I may be wrong here - dynamics here seems powered by a proxy to PE theme participation in possibility fastest growing economy in world( at least pre covid). Only listed major player ( Affle and Indiamart being others)

Naukri - seem to holding on to leading( by miles) mkt share in core biz over last many years, competition hasn’t make a dent yet, network effect at play, throw some innovation too( premium, ad biz , e-learning and so on…). None of Microsoft acquisitions have done great vis a vis when they were on their own. LinkedIn doesnt even have a proper billing based out of India and evading serious tax - it is on govt agenda.

All subsidiaries and investment are Digital platforms- covid issue seem to be only accelerating digitization. All these startups are motivated, aggressive, backed up by respected institutions.

IMO - most of them will come out stronger ( temp bump for Q1) - key would be to correlate evolving consumer trends and platform usage/stickiness as opposed to only quarterly performance.

Another big player, which can cause huge disruption, entering into food delivery segment. And it is entering at the time when zomato and swiggy are finding it difficult to survive.

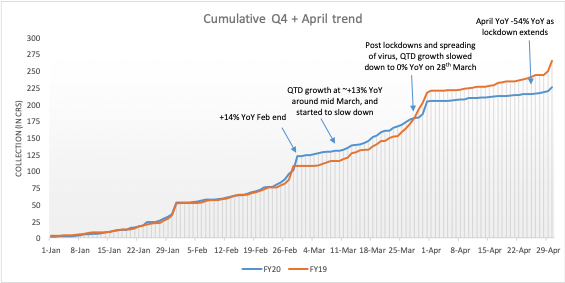

The company made a disclosure of material impact of CoVID–19 to the exchanges on 3rd Jun 2020 - wanted to highlight one stark change between FY19 and FY20 - the collections have dropped significantly for the month of April (~55% drop). The drop is even more pronounced for 99acres, where the drop in collections is ~86% for the month of April 2020. These 2 contribute ~90% of revenue for info edge c6039e93-5c56-4720-9dee-92ddd8a5f871.pdf (1.7 MB)

*

Collections in Rs. crs

FY19 + Apr’19

FY20 + Apr’20

YoY change%

Jan+Feb

110

125

14%

Q4

220

205

-7%

Mar

110

80

-28%

Q4+Apr

268

225

-16%

Apr

48

20

-58%

-the numbers are not exact as they have been inferred from the chart

I am unable to understand that why is the company reporting a net loss in the quarter ended December 2019 on a consolidated level. Even though the standalore numbers show a profit?

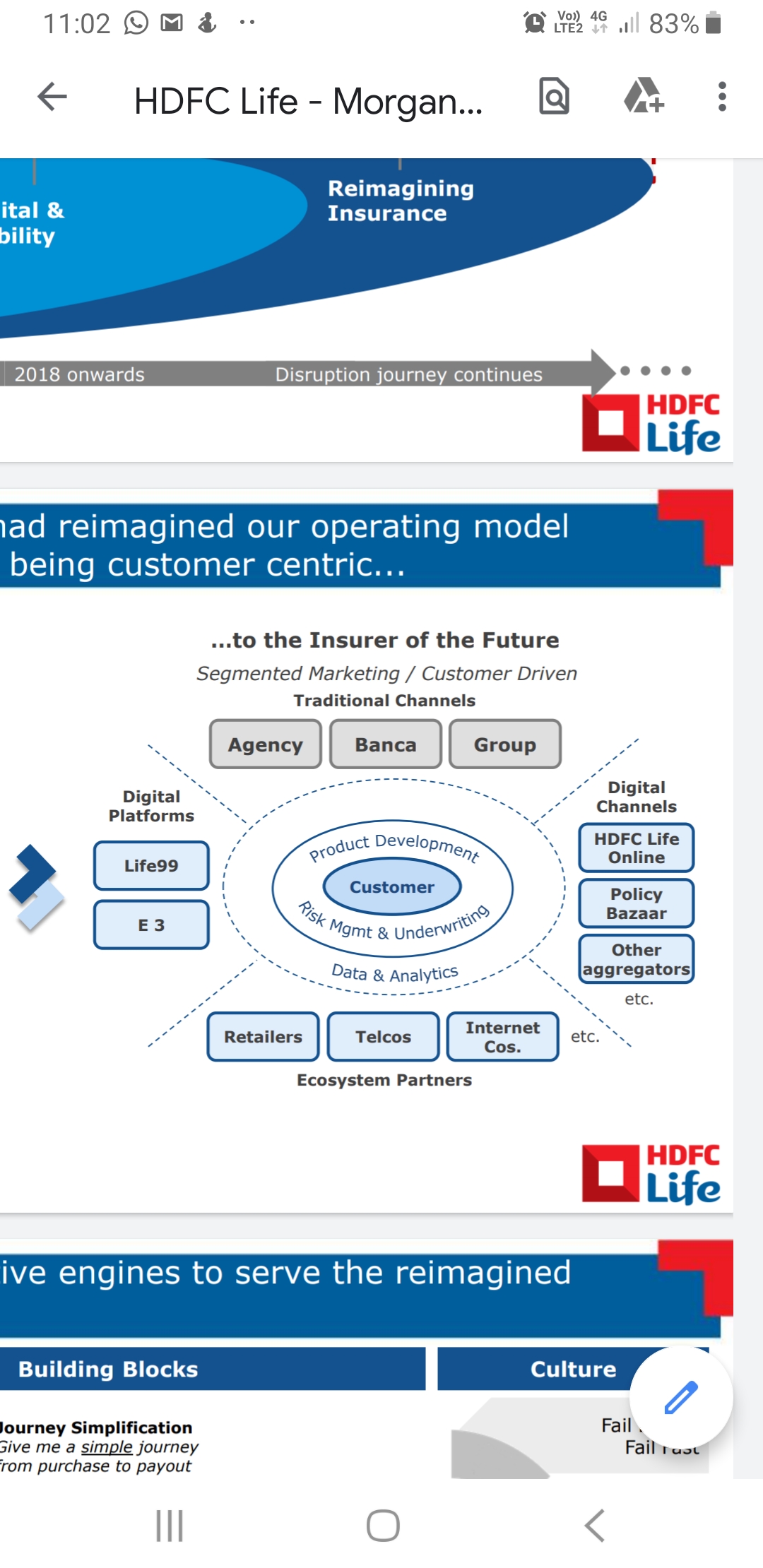

From Infoedge investee companies…Policibazaar seem to get lesser reaction in talking circle …good to see HDFC life quoting them as key channel in their key biz transformation deck…insurance landscape is evolving and policybazaar is likely a key beneficiary

Sometimes you end up missing out on stocks. That happened to me with info edge. I’m building a portfolio for the future and if info edge isn’t the future I don’t know what is. I’ve never valuated a pure tech company like this though. At the current price and PE its reached nosebleed valuations and I can’t get myself to justify buying now. A quick cashflow calculation puts the fair value around 1600 or so but considering its sitting on bohemoths like Zomato , policy bazaar etc which will add huge profits in the future how do we valuate this company for an entry point? Should I apply the same logic as Amazon/Tesla/Google etc for this and assume high PEs are just to be expected? Almost hoping some catastrophic quarter results pop up so I can pick it up on dips lol.

So as mentioned earlier I missed out on this stock at lower levels and considered hopping back on now. However, the more I researched the more I realised that maybe it really is overvalued currently. Naukri is its bread and butter and it’s what runs the whole show profit wise atm… however with linkedin(with Microsofts backing) getting bigger and bigger in india their growth rates could tumble. I’ve used the backend of naukri too to hire people… and that’s where most of their money comes in… companies hiring people. I can bet that not many companies will be looking to hire for some time. So if naukris growth stalls for a year due to this(and even longer later due to linkedin) then their main source of profits gets hit first. Then we have 99acres which was their second source of revenue… that too is obviously going to get hit since real estate is the last thing on the average consumers mind at present. Thirdly, just looking around me here in my hometown I can tell you a lot of restaurants are shutting down. On paper it seemed Zomato would do well this year since poeple would have to order in… but if restaurants shut Zomato becomes a giant expense account waiting for an outside investor to back it. And finally, Jeevan Sathi and shiksha could continue to do well but one is 3rd in the competition for marriage material(in a time where contact is is disapproved btw) and one is in an industry that is in turmoil at present with postponed exam dates/college restart fears and college fees that have reached stratospheric levels and are too high for most during a recession. Maybe I’m just bitter I missed out on infoedge so my post is a bit pessimistic… but the market has priced in all optimism (and then some) into the current cmp so to balance it out I needed to be as pessimistic as possible. I am expecting a huge correction here over the next few months… (and if it does happen im pretty sure i myself am going to ignore everything I’ve written above and jump aboard sub 2000 )

Food deliveries at quick service restaurants back at pre-covid levels

Zomato and swiggy has been quite agile and nimble in response getting back to 50% pre covid levels as claimed is remarkable in two weeks of lifting lockdown. See some lasting behavioral changes

Days of crazy cash burn are over, better cost control and sense will prevail - path to profitable operations will be accelerated with investors push.

Restaurants have realized that these partners are essential channels in growth and have equal importance as dine-in if not more in this new normal - clash/logout campaign disruptions are unlikely

3 Consumer mindshare and trust is gained o er last few months , and going to help in long run - as long as quality and safety is not compromised

Aggression, agility, scaling operations and adaptability to change - all of this at speed is best demonstrated by these startups and teams leading them - we know now they are emerging stronger

Zomato is a significant driver in Infoedge valuations and getting back on track , Policybazaar is a no brainer gainer from these disruptions - second largest investee company.

Infoedge already shared transparent updates from owned brands and Q4 & Q1 likely to be impacted but as they say market looks further ahead and most of these businesses are likely to bounce back.

Did anyone attend the concall or have the transcript? Results are not half bad and everything looks on track. Waiting for the management commentary though if anyone has it. Cheers.

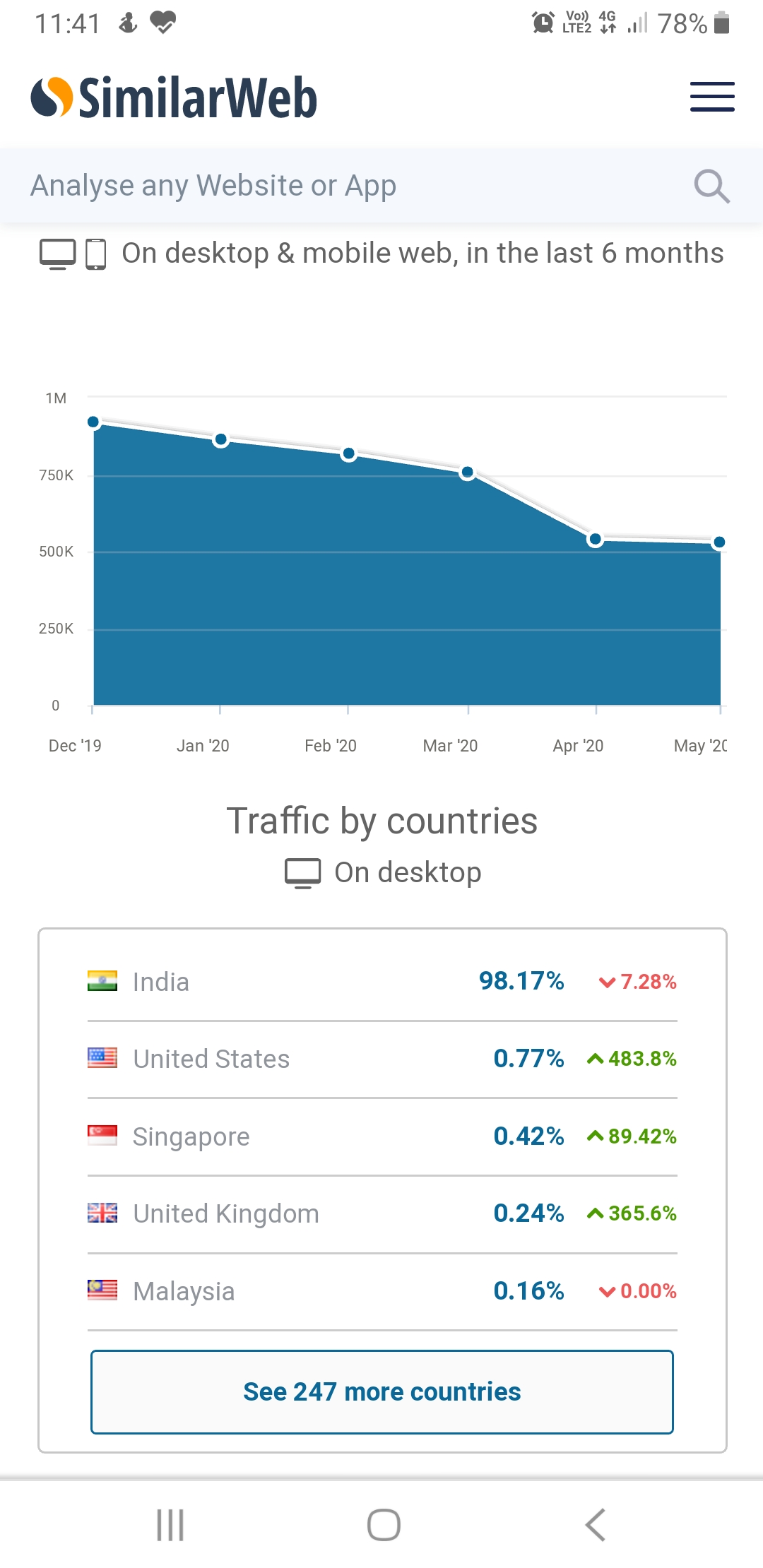

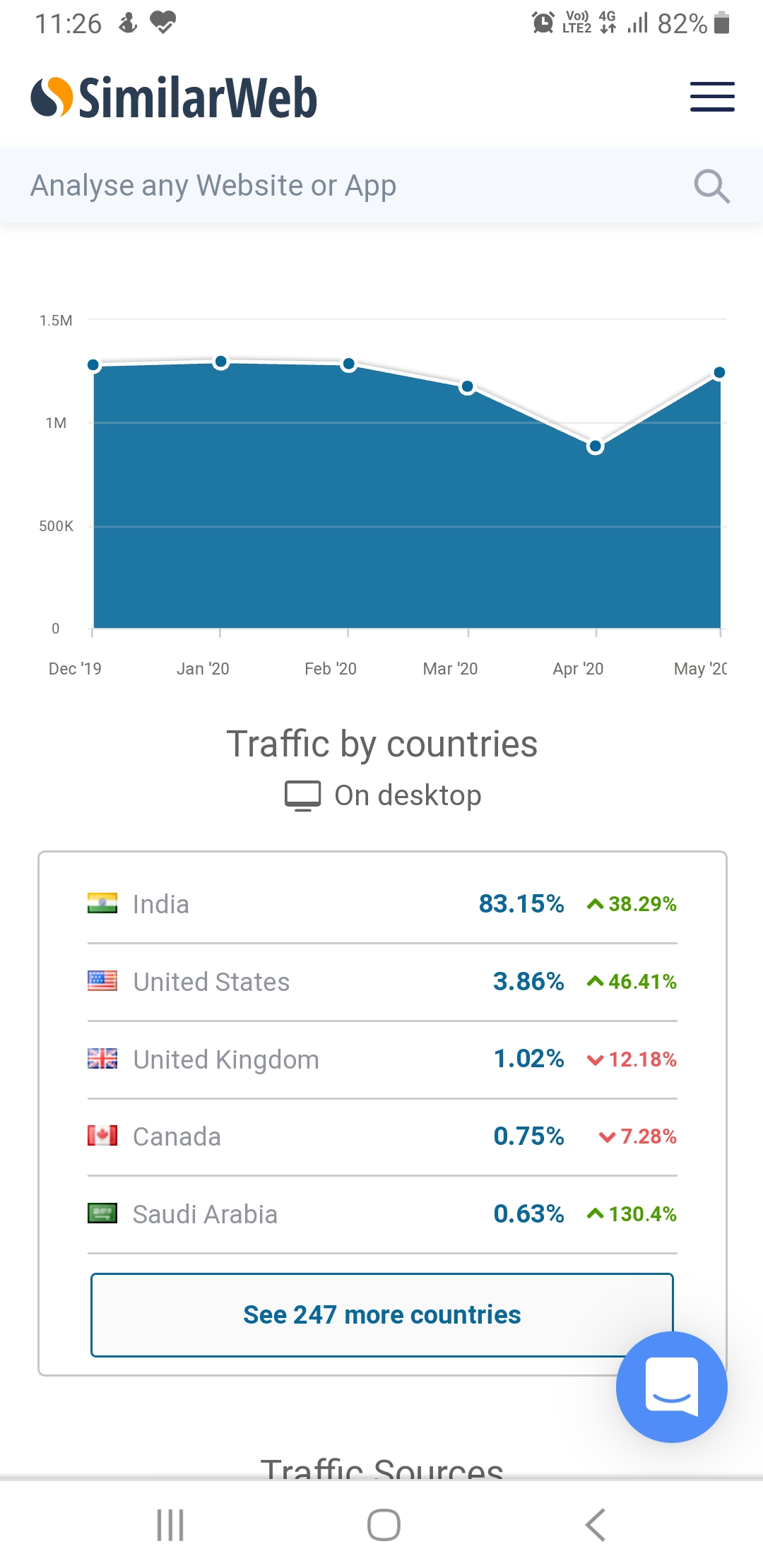

stabilisation for the recruiter site is not a good thing - the relevant statistic here is not rate of change but the absolute value

some more relevant context for purposes of gauging the scale - if you compare the traffic for the entire domain name with linkedin - naukri had ~13mn visits from India in May 2020, while linkedin had ~71mn visits in May 2020

agreed with your point that recruiter site traffic is more relevant in context of revenue - but we should look at absolute level of traffic for recruiter site rather than rate of change when comparing with previous periods

i was referring to the overall traffic to get a sense of scale and comparing it with linkedin

The management is under the impression that recovery of Zomato to pre-Covid levels will take a while. It is not clear on how WFH will effect the delivery business.

*

*