Management is saying that the import of Chinese products will be very difficult after compulsory BIS certification.

My friend is an appliance manufacturer with BIS certificate, he says that it’s just a standard that they have to follow and products meeting the BIS standard can still be imported and white labelled.

Does anyone else have a view on this ?

1 Like

GOI implemented BIS in footware also. How successful are they in curtailing the Chinese imports. One of the way GOI can do is delaying the BIS certification to Chinese companies when they apply. Any views please

1 Like

Any news on this counter…One of the director is selling his shares on a daily basis this month

Any idea, what is the peak revenue potential from both panchkula and Hyderabad facilities?

Any notes from AGM 2025 ? It would be interesting to get details on the ramp up of the hyderabad facility

2 Likes

I have been tracking this since last 3-4 years, could not able enter the script based on high valuation and management commentary/guidance is never fulfilled so far.

As this quarter results are little impressive, i have attended the conference call. Ramping up of production at Hyd facility is under progress, they are planning a 10 Cr capex at 1st facility, which will start production from Q1FY27.

There are some good order in pipe line which will start execution from Q4/Q1.

Management want to grow other products revenue in FY26 Onwards, share of other products would be ~40% in 2-3 years from the existing 10%.

New products in pipe line will be announced in December. As the contribution from other products like built in appliance, dish washer, wine chillers (which have higher ASP) will boost the revenues going forward.

Overall commentary is very +ve and management assured the growth momentum just begins, which is been in que since last 2-3 years.

3 Likes

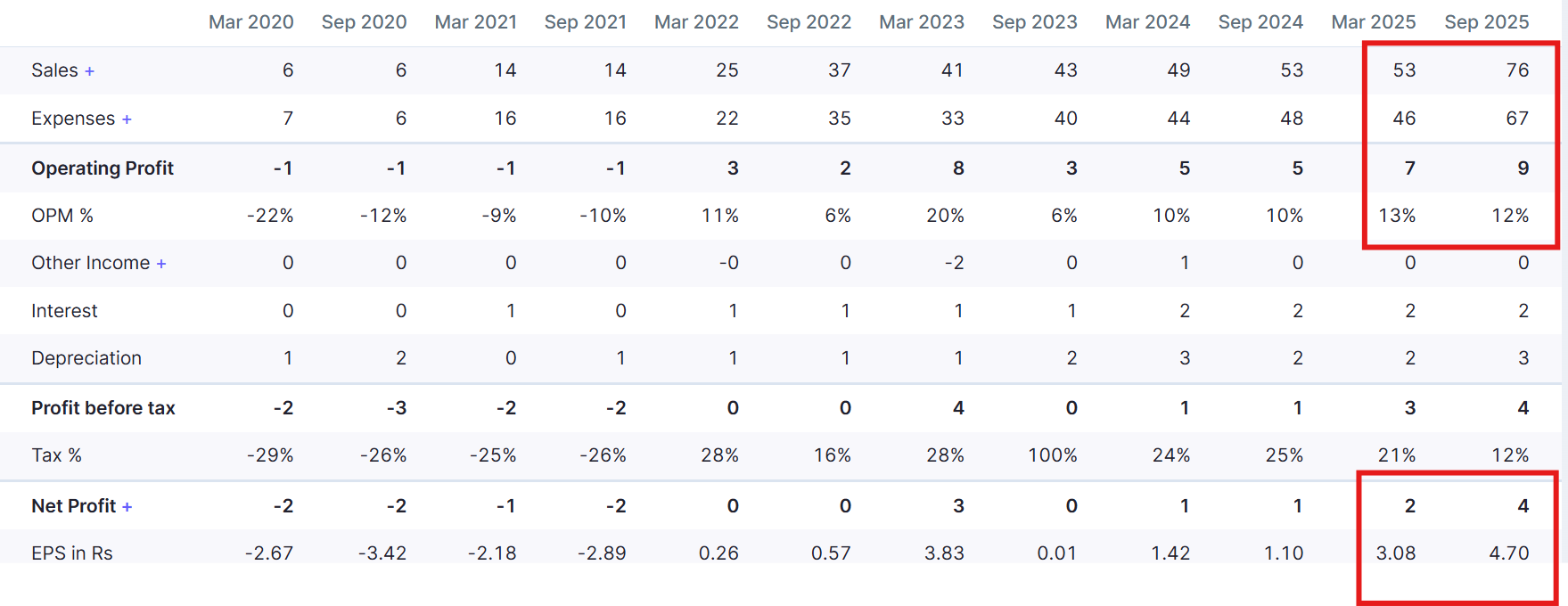

Company came with a very decent set of results for H126 and held it’s maiden con. call. Here are some points from the call.

- H1 Numbers : Sales Volume : up 27%, Topline up 42%, EBITDA up 64.5%, PAT up 333%

- Capacity, Utilization : Panchkula and Hyderbad Facility, each have capacity of 3L chimney’s, 1.5L gas stoves and 60k Hobs. Panchkula Facility is at near 100% utilization and Hyderabad facility near 50% utilization. 80-90% is the max possible utilization rate.

- Capex : Location - Panchkula, Cost - 10 Cr. , Funded - by debt. Construction Started). To be operational by April’26. Purpose - Adds space for 15k/month chimney capacity and space for finished goods.

- Margins: Gross Margin has stabilized around 30%. EBITDA margins will slowly inch up with higher volumes. No explicit guidance. Manpower cost came down from 14% to 10-11% this year.

- Customers: Big Indian brands like Havells, Crompton, IFB, Wonderchef, KAFF, Livpure, Hindware, Sunflame, V-Guard.

- Market Size : 1.6 Million (?) They are mostly either manufactured by 3 major players in India for themselves (like Haier) or imported from China. Right now after BIS, it’s the 3 players + Inflame + plus some imports CKD units (which is on it’s way down).

- Growth Drivers and Guidance : Cost competitiveness. Selling at 98 vs what costs 100 when bought from Chinese imports. 40-50% Topline growth for FY26,27. Momentum of H1 will be sustained in H2 or even better. H2 may see a volume of 1.7-1.8L vs 1.34L in H1 implying a 25% QoQ growth.

- New Product Launches : Company plans to get into additional product lines while chimneys will continue to bread and butter in foreseeable future. Idea is to get 35-40% from other product lines like dishwasher, built-in refrigerator, wine chiller etc. etc. by FY28.

- valuation : Seems like it can do 10-13 kind of eps for the year and available at 20-25x types multiple for current year. Not very cheap, not very expensive either ?

- Other Interesting Titbits on overall business environment: :

- IFB seems to have developed some components for Inflame, which they earlier used to import from China. In turn Inflame seem to be working on few products of IFB, like dishwasher.

- BIS approval need has been a gamechanger for indigenization of this industry ? Promoting local production. Some bigger chinese players like Haier are producing in India but the smaller Chinese units which used to export to India seems to have found it difficult to cope. Some players might be buying CKD units but there are lot of parts which has to be India for one reason or other like glass etc…So buying Chinese CKD and assembling in India is on the way down and may become completely unviable in 6 months.

- Chimney’s are long warranty products (8-10 yrs). Even while Chinese supply was rampant in India, Inflame’s customers were testing waters by giving it small orders and now they have confidence to give large orders.

2 Likes

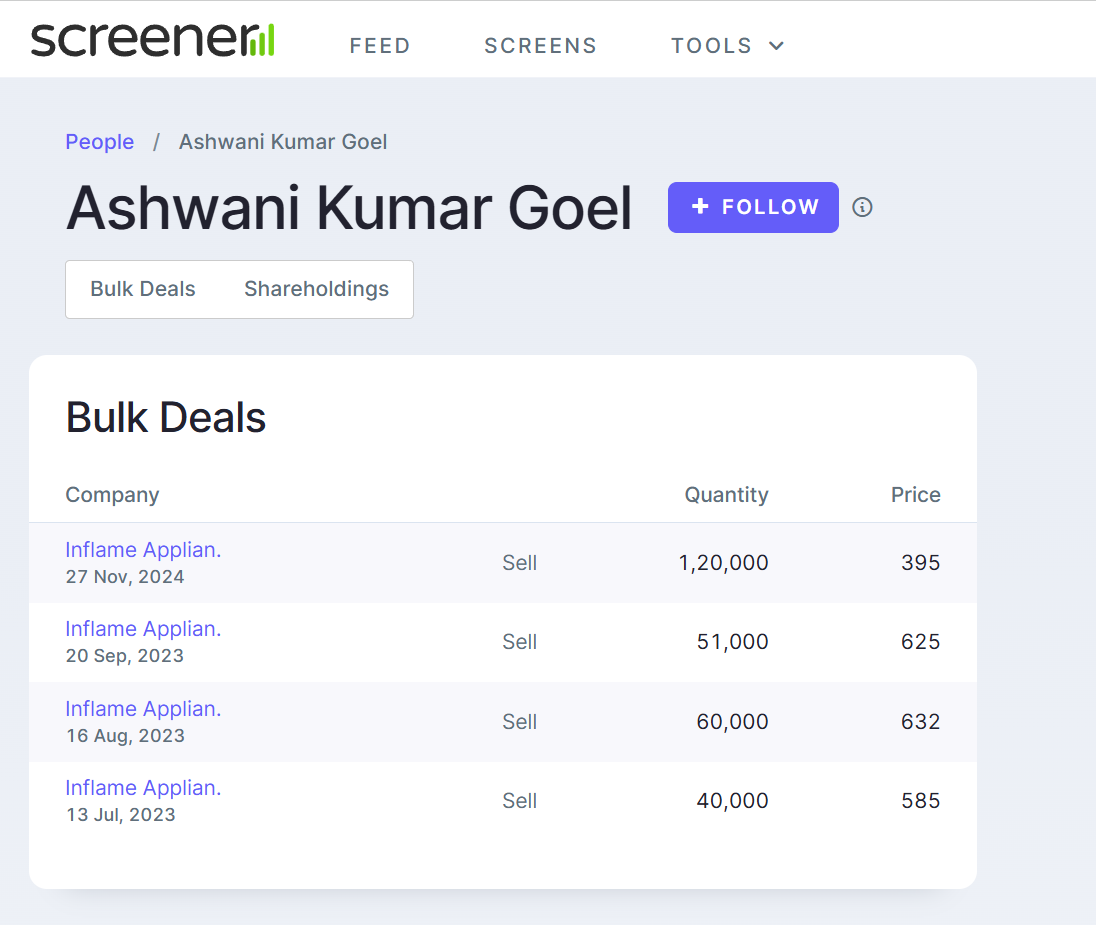

Any News or rumors or update on the reason of exit of one of the Director-Ashwani kumar Goel. Why he has sold all his shares in the open market. He is having any plan to leave the company or has he sold for his personal reasons? Anybody any news or even rumors in the gossip column?

Thanks in advance!

Maybe just a smart investor :)

This Q was raised in the call, and mgmt. said, he is free to do so in his independent capacity and he is not part of promoter group. Which is fair i guess ?

he is not part of promoter group: it is fair technically but he is sitting in a position in the company where he should be classified as promoter because his action is equivalent to “Insider Trading.” Just imagine I am a CEO in such a small company I will be having fair idea when my business is going to grow according to market expectation or not. His actions would have been only justified, “if he would have resigned from the company and joined any competitor firm.”

Am confused. Are you talking from a legal angle and saying what he did is wrong as per regulations ? Or just trying to evaluate it’s moral and signal value for the company’s future ? If it’s second, he decided to sell. It is what it is.

Mr. Ashwini Goel is an industry veteran, spent 30 yrs in JSW and 36 yrs career overall. Joined Inflame BoD in 2019 and IMHO there is not much to read into this unless you have a point on legal angle ?

Dear Maybe you are invested, so you are not liking the negative. But, you tell me one thing: Do you think: He has purchased those shares with his money or most probably got as part of ESOP? It is not moral angle that I am trying to bring it here : I am telling just one thing that he has done insider trading. Your opinion of him being “Maybe just a smart investor” is quite questionable because he is not a investor but insider.

You reserve the right to hold your opinion and so do I. I am invested so maybe I am biased.

Avoid making personal remarks. Stick to the topic.

Why try to guess this? You can find it out from the filings. I think there has never been any ESOPs in Inflame. So no point questioning the source of money.

If you are speaking from legal angle, then it’s a serious accusation and I hope you are fully aware of what you are alleging a person of, in a public forum. Good Luck.

I am fine with an opinion, but not a legal wrong doing accusations on a public forum. So, I hope, you have the legal knowledge to back it with facts. Friendly advise, if you are not sure of what you are accusing of, you may consider changing it.

I was just checking SEBI (Prohibition of Insider Trading) Regulations, 2015 and its a 77 page document full of legalities. Good for you, if you know what you are talking about. People with deeper knowledge of the subject may comment.

Thanks for sharing your perspective. I think there may have been a misunderstanding in how my earlier message came across. I’m not accusing anyone of wrongdoing, nor am I making any legal claims. My intention was only to understand the situation better and discuss it from an investor’s point of view—nothing more.

I fully agree that legal allegations should not be made lightly, especially on a public forum. That’s why I’m being careful with the wording. My reference to SEBI regulations was only to understand the framework, not to assert that any violation has occurred.

Regarding the director’s share sale, I was simply pointing out that large sales by senior management often attract attention and naturally raise questions among investors. That’s a general observation, not specific to this company. I’m just trying to gather perspectives and scuttlebutt information, as many of us do.

SEBI prohibits any insider—including directors—from trading while in possession of Unpublished Price Sensitive Information (UPSI). UPSI refers to information that isn’t publicly available and could materially impact the share price if disclosed. Directors are treated as “connected persons” under the PIT framework, so they can trade only when they are not in possession of UPSI and when they follow the company’s internal procedures such as pre-clearance and trading-window guidelines.

My point here is simply that it’s understandable for investors to be cautious when a senior director sells a large portion of their holdings, because such individuals generally have access to UPSI. At the same time, I fully recognize that a sale on its own does not mean insider trading or wrongdoing under SEBI rules.

I’m not making any allegation at all—just trying to understand if anyone has come across anything through their own scuttlebutt or observations. Please don’t take this personally; I’m only trying to understand the situation better, not question anyone’s investment or views.

Somebody asked this question in the call, CEO clarified that Director can sell the shares at his own discretion based on necessity and promoters has any intention to decrease the holding.

However, irrespective of his exit business performed well in the H1.

1 Like