Substantial acquisition from Sterlite power increasing AUM to 20k cr as guided earlier. This should increase their distribution promise by couple of years at least. Debt goes up to capacity of 65% so now rights issue will be needed to grow from now.

1 Like

IndiGrid CEO on Acquisition of Northeast Power Transmission Project:

1 Like

Intimation_of_outcome_of_Board_Meeting_India_Grid_Trust_23_03_2021.pdf (283.2 KB)

Right issue priced at Rs 110 per unit opening on 06/04/2021 , right entitlement ratio 1:5

First of all, one need to have minimum 8505 (1701*5 lot), to get right entitlement in holding. In case you hold less than 8505 units, then you get fractional entitlement. In such case, one need to apply through net banking in ABSA. I got in Zordha Demat account 2 Lot for Right entitlement. Same was trading at around Rs 17 per unit (today morning) with closing price of 14.15 in BSE and 14.85 per unit in NSE. Tomorrow is last day to renounce the right entitlement through online trading. I sold my right entitlement in BSE, as I do intend to subscribe through 4 family accounts with fractional entitlements (which can not be traded, but have higher than 50% probability of allotment as per my assumption). In two accounts, I would get second preference for allotment, in third account I would get third preference and in fourth account I would get fourth (or least) preference. Since the minimium lot size is for 1701 units, I need to apply for 4 lot in four name to try my luck. Hence, I decided to sale Right entitlement and try my luck through subscription.

However, I am facing issue to apply in HDFC Bank net banking, as my holding was in Zerodha CDSL account. HDFC Net banking not enable for third party demat account as per my discussion with my friends. I am checking with my relationship manager to understand how to go about applying in right. I also understand from my friends, that HUF can not apply in right through ABSA. Will keep posted the forum with whatever information I get on this issue.

Meanwhile, find enclosed link for FAQ in PDF from RTA website. http://lnk.ncore.karvy.com/gtrack?clientid=41952&ul=CgYPVwYBAVUBSAdEUlAAUQUFI15VV1hZTwdbCRlI&ml=CgAPV08ERFIBBwYJSg==&sl=ekt7GWZnRDB9YEpUWF8fC1FeEVwWXVBHFx0aBwpZSQc=&pp=0&&c=0000

There is not much arbitrage left. One should consider buying rights @14 or below and subscribe @110 to make it a 10% yielding asset considering the annual distribution of Rs 12.4/unit. That is one reason it is selling off but tomorrow should be the last date for the weakness to end.

Could you please give a little clarity on how to do this offline from A to Z?

Go to Indigrid website > Choose Investors Section > Choose Rights Issue 2021 > Download "Application Form. Fill it up and submit to nearby ASBA enable bank branch

Thanks @dd1474 & @sumi00 : - Was looking for RE arb, bt didnt seemed mch thr.

BTW, wat r ur views on the upcoming Powergrid InvIT? How does that compare with Indigrid competitively?

Disclosure : - Not invested.

Don’t think they would offer anything more than 9-9.5% yield. Powergrid Invit will be true sovereign AAA and should trade at GoI 10 Y yield +150bp at max. That’s why I mentioned that a 10% yield in IndiGrid is a good deal. I grabbed few lots @14/RE and will subscribe more. Look at RBI how they are hell bent in keeping bond yields low.

For people in the 30% tax bracket, post tax yield of 7% at current levels is just a better option compared to Bank FDs or some AAA bonds.

REITs can provide the same post tax yield with a much stronger element of capital appreciation.

Only those that got in at <=100 levels it makes sense and is a better alternative than REITs with stronger stability in cash flows.

1 Like

You think only retail invests here? This will be a favoured investment for insurance and pension funds and retiree’s for semi- perpetual returns. I have personally moved my family’s FDs here. REITs have to spend sometime in the recovery process. They will be a good buy for me if they go below their issue price. Don’t believe their NAVs since some of those calculations are invariably optimistic. I would rather bet on very high probability 10% per tax than speculate on capital appreciation as of now. I would wait for one big correction to invest in REITs.

1 Like

for people applying in Indigrid rights entitlement, now kotak bank is showing it and can apply thru the same

Thanks for seeking my view. My disclaimer, I hold IndiaGrid InvIT, IRB InvIT and Embassy REIT (latest addition, with major holding purchased yesterday).

Please also note that I am not expert and my understanding may be completely wrong.

I see InvIT/REIT as structuring of cashflow which changes when the trust purchase new assets which get financed from debt equity mix to provide stable cashflow over a long period to investor. So business wise, Powergrid shall be theoretical similar to India Grid. However, it would also depend on valuation of underlying assets, what price that units are issued to invest and access to new assets in future by Powergrid InvIT. This would be critical input to decide whether to invest or not for me.

In my limited understanding, while InvIT are currently providing higher current yield, over a decade, I find REIT are better than InvIT, other thing being same. REIT has main income (lease rental) which normally increase with inflation.

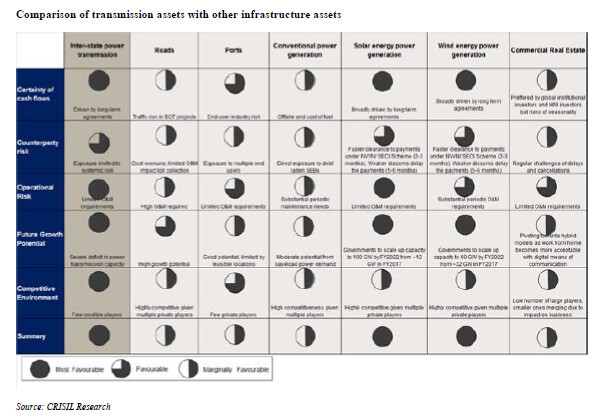

Transmission assets provide very stable cashflow, but limited (in many case no linkage to inflation). If one go through portfolio of assets of IndiaGrid, except for 1-2 Transmission assets, none have inflation linked increase. Revenue is almost stable over a very long period. Hence, the future growth in distribution can broadly came only from acquisition of new assets and change (mainly decline in interest rate).

In case of Road assets, while IRB InvIT assets has superior on inflation and growth fronts (with toll being linked to inflation and traffic growth linked to economy), it has relatively higher volatile cashflow which can result in cash distribution from toll assets. Second point, life of road toll agreement is generally 15-20 years while that for transmission assets is generally 30 years. On third point, ownership of assets of Road is handed over to Government after completion of concession agreement, while in transmission agreement, revenue would technically terminate on end of agreement, the assets are still owned by Transmission InvIT which would have some terminal value.

In case of REIT, the revenue (lease rental and leasable area), assets are owned by REIT (with average life of around 50 years with maintenance), revenue having inflation linkage and income earning capacity over life of assets (unless Work from home results in major decline in Commercial real assets). So I see relatively lower current distribution, but potential to grow distribution to grow over a long period of time. Also capital value appreciation in Real estate is more likely to benefit over a longer period, to REIT over Transmission InvIT and Road InvIT.

Find enclosed comparison of various infrastructure assets in India, sourced from IndiGrid Letter of Offer in 25 March 2021, Page 168 (in pdf) which I find very useful.

Please note that this is my personal view, may be biased and may be wrong.

25 Likes

looks interesting considering the positive experience in India Grid Trust

1 Like

Is this technology a threat to likes of power grid, indigrid?

Disc. Invested in indigrid

1 Like

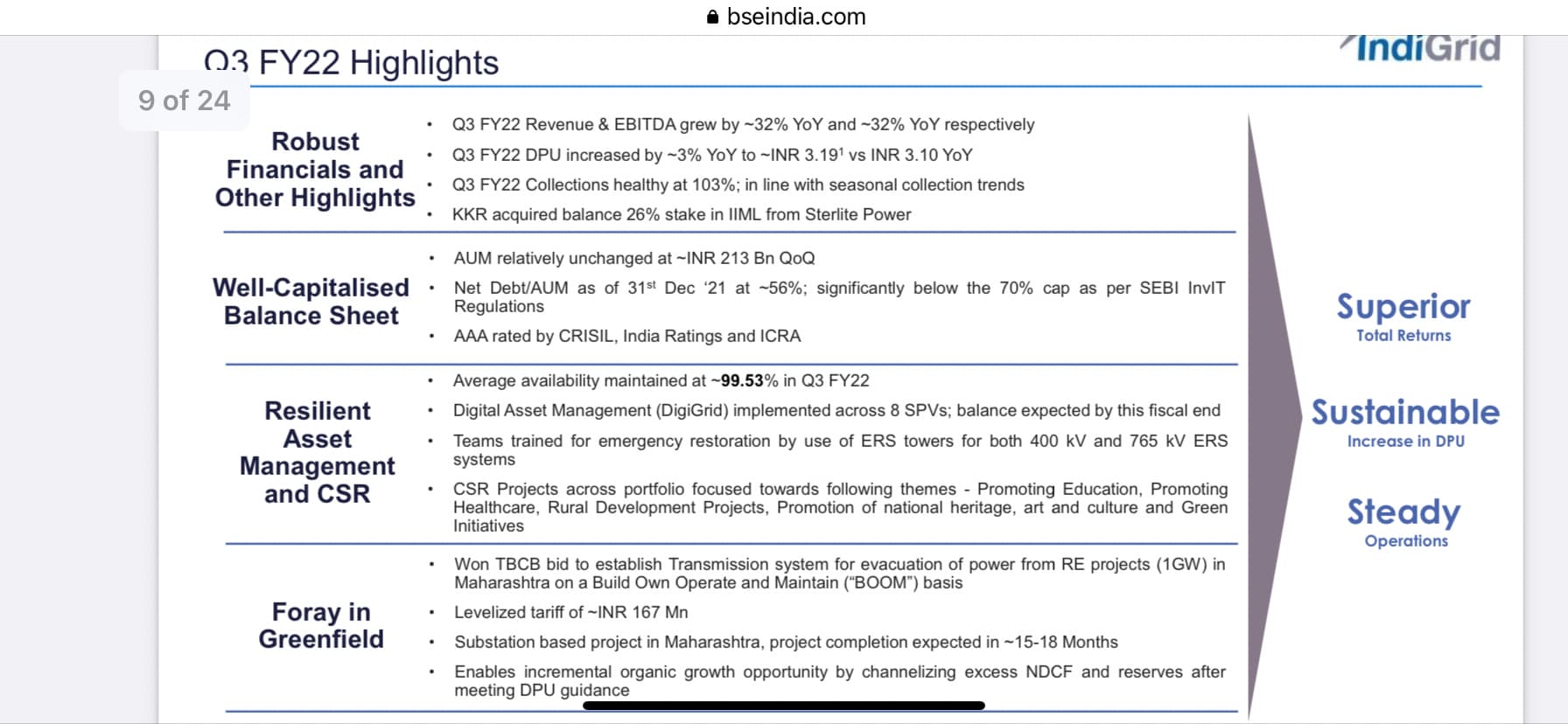

I see that there are hardly any following/updates in this thread. Here is the latest investor presentation

The distribution this time will be as follows (1st Nov 2021 is the ex Div date and the likely payment date is 11th Nov)

The Board also approved a Distribution Per Unit (DPU) of Rs 3.19 (up 6% YoY) for Q2FY22 to unitholders. The record date for the distribution is November 02, 2021, and shall be paid as Rs 1.86 per unit in the form of interest, Rs 1.28 as capital repayment and Rs 0.05 per unit as a dividend. With this, IndiGrid has distributed Rs 52.15 per unit to its investors over the last 18 quarters since its listing, a total return of roughly 90% on the issue price. The total return is the sum of all distributions since listing till Q1 FY21 and the change in price till September 30, 2021.

1 Like

The above breakup is key for all INVIT holders to note, because of the complex taxation here.

- Your returns from InvITs are subject to complex taxation. Though the InvIT itself is treated as a pass-through entity, its distributions are taxed based on their source. Any loan repayments by SPVs distributed to you are not taxed. But dividends earned by the InvIT from its SPV and passed on to you are taxable at your slab rate if the InvIT has opted for a concessional tax regime. Interest received from SPVs and distributed by the InvIT are also taxed at your slab rate. Capital gains you make on transacting in units attract tax at 15% if held for less than 3 years and at 10% if held longer.

===========================

I assume that because of the above the Rs 1.28 (capital repayment) is not taxed at all. Market veterans, INVIT holders, pl confirm… Thx (BTW…the above thread clearly discusses this topic and there are several confirmations but checking once more, for a double confirmation)…Thx

1 Like

Q3 results out. Dividend declared is Rs 3.18/unit. Record date is 2nd Feb.

Investor presentation - https://www.bseindia.com/xml-data/corpfiling/AttachLive/8c7d6825-7731-440c-ae8b-94eb8e672c48.pdf

4 Likes

3rd Quarter distribution mail to the individual holders, should be in your mailbox today. As always, the break up of interest and capital repayment is clearly given.

Feb 10th is the date of credit