Can anybody give any tips on how to value a company like info edge with so many moving parts? Thanks.

2 Likes

Why is the PE showing as 7.68 today?

Does any one has a list of the startups where Infoedge has invested ( e.g. dotPe etc). It’d be great if there are bit more details also like % shareholding in that startup.

Unrealized market gains from Zomato listing is the reason for artificially low PE

Thank you. I calculated current PE based on its annual earnings. I got a value of ~45.

2 Likes

Insider buying is rare in infoedge case, given elevated valuations or inability to value it with so many parts ( though recent beatings does make it attractive for med term - again per individual risk appetite)

Invested

6 Likes

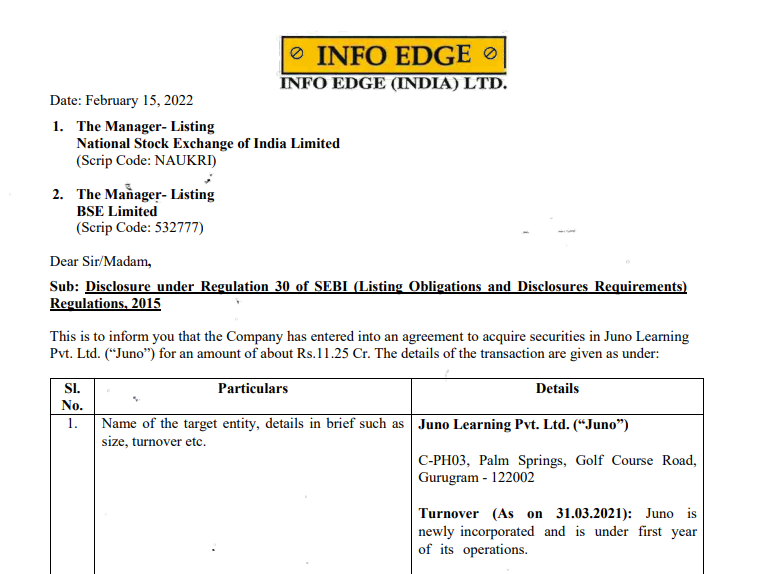

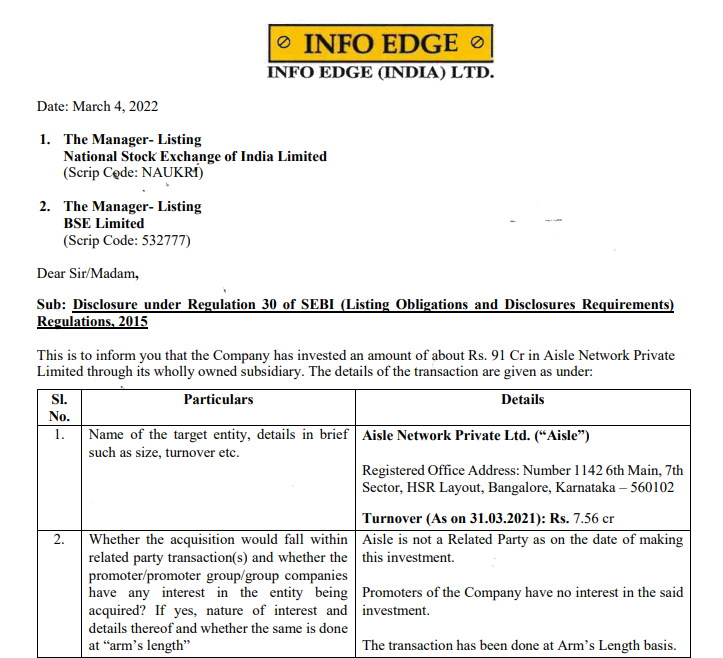

Info Edge has invested in yet another companies.

– Disclaimer

– Just started Tracking , seems like interesting Valuation

1 Like

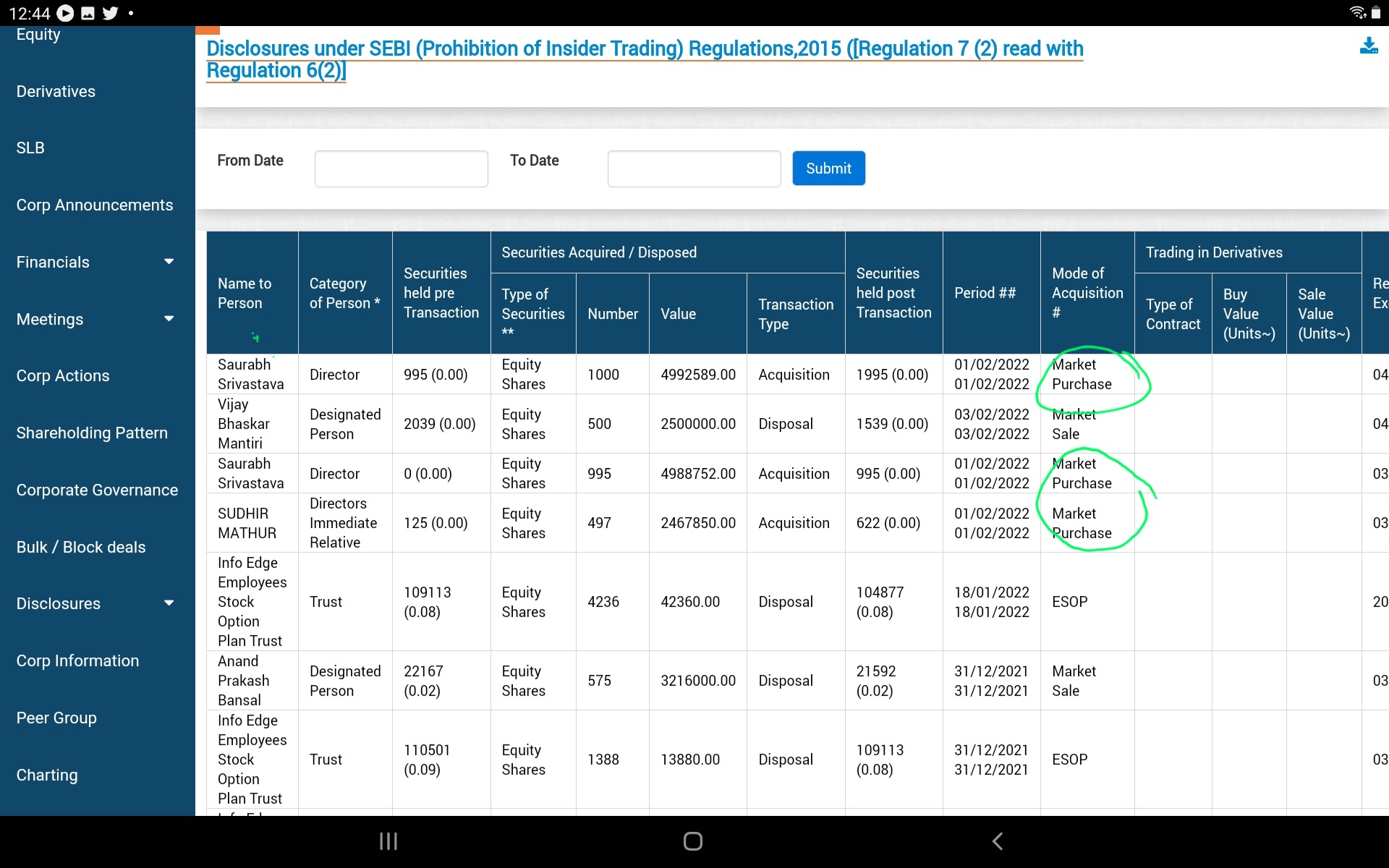

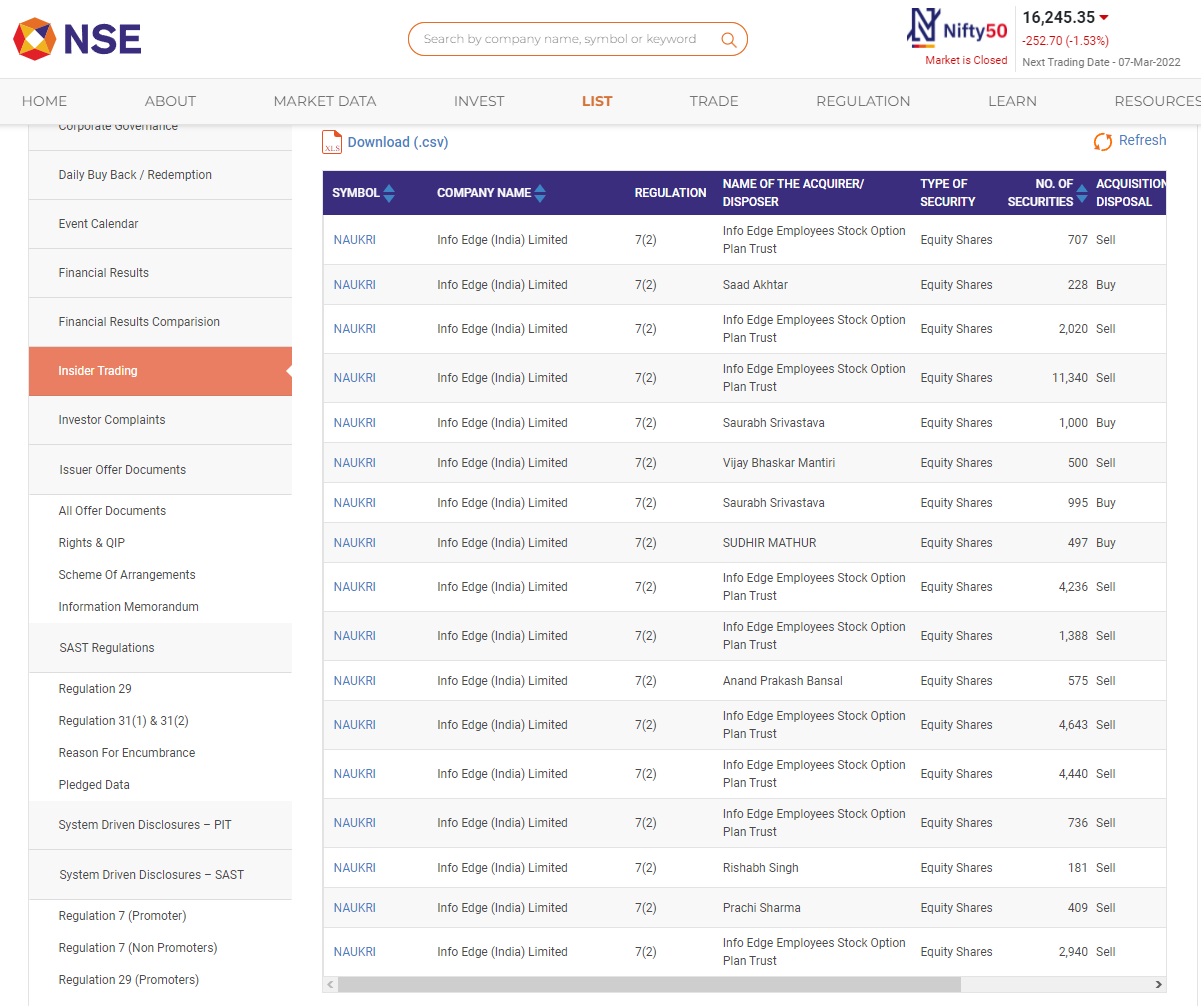

In last 3 months – quite a few insiders are selling.

– Disclaimer

– Just started Tracking , seems like interesting Valuation

Infusion commitment of 1300 cr in AIF, also sub funds structure within AIF, Sanjeev has been vocal about startup valuations froth in last year, as expected euphoria has settled with carnage in recently listed tech giants. With this valuations in secondary markets are more realistic as well, Infoedge Naukri being a cash generation machine and QIP funds, this seems pre cursor to readiness for deployment, stock has underperformed in last 6 months and has a good support 4300, bounced back few times from same. Currently under consolidation and expect a good Qtr on core biz, as well as key investments of Zomato and Policy bazaar making base after good thrashing.

1 Like

You will get the same at the end of companies investor presentation.

Given link below has been mentioned investments by Info Edge. Page no 53

http://www.infoedge.in/pdfs/info-edge-JAN22.pdf

Source of the presentation - Company Website

2 Likes

Though it has come up with good results for the last 2-3 quarters, because of its previously high valuations, the stock did not look attractive. Given that it has crashed 24% in the last one month alone and now sits at a 52 week low, do you guys think it is more reasonably valued now? For the long term (2-5 years), it does look like a 20% compounder, given its market share in the job portal market, investments in zomato and policy bazaar and a slew of other investments in start-ups which might bear fruit? Could someone point out what the downside is at current valuations, is there further scope of market cap erosion?

Note - Biased. Invested at 4500 levels and may add to average down further.

1 Like

Hey, I think if you want to quantity downside risk then you should answer or find the answer below questions (not all but containes few major one).

-

Their main business as strong Competition from LinkedIn - what is effect?

-

As now investor direct way to calculate the stake value of zomato and pb fintech so it will also affect it future returns

-

Other business performances like 99acres and shiksha and jeevansathi

Thanks!

CEO and CFO Message

“We are experiencing strong tailwinds in recruitment and real estate verticals. Post pandemic the gap between supply and demand of skills has increased globally. We expect this trend to continue in mid to long term and will create demand for platforms like naukri. ”

-Mr. Hitesh Oberoi, Managing Director and Chief Executive Officer, Info Edge (India) Ltd.

“Outstanding growth in billing, revenues, profitability and cash from operations. Naukri business has placed the company on a solid platform of consistent profitable growth. ”

- Mr. Chintan Thakkar, Whole Time Director and Chief Financial Officer, Info Edge (India) LtD

Key Highlights of Recruitment Solutions business for FY 2022

• Naukri business registered stellar growth in all key business matrices.

• Nearly 1 lakhs customer paid for Naukri subscription during the year.

• The billing from IT/ITES customers almost doubled during the year.

• Continued focus on new products launches (like Talent Pulse, Enterprise resdex, etc)

and value selling helped average billing per customer grow by 25%+

• Record growth in biling of newly acquired brands i.e iimjobs, hirist, Zwayam and Select.

Key Highlights for FY 2022

• EPS before considering exceptional items stood at Rs 35.78 per share , a YOY growth of ~62%.

• The Board declared dividend of Rs 13 per share ( Rs 8 per share interim and Rs 5 per share as final

dividend) for the year 2022.

• Exceptional gains (~9.5k Cr) in standalone financials booked during the year mainly comprises of marked to market gain on account of Zomato listing as on 23rd July’21.

• During the year , IEIL and its WOS invested Rs 278 Cr in strategic investments ( Aisle ,4B networks) , Rs 81 Cr in acquisitions ( Zwayam and Do Select) and Rs 301 Cr in financial investments.

• IEIL proposes to set up 3 AIF/ schemes with a target corpus of USD 325Mn. MacRitchie Investment Pte Limited - an indirect wholly owned subsidiary of Temasek Holding Pvt Limited and Info Edge India Limited, have committed to approximately 50% each of total corpus of the scheme.

• During the year, 2 investee companies of our financial portfolio, Zomato and Policy Bazaar got successfully listed on BSE and NSE.

11 Likes

I am happy with the info edge recent results. Not sure how long the revenues of info edge will sustain.

I work for an IT product company. All of colleagues who switched got opportunities from linked In. And not from naukri. We can see this trend switch slowly.

Second, linked In also stands as a marketing tool like fb, twitter handles. This gives them extra edge.

We need serious moves from info edge to sustain. Tech needs strong response. They must also look for new product avenues. Not just through acquisitions. They must write their own leveraging their existing know-hows.

They must move from AWS to their own datacenters to save up costs on operations. If someone gets into the conf call put these questions to the management.

7 Likes

Meanwhile the whole world is doing the opposite?

Public clouds like AWS, Azure, Google cloud are for small non tech customers and startups. It’s very costly to run servers with them in the longer run.

Tech cloud companies should go with their own datacenters. Running private cloud softwares such as openstack, docker, kubernetes for server management. Directly registering with IANA and geting their own ip block is way cheaper.

4 Likes

That’s not necessarily true. Different large firms have different use cases.

I have worked with Flipkart in the past where we had our own data centers. It’s cost-effective when you are a very large firm but you have to develop a lot of tools in-house and purchase 3rd party subscriptions for tools that you’d get by default with AWS etc. It saves you cost but it makes running the business tough and there’s pro and cons.

Large companies like netflix etc still use AWS despite having the best tech engineers only because they want to focus on the core business/tech and not managing infra. And you’ll very rarely see large companies moving away from cloud providers to their infra indicating it’s a better solution for their business

7 Likes

As a job seeker, I’d want my profile to be listed and active on all leading portals regardless of where i’ll get the offer from.

And as long as jobseekers’ profiles are there, recruiters would want to use the Naukri portal as well.

Key thing to track would be market share trend for Naukri vs Linkedin in jobs classifieds space.

Though I agree Linkedin’s ability to offer social networking for professionals is a plus vs Naukri & their job listings are more premium vs Naukri as well.

Disc.: Invested tracking quantity

i ran a Recruitment company from 2009 -2014 (specializing in Real Estate domain) For an IT Company the sourcing is easy from LinkedIn and it works well for them. IT guys are more tech savvy and they are more accessible on the Linkedin platform. We used to struggle to connect with people from the real estate construction domain, 70% of the workforce used to be on-site and most of them don’t access Linkedin that often or are that savvy. Linkedin has a lot of issues in India and they have not been as successful as USA or EU. Their pricing plan is more expensive than Naukri and the features offered are much lower. From an outsider’s perspective(job seeker), it may look like Linkedin the bucking the Trend but its actually not. Happy to give you more detailed pointers on the shortcoming of Linkedin, if you wish to know more

22 Likes

Notes from CNBC interview Hitesh Oberoi Discusses Info Edge's Q2FY23 Results & Outlook | Bazaar Corporate Radar | CNBC-TV18 - YouTube

- IT hiring is and will see less growth going forward as companies had over-hired to an extent.

- Non-IT hiring is on boom post covid as the economy opened up. Now at 35-40% of total Naukri revenue.

- Jeevansaathi revenue had a massive decline due to the ad-free model. Negative EBIDTA right now. Invested in a new dating app.

- 99acres doing decent right now. Didn’t share numbers.

- For venture investments obtaining small ticket series funding has no impact as of now in the VC landscape.

4 Likes