue.

Hi,

Company has reasonably firm plan to enter West & South and as per announcement made in November 2016, company has already received first order from INBISCO India Pvt Ltd (Ahmedabad, Gujarat). Once numbers start flowing from West & South operations, concentration is likely come down. Till then yes, Top 3 clients will contribute large part of sales. Client addition is key, since its largely volume driven and competitive industry.

3 Likes

Great thread and lot of good discussion.

The thread on Manjushree Technopack would be a good reference point to understand this business and nuances in greater details. I will highlight certain pointers in couple of posts from that thread.

2 Likes

In summary:

This is a surrogate play on the FMCG growth. The packaging companies are 'price-takers" working on cost+ basis and do not have any pricing powers.

These business will always need to fund capex for expansion - so growth will come with a deteriorating balance sheet, unless companies pause to consolidate, in that case growth will take a back seat.

As capacities are mostly linked to clients, fixed costs can wreck havoc and take a small player to bankruptcy (something that happened to JHS Svendgaard and P&G in the Gillete case)

JHS, which had signed the agreement with P&G in 2010, claimed that termination of the P&G contract had caused huge losses to the company and it was on the verge of bankruptcy. The company had to build its manufacturing capacity (or change the machinery) according to P&G’s requirement and those could not be used to produce products for any other company, it noted.

So these businesses, needs to be bought at very low PE, with adequate margin-of-safety and can be cashed out at a higher PE. Something exactly enacted by @RajeevJ .

it falls in ice-cream category business - You buy it historic low-pe and sell it at fair p/e and get handsome returns very quickly (before it melts).

7 Likes

Hello Sir:

As correctly mentioned by you that INPACK is a surrogate play on the FMCG growth, but it also is a play on the promoters ability to get contracts (in past 2-3 years, the promoter is trying in every which way to get contracts - which can be seen as a result in the new contracts), with proper execution I think the company will create a name for itself which it could later pitch to others ?

The risk you mentioned with JHS (P&G Contract) is completely valid, and even INPACK’s revenue is contributed to large extent by Dabur - mainly from the Baddi plant, along with a minor contribution by Marico.

Although I did add a small tracking position  (Close to 75) in the hopes of revenue increase from the contracts and beyond these contracts, with the comfort that the company will maintain margins (at least better than before, with these arrangements), but thanks for the heads-up (will try to buy at low PE next time).

(Close to 75) in the hopes of revenue increase from the contracts and beyond these contracts, with the comfort that the company will maintain margins (at least better than before, with these arrangements), but thanks for the heads-up (will try to buy at low PE next time).

Innovative has disposed off its entire holding in its subsidiary- Innovative Containers Services Pvt. Ltd. and has decided to remain focused on its core business.

You can read about it here.

Regards,

Yogansh Jeswani

Disclosure: Invested

1 Like

As per the 2016 Annual report -

Company is also planning to diversify into port container services, in Kaki Nada and has already obtained approvals from

ministry of service transportation and acquired land also. It will substantially add to the above profitability after it is implemented.

What would be the impact of this. Port container services is not related to their current business. Why are they diversifying into this business? Please through me some light…

Disc: Holding tracking position