Tons of information.Thanks for sharing it Varun

2 Likes

So the results are out and Indigo Paints has scored on all parameters i.e. EBIDTA, Profit, Revenue and Margins. Note that it had higher advertising spends this time and still managed to grow top and bottom lines. It continues to strengthen its position in the Premium Emulsions category (biggest revenue contributor) and has posted very good volume growth. Now my question and confusion is, why is the market not excited with these results? The stock had taken a beating for 12 months now and I was hoping this set of numbers would warrant a cheer from the market but NO ! I have read in some articles that the market did not like the fact that this PAT and margin growth came at the expense of price hikes. But isn’t it a good thing that they were able to pass on the costs? I have been studying and investing in the stock market since 18 months now so my knowledge is quite limited but from all the books, articles, experiences of other investors that I have read about, I did gather that any player who is able to sustain or improve margins during a downturn, is worth his salt. It demonstrates superior product or pricing power or good demand etc. So why is this a bad thing? Also, with the RM costs softening, advertising spends expected to come down, the margins will only improve. So what am I missing here? Thanks

1 Like

below is my opinion, at first the company offered the IPO price at 1000 bucks and listed in above 2000, which indeed gives an impression about the company. but, if you look at the facts indigo top line is ramp up at 2X speed before listing and this must be the reason market treated well at listing time. However, co is disappointed in the following quarters with witnessing slow and steady state revenue run rate, which is disappointed. And later time though revenue run rate clocked a bit due to other factors it sees a margin pressure. thus, further declined the stock and later time competition with Jsw & Cos entering into paint industry which indeed a very big threat for the player like Indigo as the base is small and other factors like concall commentary is not in sync with numbers, if you happen to listen previous con calls they mention to improve the revenue with atleast and at a min 30%, but on a overall even with 30% runrate increase the current price is justified.

I hope it is possible to clock the runrate at higher base, improve margins and I believe this is very much possible in near quarters with the launch of new factory which is scheduled to begin this year.

1 Like

When does the Lock-in period for existing investors expire for Indigo? Sequoia continues to own 13.73% and SCI investments own another 14.81%, the possibility of these shares coming into the market as these investors exit may create substantial pressure on the stock price. Even if fundamentals play out as expected, additional float in the market could contract the PE ratio. Any clarity on this point would be helpful.

5 Likes

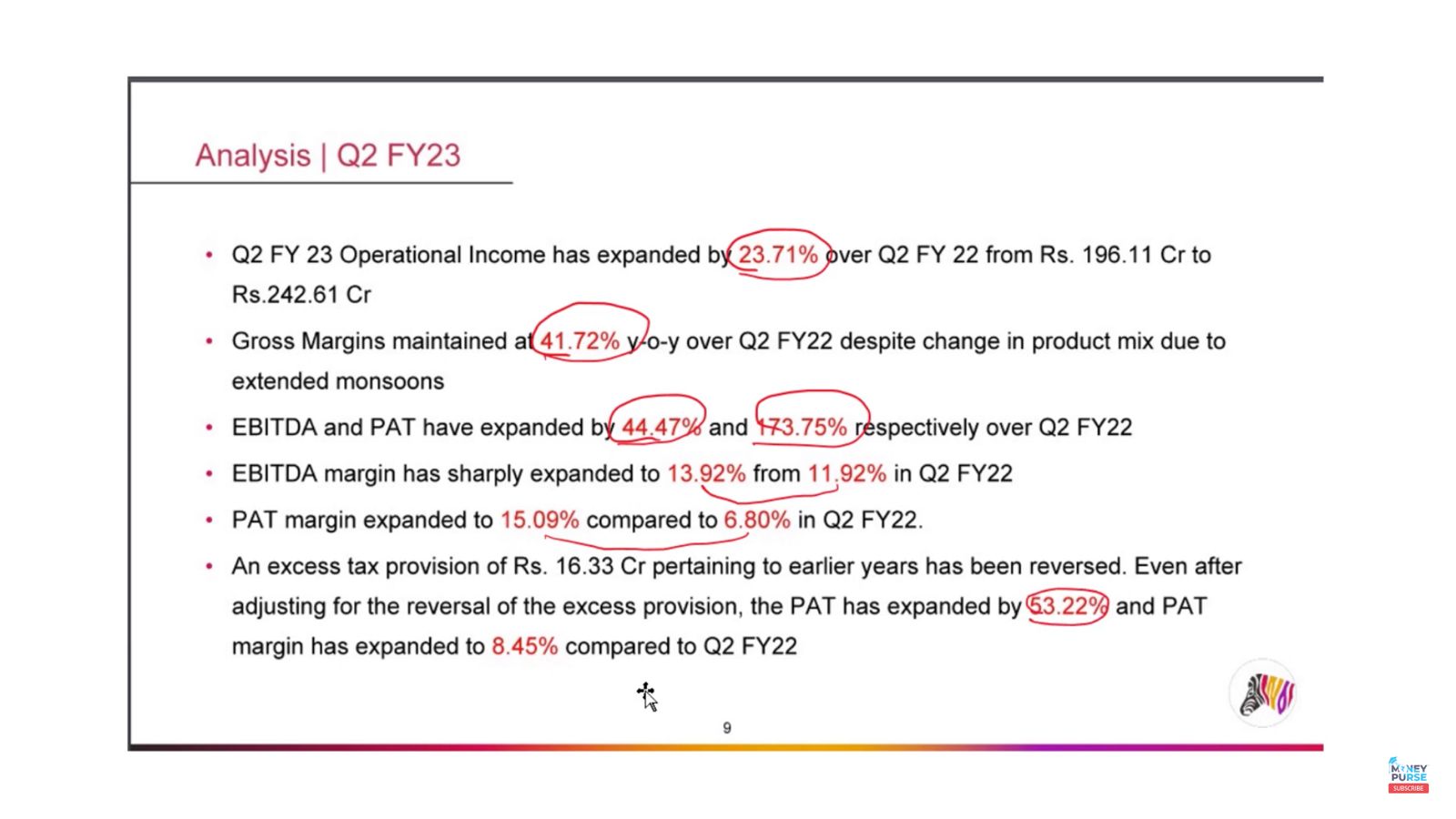

So the good thing is that for Q2FY23, IndiGo Paints posted strong results ! Net profit climbing by 174 percent on-year to Rs 37.1 crore. Revenue during the quarter came in at Rs 242.6 crore, which was 23.7 percent higher as compared to the year-ago period. Even after adjusting for the excess tax provision of o16.3Cr from last year, current PAT has expanded by 53.22% while PAT margin increased to 8. 45% compared to last quarter. It also had good sales momentum at a time when its peers are slowing down. Which is why it shot up over 15% in the aftermath of the results.

However, the bad part (atleast from a stock price perspective) is that venture capital firm Sequoia said that they will sell off 3.3 percent equity stake worth Rs 235 crore, with a floor price set at Rs 1,315 per share. As of September 30, 2022, Sequoia Capital held a total of 13.73 percent stake in IndiGo Paints, as per the shareholding pattern shared with the BSE. Which is why, the stock price has taken a beating since 2 days.

Attaching results analysis

3 Likes

Hi,

I am trying to find some information. Please see if you can help

- What is the ad spend in comparison to revenue- Has it come down over the years?

- What is the current number of tinting machines?

- **What is the current share of Kerela in the revenue? Want to understand its dependence on a single state? Has their market share fallen in Kerela in comparison to the last few years?

2 Likes

One of the main issues with indigo has been over valuations. Currently at just under 5000 crores mcap I think we can finally say it’s cooled off to reasonable valuations now. Based on the recent concall and presentations it looks like Q4 will be even better than q3 and January has already seen good growth. Q3 would’ve been better but the entire paints industry struggled due to the late monsoon end disrupting October a bit. So we are at around 4 to 5 x sales currently which makes it one of the cheaper companies in the paints sector. Management is adamant they can grow at 1.5x to 2x the leaders rate. Overall industry should grow at 12 to 13 percent per year according to them. Value growth and volume growth should be around equal now with price hikes now behind us. Raw material cooling means trade discounts cooling too. They say ebidta margins should stay steady and similar. New products coming on line in q1 and once capacity on line it’s enough to grow for 2 to 3 years(I may have misunderstood this part) and no debt. Market share currently is around 2.5 percent. Management is very open and give out a lot of information. So overall it’s currently at fair valuations for a paints company(which is still expensive!)

The question left is Does the paints industry deserve such high valuations overall. I’m not sure it does and there in lies the problem. Historical valuations doesn’t equal future evaluations. That being said This seems like a good way to play the paints space if one has belief in this sector since even the loss making Shalimar is at 3x sales and Indigo deserves a higher valuation than Shalimar. That being said assuming 12 percent industry growth and hence Indigo at 1.5 to 2 times that gives a max 20 or so percent growth per year. So it’s still expensive unless the paints company continues to command a premium which is what I don’t want to bank on.

@Prashantit2009

The latest concall mentioned ad spends (I can’t remember top of my head). Also mentions Kerala as one of the major states and how it’s performing more than the average Vs other states. No exact split though. I’d recommend reading the transcript though it may not satisfy your questions properly

Disc : Not invested. Not a sebi advisor. Just tracking the paints sector and Indigo for now.

4 Likes

My understanding:

I agree the main issues are valuations, fuss around new entrants, and not registering 2X growth like before. If you observe the results of major paint companies, Akzo Nobel registered the highest YOY sales for Q3 around 7%(need to understand if growth came from decorative or institutions). Indigo comes second at around 5.9%(decorative). This means Indigo gained market share over the top 2 players.

Right now, valuations are cheap if you observe the valuation history of paint companies but in general, it’s still expensive. According to the new strategy, management is promising 2X the industry growth(I am Skeptical here). Paint companies take capacity expansion 2-3 years before they reach maximum capacity(80% is the peak utilization level in the paint industry). They are doing this expansion because their Kerala plant reached peak capacity.

1 Like

Does the paints industry deserve such high valuations overall?

Answer:

Recently, I oversaw the paint work for my house(a small job). I personally went to buy the required paint for it. First, I wanted to select a paint that is the highest quality(the only thing that came to my mind). The dealer gave me 3 options Asian paints, Berger paints, and Indigo paints, and multiple variants of each company. In general, I asked which type of paint looks good on a particular surface. He suggested Indigo paints and Asian paints. After finalizing items and all, came the pricing. He gave a small discount and the job was completed. I visited the dealer to return some extra items then he enquired about the look and how satisfied I am with the color and quality.

My realizations:

- Price doesn’t matter in the paint industry. Low prices don’t mean people shift to a new brand.

- Dealer & painter wants to suggest the best product for the customer. Incentives don’t push sales a lot if you have a sub-par product.

- Brand and only Brand matters in this industry.

Correct me if I am wrong…

1 Like

There are a lot of factors involved unfortunately and it’s not so cut and dry. Dealers try to sell you what they get the most benefit from. For eg Asian paints(and the rest too) gives them certain targets to hit to get rewards. If they sell x amount they get to take their family for a trip to kerala and if they hit xx amount they get to take them for a free trip to Paris etc. At these events families of distributors all across India meet up and become friends and this leads to them trying to hit these targets every year. They also get rewards like bikes and tablets etc. Apart from that it’s about ease of stocking and replacing, ease of payment ie most work on money upfront so the bigger the discount the better, margins are thin so dealers need to keep this in mind too. Then the availability of tinting machines etc. The above is just b2c for the distributor. They also need to negotiate b2b contracts which are longer term with for eg a car service center for automobile paints etc and pricing is key here since whoever quotes the lowest gets the contracts. So pricing is very important in this industry. Add the number of players currently with each one undercutting each other and giving better rewards + new big players coming in it’s only going to get tougher with everyone trying to tempt distributors to sell their products.

Source: My wife’s family has a side business of a paints shop which has been handed down from her grandparents

Not a sebi advisor. Edit: invested today near 52 week low… Though with just 1/5th of my planned quantity

Apologies for the above post since its not directly linked to Indigo since they don’t stock it in their shop(since the benefits from Asian, akzo and berger are too good to switch now) but hopefully it helps with the discussion

11 Likes

Clarifications:

I tried to give an overview of what happened rather than a detailed scenario. When buying paint try to look at it from a consumer pov rather than the investor pov(because we are more aware of the paint industry). When I said price doesn’t matter in this industry I meant the decorative segment as it contributes 80-85% and the rest comes from B2B(My mistake) and Indigo only operates in the decorative segment. I did face a push from the dealer but only in low-value products like distemper but for high-value purchases, the final decision came from me(Again I should have clarified it further but if anyone tried to purchase paint recently then it would be evident). Coming to dealers, and retailers rather than going on trips or receiving gifts the high priority will be on moving products as fast and as much as possible(With newer Brands there is always this risk). I agree dealers and retailers try to sell a product that gives them more margin but all players follow and give the same discount. If you observe the trade discounts(Everyone player has a cap on how much they can give the discount) For Example:: last quarter everyone in the industry followed the same strategy(I listened to all con-calls starting from Asian paints to Indigo paints) on how much they can provide trade discounts due to raw material easing. If you listen to the last con-call of Indigo paints & Akzo Nobel they specifically talk about how trade discounts and A&P won’t increase sales and dealers.

Coming to pricing:

I respectfully disagree because pricing in B2B is completely different from B2C. If you observe everyone talks about new entrant being big, competent, and can disrupt the industry but fail to understand that already a formidable player entered and has been in the industry for the last 3 years(JSW Paints). They are large in their respective industries. I haven’t seen any pricing war in the industry (Apart from all colors same price but not being able to garner much attention at least where I am located). But on further observations, I noticed they are introducing differentiated products, increasing brand image, and trying to get dealers from weaker brands. When it comes to B2C: Brand recall, Differentiated products/Innovative products, sales aggression matters a lot more than price.

*** I have zero knowledge of the B2B category. So, I won’t comment on that ***

3 Likes

Cheers. You are right regards a lot of b2c. However, it’s not just consumers in b2c and there is a mix of b2b in there as well. In our client list for eg most of the revenue and recurring orders come from hotels and building complexes and colleges etc. These would still be consumers at the end of the day… So they’d be listed under b2c. These projects can lead to huge amount of money so every company Ie Akzo, Asian, berger etc go through long bidding wars here and usually the final decision by these businesses is based on good quality that will last a long while at low price. For the bigger clients the marketing teams of these companies come down and take us out to dinner and make a case for their product. And we meet them on our trips so I’m pretty close with the marketing teams of these companies and they tend to tell me about their struggles/competition/targets etc so maybe I’m a bit disillusioned about this space a bit ![]() .

.

Also, it’s quite rare to deal directly with a final customer here. Usually it’s the interior designer /architect or painter. And it’s easier to set up deals with them since they usually buy on credit… So the dealer has the power to recommend the products he has in stock or wants to push since he would be the one risking it all by giving it out on credit.That being said… This is just one shop in a big city that is run more as a legacy to grandparents + pay salaries of staff that have been there for decades + sponsor our trips across the world. There’ll be huge differences across India in different dealerships for sure.

Sidenote : The first time I saw the books I nearly fell off my seat since the dealership is almost like an nbfc… Giving out credit to a list of 300 or so clients per year and then needing to plan out npas and harass clients for collections and hoping they all pay lol. I know our competitors(other dealers) compete with us by giving longer credit cycles too. So we have to buy our products with cash in advance and then give it out to clients at razor thin margins. The beneficiary in this are the paints companies since they don’t have to work like and nbfc while we do lol. So while I wouldn’t ever invest in a dealership of my own I’ve also seen good things and seen the wealth this industry can create and how they can pass on costs to us and the customers easily too with no risk of collections.

Also, it’s not easy to switch to a different supplier so even with loads of capital I don’t see grasim being a huge success straight off. With the competition as high as it is the fact these companies still make such huge profits is amazing and I don’t see that changing anytime soon.

Hence why I’ve begun investing at these levels in indigo since I like their business model ie differentiated products + rural to city and the fact they’ve managed to grow even with this competition from nothing in just 20 years (even though we don’t stock them and tbh they haven’t even approached us yet in our city).

Disc: Invested. Not a sebi advisor. I am just drawing from first hand experience… But that may be a very microscopic view. Please flag of this isn’t adding value to the thread since it’s more about dealerships than the actual company

11 Likes

Hi, Not sure if you got the information you were looking for. I started tracking this company hence i have the info readily available, shared for your benefit.

All the info you are looking for is also in Annual report and investor presentations.

years are 2020, 2021, 2022

2 Likes

Thanks for your scuttlebutt. I am stuggling to pull a bear/base/bull case scenario for this as i have started accumulating after reading available information. could you please guide / share your thought process on the same?

There is no reasoning or rationale provided anywhere in the article for this price target. Not sure why they even bother coming up with price targets.

2 Likes

The rationale is clear, the writing is on the wall, there is intense competition with JSW, Grasims and likes are/ will be heavily in the sector, which will lead to oversupply, price competition, Margins are likely to be suppressed and deteriorate over next few years. Makes the Sector as a whole shaky and in for a ride, only maybe sector leader and differentiated players like Akzo Nobel may not have a major margin impact.

1 Like

Not sure if 'Oversupply ’ is a problem though. Indian Paint Industry is the fastest-growing major paint economy the world over, with a consistent double-digit growth over the last 2 decades. Don’t see why this trend would discontinue. So the demand is going to be healthy. In fact, after the supply chain issues and increase in raw material prices, there is more demand and less supply. The other points you mentioned are debatable but would like to understand more as to why the sector as a whole is shaky?

I think the rationale is something that is very similar to this video

However, Grasim is not entering the playing field till year end and while that may be a reason to buy Grasim ,the PE reduction predictions can only hit mark in bearish market . Indigo anyway is trading near the target and 40 PE . So I guess it was a low hanging fruit for an analyst looking to publish a report .

3 Likes

Thanks. Interesting video but don’t really buy the argument that Grasim will somehow magically disrupt the industry and change the dynamics just because they have deep pockets. Historically, there have been others who tried and failed before. So, it all comes down to execution, distribution, dealer relationships etc. Grasim may go on to be successful, but is it going to at the cost of other organized players is a wait and watch for me. Also, Grasim themselves believe that their entry will lead to a shift of demand from unorganized players to organized players which it aims to catalyze. This might also help the organized players further. The decorative paints sector is a Rs.40,000 crore market, with unorganized players accounting for one-fourth of the market share. So there is a good chance that the current top 4-5 companies might still be able to grow and maintain their margins over the long term. And the demand for this segment is also ever increasing so it remains to be seen how much of it can be captured by Grasim. While the points called out in the video are definitely good food for thought, I don’t see any major moats or advantages that Grasim comes with apart from deep pockets and a good starting points of using their putty distribution channels. Also, Indigo Paints is pre-dominantly in the tier-3, tier-4 cities whereas Grasim is planning to target Tier-1 and Tier-2. Its not easy for new entrants to make immediate impact as it would take a good 5-6 years to establish oneself and then start to compete with incumbents. Indigo Paints took ten years to build brand recall among customers through heavy advertising. Grasim does have the their cement depots to sell its paints but building a brand is neither easy nor quick. So, I personally don’t see any adverse impact on Indigo paints in the near term and dare I say medium term too.

7 Likes