Indostar Capital Finance Q4FY24 result Update: Posted Rs. 35.26 crores consolidated PAT in Q4FY24. The NBFC is focused on lending to the used-CV segment in T3/T4 space and the Affordable Housing Space in T2/T4 cities. The business has been running down its legacy SME book and is completely focused on growing the Retail book (CV+ Housing). Asset quality improved drastically with the company continuing to sell the bad loan SME book. GNPA: 4.9% vs 8% YOY in FY24. The overall loan book grew at a tepid pace of 11% YOY in Q4. PAT fell 50% YOY. All this would continue to put pressure on the ROE number. The company has also started monetising its security receipts which it shall use to grow the CV and the HL book. Indostar Capital Finance is still in a rebuilding phase and will take some time to come in good shape. Thnaks Deepak ![]()

2 Likes

1cc2857c-899b-4122-bb48-27e655b0536a.pdf (1.1 MB)

Views invited on the last evening move by Company.

Company has been able to sell the Housing Division for 1750 crores, this was around 20 percent of total business.

At current Market Cap of 4200 crore, company has been able to get a around 41 percent of market cap from a business which was only earning half as per current market cap.

I see a re rating from current levels and current BV ratio of 1.33 seems significant re rating in coming years.

Brookfields management is showing their potential and their concentration on used vehicle loan in this declining interest rate cycle seems to be a good move.

My views biased as I am invested significantly from lower levels

I had highlighted in Nov 2022 that the sale of the HFC could be a potential rerating event for the company. I had estimated a minimum valuation of Rs1,050 crore for the HFC based on that of peers and comparable M&A transactions. Seems like ICFL has been able to get a much higher valuation for the HFC than my estimate. The market may value ICFL’s residual business at a higher P/BV due to this transaction. Considering the presence of Brookfield as a promoter, the possibility of proceeds from the sale of the HFC being frittered away or siphoned off as that happened in some other companies is also low.

3 Likes

Your observation in Nov 2022 was perfect and stock has doubled from those levels. In fact it was below its BV at that time and a steal.

With this deal also now out of the way, what can be realistic P/BV anticipated as there is no dearth of capital, management has their lessons from past mistakes, declining interest rate scenario…

2 Likes

I think its prospective P/BV will depend on how it executes going forward given that most of its legacy problems are behind the company. One important factor will be how the management utilises the proceeds of the issue. My guess would be that the management will prioritise retirement of its high cost debt that the company had raised to tide over elevated delinquencies as a result of control deficiencies it had identified.

I’ll add one caveat regarding the current optically cheap P/BV ratio. A large part of the networth consists of goodwill that the company had recorded after the IIFL acquisition. This, in my opinion, is worthless and needs to be subtracted while calculating BVPS. It’s strange that ICFL has not impaired this goodwill considering that the acquisition wiped off more than Rs1,000 crore of its net worth. This is a sign of aggressive accounting and a negative about the company, in my opinion.

4 Likes

I feel with banks now onboarded and rating stable AA-, high cost can be swapped with low cost in coming months/quarters.

Joining of Randhir Singh in July and management strategy focus seems to be now on vehicle finance and small business loans.

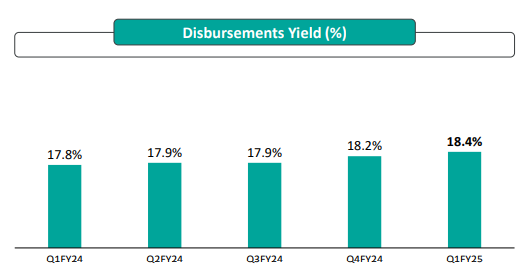

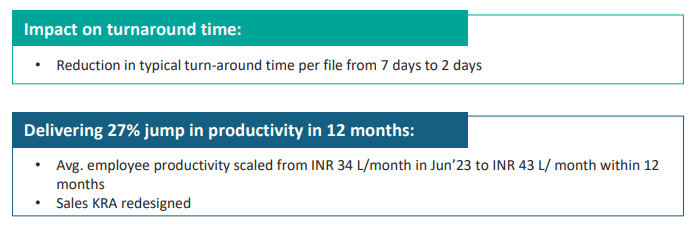

Management focus has been on increasing productivity and hence yields are on a positive trend and declining interest rates are only going to give more momentum on this vision.

If Indostar is able to change its market perception due to old legacy/goodwill a further rerating in coming quarters is likely. I can see early signs of management focused strategy on productivity, margins and growth. Any positives on NPA/Writebacks can further support.

1 Like

Indostar Capital last week sold its HFC business to EQT for 1750crs, this liquidity will help them focus on their core strengths of vehicle financing and small business loans. Also due to which the stock was in news and the trading activity picked up on back of huge volumes and the stock hit a 52 week high. The entire HFC and NBFC space is buzzing off late.

Fundamentally, during these 3 years management changes took place and legacy Corporate, vehicle finance and SME book was cleaned up. Funds were infused couple of times by the promoter Brookfield and other marquee investors took a pie of the shareholding.

Technically Indostar has been in correction mode since Aug 2021 and has formed a rounding bottom structure in form of a cup and it might create a low handle to the cup. If the pattern plays out the next technical target could be around 415 levels.

Disclosure : Invested as a trading bet.(Trades done in last week, this not a stock recommendation, anyone contemplating investing needs to do their own due diligence).

My takeways from Indostar Concall on the transaction:

- Transaction to conclude by Q4 FY 2025 or Q1 FY 2026

- Book Value addition of Rs 70 post transaction

- Proceeds utilization will be decided by management when they are near to receiving money

- ROA/ROE accreditive deal in coming 2-3 years and exact ROA impact will be shared later

- No plan to takeover any other company with this proceeds( 1300 crores+ post Tax-Cash balance)

- Cost of funds will also decrease in coming quarters

2 Likes

b6eff5f1-55c0-4873-afa2-64a4a9b1daee.pdf (1.6 MB)

Results are as per management guidance and growth in vehicle finance business is heartening. Post housing finance exit, book value will be more than 300 and current price likely to get re rated in 2-3 years.

QIP proceeds and recent rating change to AA- will help in growth capital and reducing interest rates will support return ratios.

Brookfield parentage ensures governance and Madhu soodan consistent holding gives more confidence in the building story.

I see it as a doubler in 3years. Am I missing anything?

2 Likes

-

The management took certain steps to maintain liquidity and clear the NPAs:-

-

Strategic refocus on core verticals of vehicle finance and small business loans

-

Sold ₹292 crore stressed SME loans to Encore ARC in 2024

-

Sold ₹915 crore legacy corporate loans to Phoenix ARC in 2023

-

Used commercial vehicle financing in tier 3/4 markets with yields exceeding 18%

Micro LAP product launched for small business loans

IndoStar Capital Finance represents a transformation story from a stressed NBFC to a focused retail lender with strong institutional backing. The recent subsidiary sale provides significant capital for growth in core businesses, while the company continues to address legacy issues through systematic portfolio cleanup strategies.

In the recent results ,it is clearly seen that their cost of finance is decreasing , their collection efficiency is increasing QoQ. Their NPA levels are already down , with 91% secured lending the collection of money doesn’t look challenging .

1 Like

Also, Price to Book of 0.9 in current decreasing interest scenario for a strong NBFC franchise gives the Margin of Safety.

P.S: Invested, views biased and generally optimistic in approach

1 Like