Surprised that there isn’t a thread for Info Edge so trying to put in whatever I know to get the conversation going. Info Edge is the company behind Naukri - India’s No.1 Job portal. They also own 99acres which is the No.1 in Real Estate classifieds, JeevanSathi (Behind Bharat Matrimony and Shaadi here) and quite a few others. They also own nearly 50% stake in Zomato and about 10% in Policy Bazaar/Paisa Bazaar and a few others like Shiksha, Merit Nation etc. Although the businesses come across to be quite diverse, the unifying theme if any, is that they are all mostly online classifieds. That’s what they consider themselves and there is indeed a method to their madness. They seem to have been around a long time (17 years). IPO was in 2006.

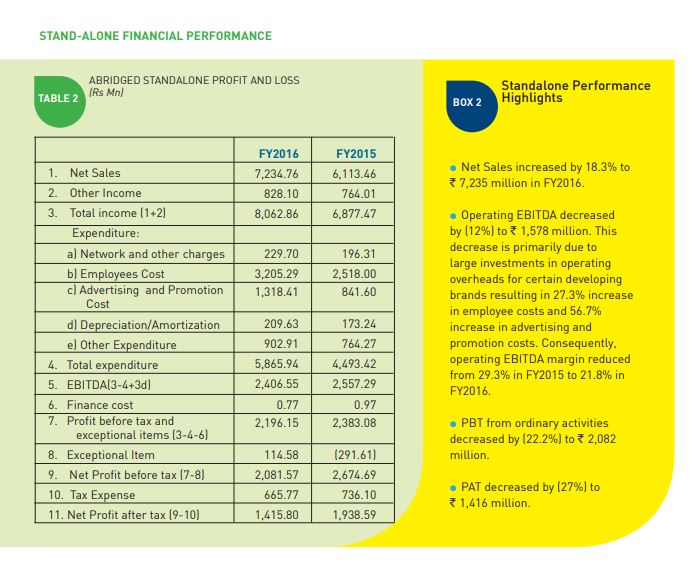

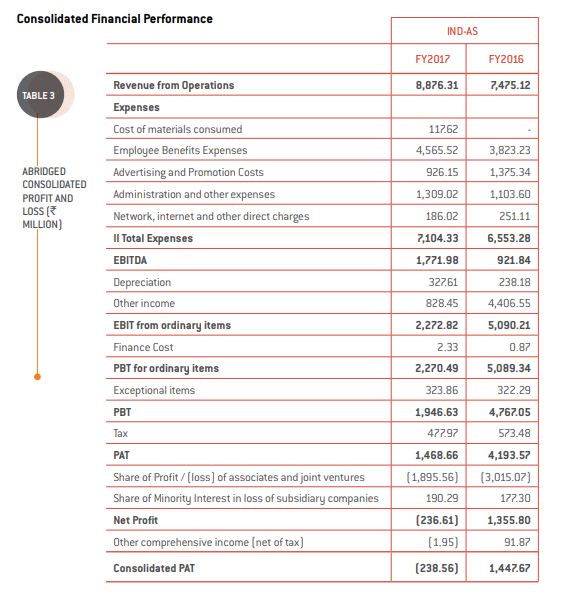

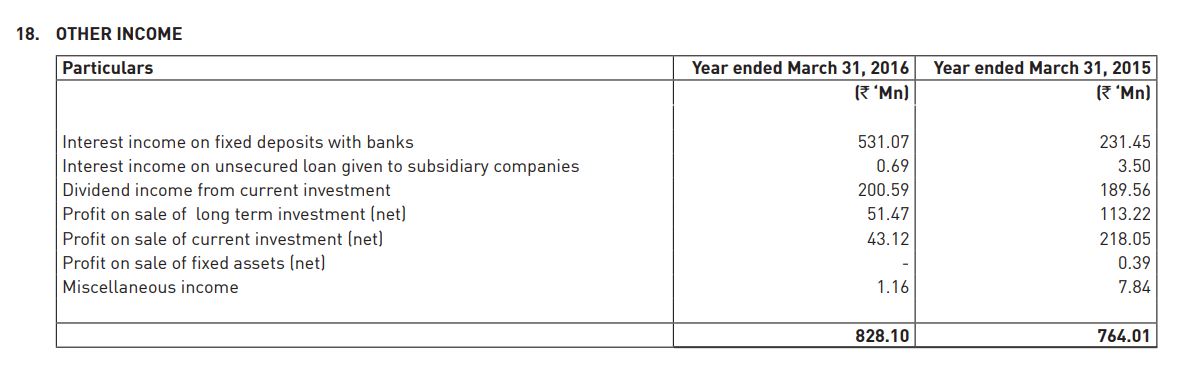

As a standalone entity, the revenues have grown from Rs.140 Cr in 2007 to Rs.820 Cr in 2017 (About 20% CAGR) and PAT has grown from 27 Cr. to 204 Cr. (About 22% CAGR).

This is not the whole story though, since unlike the software services companies like Infosys and TCS, the free cash has been deployed in several tech businesses. This is the sort of company that takes risks with its cash, tries to build products instead of hoarding them through the years. Their approach to me seems to be very Peter Thiel-ish, in that they have a portfolio of companies to invest in and they don’t seem to mind few of them going belly-up, as long as they end up with one or two big winners. They have also not been shy of accepting defeat in cutting out and writing-off some of their investee companies.

Standalone Companies

These are the businesses that are under the direct management of the company

Naukri.com

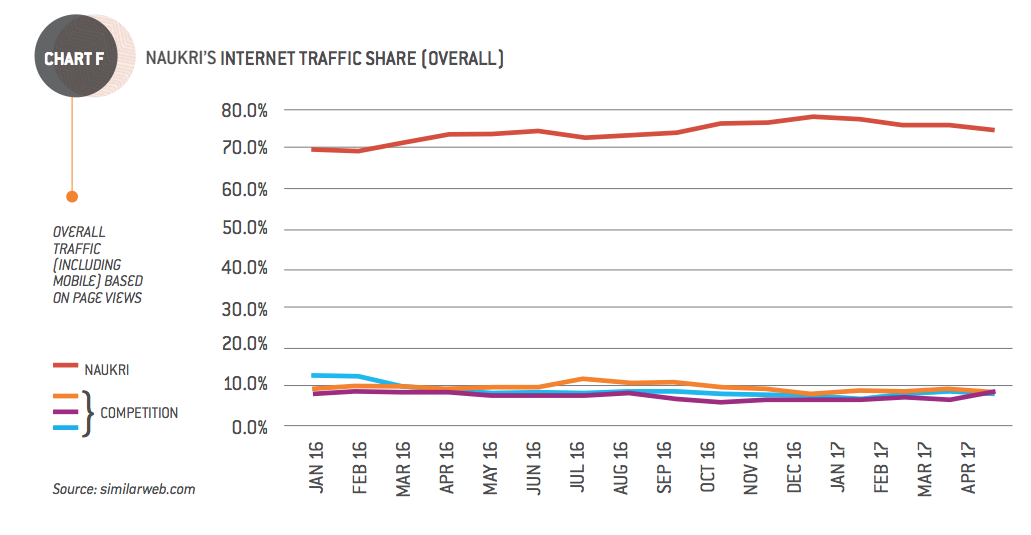

This is the bread and butter of the company and its current crown jewel. All the free cash flow comes from here. FY17 Revenues were 595 Crores out of the total 820 Cr. reported by the standalone company (75% of total revenues) and EBITDA was 321 Cr. (Outstanding 54% EBITDA margin). As for traffic share, they have about 75% of the overall market when the nearest competitor doesn’t even have 10%. That’s pretty much a strong monopoly driven by a strong brand and network effect. Continuous innovation in “product, engineering, channels and services” has kept the moat safe and sound.

90% of revenue comes from recruiters and 10% from job seekers.

99acres.com

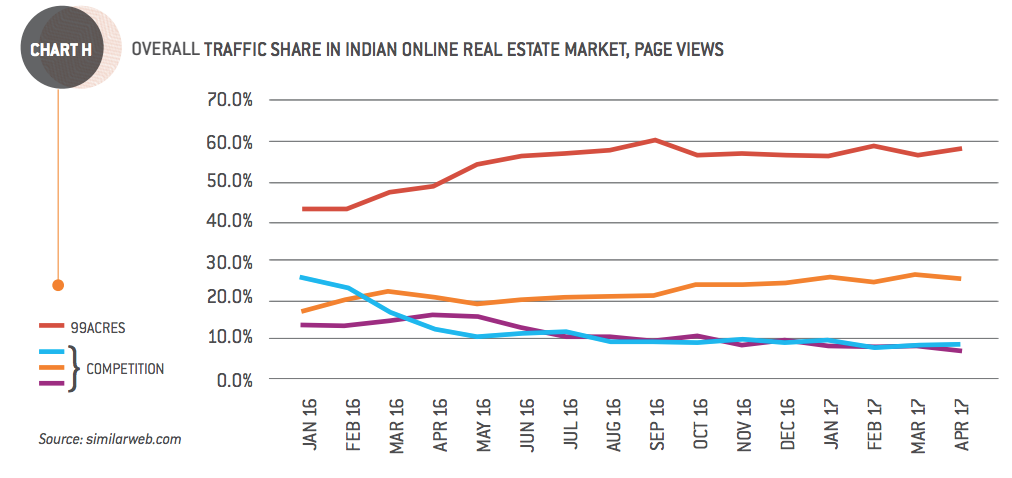

This is the company’s real-estate classifieds business which again has a leading position. Their traffic share is close to 60% while the nearest competitor has about 25%. This must be magicbricks.com. Housing.com and Commonfloor.com seem to have given up investments so this sector will survive going ahead as a duopoly with 99acres.com leading is my guess. FY17 revenues were at 112 Cr, EBITDA loss was at 59.7 Cr (Down from 91 Cr in FY16). The hit seems to have come from demonetisation which hurt the RE sector in FY17.

Current revenues seem to be driven mainly by paid listings and ads placed by developers. Whenever Real-estate sector picks up and ad spend moves from offline media to online, 99acres.com should capitalise, considering their market share.

Jeevansathi.com

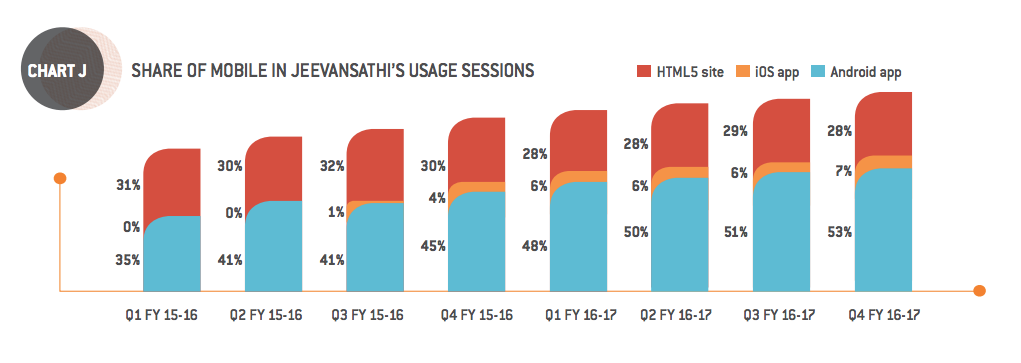

FY17 Revenue at 58 Cr. and EBITDA loss at 7.9 Cr. Seems to be doing well in terms of profile listings (11.8% growth) and has a 3rd position in the market behind bharatmatrimony and shaadi. Mobile penetration seems to be good and growing.

shiksha.com

This caters to the online education classified market and is still new and growing. This could turn out to be a great business in the future as school and colleges move their ad spend from offline to online. The revenue stream (Currently) seems to come from branding and advertising for colleges and universities and also from lead generation (selling student profiles to colleges). They also seem to provide counselling services for their international university partners. FY17 revenues were at 36.5 Cr and EBITDA loss at 3.7 Cr which doesn’t seem to be too bad for a fledgling business with a very large and lucrative potential market.

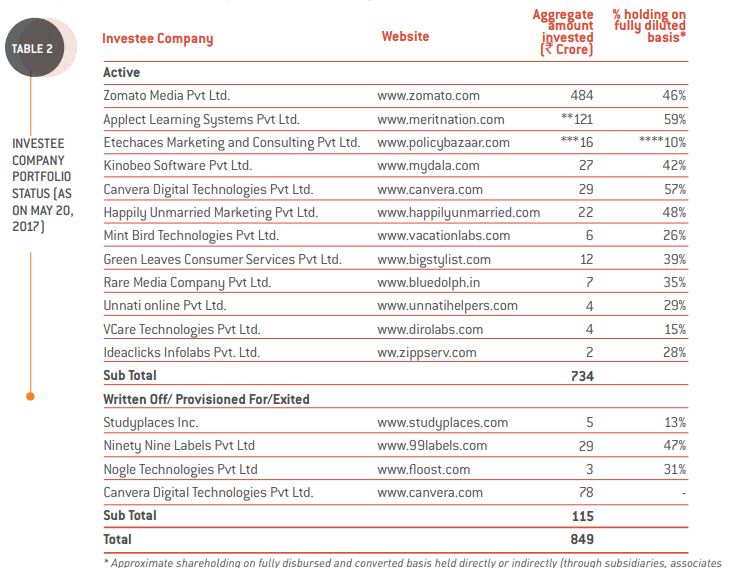

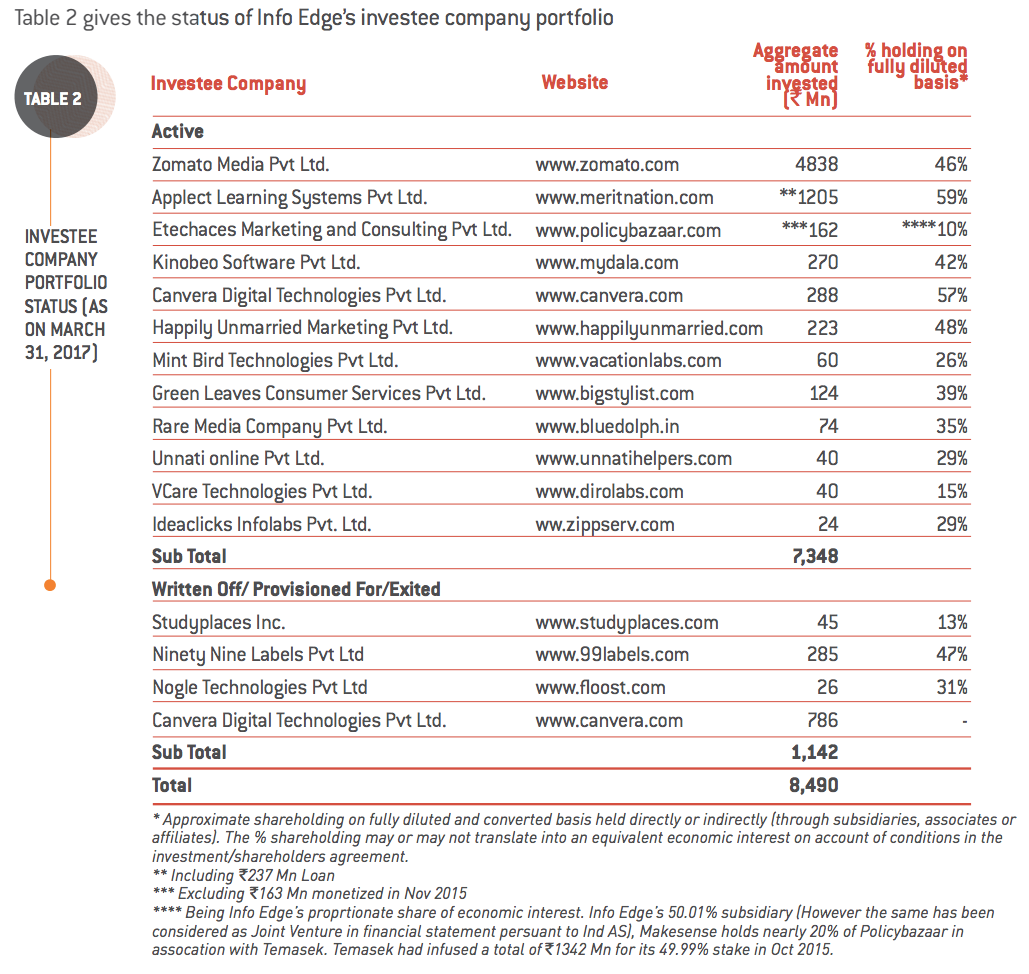

Investee Companies

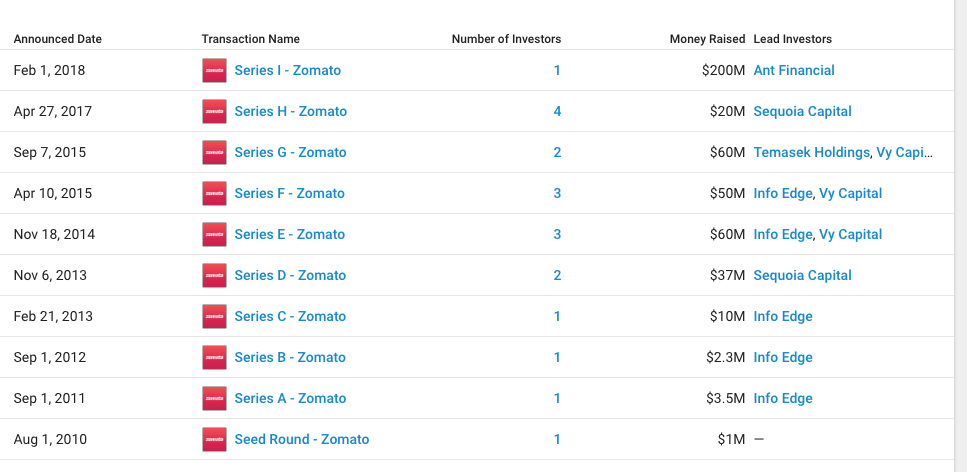

Zomato.com (46% Stake)

Online restaurant discovery with presence in 23 countries, leading position in India and UAE. Revenues were at 332.3 Cr and EBITDA losses at 152 Cr. What’s interesting though is the trend – Revenues are galloping and cash burn is reducing. FY15 revenues were 96 Cr, FY16 at 184 Cr and FY17 at 332 Cr. EBITDA losses in FY15 were 136 Cr, in FY16 it was 441 Cr and in that light FY17 losses at 152 Cr shows that losses are reducing drastically. Average monthly cash burn is down from $4.2 million per month to around $1 million per month between FY16 and FY17. Food Ordering and Ad sales are both growing well too.

The key thing to watch out for is how its battle with Swiggy.com pans out. There were talks of a merger last year and Nomura had put the valuation for Zomato at $1.4 billion back in Nov last year. The only problem seems to be that they both can’t seem to agree on their valuations but its only been 4 months since the rumours came out. It is impossible for either of them to survive by competing with each other so a merger is inevitable and it is post this merger that Zomato could undergo serious re-rating because the food delivery business is massive.

Policybazaar.com (10% Stake)

India’s online financial supermarket – Has 90% of online policy comparisons and 40% of online insurance transactions – Clear market leader emerging here. This is another business I am extremely positive on because the business model is very strong and PB fills the price gap between online and offline policies. This reminds me so much of GEICO’s business model (although they do the underwriting themselves) as the whole business is based on arbitrage. Unfortunately, Info Edge which was an early stage investor here got diluted in subsequent rounds and currently owns only 10% here. This may not be something to scoff at though, as the opportunity size is huge and if they manage to build a large enough moat and also somehow get into underwriting, they might be huge someday.

Meritnation (59% Stake)

Supplementary online learning platform (like Byjus) with assessments, tests and live classes having content from KG to K-12. Revenues have grown from 28.7 Cr to 36.2 Cr (26%) and losses have reduced from 41 Cr to 23 Cr. They seem far, far behind Byju’s. Not sure if they can carve a niche for themselves.

Canvera

Main source of revenue comes from Wedding album printing, design of albums, portfolio microsites for photographers in this space, lead generation (Classifieds comes into play). Revenues down from 56 to 49. Losses down from 33 to 27.

Mydala

Seems to be a couponing site. Not sure what the business model is here. I thought coupon sites were dead and buried for good.

Happily Unmarried

This seems to be a very interesting business with a great online presence (Check out their facebook page for eg.), although its an offline business. It’s a range of boutique grooming products for women and men, with some modern, smart marketing strategies. (Think Paper Boat).

Shareholding, Financials, Valuation etc.

Promoters held about 50% in 2007 and now hold about 42%. MFs hold about 15%. FPIs hold about 33%. Only about 2% is with small retail shareholders. There has been quite a few dilutions along the way – share capital was 21.84 Cr in 2006 and is now 121 Cr.

The company has zero debt and has always had zero debt in the last 11 years which is an excellent thing. The cash flow from operations (standalone) has always been positive and growing. Oh and they have about 1250 Cr cash on the balance sheet.

Negative working capital is another thing to note as well. The management seems ethical and open. Their approach to me seems very much like Peter Thiel in trying to build businesses that go from zero to one. In that respect, I really hope they merge Zomato with Swiggy.com sooner and stop the bloodshed there.

It is not going to be easy value anything here other than naukri.com since they have free cash flow and perhaps 99acres.com. This is the sort of space where growth can be exponential or bust, and valuations have in the past taken hilarious proportions. I don’t want to venture into doing anything silly like that.

Back of the envelope calculations make me value Naukri.com at about 7000 Cr.

Nomura thinks Zomato was worth $1.4 billion. That’s about 9000 Cr – Info Edge’s stake could be then worth about 4000 Cr.

Matrimony.com is valued at about 1800 Cr – Jeevan Sathi could perhaps be valued at 500 Cr.

Housing.com was valued at $75 million (500 Cr) and its traffic share is much lesser than 99acres.com. Let’s go with 1000 Cr here for 99acres.

The rest could amount to nothing as of now although they may raise funds at fancy valuations. The current market cap might be expensive by anywhere between 10-50% but that’s not abnormal in the tech industry.

Key Triggers/Opportunities

Near-term: Zomato – Swiggy merger, Zomato breakeven, 99acres.com performance post RERA/demonetisation, Policy Bazaar’s growth

Long-term: India doesn’t have an Amazon, Netflix, Google or Facebook. It has very few tech products and our services companies don’t seem intent in risk-taking and keep piling up cash until kingdom come. In that aspect, Info Edge seems to be a company which has the next-gen start-up mindset and may in fact end up with a few India-centric tech monopolies in the future. Think of Amazon in the 90s.

Risks

- IT/ITES seems to contribute 50% of the naukri.com revenues. Any adverse impact to this sector could potentially hurt revenues

- Tech valuations are at most times a joke. Most tech businesses have had a significant mark-down from 2015 heydays. There is no saying where they will be 5 years from now as rates rise.

- With the financial deregulations, it’s easy for a SoftBank or Alibaba to pump cash and fight pretty much any tech business it fancies, even to complete destruction.

Disc: Invested