Regarding your whats next after zomato and policy bazaar, my speculative answer would would be that infoedge would invest in late stage startups rather than early stage startups because of higher cash on their books, late stage startups also means less probability of failure

1 Like

Zomato has filed DRHP for IPO. This is going to be a stepping stone in the history of Indian Startup ecosystem!

It will not have a shareholder quota for Info Edge shareholders.

SEBI website has slowed down. Alternate link to view the DRHP.

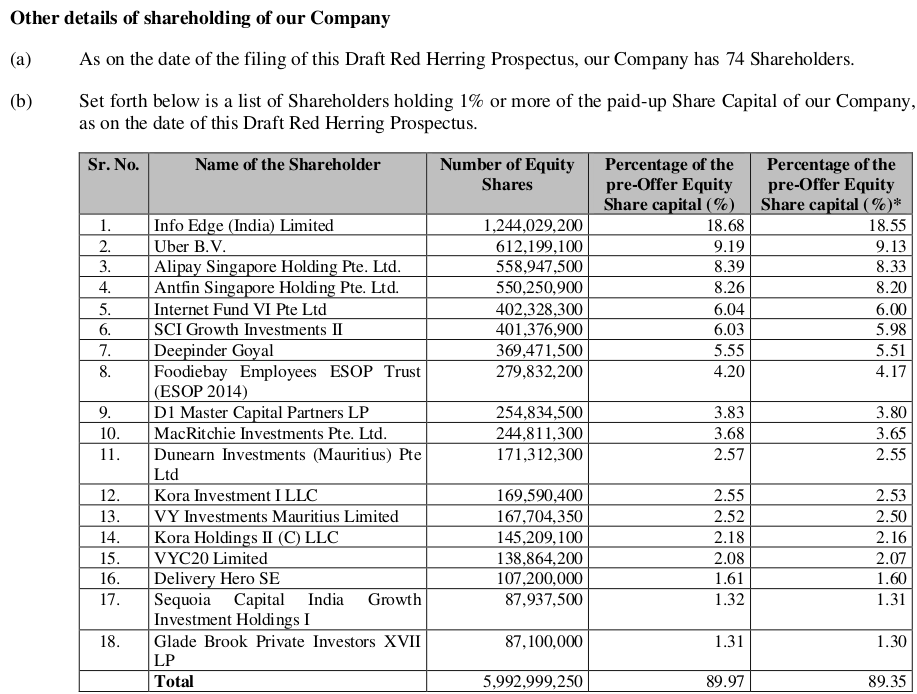

List of shareholders of Zomato as on the date of filing DRHP:

6 Likes

Post Zomato Lisiting would it be a good idea to Sell Infoedge and buy Zomato ? Infoedge has become difficult to value as many startups to figure out .

2 Likes

Why this change of heart? What changed in the business since your post that you talk of selling the 85% allocation of your PF? You said Info Edge is 85% in your PF, probably the highest allocation I have seen in anyone’s PF on VP.

I have a position in Info Edge.

1 Like

I like Zomato platform. Expect them to cash positive by September quarter. believe Zomato can build large business profitably in India and then expand overseas over time. I hope it opens lower post listing - then plan to at least switch 50 % of my holding of Infoedge.

I expect Zomato valuation will rise faster than Infoedge in percentage terms - therefore the switch . Global valuations of this sector may impact Zomato valuations positively.

INFOEDGE market cap is currently 64500 CR (based on screener.in)

Of which, Zomato/Policybazar is roughly 12000 CR and Naukri/99acres/Jeevansathi is roughly say 10000 CR max. ALL the other 7 startups: meritnation, happilyunmarried, mydala, canvera etc amount to probably less than 1000 cr in my view…even keep 2000 CR to be generous.

All of that is worth INR 24000… which was what INFOEDGE was valued last year, when it was trading at INR 1750-2000.

So in my view, INFOEDGE was perfectly priced at that band. the current price of 4800-5000 makes no sense to me. What is the remaining 40000 CR excess valuation premium for? If someone can help explain this valuation gap will be good.

So yes, I feel its better to exit INFOEDGE at current valuations and directly invest in Zomato and Policybazaar.

2 Likes

Naukri makes annually 800 cr cash — 20 to 25 times for a profitable platform? 16000 to 20000 cr cr . the other 3 - vallue of platform 10 to 15 times sales as they are close to breakeven.

You are right - its becoming more difficult to value all its portals & now the new VC fund .

Info Edge, Its looks like an holding company to me, just like Tata Inv. Corp or Baja Holdings, but instead investing in listed companies it invest in unlisted stirrups.

But, holding companies generally trade almost 40-60% discount to their NAV how come Info Edge is trading so high?

Also, I read somewhere that Amazon is entering in food delivery space, we know that how much damage Amazon like companies can do, is that the reason for selling of Zomato in IPO?

3 Likes

This is what I could gather on Zomato: https://twitter.com/manujindal2803/status/1388456226753716226?s=20

5 Likes

Information on Zomato

Litigation against the company regarding indirect taxation to the tune of 96 crores

Also civil proceedings against directors - 276 crores

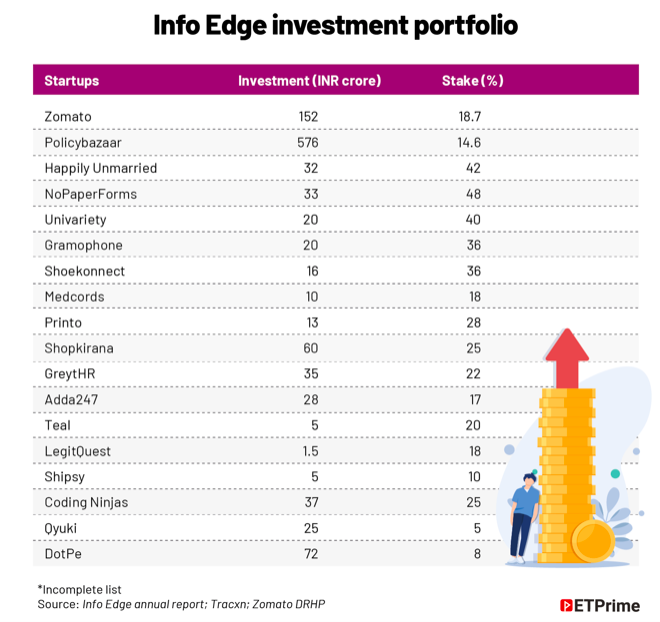

updated list of startups INFOEDGE has invested in:

How much are these startups worth? how many written off?

no way to know. So beyond main classifieds, Zomato, Policybazaar… the rest are being valued in market basis just guesswork. One way, is to painstakingly go into MCA records and get annual filings of each and every startup, and see balance sheets and make an estimate.

2 Likes

I doubt MCA records and financial statement analysis will help.

Most of the assigned equity value is for future potential not current financials. Hence the typically insane EV/ Sales multiples (15x etc.)

A better way might be to

- Understand what market vertical each of these start-ups are targeting.

- How rapidly is digitization happening here (assuming they are all in ecommerce).

- What is the Total Addressable Opportunity in each vertical?

- What is this start-up’s competitive positioning?

- Finally, is it a winner takes all market?

2 Likes

a great analysis of zomato business and valuation

Deep Dive Into Zomato. Will growth create value? | by Pinanity | May, 2021 | Medium

1 Like

Balance sheets will at least help you see TOPLINE REV GROWTH so you can extrapolate growth and hence some valuation… not different to how VCs themselves value.

its amazing how profitability metrics go up before IPOs

3 Likes

I think it’s the other way round for Zomato.

Because the profitability has recently gone up and no immediate threat, they decided to roll the offering.

1 Like

Earnings Call for Q4FY21")

Q4 result call here, adding some non explicit points( own interpretation)

-

Naukri vertical doing better than expectations, driven by IT and ITES, billing growing in double digits - LinkedIn competetion not yet visible and mgmt not concerned at all. This biz has survived covid well and will continue to do well with double digit organic growth and inorganic aided by contnued adjecncies acquisition( iimjobs, swayed etc, - its approx 1500 cr annual runrate biz - platform monopoly with >50% PBIT, can do a 25%+ CAGR for visible future

-

99Acres would likely see sub verticals - builder/ resale/rental etc, work already in progress at back end - with two covid waves real estate is tilting towards organized players( visible in listed players), and lion share to move to digital in marketing budgets - approx 300 cr annual revenue and 25%+ growth in forseeable future - EBIDTA getting in green, focus on growth for now - high competitive space

-

Matrimonials - clear subtle callouts of consolidation in near future - they plan to be a buyer - 15-20% growth space but high margins post consolidation - current cash war chest could find a use here

-

Gramaphone, shoeconnect, and few more were called out by Sanjeev as future possible unicorns( 1-2 out of 6 investees)…nothing in near future

-

Bonus issue to be considered by board per Sanjeev

-

policy bazaar ipo yet to be discussed with board

9 Likes

Another minor addition.

Disc: Holding