Zomato OFS for Infoedge reduced to half the size

With QIP funds already sitting in cash unutilized, mgmt doesn’t seem to have a large cash usage as of now. It is clear that they are not able to find sizable investment opportunities, esp when global PE funds with much deeper pocket are out there.

While Zomato and Policy bazaar IPOs will help on Infoedge valuations over next 2-3 quarters, it is increasingly visible that Sanjeev doesn’t have a pipeline for next set of unicorns in sight.

Lot would now hinge on core business performance in near term as well as their ability to find promising investments, mkt may be patient with them given outstanding track record for now.

Invested.

Or on after thought they felt it makes more sense to keep higher ownership stakes in Zomato post its listing… This news may not have much impact on Info edge stock price but surely has implications on Zomato IPO

Infoedge AR 2021

As they complete 25 years and being a poster boy of Inyernet listed story - it’s good to see their own assessment of strength, improvement areas and more importantly path forward

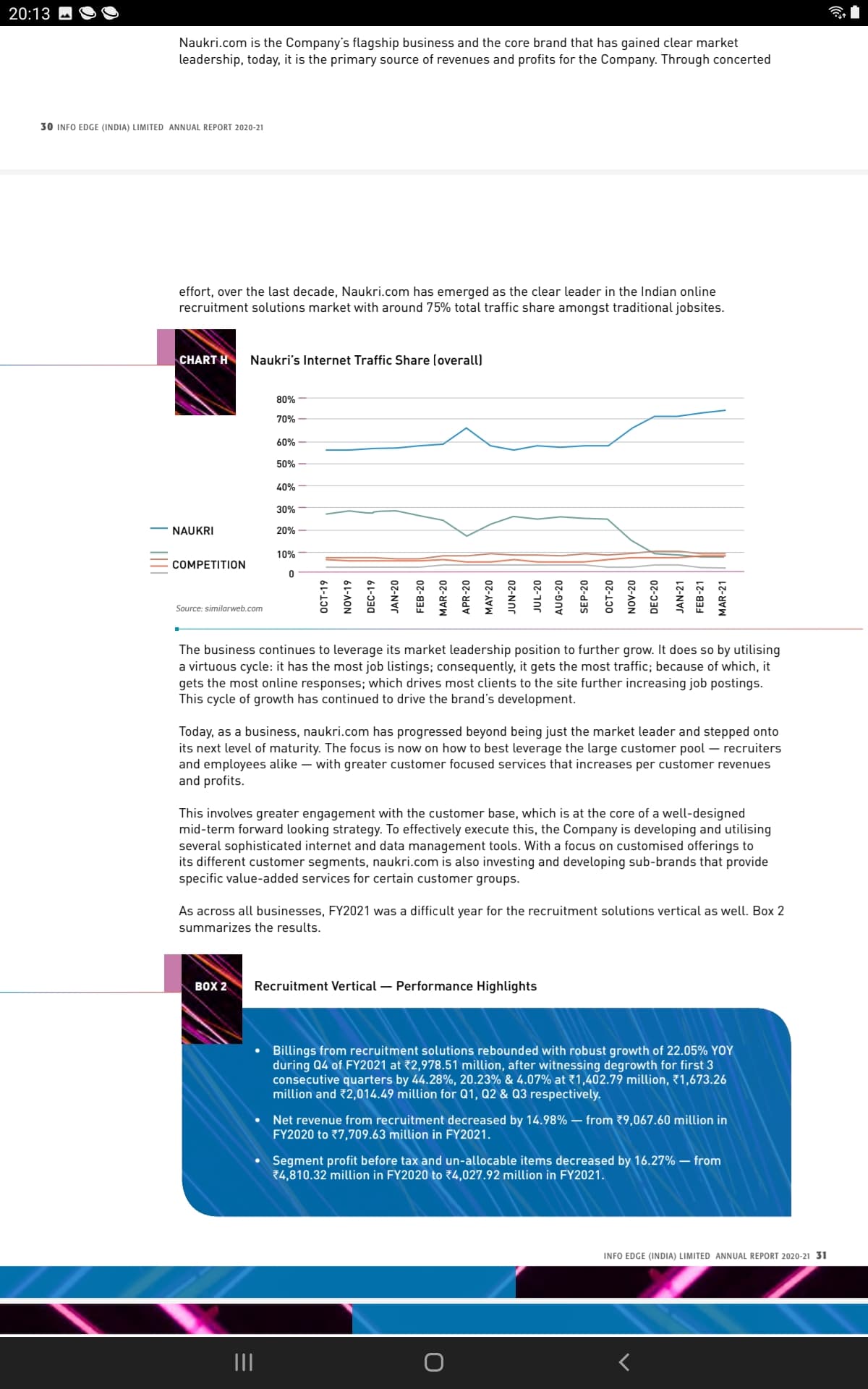

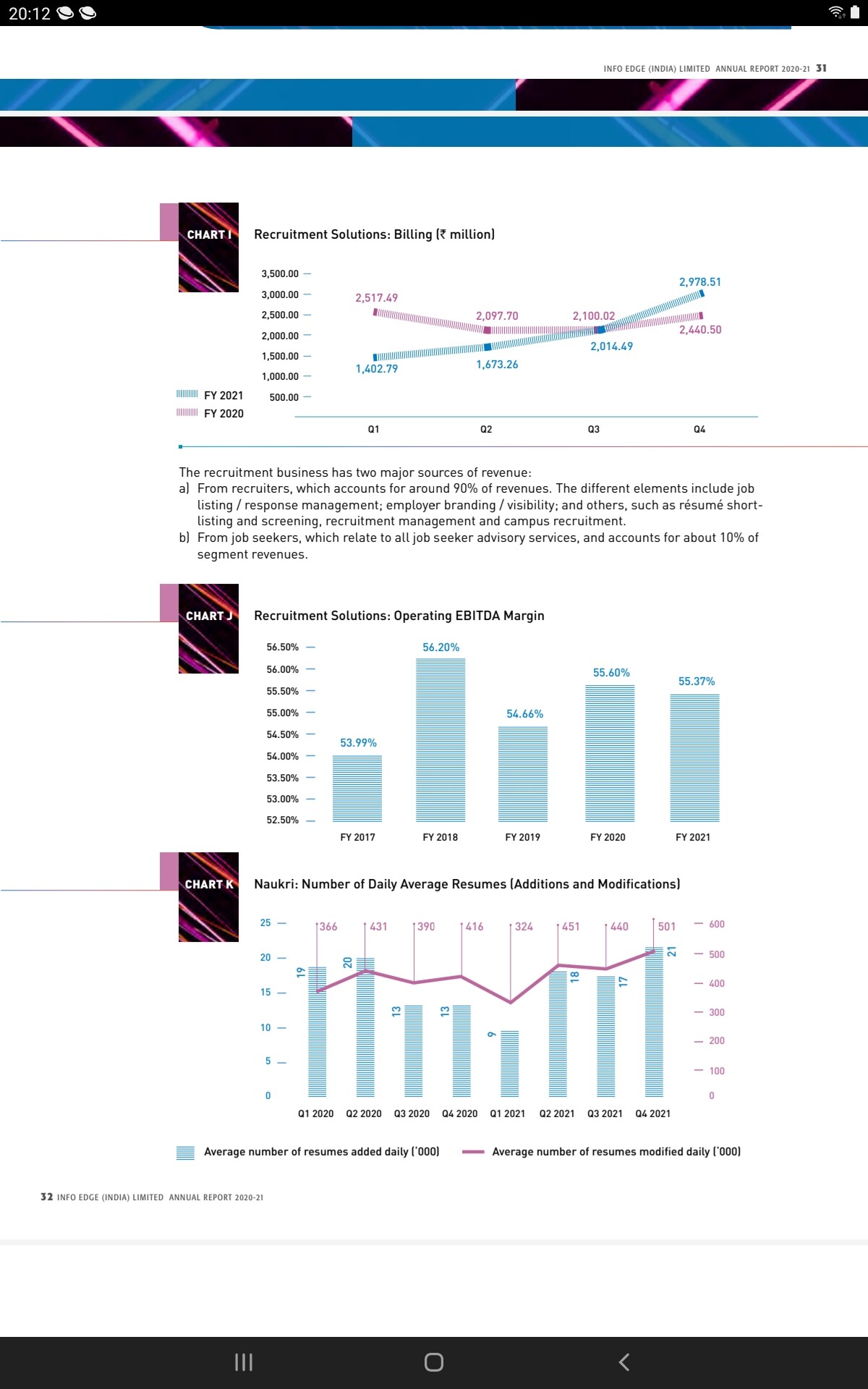

- Naukri vertical has done well, esp in Q4 onwards and supported by IT hiring bump up, they coninue to lead with 75%+ mkt share( gap widens with competetion) and importantly with reduced marketing spend. Of course acquisition if iimjobs, hirist and scaling of AmbitionBox as well as future plans looks solid. 2020 was lackluster and 2021 turned out well towards end with solid start for 2022.

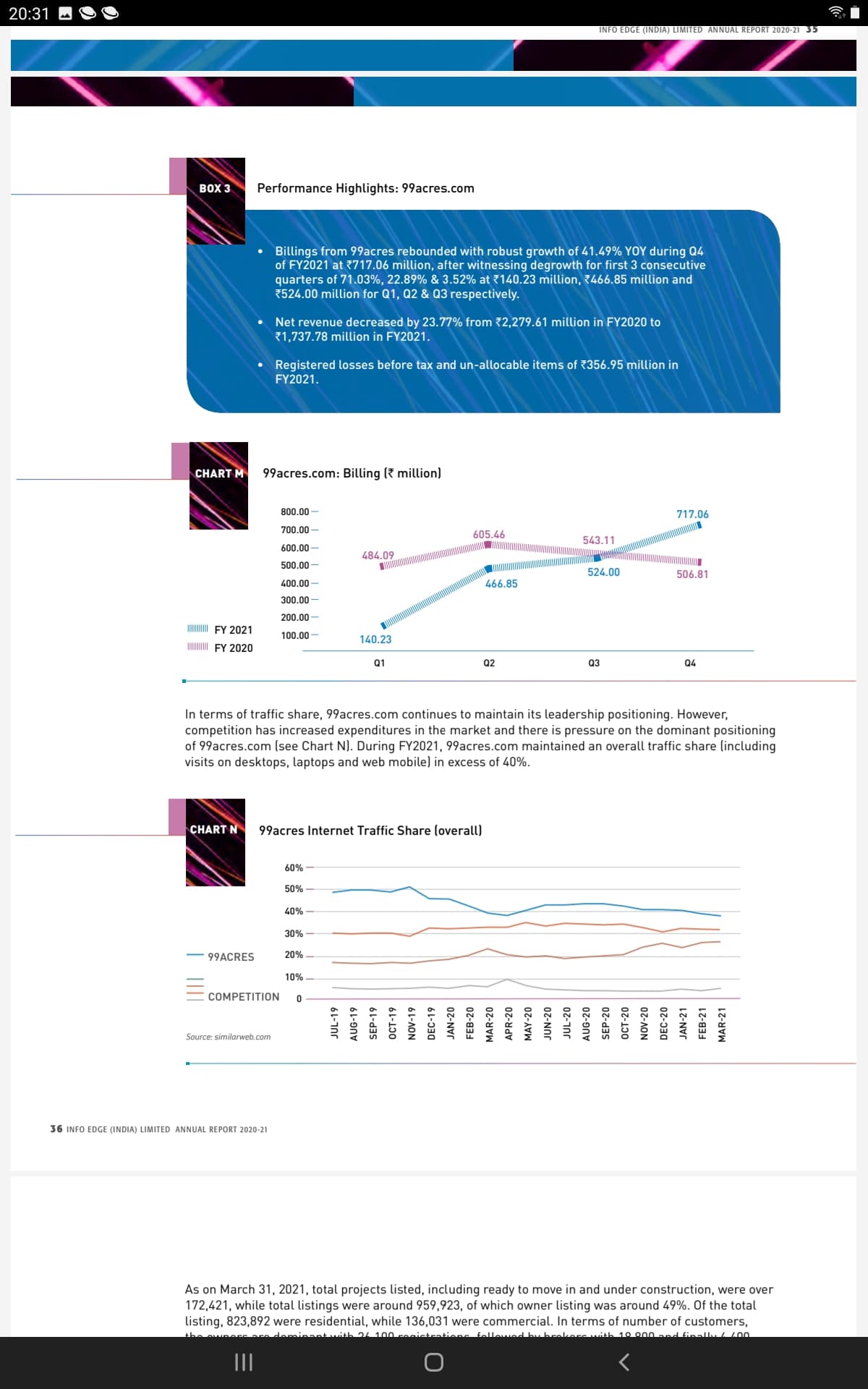

- 99 Acres - this is where opportunity size is large ( growing digital pie of RE mktg budgets, Organized RE players becoming bigger and so on), however competetion is catching up and they know it well, full org restructuring with sub verticals dor higher focus, leadership layer build up and heavy focus on personalization using analytics stands out. Performance has improved Q4 onwards but will need marketing push.

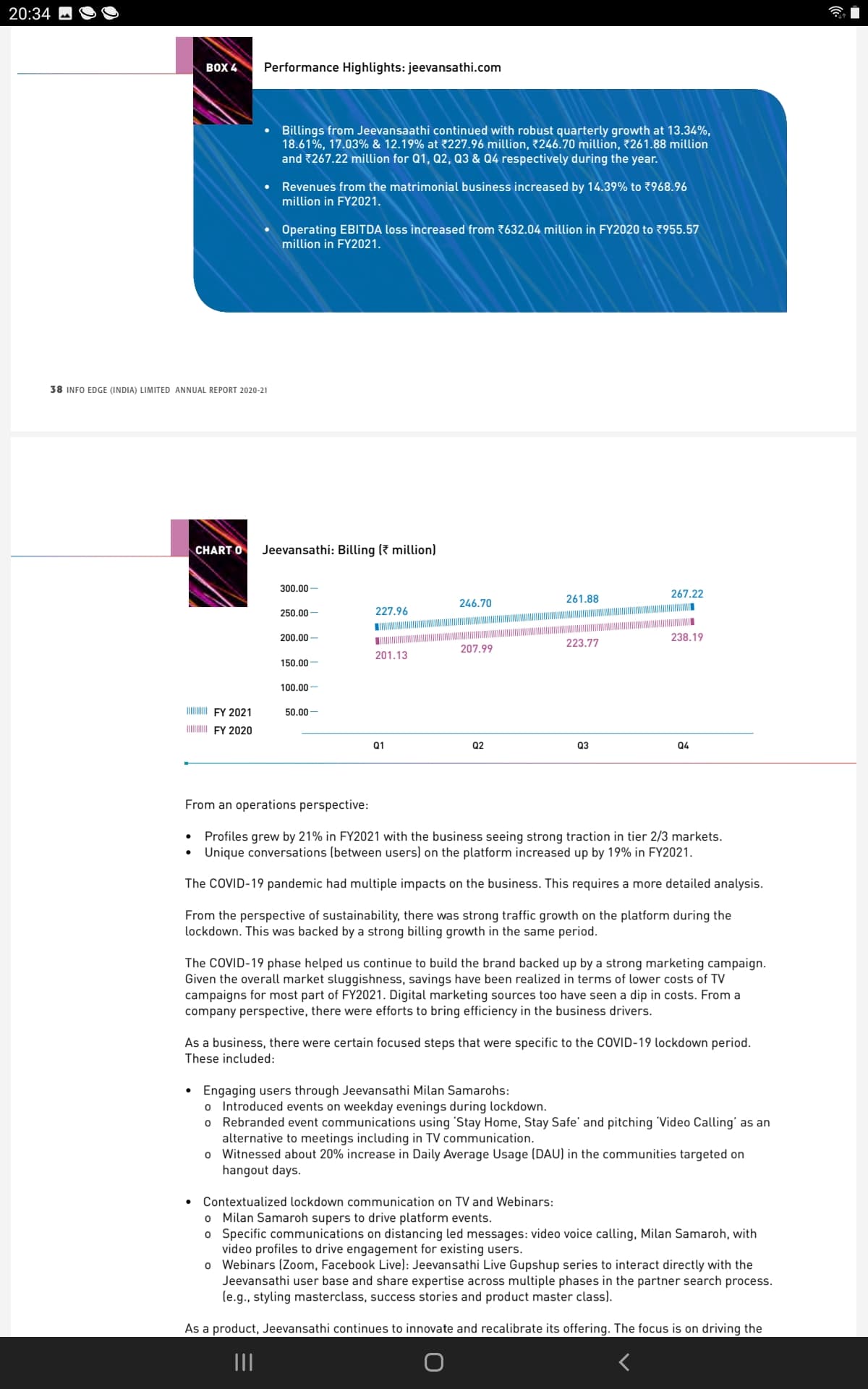

- Jeevansaathi - IMO A drag on bottomline and opportunity size is relarively small with very high competitive intensity - M&A / consolidation at industry level is a more apt solution ( esp when there isn’t a deep pocket PE money to burn) - mgmt has indicated that they are open to it.

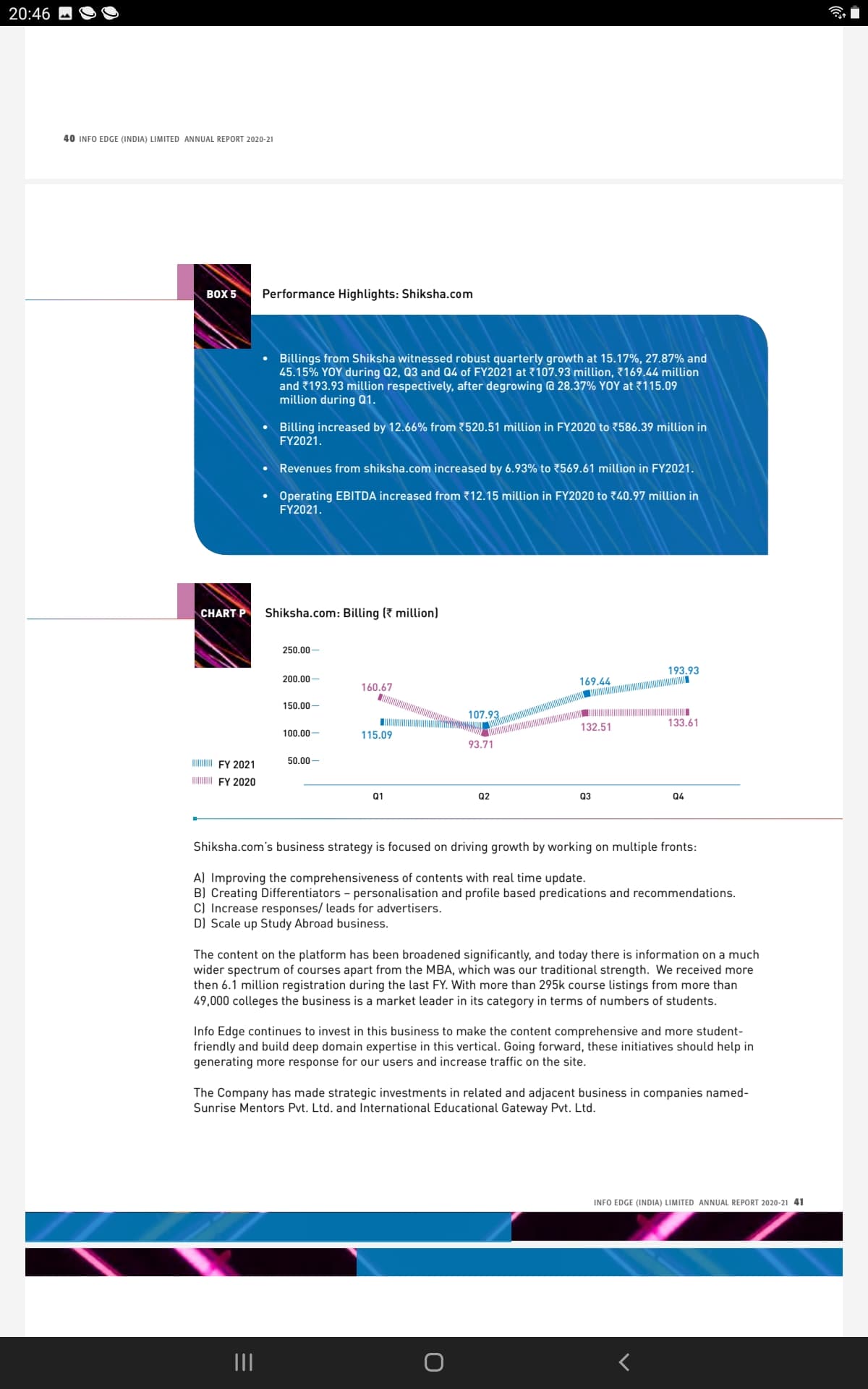

- Shiksha - a dark horse possibilities, lot of adjecncies beyond basic lead gen portal, they are working on content, UX - have got 21 M registration in FY21 - engagement with users is key as this has got good potential in large opportunity size of education institutions adopt digital ways.

-

Other highlights

-

While at the end of FY2020, the Company had a nation-wide physical presence through 77 company branch offices across 47 cities in India, by the end of FY2021, this was reduced to 70 company branches across 45 cities. The sales work force has reduced from around 3,098 sales, servicing and client facing staff by the end of FY2020 to 2,767 such staff by the end of FY2021 who support the businesses.

-

Investee companies

-

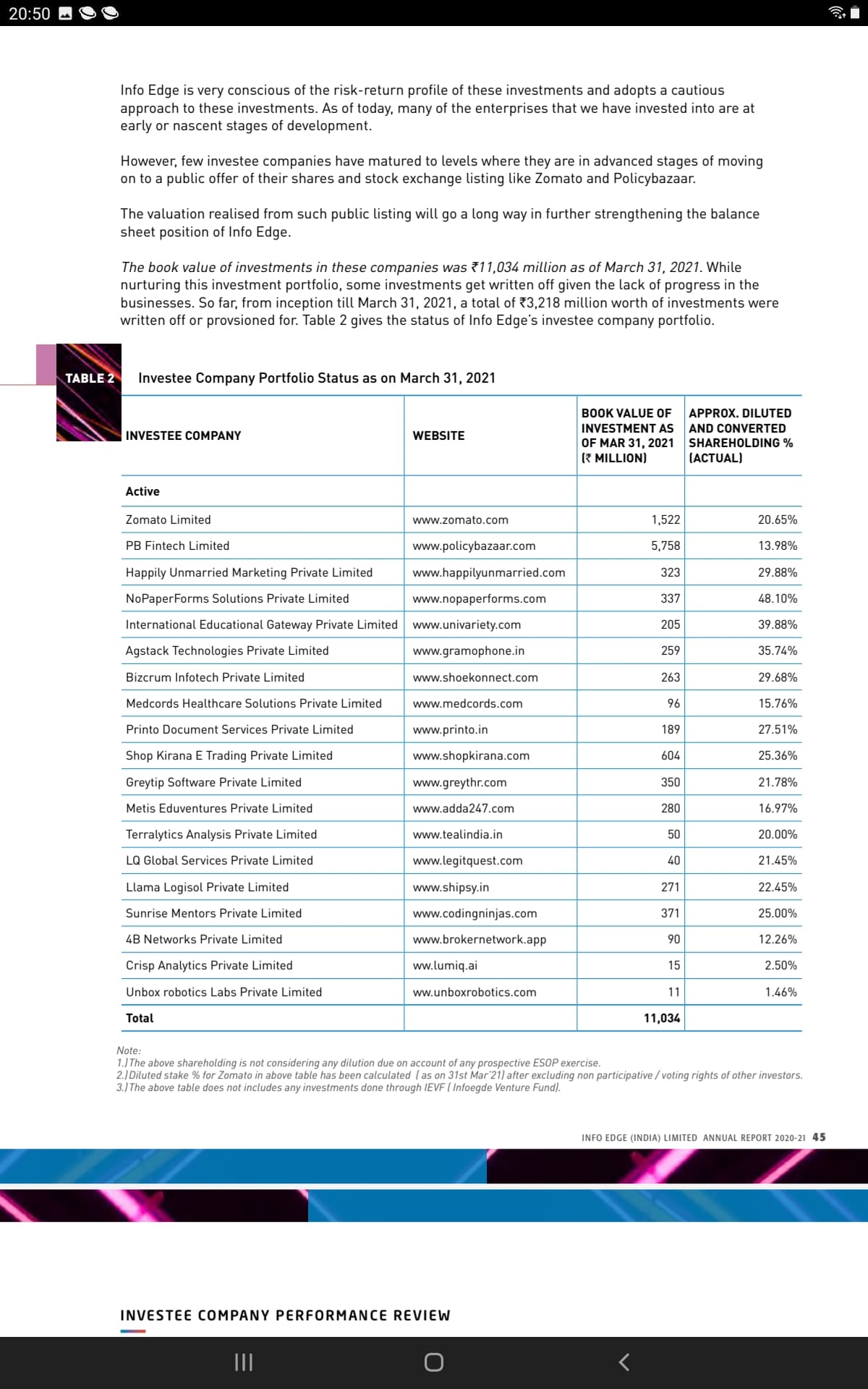

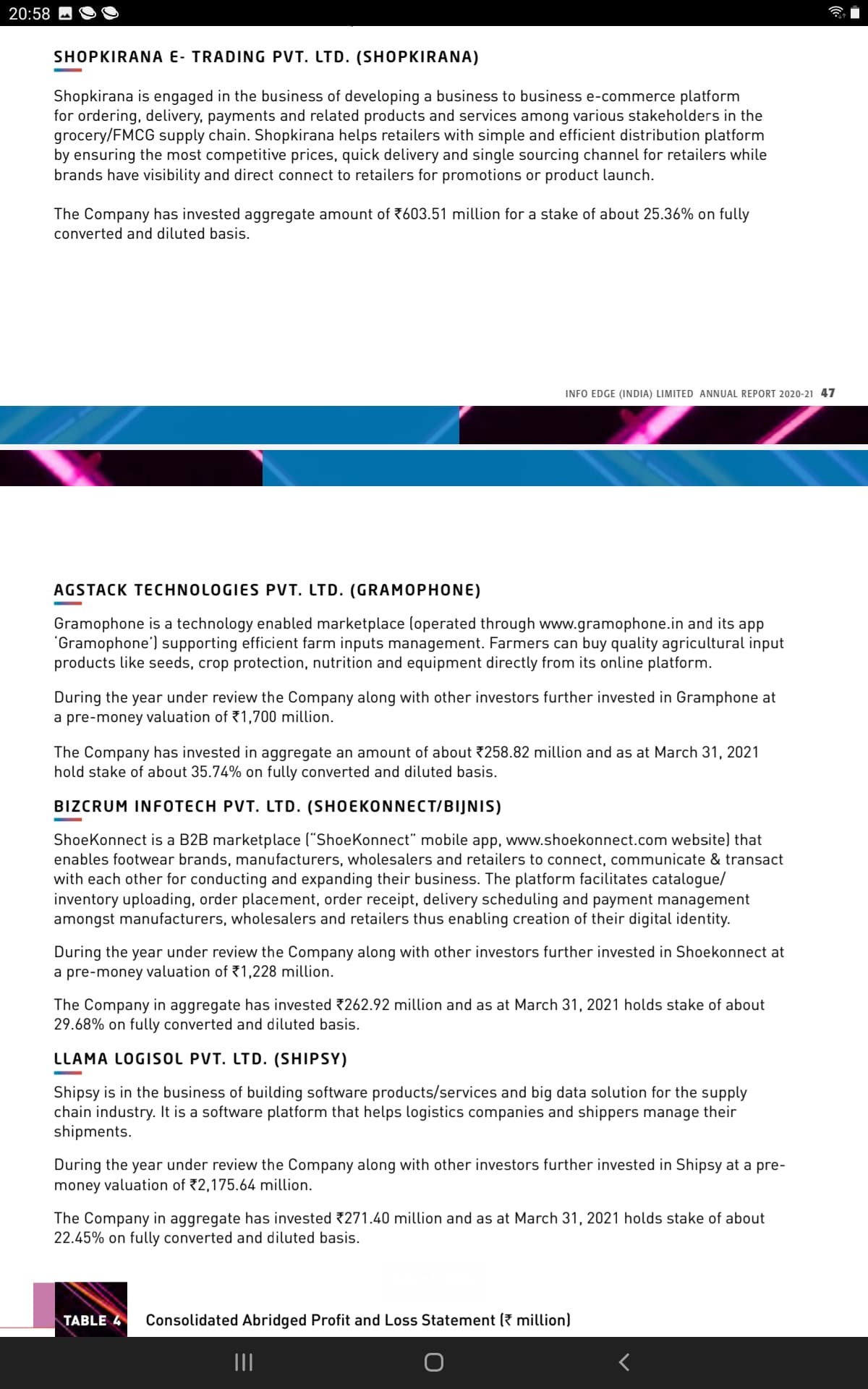

Interestingly among sizable investment they have specifically called out below four companies outside Zomato and Policy Bazaar- they wouldn’t highlight unless they are seeing good outlook - deserves further research. All four put together have Approx 1000 Cr + valuations in latest rounds.- Shopkirana, Gramaphone, shoeconnect, Shipsy - a common theme among all is large opportunity size.

Valuations ( Speculative and somewhat optimist cases)

- Core Infoedge ( Naukri, 99acres, Jeevansaathi, Shiksha - ) - approx 1500 cr rev in FY22 - 10X-15X sales puts it to 15000 -22500cr + 3000 cr cash

- Zomato - Listed now - Infoedge share of 20000 cr - listed company discount applies further

- Policy bazaar - news of IPO at 40000 cr, may list around 60000-70000 cr cr and Infoedge share at 14% around 9000 Cr - OFS if any and holding discount apply

- Rest all - no way to do scientifically but let’s say all put together 5000 cr.

Current market cap is 70000 cr.- Given all businesses have longevity and digital DNA - long term optimist view on tech driven businesses and optionalities + Proxy PE play on India digitization+ Top quality mgmt. Valuations is individual aspect and my bets are with them.

Technically looking strong in recent shakeout in market. Given Zomato+ Policybazaar( once listed) will have a lion share of Indoedge valuations in listed sense - there will be correlation in price movement going forward in either direction.

Disc: Invested as top holding in PF.

Even after very optimistic calculations, total value is coming at 60K Cr, 14% less than the current market cap. With all bull case scenario for Policy Bazar & Zomato factored in, the stock has very little upside from these levels in this quarter. The trigger of any upside will be generated by better than expected results from core business in next quarter (most probably 99 acres with expected rise in real state sector).

From Investee Companies of Info Edge, one company which I think everyone is overlooking is Greytip Software Pvt Ltd. It is a SAAS company providing HR management software GreytHR, currently it is being used by many tech startups in India.

https://entrackr.com/2019/10/greytip-raises-rs-34-5-cr-info-edge/

With over 9000 customers and 1 million payslips being generated on the platform every month, Greytip Software has become one of the largest players in the SMB HRtech space in India and is becoming the provider of choice for all fast-growing businesses.

Toshiba, Volvo, Dell, foodtech major Swiggy and payment gateway platform Instamojo are notable customers of Greytip.

With over 10 Million $ in funding, according to me the current valuations are around 30 Million $ (222 Cr).

Valuations are not much at this point of time but if new age tech startups are using GreytHR, then its a solid a validation to the product.

The HR Tech space is booming right now but that also means a lot of new competition. Recently Infoedge invested in another HR startup DoSelect

Disclosure: Invested In InfoEdge

Disclosure: I use GreytHR HRMS ![]()

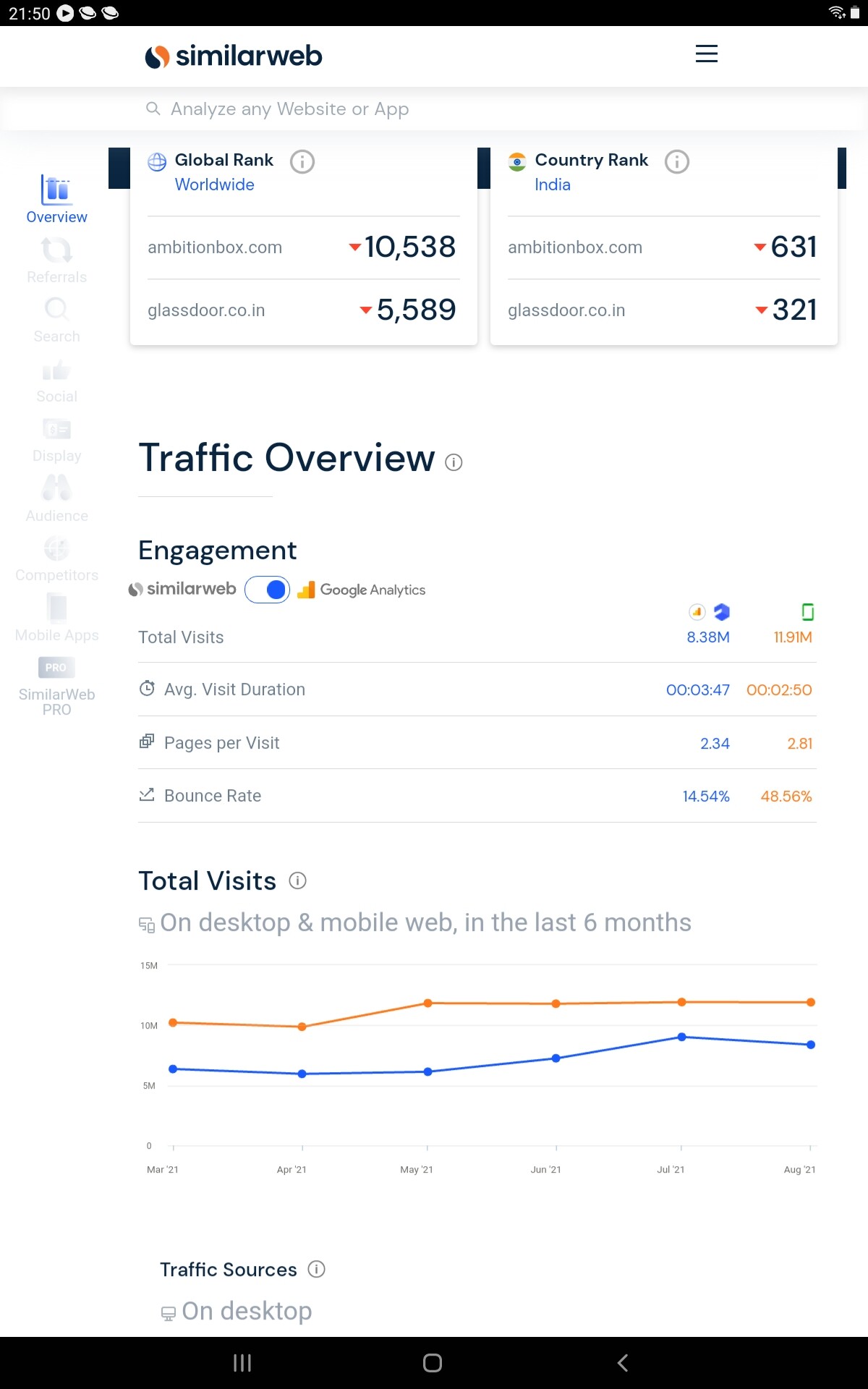

Infoedge owned company Ambitionbox catching up with Glassdoor and very close at traffic levels, very low bounce rate, and higher avg time spent reflects content quality as well.

There is a strong synergy with Naukri as segment( one needs both in any job changes).

With no of job changes over career span increasing every decade - augers well for Naukri as well as Ambitionbox, with Tech hiring boom, this seems very interesting though 2021 mkt focus is on Zomato and Policybazaar, more curious on next set of winners, Ambitionbox seems to be scaling very well, almost a duoply in their space. Need to better understand monetization plans.

Glassdoor valuations ( 3 yr back)

Ambitionbox promoters own version on his journey and Ambitionbox

https://mayurmundada.com/how-we-sold-our-startup-in-1-5-yrs-with-just-2-founders-and-zero-funding-the-story-of-ambitionbox-3b164d7c831f

Time for Infoedge core businesses to shine as well with solid tailwinds supported by Hiring and real estate industry growth all around. Should also help establish and monetize value add services that were launched in recruitment and RE spaces

Invested

Good market share is there, it gets competition from which other strong similar company?

info-edge-research-lab.pdf (1.3 MB)

Hi,

I have a couple of Questions w.r.t INFO EDGE. Do let me know if you know more regarding the following questions.

- What’s the plan when compared to Linked In Social Job Searching sites?

- Naukri is concentrating only on India and the Middle East. With the power of the internet why not a generic job site serving all the countries?

- Whats the new vertical info edge is exploring? other than the well know one’s like jobs, matrimony, real estate, and education.

- I have a strong feeling that the management believes more in acquisitions rather than writing their own product.

- Since all the traffic is from India, I assume that dollar appreciation has no positive impact on Naukri. In fact, it has negative impacts like the services (akami edge) are bought in dollars. kindly clarify on the same.

Any suggestions on long-term goals of info edge are welcome. Thanks in advance.

Are you considering with current situation and valuation to enter if not entered earlier.

would like to hear from you.Thanks

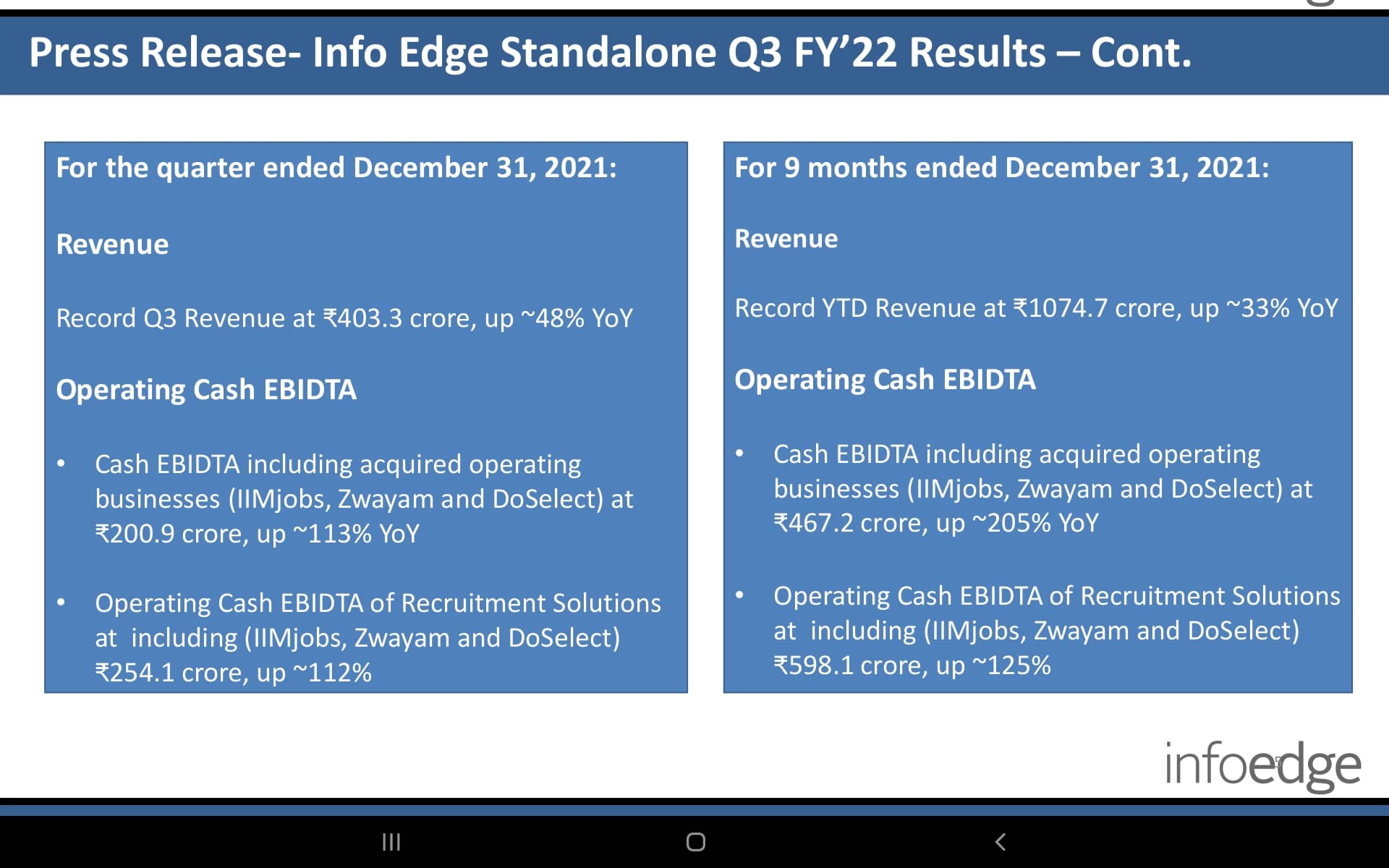

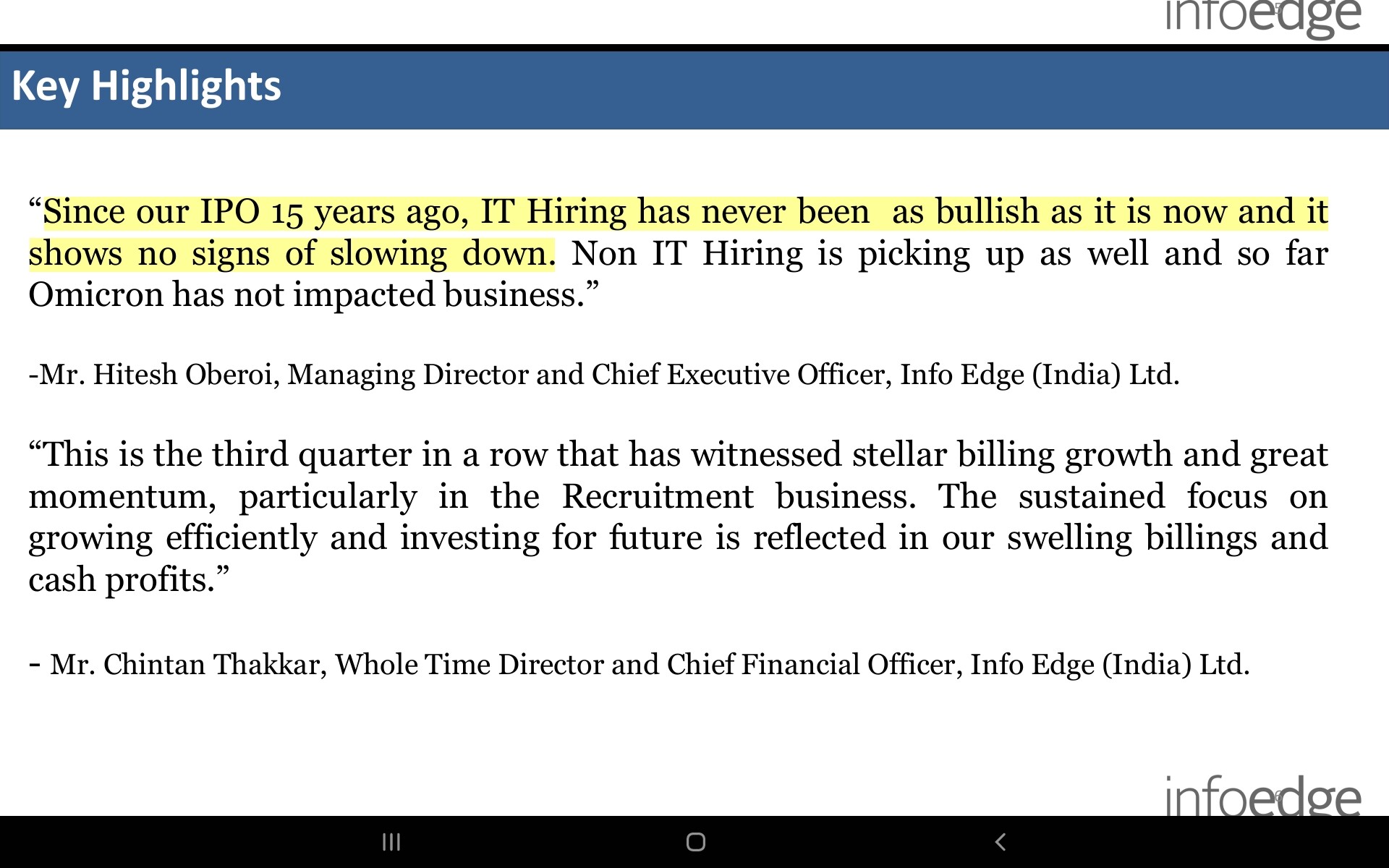

Excellent performance by Naukri core biz - By far the best numbers, quality of earnings is unparalleled

-

400 cr revenue, 250 cr cash EBDITA runrate , EBDITA Margins at 60% , that is a real example of operating leverage monopoly at work, which is an eternal cash flow machine

-

Demand scenario is strong ( also reflected by much higher billing growth than revenue - read as future revenue)

It would be understatement to say that Naukri business vertical itself growing strong at 30-40% topline and much higher at EBDITA level - this is a sheer monopoly and cash flow machine- FY 23 with this type of IT hiring they can do a topline of 2200-2400 cr and 1500 cr at EBDITA- at 35X EBDITA the entire current mkt cap is just Naukri vertical valuations. Even if growth tapers down if future to historical 20%+ level , this business will keep throwing cash for eternity.

Invested and adding in dips, and believe this is a basket of top India consumer brand tech story, ( Naukri , 99acres, Jeevansaathi, Shiksha being core, Zomato, policy bazaar and many more investee companies), each of them with a very very long runway. Current tech sector beating is a good opportunity in many ways.

Are these numbers sustainable? We all know attrition rate is very high currently but it’ll cool down in few quarters so my question is after that will naukri be able to generate this kind of revenue and profit from it’s core business?

Disclosure : Not invested

https://www.bigshyft.com/ is a new offering for premium candidates by Naukri. heard it will be marketed soon

InfoEdge Edge is Huge Cash Generating Internet Conglomerate while most of Internet Cos burning the Cash

Have around 17-18K Cash/Cash Equaliant approximately 1/3 of Market Cap

Around 1000 Crs plus Operating Cash Flows

Bouquet of Great Investments

Promoters are Great Capital allocators

Expecting some more lottery like Zomato & Policy Bazar

where to source this data? “1000cr. + operating cash flow”

It’s annualized based on this qtr Cash Ebitda of 254 Crs