It is still a value play - whether to submit or not, behaviorally depends on your buying price really (But actually it should not depend on that).

I personally think that PE ownership generally benefits companies, so good to accumulate these at lower than buyback price gradually, which was the case with Essel Propack etc.

Co. is going to hold an EGM where the 3rd resolution was for a loan to the related party of the CEO.

After questions raised from shareholders the co. has withdrawn the resolution.

Since this is a subjective argument, take from it what you will about the management quality.

Today volume of Indostar raised and price touched 20%. Though there is no change in fundamentals, big interest shown in the stock. Is it turning around? Experts - can you share your views? The results also inline with covid impact…

Again, today too the stock hits 15% up… Good to see some volume raise… Any expert views on management did all possible provisions to have good base - will it improve the fortunes?

Is there a way to find out the ofs buyers in the nonnretail category?? If yes let me know please

For those tracking: any good thesis on back to back UCs. Looks like Mr Market has faith in what the management said earlier this month.

Disc.: invested

Indostar is looking to raise funds in its housing finance subsidiary through primary/secondary route.

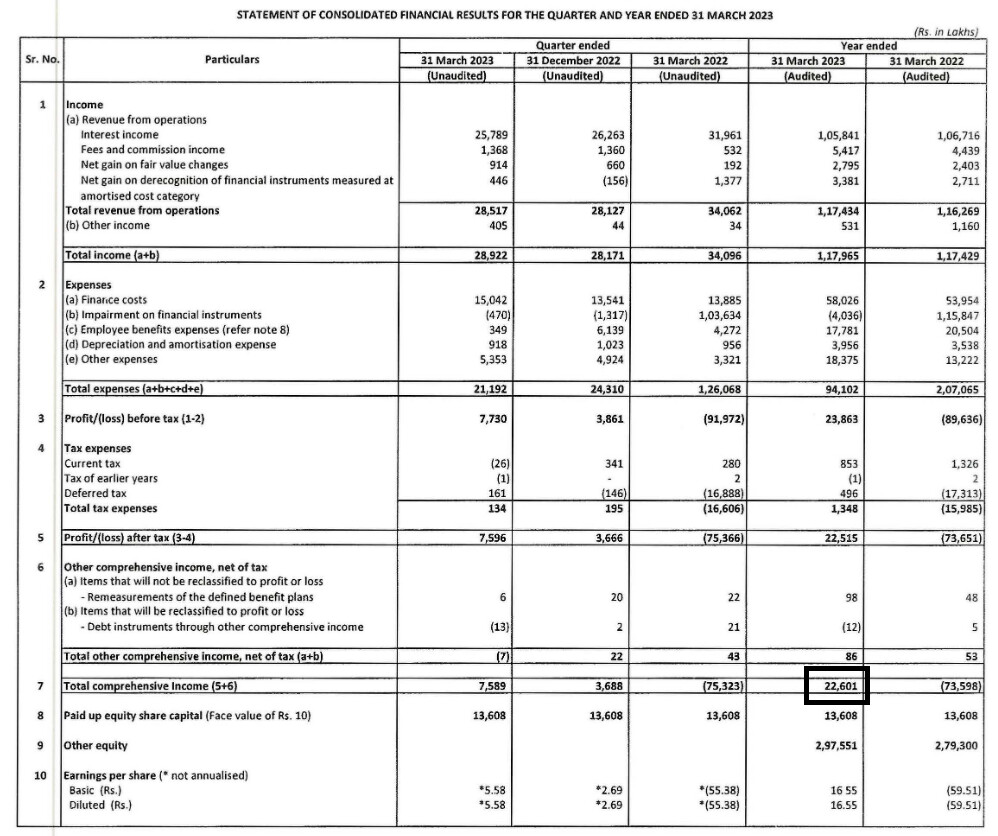

As of FY22, it had a net worth of Rs496 crore and in H1FY23 it generated a net profit of Rs29 crore. As there were no other changes in its equity, its H1FY23 net worth can, therefore, be estimated to be about Rs525 crore. The company seems to be on an expansion spree with the AUM up 34% y-o-y and GNPA and NNPA down to 1.4% and 1.1% in Q2FY23 from 3.1% and 2.4% in Q2FY22, respectively. Q2FY23 RoA was 4.4% compared to 2.6% in Q2FY22. Its Q2FY23 CRAR is 89.4%.

Aavas, Aptus and Home First currently trade at P/BV of 5.03x, 4.91x and 3.69x currently. If ICFL is able to raise funds for IHFL at 2x BV, that would be at a valuation of Rs1,050 crore. ICFL itself currently has a market cap of Rs1,841 crore. Any views?

1 Like

If there are no more skeletons in the closet (which management claims to be the case) then ICFL looks a very lucrative bet. We will have to wait till Q4 23 results to know for sure.

I am invested and adding more below 2000 Cr mcap.

Investment Thesis:

- change of management recently

- progressive retailization of loan book

- one time book clean up that happed earlier this year

- home finance division looks to be doing really well already; this fund raise will give a further fillip to overall valuations

- Deloitte removed the Going Concern Risk comment

- backed by high quality promoters (in FY22 AR Bobby Parekh came clean – I liked his courage and honesty); Brookfield has a major stake and this is their lone investment in India

Disc.: invested; dont go by what i say because I mostly get my thesis wrong ![]()

4 Likes

Good pointers! I too am invested, and hoping for a good housing finance story to play out.

But Deloitte saying no more a going concern is a worrying fact right? I’m confused how this is a good thing listed in your investment thesis…

What i meant was going concern is not a concern anymore per Deloitte. I have updated my comments in the post above. Thanks for calling it out.

1 Like

(Behind a paywall)

If it’s possible, pls so post the contents of the article…or a summary, since it’s behind a paywall…thanks

The article has a positive tone to it – the author sounds optimistic that ICFL will be able to turn the corner. I have noted couple of points from the article below:

- To address liquidity issues on its liability side, ICFL raised an incremental funding of Rs1,850 crore from 1 April 2022 to 10 August 2022. Also, the company repaid debentures worth Rs700 crore which were due for repayment later in August 2022 (highlighting it’s comfortable liquidity position). Timely resolution of its liquidity issues will remain a key determinant.

- ICFL has recognized most of its asset quality stress upfront and, going forward, its bottom-line will be aided by provision write-backs for the coming few quarters. Management expects a trend of provision write-backs to continue which will aid its bottom-line, going forward.

I would encourage you to purchase the article and read for yourself (MoneyLife allows you to purchase a single article for like 100 bucks).

3 Likes

whats your opinion on the OFS floor price?

I may be wrong but i find myself in the same situation as yours. same sentiments.

Disc: Tracking position only

1 Like

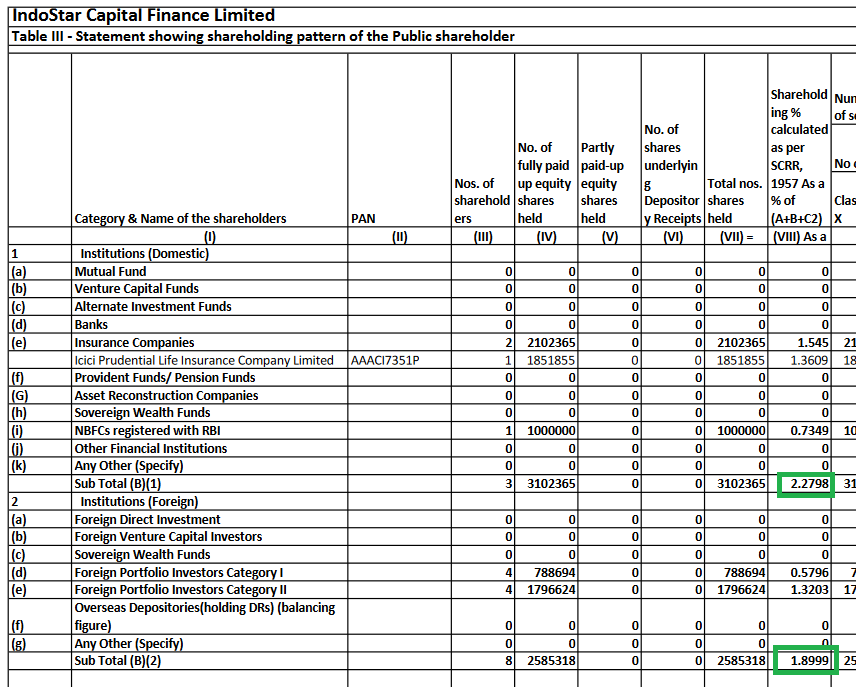

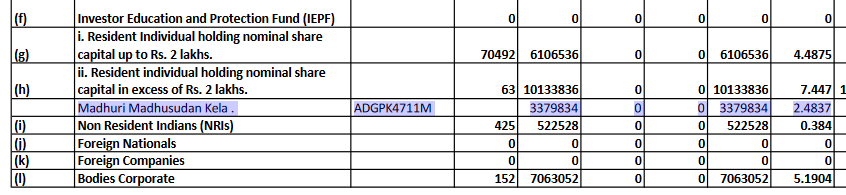

Post OFS the DII + FII holding is ~4.2% as opposed to ~3.7% pre OFS.

Madhusudan Kela has taken up ~2.5% stake in the OFS

Disc.: invested

2 Likes

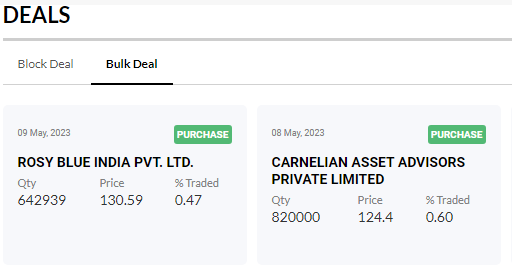

After the OFS was done there were two other major bulk deals

Disclosure : Invested

1 Like

What are the chances of indostar capital coming out of ASM? Does anyone have idea on when we can expect it to happen