The incentive to make best efforts will remain as long as promoter has significant wealth tied to the fortunes of his shareholding. Having a benevolent owner at the helm is necessary, but not sufficient, to ensure management has a long term strategy. It’s not necessary for the owner to run the business themselves, they can always employ capable managers having right values for the job. For the minority shareholders, it is more important to ensure that the owner has integrity, so they wouldn’t try to cheat the minority shareholders in future. The Info Edge promoters do have sufficient holding to act as owner, and this holding represents a significant wealth for them.

Of course promoter has better insight into the business than the average investor. It’s natural to wonder whether promoter buying/selling can be used to make a profitable trading signal. Page and Bajaj Finance are good examples where it worked. But a trading signal must be thoroughly tested to determine if it gives an edge. You must also look at the incidence of deconfirmatory examples. Also, if you decide to use a trading signal, you must use it consistently. You cannot use it sometimes when it support your position, and ignore it otherwise.

I don’t believe promoter buying/selling information obtained from exchange would give any trading edge, as it is easily available information to everyone. Let’s look at Page again, its promoter holding was reduced from 51 to 49 in Mar 2016. Its price in April 2016 was around 12k, and the holding remained constant till June 2018. The price peaked around August 2018 at ~35k. Even after the price fall, the investor/trader is better off ignoring the Mar 2016 stake reduction.

Thanks for the revert. this is helpful . What do you feel would be growth drivers of Info edge in future and what growth can one expect considering its into multiple streams of businesses ?

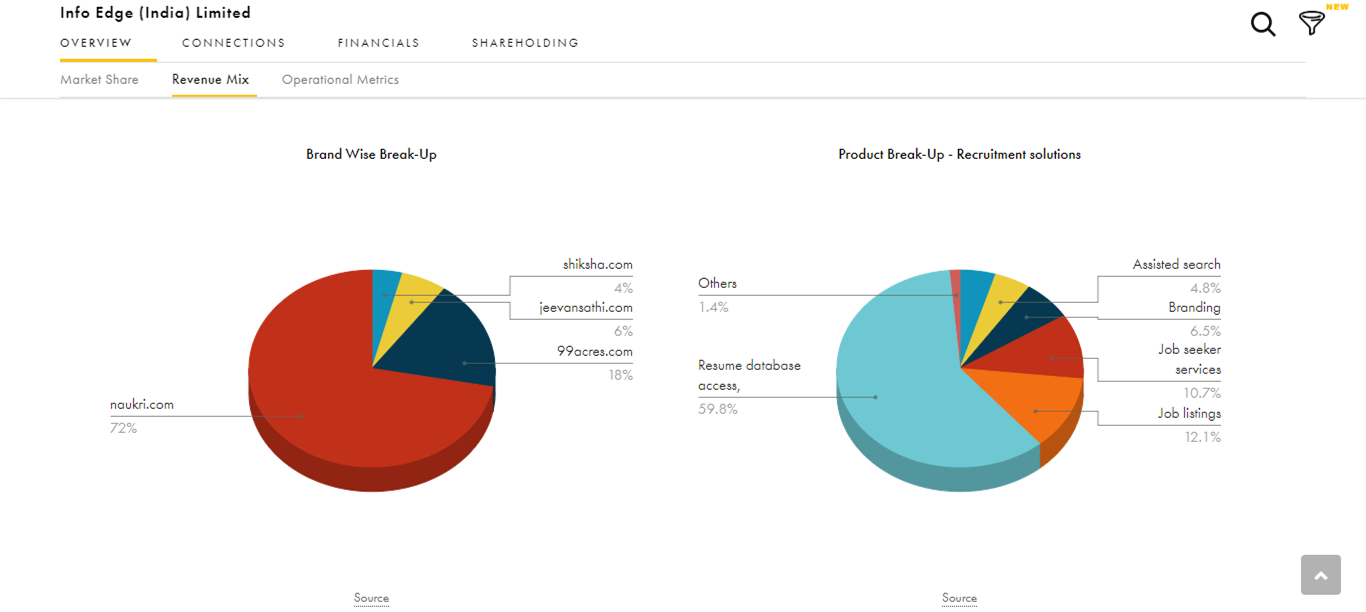

The 4 operative business Naukri, Shiksha, Jeevansathi , 99 acres where they own 100 % is growing 18 % annually and should maintain that growth. Losses from 99acres and Jeevansathi will now be minimal and can expect breakeven this year due to to more adoption.

The large business zomato they own 23 % grows 200 % annually. operational level zomato is doing good but as they expand to more cities there are losses.

Policy bazaar they own 13 % grows 50 % annually.

The 10 other investments are in growth mode and will grow 25 % annually though large loss making.

So broadly Infoedge will keep growing 30 % plus consolidated along with proportionate share of associates.

future positives : they have cash balance 1500 and annually they add 500 cash from operations. So we can expect 5 new start ups coming up plus more money being put in current investments.

The new VC venture where invest 100 cr will bring in more partners with larger amounts. This VC enables investments where Infoedge balance sheet cannot manage.

Largely valuations of the consumer internet sector will keep growing due to more adoption and increase in use of smart phones.

over last 10 years , promoters stake has come down due to Stock options & one Qip 5 years ago. Their own promoter sale very small and promoter do that for their personal requirments. Here owner has founded Ashoka University and some money went there . Personally I am not worried due to to reduction in stake as they are clean and transparent & have no governance issue.

Naukri is promoting their new platform learning.naukri.com way too much, and I’ve been receiving the mails daily and it looks promising. Their courses are ranging from 1K to 7K so far from what I’ve seen. Its really an interesting take here to observe.

“” Info Edge (India) Limited announces Q3 FY20 results for the quarter

ended Dec 3 , 2019, Q3 Net Sales (Revenue) up by 14.0%, Billing up by

10.3%, Total Income up by 9.7%, Operating EBITDA up by 27.2%""

Believe this trickle of slowdown(although Q3 seems alright with solid EBIDTA growht) may turnout to be good for Infoedge,

Slowdown in recruitment at industry will force smaller players to struggle/newer players to stay out, with network effect in play(leading traffic share maintained) and inorganic steps(IIMjobs acquisition), Training and value added services - as of now they seem to be well positioned, would be great to see them innovating and evolving around Gen Z specific coverage (niches in jobs/higher churn/gig economy and so on)

Slowdown in real estate is resulting in consolidations among industry - so will be the case of online space - 9 mo performance of 99acre is commendable - rev growth from (137 to 171cr) losses narrowed from 28 cr to 4 cr. Infact Q2 was positive - this reflects pricing power in hand.

with recent F&O entry and recent frenzy around Internet stocks(IRCTC/Affle/Indiamart) - this tech segment is under owned in India (not referring traditional IT services setups) and bound to get larger players attention.

I think Info Edge is a better play on increasing internet and smartphone penetration in the country, than telecom or internet services providers and smartphone manufacturers. Competition forces the service providers and manufacturers to keep investing in improving technology, leading to better and cheaper options for the end consumers, and hence the explosion in smartphone usage in the country. The absence of moat for the telecom providers and smartphone manufacturers leads to low returns for their investments and flow of value to the end consumers.

The huge networked population, which is further growing, is disrupting how businesses used to find and reach their clients, and vice versa. The internet platforms which connect these businesses with their clients, the buyers with sellers, become important. Network effects ensure that most buyers go to platform with largest number of sellers, and vice versa, therefore building a strong moat for the dominant platform. Info Edge is doing a good job at building these internet platforms with network effects. Naukri is already a dominant and profitable player in its area, and the other ventures are being funded mainly with its profits. Longevity of business and huge potential for growth will ensure that the stock appears expensive when compared to other businesses not having these characteristics.

Beg to differ on this. With young demographics and job market not being so benign, more job aspirants will flock to Naukri com. If, let us assume, out of 100 job seekers who are registered on the portal, 10% opt for the paid services. The percentage will increase in case of recession, as the job seekers would want to buy premium services that could differentiate them from others - a new look of the resume and other value added services. So, more revenue for the company. This is just one angle though, and there will be some other positive / negative effects of recessation

Depends on the split of the revenue share they get from corporates and the individuals uploading their CV. If the revenue share from corporates is higher it will be negative for the top and bottomline of the business IMO.

Job seeker services are a small portion. The database access to recruiters is the major one which will suffer.

Also, apart from jobs, the other significant business is the real estate one through portals such as 99acres. These will suffer as liquidity dries up.

Some part of revenue may be annual subscriptions which may not be impacted much if the situation resolves in a month or so. Need to understand accounting practices to evaluate quarterly impact.