To my view, comparing Innovative Tech Pack with JHS Svendgaard Laboratory seems not justified because of the type of product. Svendgaard manufactures toothbrush and tooth paste as their main product and supplies to other companies. In their own brand name there are hardly a few products, for which they could not create a good status. Fierce competition is there in these products from big companies like Colgate, HUL etc. Patanjali is another new entrant in this sector and also a big competitor. Those big companies can easily adopt new and changed technology without having much financial impact due to their scale of operation. In such cases, customers of Svendgaard (like P&G) will obviously ask for a change in product and technology to carry out the competition and keep intact their market-share. In this respect Svendgaard will have to cut a sorry figure due to heavy financial impact on them due to small scale operations and dependency on a few products. Hence, once their business failed earlier and may recur anytime in future.

In contradiction to the above, Innovative Tech Pack is engaged in production of PET bottles, where market demand is always increasing and will go on further increase. Here, competition from big companies does not threat their existence. Change in technology, impact of market demand and adoption of any new products can easily be taken up without much financial impact on the company. However, one thing common in both is that they are dependent on contract selling to other companies. But here also, Innovative has the advantage because their products have heavy demands in FMCG and Pharma sector and can be sold to numerous companies irrespective of status of the buyers(big, small famous infamous etc.). Their customers may be big domestic or multinational companies or even small domestic companies. Financial impact on the company for change of technology will be small and temporary, existing for one to one and a half year. Survival of the company will not be threatened by change of product and technology except in case of drastic measure by many Governments to curb plastic. However, in the current situation the same does not seem possible for any country.

I was once presenting to mgmt committee of a MNC FMCG for vendor selection. I had missed the point of vendor proximity and mgmt pointed out that we want our vendors to be close to our mfg plant. So ITPLs strategy to have mfg plant nationwide will be highly beneficial in future to get more contracts from FMCGs + it will be difficult for new comer to be present nationwide in small time frame. If any company wish to do that, it will take at least 3-4 years

Thanks for your response. The point of proximity to location of FMCG companies was not known to me. I hold a good number (14K+) of shares of this company, however cost price is near the current market price. My hope is that it will give several times return in next 2-3 years.

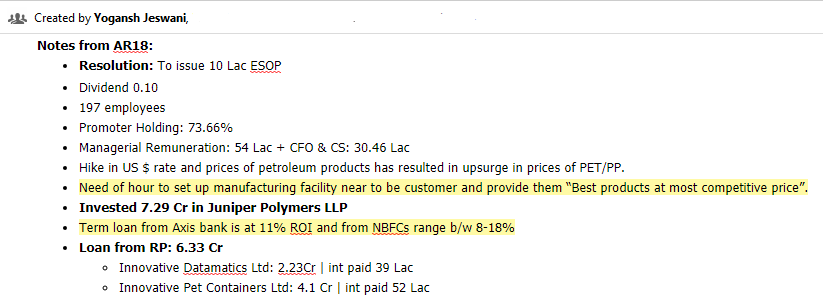

Notes from AR 2017

• Customers – marquee list of FMCG & Pharma players – Dabur / Perfetti / Heinz etc.

• Sales increased by 15% but Profit increased by ~2.5 times mainly due increase in operating margins from 18% to 24%. Operating margins increased due to economies of scale and production efficiency.

• 142 employees, median remuneration increased by 10%, no increase in mgmt. remuneration

• Ayush Mittal as top shareholder

• 32% ownership in Jauss polymers which contributed 29 lakhs profit

• Future Strategy –

o Adding customers from F&B, confectionary, Personal Hygiene

o Setup a mfg unit in South India

o Improving operational efficiency and utilization of resources

• PET Advantages – Versatility, Safety, Recyclability and Eco-friendly, Economical

• Stricter norms in F&B, GST, Premiumisation – will help organized players

Observations

• Debt increased by 10 cr, Fixed assets increased by 19 cr,

• non-current investments reduced by 4cr due to liquidation of Innovative Containers

• Provision for taxes increased by 2.5 times

• Sales increased by ~14 cr from 90 cr to 105 cr

• Trade Receivable increased by 5c r from 11.6 cr to 16.2 cr (= 56 days)

(with OPM increased from 18% to 24% and incremental increase in Trade receivables (5cr) is just one third of incremental sales increase of 14 cr. Hence sales increase is not based on promotion / increasing credit limit)

• Trade Payable increased by 7 cr from 7 cr to 14 cr (= 48 days)

• Inventories also increased from 5.6 cr to 9.3 cr ( = 32 days)

• 2.2cr of Receivables from Assam govt for power subsidy from 2012-13 to 2016-2017 noted under Short Term Loans and Advances

• Trading revenue has come down from 14cr to 9cr and Mfg revenue has gone up from 74cr to 90cr

Doubt

Potential increase in equity shares – 6 lakhs

Issue of share warrant – 51 lakhs

So is the mgmt. planning to execute warrants at Rs. 8.5 per share ?

However, the interest expense has increased by almost 65% to 6.75 cr. Hope the promoters keep this in check while company is on a growing path.

Also, travelling expense has increased by close to 72% to 63 lakhs. This is a big jump. Will be sending an email to the company regarding the same. I hope someone else also writes an email to them regarding this as on previous occasions when asked particular questions I have never received a reply.

Co has issued 6,00,000 warrants of FV 1/- at a prem of 33.37/- to the promoters. Now, in case of warrants issue, the warrant holder has to put in just 25% of the total money (i.e. 51,55,500 in case of ITPL) at the time of allotment. Remaining 75% balance needs to be paid within 18 months of the issue of such warrants. You can find this data in the footnotes as well.

So, promoter will bring in a total of 6 Lac * 34.37 = 2.06 Cr via this warrant issue. Currently, they have put in 25% of 2.06 Cr = 51.55 Lac

I’m pretty worried by the upcoming leveraging and equity dilutive resolutions in the AGM:

Item No.5

This special resolution enables the Board to issue Securities for an aggregate amount not exceeding Rs. 150 Crores (Rupees One Hundred Fifty crores only) or its equivalent of any other foreign currencies. The Board shall issue Securities pursuant to this special resolution and utilize the proceeds to meet capital expenditure and long term working capital requirements of the Company and exploring acquisition opportunities and general corporate purposes.

Item No.6

In order to reward and motivate employees as also to attract the talent as well as to retain the key managerial employees, the Board of Directors at its meeting held on 4th Day of September, 2017 have approved and proposed for the approval of the shareholders for issue of Stock Options as per which employees. The total number of options to be granted under this scheme is 7,75,000 ( Seven Lacs Seventy Five Thousand Only).

Members are requested to note that the draft ESOP 2017 shall be open for inspection by the Members at the Registered & Corporate O ce of the Company during normal business hours on all working days up to the date of the Meeting and shall also be placed at the venue of the Meeting.

Item No.7

To meet funding requirements towards proposed capital expenditures, operational expenditure and working capital with respect to the power projects being set up by the Company, its Subsidiaries and Associate Companies and for general corporate purposes, your Company has availed / will avail financial assistance by way of Rupee Term Loans, Corporate Loans etc., from time to time from various lenders i.e. Bank(s) / Financial Institution(s) upon such terms and conditions stipulated by them and approved by the Board.

One of the terms of sanction provides that in the event of default by the Company under the lending arrangements or upon exercise of an option provided under the lending arrangements the Bank(s) / Financial Institution(s) and other lenders may be entitled to exercise the option to convert whole or part of their outstanding facility into fully paid up ordinary Equity Shares of the Company at a price to be determined in accordance with the applicable SEBI regulations at the time of such conversion.

For QIP of 150 cr - assuming funds raised at 90/share leads to fresh issue of 1.67 cr (close to doubling the current equity shares). The company may choose to only raise a much smaller amount but having the power to raise funds upto 150 cr without a detailed action plan is concerning.

Would request anybody attending the AGM to please quiz the management and share detailed rationale for these resolutions.

Source :- Money-life Magazine :Stock Manipulation

Debashis Basu and Aditya Govindraj and Jason Monteiro

23 August 2012

If you think SEBI is out to protect you against habitual offenders and the stock exchanges are there to monitor listed companies, perish the thought. **Anil Kulbhushan Barar and Atul Nripraj Barar** were both directors of Barar Industries. Barar Industries had been pulled up for default of dues and, finally, had to be wound up. They are directors of Innovative Tech Pack which has been pulled up for not submitting the shareholding pattern and corporate governance report. It has also been suspended from trading for not complying with the listing agreement. Between August 2010 and March 2012, it rocketed 4487% on very erratic sales. Its profits resembled a seismograph, going up and down, in an unpredictable fashion; yet, the stock price charted a dizzy rise. The stock plunged by nearly 75% within just four months.

Close price of stock on Nov 7 is 56.80. Which means they are buying / getting right to buy at a discount of 40%. Promoter has right to buy 6 lakh shares at Rs.34.37 anytime before May 2018. At current price, promoter has already made Rs.52.73 per share (87.1 - 34.37). They have made whooping 3.16 Cr profit out of 51.5L investment. The option is still worthy even if the price dropped to Rs.26 since they can opt not to convert warrants into shares. Good for promoters bad for shareholders.

The key concern I have is not about the debt but the exorbitant interest paid on top of warrant benefits they enjoy.

Out of 26.8 Crores LT debt only 75 lakhs is from banks. 17 Cr at 12% to 15%. Rest is not disclosed which I suspect to be beyond 20%. Cost of debt is high for a company with decent interest coverage ratio. Management remuneration is also close to ceiling as per act.

IMHO company should consider shareholders interest too.

However, no mention of when will the new plant be operational. I have written emails many times in the last couple of years, but have never received a reply. If someone has then please ask them this query.

Hello @ayushmit sir…any insights into what the future holds for ITPL would be greatly appreciated. The stock has been beaten down very badly. I know that it has been posting bad results since last 2-3 quarters but I just want to know whether there has been any changes as far as the fundamentals of the company are concerned or any major management concerns that investors should be weary of or is it just bearing the brunt of bearish market sentiments like all other small companies.Any pointers and details on ITPL from your end will be very helpful.

Rating Reaffirmed even after bad results in the past one year.

Dabur accounted for 45% revenue in fiscal 2017.

Acquisition of clients such as Patanjali Ayurved Limited, Perfetti Van Melle India Private Limited, Godrej Group, Emami Ltd and more recently Marico Ltd, has helped diversify the customer profile and lowered Dabur’s revenue contribution from 69% in fiscal 2011.

Strangely the Credit rating report published in Aug 2018 is still using the financial data of FY17 and has discussed all the metrics based on FY17 numbers. Whereas, it should have taken FY18 data.