Inflame Appliances

The company is engaged in the manufacturing of glass gas stove/cooktops; hobs; and chimneys.

They are selling these under their own brand, Inflame, in the domestic and overseas markets. Within India, they cater to 18 states. Inflame has a network of 40+ distributors across India. In FY21, exports sales were around 1 Cr (out of total sales of 20 Cr). The major market in exports is African countries. But the prime focus of the management is domestic market rather than exports for the next 5 years.

They are also doing contract manufacturing of glass top LPG stove in 2/3/4 burners in premium ranges for brands such as Hindware and Avaante. (It is worth noting that Inflame is not exactly a contract manufacturer- Inflame designs the products itself and then presents these to the OEMs. However, since I do not know of the specific term used when a company does this, I have used the term contract manufacturing throughout this writeup.) They have been manufacturing different models of gas stoves for Hindware for about 4 years and currently contribute to over 80% of Hindware’s total demand:

They are also into contract manufacturing of chimneys within the country, which will cater to the requirements of other big brands. Clients in contract manufacturing of chimneys are Hindware, Sunflame etc. Seems like clients are very happy with Inflame’s quality. Inflame is the exclusive manufacturer of electrical chimneys, hobs and gas stoves for AKAI India. They are also in the pool of suppliers for chimneys for BSH Home Appliances (Bosch Siemens Home Appliances). The company can probably gain a higher wallet share of clients as well as do contract manufacturing for them in other products e.g. they extended the partnership with Hindware, where they were doing contract manufacturing of glass top LPG stove to now also start doing chimneys manufacturing.

They have recently been adding many clients like Wonderchef, Kaff Appliances (10,000 units of chimneys) etc:

Just to clarify here- in stoves they are doing both, own brand and contract; but in chimneys they are only doing contract manufacturing. In chimneys, no company does production of more than 3 lakh units per annum. By doing contract manufacturing rather than their own brands in chimneys, they do not have such a ceiling on the sales and they are not restricting their potential market share in the competitive, fragmented market (they can do contract manufacturing for all brands).

It is interesting to note that these companies currently import all the chimneys from the overseas market. This way, it is also a play on import substitution:

Not only are they acting as import substitution for clients, but they themselves are also substituting with domestic suppliers for the components they are importing.

They have done massive reduction in import dependence from China, from 50-60% to 2-3%:

They are expanding their product range and have started manufacturing electrical chimneys, glass cooktops, glass hobs and cooking ranges to increase presence in the cooking appliances market of the country.

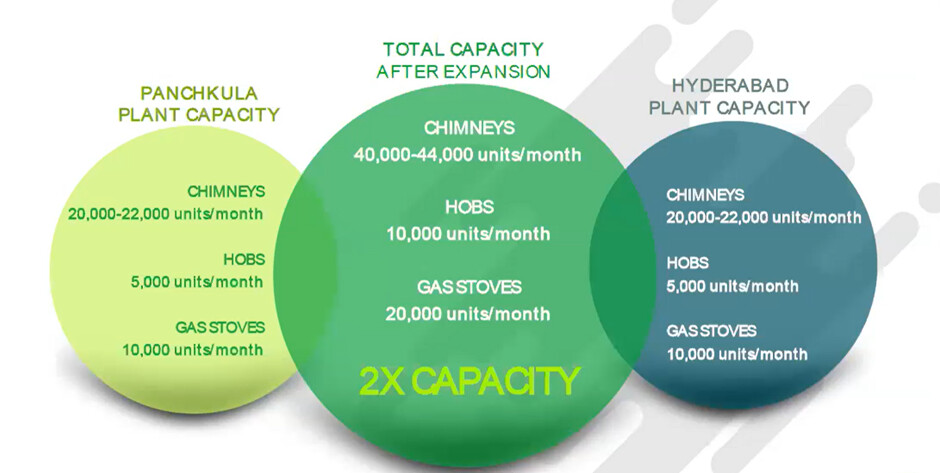

The latest currently installed capacity in units per month is 10,000 for Stoves; 5,000 for Hobs; and 20,000 to 22,000 for Cooker Hoods (Chimneys). Average realisations in chimneys are in the range of Rs 4000 to Rs 4500 per unit; for hobs it is Rs 5500 to Rs 5700 per unit; for gas stoves it is Rs 1600 to Rs 1700 per unit. Using the lower bound for each, monthly revenue at peak utilisation for stoves can be Rs 1.6 Cr; for hobs can be Rs 2.7 Cr; for chimneys can be Rs 8 Cr. Total monthly revenue can be 12.3 Cr (1.6+2.7+8). Hence annual revenue from existing capacities can be Rs 147 Cr. TTM sales are Rs 28 Cr. Latest utilisation was 50% each for gas stoves and chimneys; and around 15% for hobs. They are expecting to reach peak utilisation between March and June 2022. Management has said that at peak utilisation of current existing capacities, EBITDA margins can be 18-25%.

They are already under the process to scale up the current production capacities via large capex:

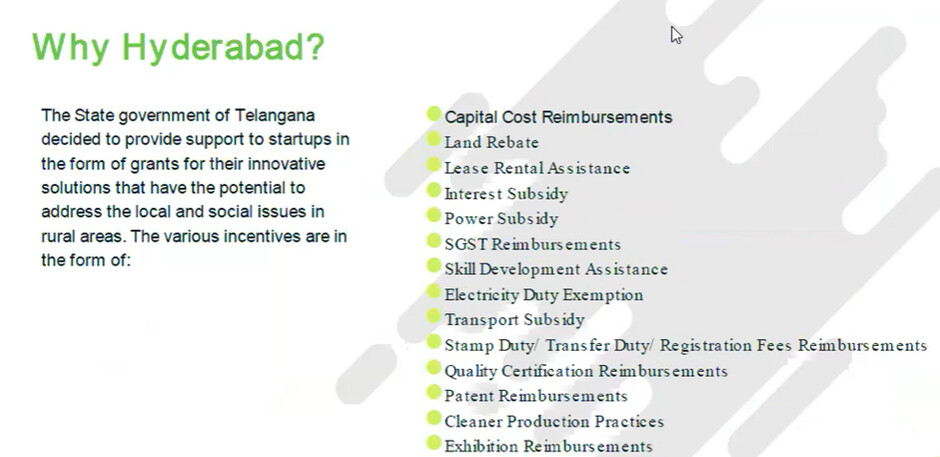

They are planning to set up a new plant in Hyderabad with installed capacity in units per month is 10,000 for Stoves; 5,000 for Hobs; and 20,000 to 22,000 for Cooker Hoods (Chimneys), i.e., capacity will double post Hyderabad plant:

The reason they have chosen Hyderabad is because of various subsidies offered by the state government:

They have also got 2 acres of land for new capex at a subsidized price:

They are expecting this to be completed within next 6 months:

Seems clear that chimneys would be a big driver of growth going forward.

The key raw materials for the company are various types of Brass Burner, Brass gas Valve, MS Pipe and Aluminium Mixing Tube, Toughened Glass, Pan Support Rings and Various Rubber Components. They are backwards integrated into the making of sheet metal components for captive consumption. Also, they are increasing/extending backward integration and a modern glass toughening plant is being added to cater to the requirements of toughened glass for use in glass cooktops and cooker hoods:

There has been raw material price inflation but they are able to pass on this in the form of price hikes with a lag of 30 to 50 days. More than RM prices, the bigger challenge is around RM availability and backward integration is expected to help overcome this.

They are working on multiple new product launches and they are looking to increase their presence in the cooking appliances market. One such product which they expect to launch in near future is dishwashers (where they expect to price at around Rs 18000 to Rs 22000 per unit). Another potential product they have identified is OTG- oven toaster grillers. Management has clearly explained that the new products will be only those which are import substitutes. These could potentially accelerate revenue growth.

During the recent years, the Company had bought 12175 sq. meters of land on NH73, near Panchkula, Haryana for setting up a new facility where approximately 4500 sq. meters (around 45000 sq. feet) of facilities are already constructed. Another 18000 sq. feet is under construction. The Company shifted all its operations from an earlier facility at Baddi, Himachal Pradesh to this new facility in a phased manner during FY21.

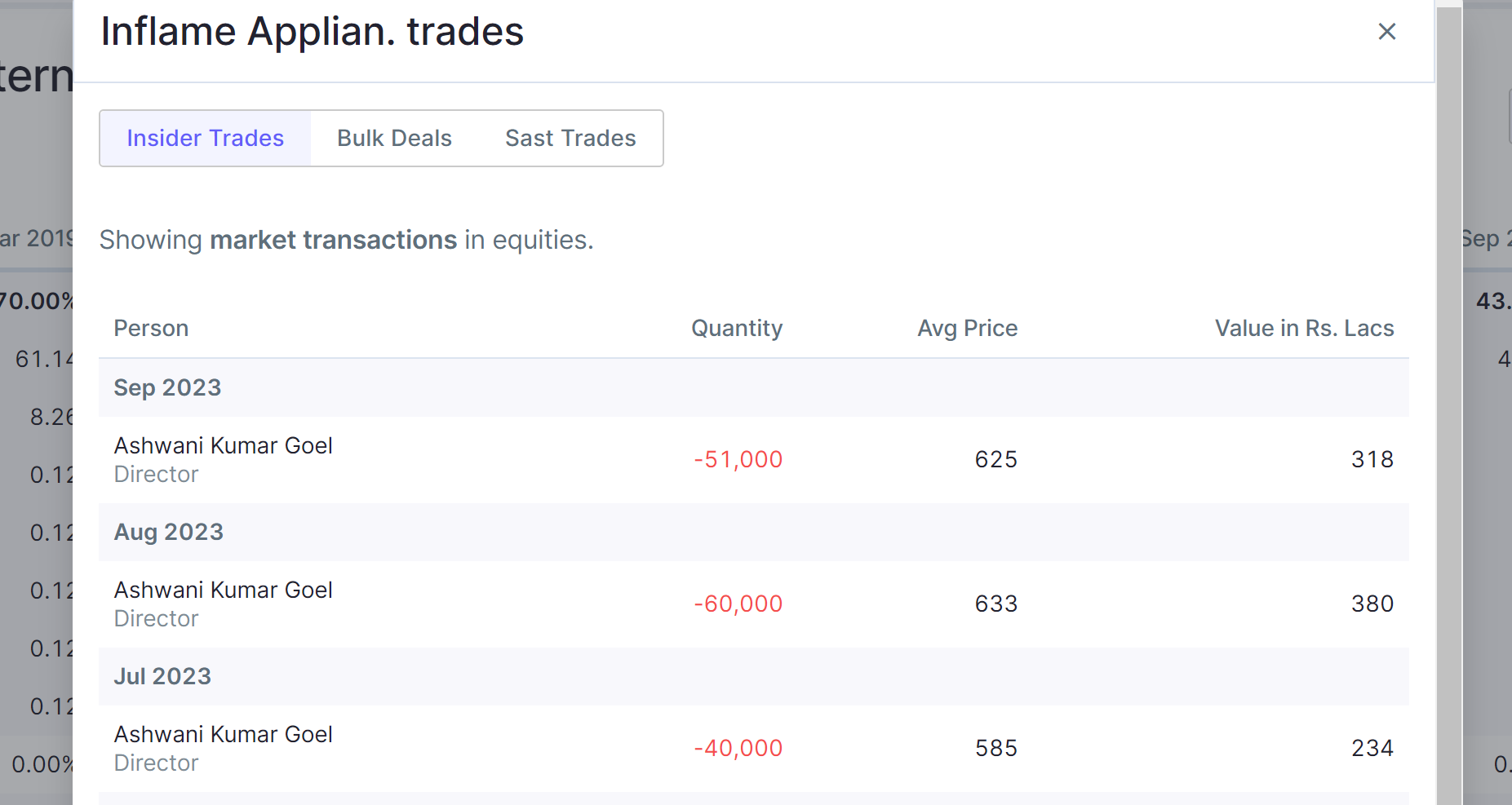

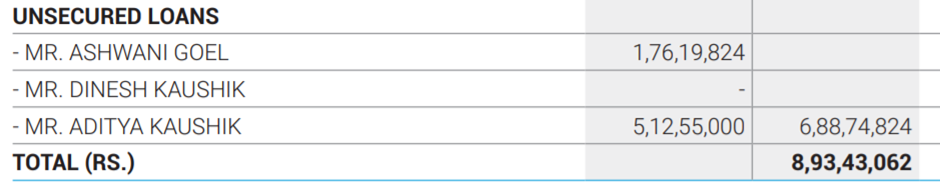

On the corporate governance side (positive), there is an unsecured loan of 5.13 Cr taken by the company from Mr Aditya Kaushik (CMD) and 1.76 Cr from Mr Ashwani Goel (Whole-Time Director)

Importantly, these are interest-free:

As of FY21, total long-term borrowings were 8.9 Cr and out of that 6.88 is unsecured, interest-free from directors.

They recently did preferential issue and some portion of the capital raised was used in debt reduction.

I heard that in the last few years the management even went to Turkey and China to learn the art of the trade. In their investor meeting, the management shared their vision of gaining 35-40% market share by 2026. Their present market share is around 5%. They aspire to produce 1 lakh units of chimneys per month. This would mean Rs 40 Cr monthly revenue from chimneys alone. They have given a guidance for 50 to 70% CAGR in revenue over next 5 to 7 years.

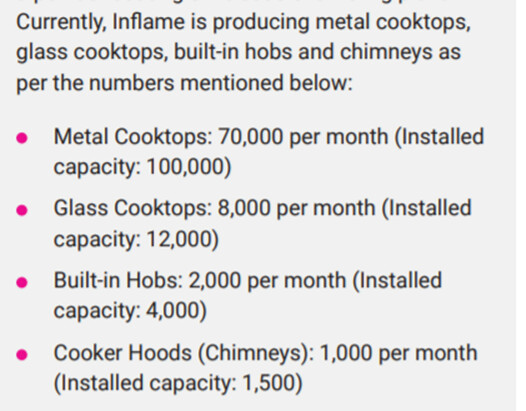

There have been some big changes since the publishing of FY21 AR to now. AR mentioned this production capacity:

However, they have discontinued metal cooktops completely and scaled up chimneys massively. The latest currently installed capacity in units per month is 10,000 for Stoves (same as glass cooktops); 5,000 for Hobs; and 20,000 to 22,000 for Cooker Hoods (Chimneys).

Also, earlier, under Pradhan Mantri Ujjwala Yojana, the company had marketing agreements with Oil Marketing Companies (HPCL, BPCL and IOCL) to market, sell, distribute and promote LPG Stoves to domestic consumers using their distribution channel. However, they have now discontinued this.

The major risks are intense competition and high debt. One key disconfirming evidence is that for gas stoves they only have 1 customer, hence there is big customer concentration risk. They are planning to add 2-3 more customers for gas stoves soon.

I personally think this is one scenario where it is more about management and narrative. If we just look at RoCE, P&L, margins we will get a false picture because it is currently making losses. Because of the accumulated losses, reserves (hence book value) are very low hence price to book looks very high and debt to equity looks very high. There is no P/E since it is making losses.

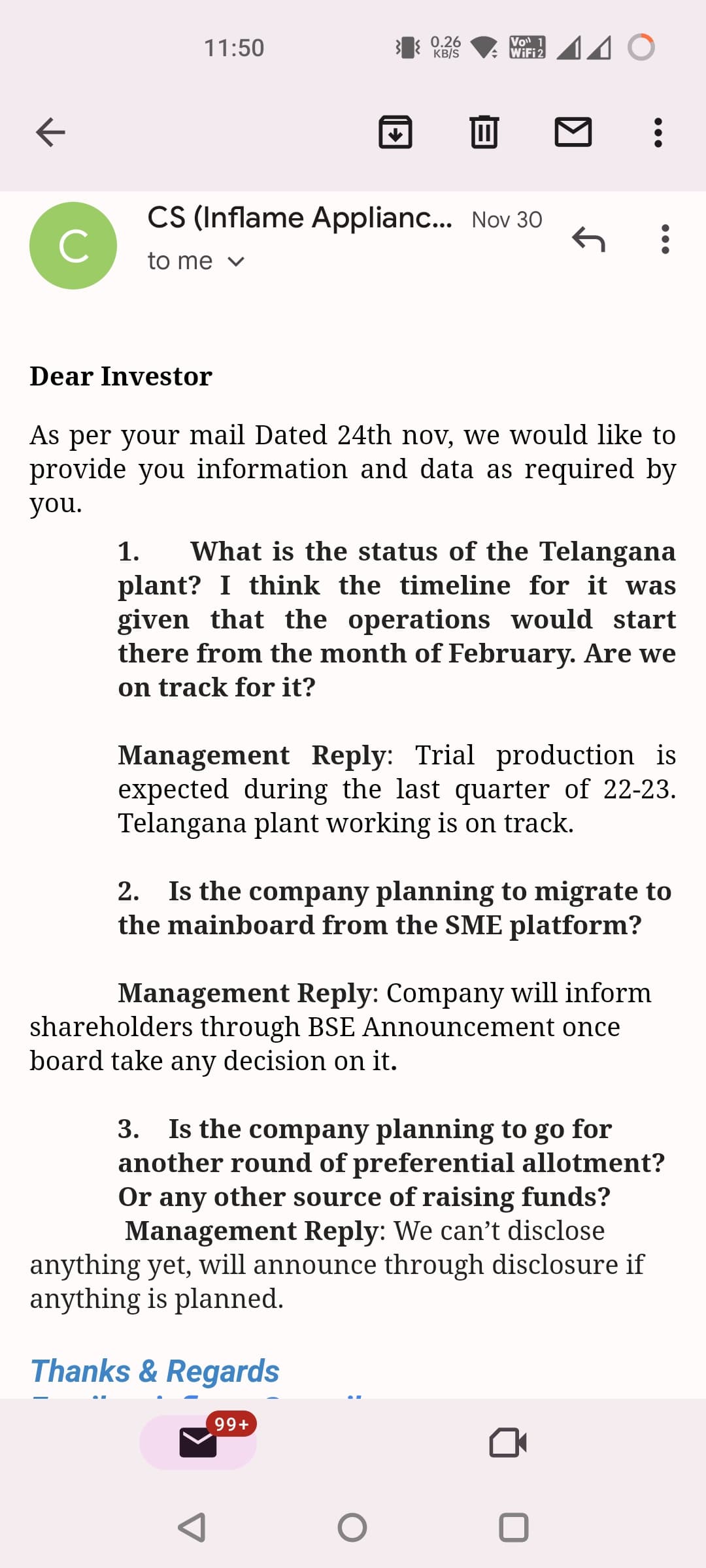

The company’s recent investor meeting is available at Passcode Required - Zoom and the passcode is 5Y^.fLq6 (note- this is given on company website IR page and hence is in public domain)

Disclosure: I have a tracking position