Can someone tell why did they sell their meritnation stake at 100 crore loss in january? Infoedge invested a total of 150 crores in meritnation through various rounds and suddenly they sold their complete stake for 50 crores. Any reasons?

1 Like

This is the trend which is very visible. Now many FMCG, big hotel chains, medical stores etc are partnering with delivery service to reach customers.

1 Like

I got interested in Info Edge because I felt it might be recession proof business. But when I started researching, I found stock to be overly expensive. This is one of the stocks which one likes to have in the portfolio because of great promoters and brands but not at this price.

Let me run a bull scenario

Company maintains the same revenue as of FY20 with no growth. This would be the best case scenario. In my opinion, it is highly unlikely.

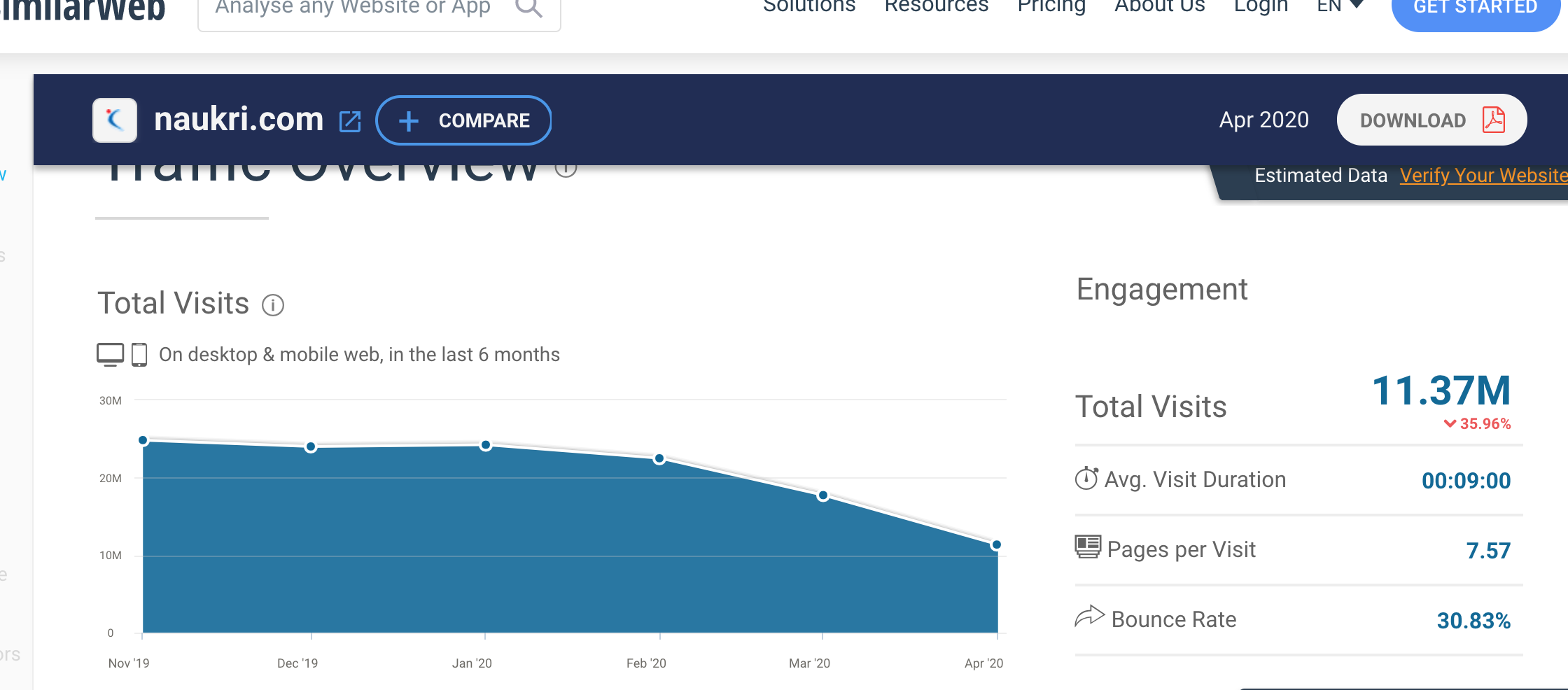

Revenue would take a dip because traffic on all websites (Naukri, 99 acres, Jeevansaathi, shiksha) are down 35%. Check similar Web: https://www.similarweb.com/website/naukri.com#overview.

This is opposite of the belief I had , I thought people were getting fired and would go to Naukri for job search. Maybe that’s not happening. In the concall they mentioned, a major part of Naukri revenue (which is the only business with positive OPM out of 4 core business) comes from institutions and not from the candidate side. I expect revenue to come down a lot because hiring is not happening anywhere. Also, they have over-dependence on IT in Naukri business (source concalls) which is also hit.

The other interesting thing is the sell report. Report clearly states that the Linkedin entry into the Hiring business will hurt Naukri. They did the same to Monster.com in the US at the time when Microsoft deep pockets were not backing them. With Linkedin cash burn capabilities even the hiring business would slow down in growth. https://www.barodaetrade.com/Reports/InfoEdge-InitiatingCoverage12Mar20-Research.pdf.

In 2008-09 Monster.com was valued at 5x PE. Here Naukri is getting valued at 60X PE. Because consolidated OPM is negative for infoedge, I would value company 10X sales.

Hence 10*1000 crore = 10K crore

The other part is startup investments. Apart from Zomato and PolicyBazaar all others are too small to move the needle. Even if we take Zomato and Policy bazaar valuations based on last round (because bull case) that comes around 6-7K crore. I expect Zomato valuations to cool down with no food delivery orders happening in most of the India.

Total comes around 17K. Company is currently at 32K. What is the correct price to enter here?

2 Likes

To clarify, India is basically a service sector, most of the IT firms caters to US or European clients, so companies performance in those countries reflects back here in India for the IT sector!

Hiring & firing, India being a low cost labour market, is somewhat resistant to firing, but cost cutting has halted hiring here in India, I know this because I am a software engineer and approx. 70% of friends too are.

After attending Bostons all hands meet, I could say that the companies would in the future move to India for more of their project(Low cost market)

So I am very much positive about the future Job market in India, but at the same time until things cools down & businesses are running normal, hiring are very much an issue.

If the company sells its stake in these companies and generates say 6000 crs, do you think the company will park these funds in liquid funds, I dont think so. They have the capability to deploy this cash to get an yield higher than risk free rate and so this cash does need be valued with some premium say 10000crs

1 Like

I disagree with this - cash is always valued at face value till it is gainfully deployed.

If it is deployed at risk free rate then the corresponding cashflows are also discounted at risk free rate

If the company deploys it in business/ investment then the cashflows are discounted at the cost of equity which is higher than risk free rate

Usually companies don’t have significant cash in investments, so you don’t need to worry about this.

But valuing cash higher than face is absurd.

3 Likes

I am confused - are you saying that hiring would be negatively impacted or would remain unaffected- from what I understand, you are saying that people won’t be fired but won’t be hired either - in that case info edge should be negatively impacted, right? @deepender thanks for sharing this analysis

2 Likes

yes, people won’t be hired & info edge should be negatively impacted in the shorter run, I would say 2 quarters(If being more optimistic then 1 quarter)

Why mr. Market is still awarding high valuation and long rope ( when many stalwarts are beaten around esp finance etc).

- One of the only listed quality tech platform theme player, quality mgmt, proven record - lot demand and limited supply case. Naukri is undisputed leader and will retain/ grow mkt share as percentage. Infact over medium term - now layoff and later hiring will lead to higher churn and thus income. Will mkt re’rate for 1-2Qtr issue? Swift bounce back so far.

- PE model to play India story - policybazaar seems to be doing good, Zomato may suffer but so will competition, 99 acre is well placed for RE landscape will see consolidations - burn is in control. They may acquire few more at better valuations given situations.

- See similar trend for Affle, IRCTC, Indiamart ( very short history and yet yo prove)- clear trend of theme holding on to as of now.

- All these businesses are better placed to survive well opposed to capex heavy biz,

Titan, Bajaj fin or HDFC bank is a great biz but still riskier than Infoedge, Indiamart or Dmart where market seems to be giving long rope. FMCG will fall somewhere in between.

My personal views!!

Invested in all names.

3 Likes

Market can do whatever , as an individual we need to decide if we can enter at current price. Let me answer all your points one by one:

a) when many stalwarts are beaten around esp finance etc: Because they started giving bad quarter. If our assumption this is just 1 -2 bad quarter then same applies to BFSI, they will bounce back much faster and return will be more here because they have corrected more than 50%. Market is valuing info for growth if quarter result doesn’t show that then it will not be patient.

b) Regarding quality management, no doubt. One of the best promoters of our country hence company deserve high multiples. The question what are the multiples justified. If we see a drop of 30% in revenue then this business might not be a recession proof business what we are paying for. Also, please read report of Linkedin coming into hiring space and disrupting Naukri. Already on last con call, Hitesh mentioned that competition is forcing them to spend money on advertisement in Naukri, first time after many years. They are seeing decline in CV uploads etc. I feel Linkedin with so much cash (Microsoft backed) in hand will just continue to spend.

c) Regarding PolicyBazaar and Zomato: I am valuing them based on last round only because this is a pure bull scenario.

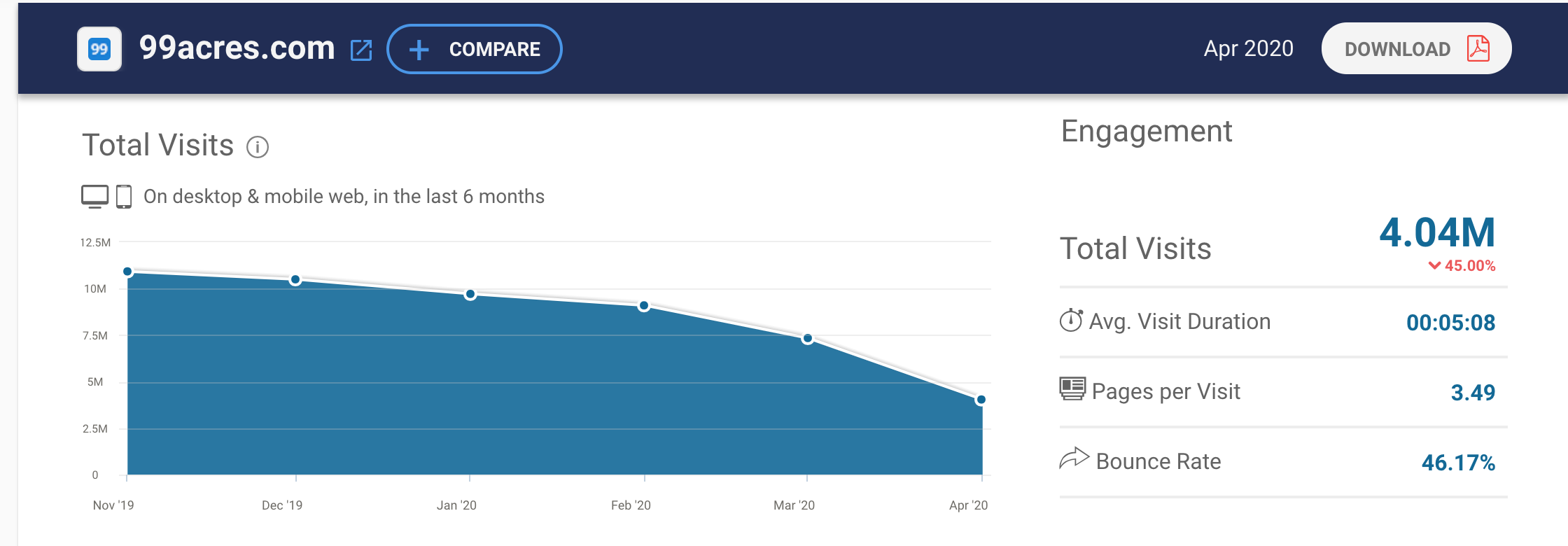

99 Acre is a difficult business, Hitesh mentioned on concall, they see a lot of churn in 99 acres and site traffic also down 45%.

Other interesting thing Jeevansaathi traffic is down 5% whereas shaadi.com 2rd in space after Matrimoney traffic is up 11%. I think this might be because of shaadi.com advertisement coming on TV. Looks like competition continue to spend and they will have to do the same.

- A week ago, you could have added AsianPaint and others FMCG list. But now they are down around 15%. Market can change mood anytime, we need to make our individual decision based on facts.

2 Likes

A counter point - Longer an applicant stays unemployed, more likely he is to buy a paid 3 month subscription to get faster access to opportunities etc.

1 Like

2 Likes

Which contribute only 10% to revenue and does not make large impacts. Almost 60% revenues are generated from the Resume database access service, which is consumed by the Job provider. which will be going to tack a big hit.

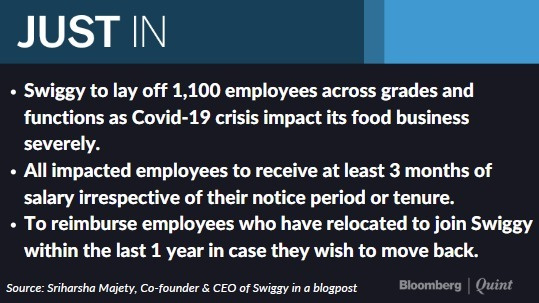

Zomato will let go of 520 people or 13% of its workforce and undertake up to a 50%

CEO, Deepinder Goyal, said, “A large number of restaurants have already shut down permanently, and we know that this is just the tip of the iceberg. I expect the number of restaurants to shrink by 25-40% over the next 6-12 months. What actually happens, for better or worse, is anybody’s guess,” he said.

2 Likes

3 Likes

Info Edge

Sharp Slowdown in Business in 1H

Recruitment sector should bounce back first

Property may take a while to recover

Zomato has seen a sharp slowdown in demand post-COVID-19 (April vols down 70%)

PolicyBazaar less impacted; Paisabazaar affected

Source: Citi Conference

: Got it via tweet from journalist Dharshan Mehta

2 Likes

Competition would get even more fierce for zomato - Value of investment in zomato is currently valued at ~5k cr (~17% of current market cap of infoedge)

2 Likes

https://www.barodaetrade.com/Reports/InfoEdge-InitiatingCoverage12Mar20-Research.pdf

Report gives good insight into segment wise competition.

Structural threat to Naukri: INFOE is a clear leader among online job listing platforms in India with 85% market share at Naukri.com (ex-LinkedIn). But we believe an inability to evolve beyond job listings puts Naukri at serious risk of competitive headwinds – reminiscent of the decline at erstwhile US market leader Monster.com post LinkedIn’s entry. Our view is premised on (1) LinkedIn’s clear edge as a professional networking platform (vs. a plain vanilla job listing portal),(2) its steady user base growth in India (at nearly double Naukri’s run-rate for FY14-FY19), and (3) parent Microsoft’s deep pockets for product innovation.

Elusive profitability in 99acres: INFOE’s portal 99acres.com is also the No. 1 property platform in India, but persistent weakness in the residential property market and stiff competition – marked by a narrowing traffic-share lead over the second-largest peer – hinder predictable, profitable growth. In 9MFY20, 99acres posted EBITDA of ~Rs 90mn. We expect future profitability to be elusive as rising competition from MagicBricks.com and Housing.com drive up advertising and marketing spends moving into FY21.

3 Likes