Indostar Capital Finance Limited

About the company

Incorporated in 2009, Indostar came up with an IPO in May 2018. Promoted by Indostar Capital (Everstone group), the company started its business with corporate and SME lending. In FY 2018, they ventured into retail lending by adding Home Finance and Vehicle Finance Business. This is how they introduce themselves on their website –

“We are a professionally managed and institutionally owned organization which is primarily engaged in providing structured term financing solutions to corporates and loans to small and medium enterprise “SME” borrowers in India. We recently expanded our portfolio to offer vehicle finance and housing finance products through our wholly-owned subsidiary IndoStar Home Finance Private Limited.”

About Business

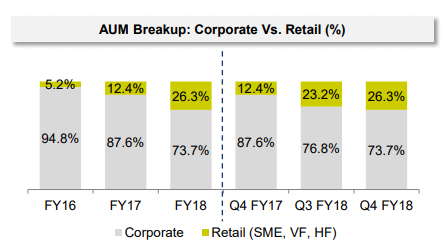

Indostar started its business with corporate lending and SME finance. The share of Corporate and retail (SME) lending in FY 2017 was 87.6% and 12.4% respectively. In 2018 they started Vehicle Finance and Housing Finance under the umbrella of retail finance. This resulted in change in their corporate and retail AUM mix which became 73.7% & 26.3% respectively at the end of 2018. Also they hired Ex-MD of Shriram Transport Finance Mr. R. Sridhar to take care of their retail lending business. Mr. R. Sridhar is the executive vice-chairman and CEO of the company. He is associated with the company since April 2017 and building his team.

Source: Corporate Presentation

Total assets of home loan and vehicle finance as of March 31, 2018 have been around INR 300 Cr. This year, they are targeting a run rate of 100 cr. Per month in VF and around 50 cr. in HF which makes a total of 150 cr per month or 1800 cr of book in FY 19 from these two verticals. Add another 150-200 cr of SME loan in it to arrive at 300-350 cr / month in total retail segment. That makes a book size of 3000+ cr in retail segment for the year 2019. (Source: Company Concall)

Strengths

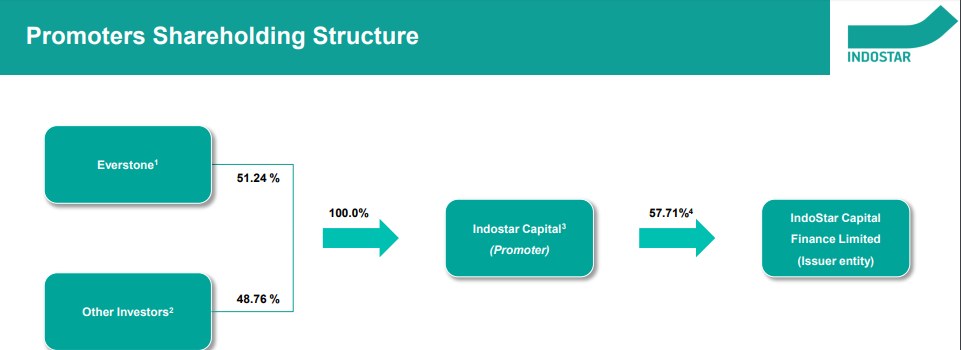

- Promoters – Promoted by Indostar Capital which is backed by Everstone group and other global investors.

Source: Corporate Presentation

- Indostar will possibly become a diversified NBFC with presence in wholesale and retail lending.

- 100+ Branch network & 1000+ employees -

- Major Shareholders post IPO – As on 25th May 2018 17.95% shares were held by FIIs, FPI, MFs & Banks. SBI Mutual Fund, Lenarco, BNP Paribas Arbitrage, SBI Life Insurance, ICICI Prudential Life Insurance, SBI Amundi Funds, Fidelity Investment Trust, ICICI Lombard General Insurance, HDFC Standard Life Insurance, Aditya Birla Sun Life Insurance, Reliance Mutual Fund, Bajaj Allianz Life Insurance, Max Life Insurance, Jupiter, Sundaram Mutual Fund & Reliance Nippon Life Insurance. 58.95% is held by promoters and remaining by others.

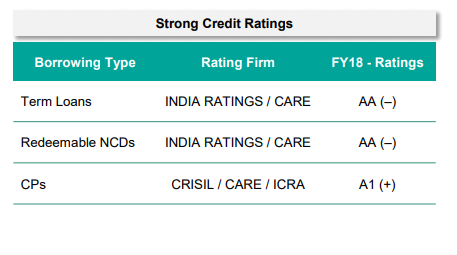

- Strong Credit Rating –

Source : Corporate Presentation

Business Opportunities

- Retail loan which comprise of Housing Finance, SME Finance & Vehicle Finance to double from here in next 2-3 years.

- Vehicle Finance is going to be the growth driver for next couple of years. As mentioned above, they are primarily into used vehicle finance where yields are high and so are the NPAs however higher yields will take care of high NPAs.

- Focussing on Corporate Lending and vehicle finance business, where yields are high, and targeting it to be around 70-75% of total assets. Both the businesses are expected to have a spread of 600 basis points.

- Low base advantage – They have recently started VF and HF business and the AUM base is low at present. This is going to result in high growth rate in these verticals in the years to come.

- Aggressive expansion – In 2018 itself, company opened 100 branches. This aggressive expansion will ensure high growth in loan book in years to come. In short term it may have negative impact on costs and return ratios but gradually cost will come down and with incremental revenue flowing in; their ratios will improve as well.

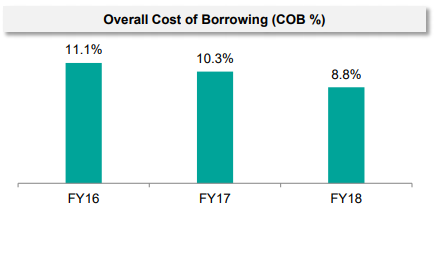

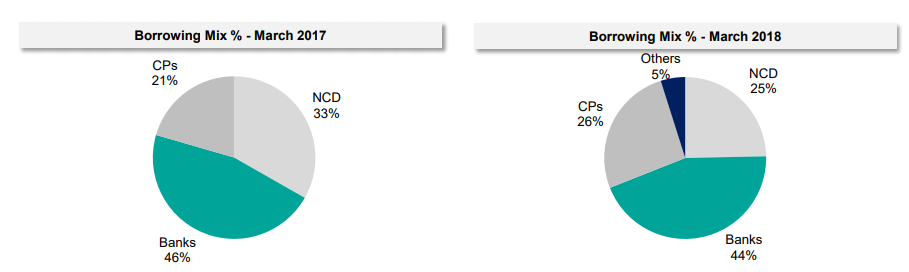

- With change in borrowing mix, Cost of borrowing is coming down

Source: Corporate Presentation

Indostar, with a Market Cap of around 4800 cr. and sales of Rs. 715.54 Cr (expected to grow from here due to aggressive targets in VF business) look cheap on valuation front. CMP of Rs 510 and Book Value of Rs. 262.75 translate P/B to 1.94 which is cheapest amongst NBFCs. Also with EPS of 29.95, PE comes to 17.02 which again is not too expensive for a growing company.

However there are few risk areas which are as follows -

Key Risks

-

Interest rate volatility – With interest rates rising in India, this could adversely impact their lending and treasury operations thus impacting their net interest income.

-

Execution of new ventures – Not being able to execute newly started ventures could result in adverse impact on NIMs and overall results of the company.

-

Increased in NPA

Company’s Gross NPAs were 890.00 million, or 1.7% of Gross Advances as of December 31, 2017,

as compared to 727.34 million, or 1.4% of Gross Advances as of March 31, 2017 and 100.00 million, or 0.2% of Gross Advances as of March 31, 2016.

Company’s provision for NPAs was 182.86 million as of December 31, 2017, as compared to 107.82 million as of March 31, 2017 and 20.00 million as of March 31, 2016. Company’s Gross NPAs and provisions have increased in recent periods and may continue to increase in future.

-

Exposure to specific sectors – Housing finance (HF)/Real estate are the sectors which are not doing well these days and in used vehicle finance business deviation (NPA) is usually high. For Indostar, HF and SME segments have low yields and have a spread of around 200-250 basis points. These two verticals are going to drag down overall yields for the time being.

-

Dependence on key Person – Hired Mr. R. Sridhar, Ex-MD of Shriram Transport finance to drive its retail foray. He is the key person as of now who is driving the retail lending growth. Over dependence on him is another key risk factor.

-

Competition – Most of the verticals in which company operates in except Used VF business are such where there is high competition mainly from banks, HFCs, MFIs and NBFCs. In Corporate lending business, existing players Edelweiss, L&T and in real estate we have Piramal, PNB Housing & L&T to name few.

-

Regulatory Changes – NBFC business is a regulated business and any change in regulations may adversely impact the company.

-

Macro Factors – Sale of commercial vehicles (CV) is positively co-related to various macro factors like GDP growth and per capita Income etc. Any deterioration in Indian/Global Macro picture can adversely impact of CV sales and business verticals like Home Finance, SME & Corporate Loans as well.

Company details

Registered & Corporate Office: One Indiabulls Center, 20th Floor, Tower 2A, Jupiter Mills Compound, Senapati Bapat Marg, Mumbai - 400013, Maharashtra, India

Telephone : +91(22) 43157000, Facsimile : +91 (22) 43157010

Contact Person : Jitendra Bhati, Company Secretary & and Compliance Officer

E – mail : investor.relations@indostarcapital.com

Website : www.indostarcapital.com

Disclaimer: - I’m not a SEBI registered Investment adviser and this is not an Investment Advice. I have recently taken a tracking position in this company and my views are positively biased. Please consult your investment adviser before Investing.