Innovative Tech Pack Ltd. looks like a promising story. The Co. is into packaging business for FMCG companies like Patanjali, Dabar etc. & has 3 plants running at Pant Nagar, Baddi & Guwahati. The Pant Nagar facility which was recently commissioned is a modern, state of the art plant. Another new plant is in the process of being set up at Baddi. These new plants will help the Co. attract the bigger names in FMCG & Pharma, leading to higher sales with improved margins & that primarily for me is the investment thesis here. The Annual report & the Mgt. Discussion n Analysis are pretty exhaustive & give a decent insight into the working of the Co.

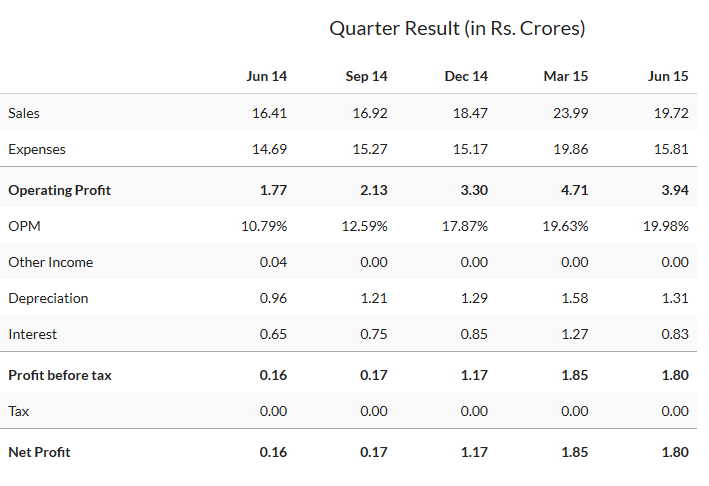

The Company has been a beneficiary of falling crude & is doing well. Due to a big fall in crude, the Sales growth, though higher in volume terms is not reflected in the figures.

The Co. has recently acquired another listed co. called Jauss Polymers Ltd, which is in the same line of business, & having a few marquee multi-national clients. Part of the new plant coming up at Baddi will be leased out to Jauss. The Co. owns 41% of Jauss directly. With the promoter holding another 12% in his individual capacity, the mgt control of Jauss is with the Co. Jauss, too has been coming out with very good numbers, though on a much smaller base. It is logical to expect a merger of Jauss with the Co., & since the promoter holding is much higher in Innovative, than in Jauss, the chances are that the merger ratio would be in its favour!

The Co. should do Sales, EBIT & Pat of about 80 Crs, 9.6Crs & 7.85 Crs. There are some one-time expenses pertaining to the Jauss acquisition. The Co is not paying any taxes due to MAT credits. For the year ending 2015-16, the Co. will be coming out with consolidated numbers for the first time, which could act as a trigger in rating the stock. Jauss should do Sales, EBIT & PAT of about 31Crs, 5.1Crs & 4.16Crs for 15-16. There is a one time gain of Rs. 1.6Crs that I am ignoring to be on the conservative side. 41% of Jauss’s earnings would be added to Innovative in its consolidated numbers, taking the consolidated EPS for the year 15-16 to be about Rs. 3.15 We are now almost through with 15-16, & very shortly the markets will start extrapolating 16-17 numbers, where in the new capacities will come on stream.

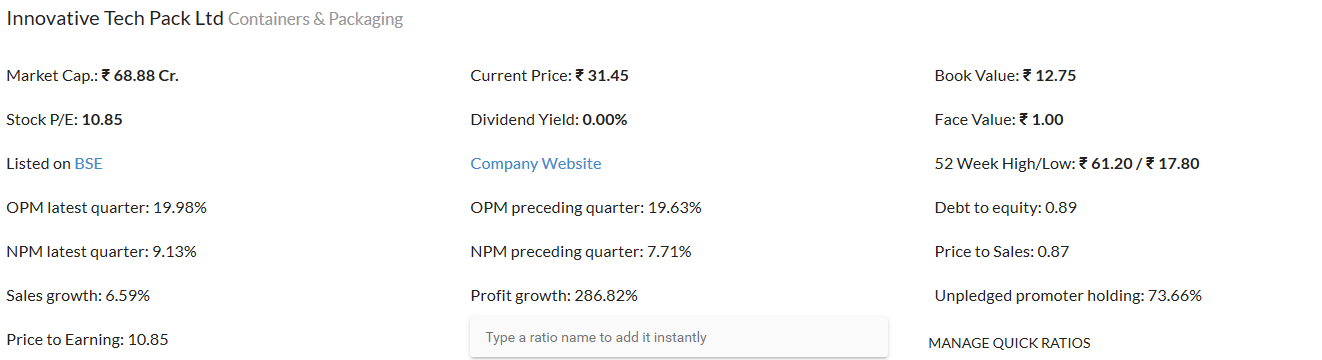

The current market cap of the Co. is about 61 Crs, which appears to be under-valued. The debt levels too are comfortable. As on September 30, 2015, the combined debt was about 23 Crs. This includes debt if any, taken for Jauss’s acquisition.

The Company also has a subsidiary called Innovative Container Services § Ltd., which has been allotted land in Kakinada to build a Container freight Station. Since it is still at an early stage of implementation, perhaps it would be prudent to just be aware of it without taking any future projections into account.

Concerns: The story is still unfolding & there could be delays in project execution. The investment thesis is based on future growth & the numbers are still to come in, & we all know that there is many a slip between the cup & the lip!!

Disc: Invested & looking to add as the story unfolds!