Looks cheap as compared to other nbfcs. Only 0.6 times BV

IndoStar Capital Finance Limited

FY23 Performance (Consolidated) in Key Focus Areas:

PAT of ₹ 225.2 crore in FY23 vs. loss of 736.5 crore in FY22

FY23 Gross Stage 3 improved to 6.8% vs. 13.6% in FY22

FY23 Retail AUM has risen to 85% vs. 84% in FY22 with a focus on used Commercial Vehicle

and Affordable Housing Finance business

Q4 FY23 Highlights:

AUM at ₹ 7,813 crore up 2% from ₹ 7,669 crore in Q3 FY23

Disbursements ₹ 898 crore up 72% from ₹ 522 crore in Q3 FY23

Incremental funding of ₹ 908 crore raised during Q4 FY23

Continued Profitability – Q4 FY23 PAT at ₹ 76 crore

Debt/Equity Ratio sustained at 1.8X times

Gross Collections of ₹ 918 crores

Gross Collection efficiency of 126%

Gross Stage 3 assets are at 6.8% for Q4 FY23

Net Stage 3 assets are at 3.2% for Q4 FY23

Retail AUM ~ ₹ 6,613 crore; ~ 85% of AUM

Strong Capital Adequacy at 31.5%, on a standalone basis

Other Key Takeaways:

AUM stands at ₹ 7,813 crore

The company is focused on growing its retail business.

As mentioned in the last con call, management is focused on the higher-yielding used commercial vehicles segment and increasingly on used light CVs in tier 2 and tier-3 towns. (CV Business has demonstrated a high disbursement growth of an average of 48% CQGR, from ~ ₹ 203

crore in Q1 FY23 to ~ ₹ 657 crore in Q4 FY23)

The company is also leveraging technology-enabled systems to drive higher process adherence,

improve collection efficiencies, credit underwriting, and sales productivity.

CARE removes ‘Negative Watch’ on Rating and assigned a ‘Stable’ Outlook

As the company accelerates its disbursement engine, it aims to raise a significant amount of debt and bring its current low debt-to-equity ratio position closer to industry norms. This implies that they will disburse more in the coming quarters as the platform is set and legacy issues are resolved.

In the recently concluded OFS, IndoStar Capital and Everstone Capital Partners II LLC diluted their stakes, but Brookfield did not. This reflects their support and confidence in the business.

IndoStar Home Finance Private Limited (“IHFPL”)

IHFPL delivered a PAT of ₹ 37.8 crore in FY23, up 10.1% from ₹ 34.3 crore in FY22. The AUM in IHFPL stands at ₹ 1,623 crore, up 15.4% from ₹ 1,460 crore in Q4 FY22.

company is engaged in preliminary discussions to explore potential strategic options including a potential combination and listing of the retail mortgage portfolio of JM Financial and the home finance business of Indostar Home Finance Private Limited including other mortgage-backed businesses of Indostar.

Indostar q4 results.pdf (1.0 MB)

Disclosure: Invested

1 Like

Indostar Q4 conference call highlights:

Company to focus on used commercial vehicles and HFC. More focus will be on cv where yields are better at 18% and 90 to 95 % disbursements will be done on the used cv front.

Processes and technology are in place. Will grow from a low base and maintain better than Industry growth

The reversal was done for unvested ESOPS that were charged to P&L last year

Collection against the pool assigned to Arc has been substantial

For Hfc, discussions and due diligence are ongoing with JM Financial.

To avoid errors we have strengthened control, reviewed policies, and upgraded our technology system right from loan origination, credit appraisal disbursal, and as well as collection processes. New controls are in place and new underwriting is taking place and will help to grow the loan book.

The cost of funds in q4 was at 10.5% and is at its peak. Going forward cost of funds will come down gradually.

Will disburse around 4000 crs for cv and 1100 crs for hfc this year.

Expect opex at 4% of aum and credit cost will be at 1.5 to 2% (without any reversals)

ROA should be at 1.5% to 2% for FY24 and FY25 ROA to be at 2 to 2.5%

To improve ROA, Will focus on high-yielding CVs. Will look to reduce opex and maintain branch profitability.

Loan book guidance for FY 25 - Expect to have a book of 9000 crores for cv and 4000 crs for HFC. The rest will be SMEs and Corporate as they will see degrowth.

The market of used CVs is at 1.7 lakh crs 40% organized and 60% unorganized. Will tap unorganized, unorganized play at a higher rate. Our rates are much lower with better services.

Customers are retail and first-time users. Typically the Loan tenure is at 3 to 3.5 years for CVs.

Hfc to focus on retail in tier 3 and tier 4 cities, that are first-time home builders. Avg ticket size is at 8.9 lakhs. Strong foundation in the South. 5.5% to 6% spread.

Please add if I have missed anything.

Disclosure same as above.

2 Likes

Anyone have access to motilal oswal report released yesterday on indostar

File_1685521787313.pdf (983.9 KB)

^ Motilal Oswal report

2 Likes

Revision of Credit Rating of IndoStar Capital Finance Limited by CRISIL.

Report attached.

1 Like

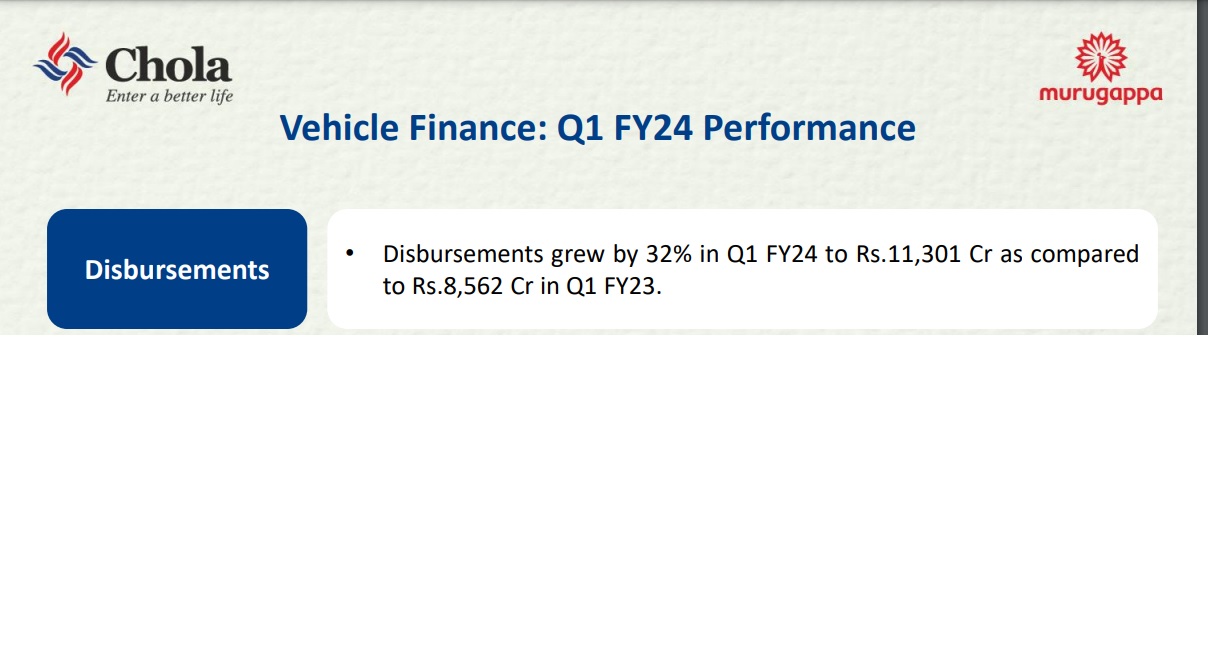

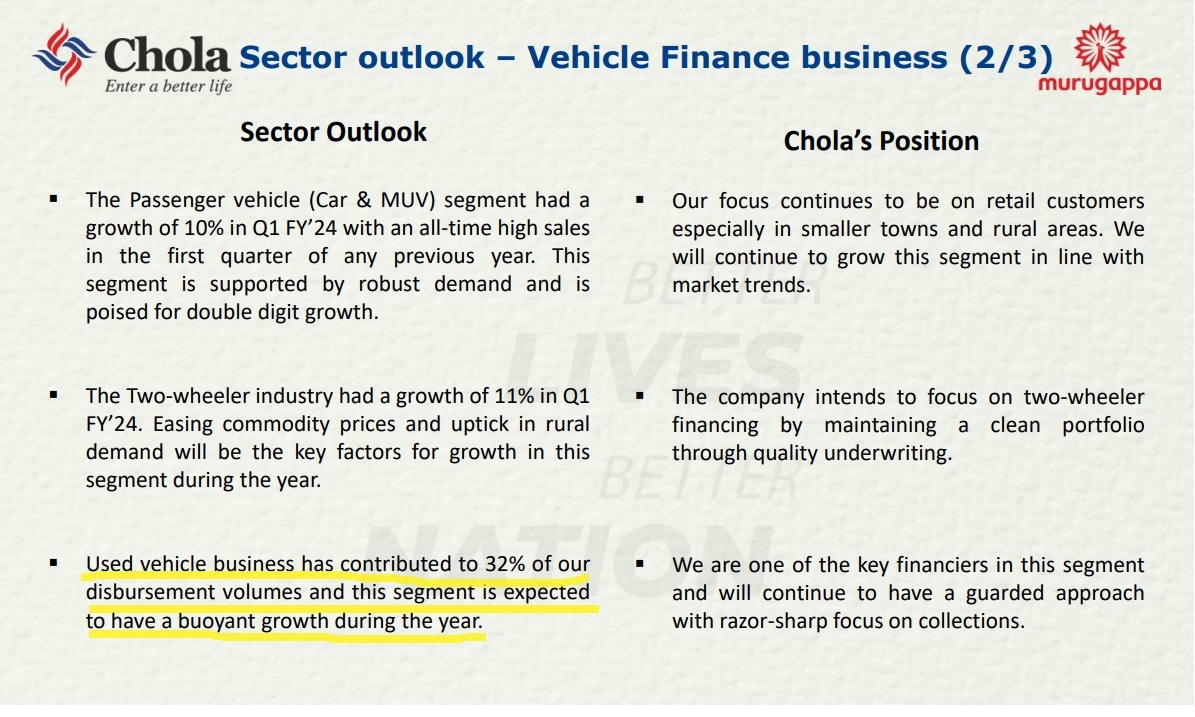

Used LCV/CV business comprises a major chunk of Indostar’s vehicle loan business and as per the Investor presentation for Q1 FY24 by Cholamandalam, who competes with Indostar in the used vehicle business, expects buoyant growth in FY24.

Used vehicles segment has contributed 32% disbursement volume out of the total disbursements of 11,301 crs under Vehicle finance

Disclosure : Invested

1 Like

Results look bad Prima facie but after excluding esop costs, results are v good

2 Likes

Indostar Q1 FY24 result highlights from investor presentation:

-

AUM : 8062 crs (AUM break up : CV - 3928, HFC - 1741, SME - 1177, Corporate lending - 1190)

-

Disbursements for – Q1FY24 : 1,116 crs. For the Entire FY23 the Disbursements were at 2,099 crs

-

Disbursement break up : CV - 755 crs, HFC - 190 crs and Corpotare lending - 171 crs

-

Consolidated Gross Stage 3 : 6.6% and Net Stage 3 : 3.1%

-

CRAR : 34.4%

-

PAT for Q1FY24 : 38.9 crs (Q4FY23 and FY23 includes reversal of ₹ 50.5 crore & ₹ 44.2 crore on account of cancellation of unvested ESOPs)

-

YOY NIMs : 6.5 % vs 5.5%

-

Collection efficiency at 138.8%

-

Capital Adequacy - 34% . Net worth - 3151 crs. Gearing ratio - 1.9x

Management is walking the talk as discussed on the last conference call, the disbursement engine is picking up and major chunk of disbursement is towards retail (CV and HFC). SME and corporate lending is showing de-growth. Disbursements are picking up and Ratings upgrade will reduce the cost of funds going forward. According to me this PAT figure should be the baseline number.

Disclosure : Invested

1 Like

Anyone who attended concall, why they are reducing sme book when almost all nbfc and banks are growing SME BOOK

Hi. Indostar main focus is on CV book. They have been a failure is sme with huge NPA. SME financing is not cup of tea for everyone. Also be little careful with these small NBFCs. Their credit process, teams is not very strong due to which NPA was v high as compared to peers. The only comfort in Indostar is Brookfield as promoter. One should watch the asset quality and then take a position.

1 Like

Indostar Capital Q1 FY24 Earnings Conference call highlights:

-

Focused on used commercial vehicle lending and affordable housing sector, and we have

kept our focus unwavered. -

Focus remains on the Tier 3 and Tier 4 market, which contributes to the bulk of our volumes.

-

QoQ net interest margin expanded by about 50 basis points to reach about 6.5%

-

Our profit after tax for the quarter was at about INR39 crores, an increase of 50% compared to

the adjusted PAT of the previous quarter, which was at about INR26 crores. -

Used CV is not seeing any margin compression where Indostar operates (Tier 3 and 4 market), demand is pretty good and do not see margin squeeze in the immediate quarter or in the immediate future.

-

Operating only up to the 12-year-old vehicle, scrappage policy comes, which will be a positive momentum to the industry, for the used vehicle sale will go further faster. We are very much protected against whatever is going to happen.

-

Onset of monsoon slows down new CV sales due to certain aspects. But we didn’t see any slowdown in the used commercial vehicle industry.

-

Management is comfortable leveraging to 4x in terms of the debt versus equity in Five quarters, six quarters. (Currently at 1.9x, 2x leverage)

-

We have now only recently started approaching the banks, which we had stayed away from for almost a year. It’s only after the Q4 results that we started going to the banks.

-

Opex will go up but in a muted manner as revenue goes up and reduction in the interest cost will improve ROA. Leverage increase will improve ROE. (Down the line will be comfortable with 2.5 - 3% ROA and ROE 14 -15%)

-

Targeting AUM of 13000 crs by FY25 (Currently at 8062 crs)

-

CVs are very short-seller book - 30, 39-month average.

-

Yields are improving as we are not doing deals below a particular rate. The old book is at a lower rate is running off, and the new book is getting

added at a much higher rate. -

Expected disbursement will be approx 4400 crs this year, NIM of 8% on incremental book.

-

Focusing on reducing the NPA levels to single digits in the SME book and run down the book (pure LAP Portfolio).Focus today is to reduce the Stage 3 percentage, then come back to the market with a clear strategy of lower ticket slab at around INR20lakhs, INR25 lakhs.

-

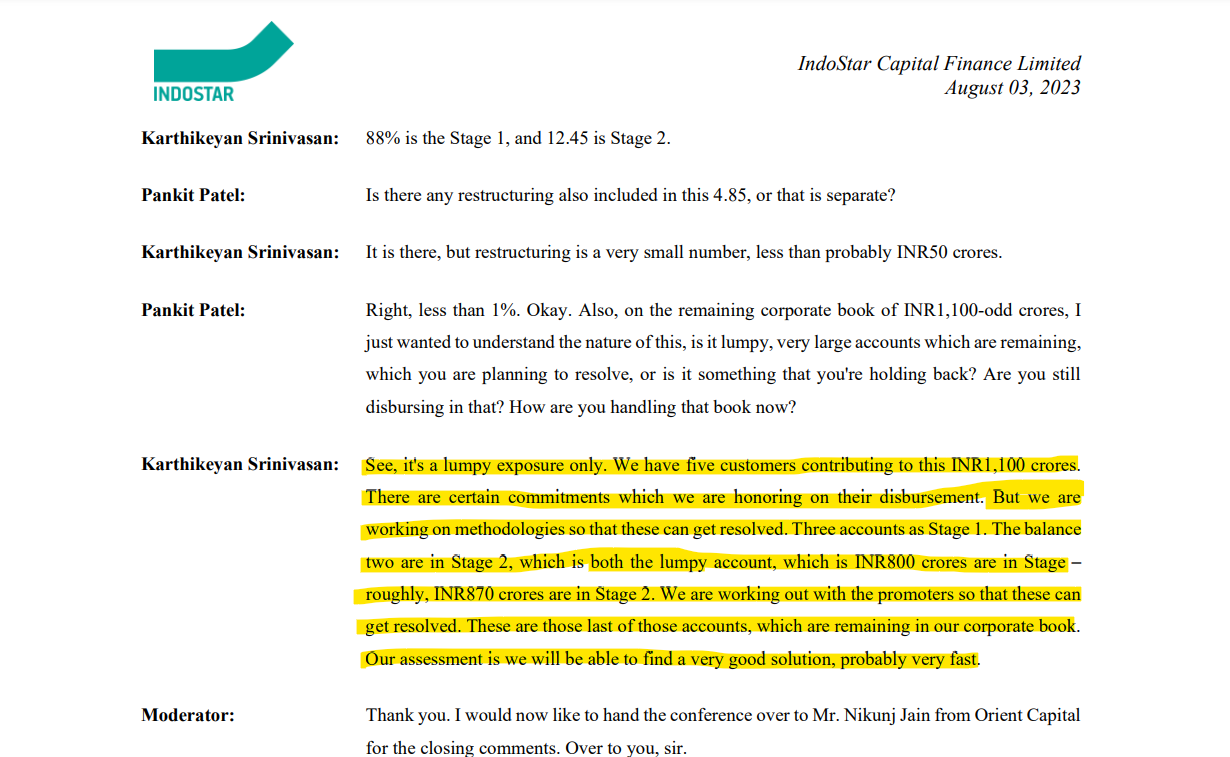

On Corporate side management is very serious to reduce it without impacting P&L. Mgt mentioned that there are certain commitments which we are honoring on their disbursement. But we are

working on methodologies so that these can get resolved. Our assessment is we will be able to find a very good solution, probably very fast. -

Yield on SME book is around 13%. Corporate book is at around 15%.

Disclosure : Same as above.

2 Likes

IndoStar Capital Finance Limited on August 25, 2023 has sold a significant portion of its legacy corporate loan book worth 915 crs to Phoenix ARC. This is a significant portion of the corporate loan book which was at 1190 crs as on March 31 2023.

Post the transaction, the share of the retail lending book in the company’s assets under management has increased from 85% to about 95%.

This is a decisive step and a major shift towards a pure retail lending book which the management was focusing on since couple of years. This will free up a lot of funds and reduce a lot of risk that was concentrated with couple of customers, the same was mentioned in the latest Q1 FY24 earnings conference call.

1 Like

Indostar Phoenix ARC.pdf (273.1 KB)

Old but relevant if u are looking to study indostar and Used CV theme

Do you know at what cost did they sell the loans? My guess is it will impact the q2 results as an exceptional item as expense. Is my understanding correct?

Indostar sold their loans for 790 crore, which is an 86% recovery on the total loan outstanding of ₹915 crore as per the below article. Honestly I don’t know how it will be treated on the P&L statement and what impact it will have, we will get to know tomorrow.

1 Like

Indostar Capital Finance approves preferential issue of convertible warrants

7518865b-a233-42a7-9704-75891e6f3aa3.pdf (321.3 KB)

1 Like

2 Likes