Expstrong textanding presence. Indigo Paints to foray into waterproofing strong text , construction chemicals; expand reach

Posted good set of overall numbers.

Some highlights:

- Gross margin in Q4 FY23 came in at 46.82%, best in the industry if I am not wrong.

- EBIDTA margin also expanded to 22% this quarter.

- Crossed the 1000 Crores mark in revenues for the full year for the first time

- Revenue, PAT and EBIDTA all grew considerably this year. However, interesting thing to note is that while revenue grew at 18.47%, EBIDTA grew at 33.5% and PAT at 56.98%, which in my mind is a big positive as bottom line is growing more exponentially than sales.

All good signs so far. If someone else who’s also been following this business can analyze the results and point out any negatives, that would be great.

Disc: Invested and biased. Not a buy/sell recommendation.

4 Likes

Positives:

- Margin expansion even though some of the benefits are passed to retailers due to a better product mix.

- Good growth in enamels and wood coatings.

- Acquisition in construction range and also entered into waterproofing products.

- Slight market share gain over peers(Maybe in the range of 0. something for the quarter)

- Growth in Tier 1 & 2 towns is double of Tier 3 & 4 towns.

Negatives: - Decrease in Active Dealers.

1 Like

1 Like

KEY insight From Concall of Q1 FY24

- One of the best Concall that I have read this year

- Management is very bullish on there business

- High volume growth in all categories

- Jodhpur plant 90000 KLPA operational by end FY25

- Three month back they acquired satke in Apple chemie a fast growing company in construction chemical and water proofing space

- Apple chemical expected to become a pan Indian player in couple of years (currently only maharashtra)

- The only risk i found is that there 28% revenues come from only kerala state,

But this share gradually decreasing.

Disc : Invested and biased. Not a buy/sell recommendation.

6 Likes

4 Likes

Hi, I came across the company recently, went through the concalls/PPTs and below are my observations.

The super high valuations of the company at the time of the IPO has not held up, and the current price has gone below IPO price and profits have increased, thus making the company relatively cheaper, hence attracted my interest.

The co. is growing ahead of the industry, margins have improved and now there is little headroom for margins to improve from here, based on A&P spends. If they continue to grow ahead of the industry, and A&P spends grow at lesser rate, then some benefits will show up in the EBIDTA, and the co. expects that it could reach 20% EBITDA margins next year. Currently their margins are second best, slightly behind Asian Paints.

The company has finished the TN capex and initiated the Jodhpur capex. Their strategy of focusing on 750 cities has resulted in growth. The mgmt is expecting to finish the year (FY24) around 1350 Cr, this is 25% growth over last year. And next year they are targeting to grow beyond 25% (their target is to grow between 30-40%), provided industry grows to its pre-pandemic levels of around 8-10%. The co. is expecting Apple Chemie also to grow to 55-60Cr, and very bullish on the subsidiary outperforming going forward.

The mgmt has, multiple times, alluded to reaching closer to #2 and #3, and if from Fy24, they grow 5x they would still not be #3 by 2029, they will be less than 7000Cr topline. Assuming they maintain their margins (10% NPM), and assuming PE multiple of 40, the mcap could reach 28,000Cr, that would be over 4x from current levels in 5 years (32% CAGR).

The triggers are:

- Focus on 750 cities, increasing the tinting machines, increasing per dealer business, increasing engagement with influencers in these 750 cities

- Foray in projects business

- Foray in retail waterproofing segment

- Taking Apple Chemie’s waterproofing and construction chemicals business to PAN India level from a single state of MAH at the time of acquisition.

A big question is, will the company be able to grow as per its own expectations.

Another big risk to this thesis, and connected to the above risk will be, how Grasim executes its plan. There are fears that Grasim will alter the industry structure significantly and historical profits/returns earned by the incumbents will reduce. If that plays out, then all the parameters like growth, margins, multiples will reduce for the current players and above thesis will fail.

Disc: not invested, but interested

4 Likes

Another set of good results (just skimmed through them). They have been delivering consistently on the business front. It has undergone price and PE correction during the same time frame in which it increased its revenue, profit and market share. To me, the current stock price behaviour is a reflection of the macro environment and nothing more. I am happy to hold as long as they keep walking the talk.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/56bc180f-b452-45f7-8180-284cfd868b92.pdf

NOTE - Invested, biased and not a SEBI registered advisor. So if you want to gamble your hard earned Rupees on my 2 cents, you are better off playing Roulette ![]()

3 Likes

Few of my takeaways from Q1 FY25 of Indigo Paints

Indigo Paints delivered industry-leading growth of 7.8% in a challenging quarter, though management admitted this fell short of internal expectations. The company saw robust 47% growth in its subsidiary Apple Chemie, signaling strong momentum in the construction chemicals segment. However, weakness in the key Kerala market dragged down overall performance. Management expressed cautious optimism about demand revival, noting strong sales in July.

𝐒𝐭𝐫𝐚𝐭𝐞𝐠𝐢𝐜 𝐁𝐥𝐮𝐞𝐩𝐫𝐢𝐧𝐭:

The company is doubling down on digital marketing to complement its TV advertising. It’s also expanding its waterproofing and construction chemicals portfolio, aiming for 8-10% revenue contribution in the medium term. Indigo continues to focus on expanding its dealer network and tinting machine installations to drive growth.

𝐌𝐚𝐫𝐤𝐞𝐭 𝐃𝐲𝐧𝐚𝐦𝐢𝐜𝐬:

There’s a clear shift towards value-added and differentiated products. Indigo is leveraging its technological edge from subsidiary Apple Chemie to develop superior quality waterproofing solutions. The company is also seeing traction in its economy range of distempers, indicating demand across price points.

𝐈𝐧𝐝𝐮𝐬𝐭𝐫𝐲 𝐓𝐚𝐢𝐥𝐰𝐢𝐧𝐝𝐬:

Gradual recovery in rural demand could boost sales of economy products. Recent price hikes of ~2% by the industry should aid margin recovery. Growing focus on waterproofing and construction chemicals presents a sizeable growth opportunity.

𝐈𝐧𝐝𝐮𝐬𝐭𝐫𝐲 𝐇𝐞𝐚𝐝𝐰𝐢𝐧𝐝𝐬:

Subdued consumer sentiment continues to impact discretionary spending. Raw material cost volatility remains a concern. Intense competition among established players is putting pressure on channel discounts.

𝐈𝐧𝐯𝐞𝐬𝐭𝐨𝐫/𝐀𝐧𝐚𝐥𝐲𝐬𝐭 𝐐𝐮𝐞𝐬𝐭𝐢𝐨𝐧𝐬:

Analysts probed about the impact of new entrants like Birla Opus. Management downplayed concerns, citing historical precedents of new players struggling to gain significant market share quickly. They emphasized Indigo’s 25-year survival instinct and ability to compete against giants.

𝐂𝐨𝐦𝐩𝐞𝐭𝐢𝐭𝐢𝐯𝐞 𝐋𝐚𝐧𝐝𝐬𝐜𝐚𝐩𝐞:

While dismissing immediate threats from new entrants, management acknowledged fierce competition from the top 4 players. Indigo aims to differentiate through superior product quality, especially in waterproofing, and better execution on the ground.

𝐅𝐮𝐭𝐮𝐫𝐞 𝐏𝐫𝐨𝐣𝐞𝐜𝐭𝐢𝐨𝐧𝐬:

Management refrained from providing specific guidance but expressed hope for sharp uptick in both top-line and bottom-line from Q2 onwards. They cautioned that July’s strong performance may not necessarily continue in August and September.

𝐂𝐚𝐩𝐢𝐭𝐚𝐥 𝐃𝐞𝐩𝐥𝐨𝐲𝐦𝐞𝐧𝐭:

Indigo has completed major capex with its Tamil Nadu plant and is now expanding capacity at Jodhpur. Management expects these investments to meet requirements for the next 4 years, indicating a shift towards sweating existing assets.

𝐎𝐩𝐩𝐨𝐫𝐭𝐮𝐧𝐢𝐭𝐢𝐞𝐬 & 𝐑𝐢𝐬𝐤𝐬:

The waterproofing and construction chemicals segment presents a significant growth opportunity. However, the company faces risks from potential prolonged demand weakness and margin pressure due to competitive intensity.

𝐂𝐨𝐧𝐬𝐮𝐦𝐞𝐫 𝐏𝐮𝐥𝐬𝐞:

Management noted subdued market conditions but saw encouraging signs in July sales. They remain cautiously optimistic about demand recovery in the coming quarters.

1 Like

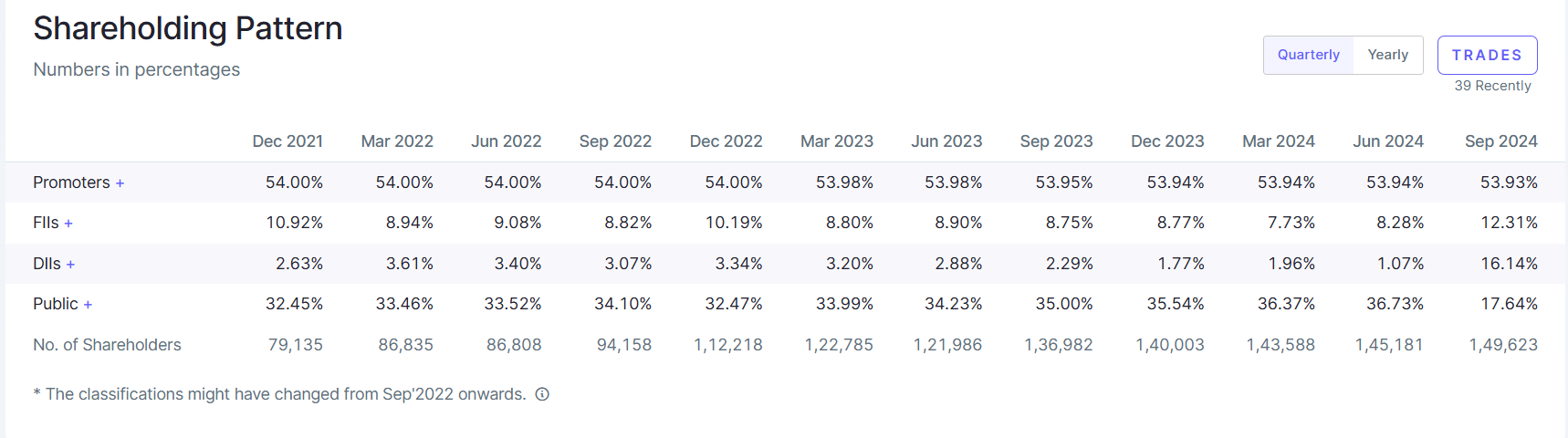

Peak XV (formerly Sequoia capital) sells 22 pc stake in Indigo Paints to investors like Morgan Stanley, Mercer, HDFC MF.

1 Like

While studying Indigo Paints found some interesting insights on what Hemant Jalan, the promoter had to tell about the industry from his learning’s. Below is a presentation on the same

Management Insights.pdf (932.1 KB)

2 Likes

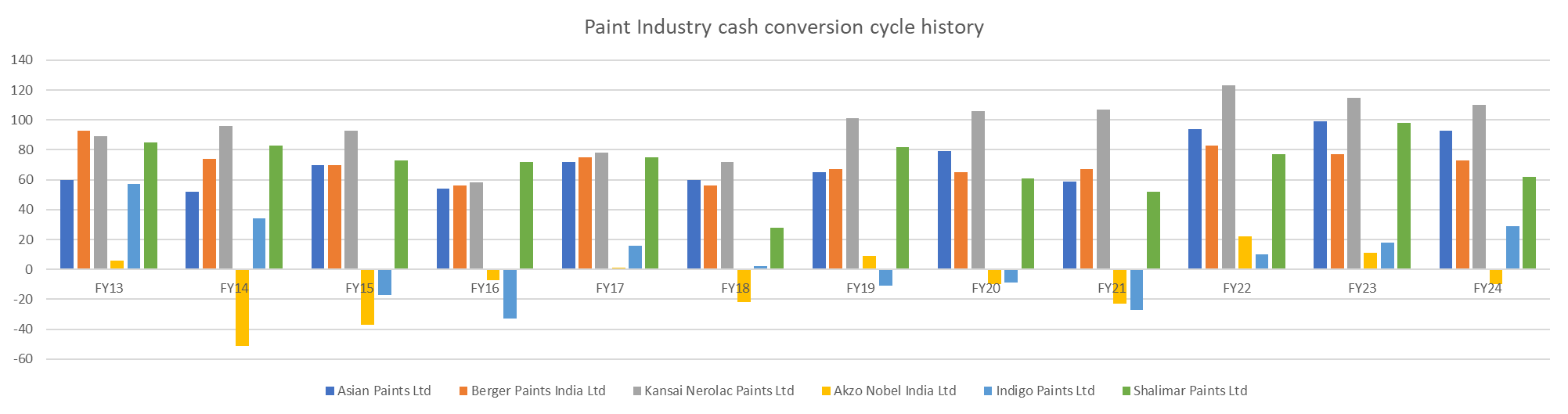

I believe the chart is self-explanatory in identifying the most efficient player in the paint industry when it comes to working capital management.

Inspite of the pain in the industry, wonder why FIIs and DIIs have increased stake so much? Any insights what is cooking here?

This is because Peak XV Partners sold 22% stake in a bulk deal in September. FIIs and DIIs picked up most of that stake. Peak XV Partners is classified under “Public” shareholders.

6 Likes

Indigo Paints Q3 Outlook

- Demand Recovery: Anticipating a breakout from year-long slowdown in Q4 FY25 (seasonally strong quarter).

- Margin Expansion: Driven by higher premium product sales and better product mix in Apple Chemie (focus on select states).

- A&P Expenses: Expected to decline slightly as % of revenue despite higher digital ad spends.

- EBITDA Margins: Projected to improve sequentially in Q4 FY25.