Initiating Coverage report from Sharekhan

4 Likes

Good set of recovery post Q2FY22, margin pressure depreciet the bottom line otherwise would post more better numbers, awaiting to participate in management concall to understand concerns towards this front.

1 Like

There is zero upward movement in its share price over the last 6 months. In fact it fell 37% during this time. Given that they have increased revenues, dealer network and added over 1000 tinting machines last year, they seem to be doing the right things. However, their profit/EPS dipped last quarter. I am trying to understand if we could see a turn-around soon if the following 3 areas improve i.e.

- Decrease in crude prices (will lead to overall decrease in in raw materials and increase in margins)

- Increase in demand in auto industry

- Uptrend in Construction, Infra, Housing activity

Or, is there more going on in the back-ground which we should be wary of? Also, its market cap is now just under 7500 Cr, which is much more reasonable than what it was during IPO. Thoughts?

The simplest answer to this in my opinion is - Its IPO came at very high valuation and it then further ballooned up after it listed at 109% premium. You can go through this thread and find various members’ opinion about the overvaluation.

Also, the total free float of the company’s stock is also very low which is a double-edged sword.

Everything which was overvalued in last one year has been corrected on a proportionate scale and Russia-Ukrain War followed by Crude oil price relation inflation (which is very much real) has only accelerated the correction further (due to margin compression worries).

Leaving here these two for further reading:

For educationcational purpose, posting this thread to understand how the game of low float works:

5 Likes

Indigo Paints was touted to be fastest growing Paints company in India during the time of IPO. What has happened in last one year time is there was impact in sales from Kerala where they have major market share due to prolonged Covid cases. If you see the profits are going to be almost flat for FY22 compared to FY21. Not sure how it will pan out in future but you have a company with little or no growth in bottom line with almost 100PE. So the stock price is bound to be corrected if it does not deliver the investors expectations.

Disc: No holding in Indigo Paints. Was tracking after IPO

1 Like

Thank you. I agree it was overvalued during IPO. But now that it has corrected by ~40%, is it a good long term bet? It still trades at a higher PE of ~100 but given how quickly it scaled up in terms of sales and OPM over the last 5-6 years (per data from screener), it looks like a solid business. Maybe the next quarter or two will provide a better picture on how it can cope with macro + competition.

Whether or not it’s a long term bet - hard to tell. Company’s past performance doesn’t necessarily guarantee the same in future. One has to take a call based on his/her risk appetite. But there are many risk factors which market definitely don’t like and has punished the stock price accordingly.

Mutual funds have been decreasing their stake significantly in this company:

Disc: Never invested

1 Like

Inflationary environment would be a big test of pricing powers of all companies, more so for smaller companies like Indigo. For a equivalent PE of around 100, Asian Paints clearly looks like much better from risk reward point of view, although it may be slower growing as compared to Indigo

1 Like

Recently while listening to veteran Kenneth Andrade (Old bridge capital) on youtube, came across an interesting slide that shows analysis of paints industry by sales, profit pool, mcap and new entrants on horizon - shalimar, aditya birla group etc. I am not pasting the screenshot here as their is risk of potential copyright violation.

The key takeaway was that profit pool of 6000 cr of entire industry will be under higher pressure with entry of new deep pocketed players and could lead to pricing war and margin erosion. Given the super elevated current valuations of most paint players, it can be a significant risk in near to medium term for the industry.

3 Likes

Not sure if you are talking about the same, but Kenneth touches on paint sector on in the video ( see at 58 min).

6 Likes

Yes, the slide I am referring to is presented in this video and also some of the other recent youtube videos where Kenneth has presented his ideas.

Below article also has some data points on how Paints industry is attracting new competition. At the same time existing players are also increasing capacity. So the scenario that Kenneth is trying to draw attention to has a high probability of playing out in next 2-3 yrs

1 Like

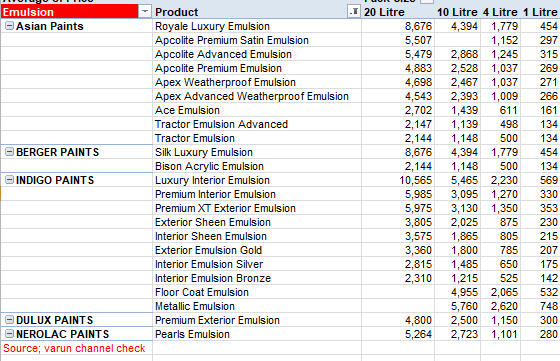

Over here we are assuming that Paint is perfectly rational product (meaning; consumer compares price and features, and hence conclude which product is superior. This is a false assumption. And hence, fear of price/margin pressure in the industry is unwarranted. Infact; I did price comparison of APNT, BRGR, Indigo (attached image of the same), and figured out that there is no price-challenging strategy being used by Indigo to win APNT and BRGR market share. This industry is immune to pricing pressures, historical evidence both in India and Globally proves so!. Enjoy being investor in APNT, BRGR. There is zero risk!! …infact, newbies must obsess about creating institutions (focused on culture) rather than obsessing about business-activity (promising capex and creating and selling products!).

13 Likes

Hi Varun,

Thanks for this insight. Appreciate your channel check on prices.

My thoughts:

- Your channel checks only cover decorative paints. There are lot of other applications of paints in different industries which also contribute to revenue and profits which we are missing here

- Choice of a selecting a particular decorative paint by customer will depend on different factors for different categories of customers - not everyone is seeking brand. Also, local dealers, local painters and local architects can be easily influenced (at least in short to medium term) - there are enough and more known successful tactics that sales team uses for this day in and day out

- Margins are already under tremendous pressure due to cost escalation on oil and its derivatives used in paints. If inventory continues to build up, some players will be forced to go for occasional inventory unload by offering steep discounts (again a defacto practice used regularly by many business)

- As the number of players increase (especially deep pocketed players who are also digging in for long haul), profit pool will be under pressure. Only question is what will be the degree of pressure.

- No investment is zero risk…if that was the case, entire world would have piled up on Asian Paints or Berger Paints…if you look at the stock chart history, there are long periods of underperformance of share prices of both companies when they too had faced challenges.

Just My Opinion!

4 Likes

Just adding on some pointers on the discussion:-

-

All paint companies took massive price hikes in Q3, which will be visible in sales numbers fully from this quarter. The margins under pressure point might actually end up surprising markets - considering inventory will be selling from Q3 and prices will be higher - OPMs might not be as bad as people expect

-

In Indigo’s latest conference call - Mr Jalan clearly points out that Q4 is an exceptionally strong quarter for them seasonally. If this does happen the reaction will be interesting - we still have not seen a single Q4 from Indigo so markets are still evaluating/gauging a high growth story

-

Indigo has seen healthy growth last couple of years inspite of COVID - faster than industry leaders. Laggards have been Akzonobel and Nerolac.

-

Paint market is quite price inelastic and still growing decently in terms of top line. That historically makes ‘margin erosion’ periods usually decent times to invest - as these companies even otherwise are prohibitively expensive. That said, current valuations are no where near cheap despite corrections

-

Indigo follows a very different rural first strategy. They also recruit new dealers from clearly differentiated products and then extend range. Competitive intensity is definitely there - but it would be interesting to see if these competition brands go for the massive markets of the leaders or the relatively smaller pie of Indigo

-

Profit pools will definitely be shared more. But considering industry growth rate - profit pools will also continue to compound for a long period of time and won’t be stagnant at the current number. So we should not be looking at the profit pool now but over a long term period.

That said, I completely agree on the point that

there is absolutely no stock which is ‘zero risk’

Discl : Invested, biased. Not a registered advisor.

4 Likes

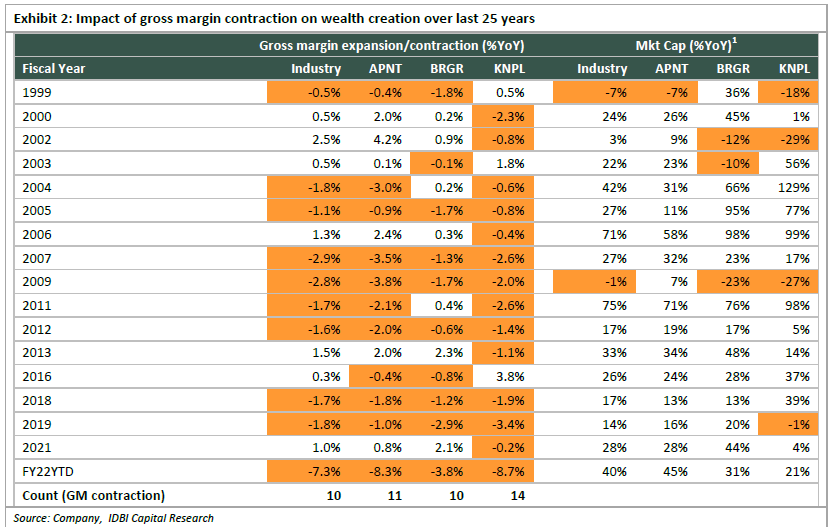

Lets talk some data over here; instead of shelling emotional bombs! …we say time is toughest test to pass …as fantasies almost always catches up with realities with time/age (you see as you age, how you become less aggressive!) …last 25 years; plot the chart on Gross margin contraction and market cap contraction … and this is how it looks like (from my research note)

Also, if you do regression analysis; you will figure out that permanent damage to revenue growth (due to new competition/change in business landscape) should be the first red-flag to junk the stock (answers when to sell; read; common stock uncommon profits - recommended by his holiness Mr. Buffet) …so, when i say zero risk, i said it poetically! …need not take it literally …

But offcourse; mathematical gymnastics has its own point of diminishing-marginal-returns …hence, Mr. buffet uses calculator to find value …while rest of the time (90%+) he is reading and thinking …so, main question is what kind of permanent damage to revenue growth APNT, BRGR are frought with …this requires lot of evolutionary study of paint companies (india + global) …base on whatever reading i have done (read 120+ books last 2 years), my conviction on no-permanent-damage-to-revenue-growth is high …hence, I would conclude to better buy companies at 100 P/E and expect multiple de-rating (to 25-30P/E) after 20-30 years …and its a mathematical certainity that your compounding will range between 18-25% if ROE and PAT growth is c. 20% during same time period (This is Charlie Munger’s statement; read poor charlie book) …

8 Likes

Also, never to forget that paint is 50% penetrated product only …and also BRGR has always been serious competition to APNT compared to the up-coming newbies …Indigo going rural is not a choice in strategy but compulsion as they cannot win the battle with APNT and BRGR in markets where they are strong …BRGR made this point a several time that they would prefer virgin markets over well-contested markets …strategies which obsessed about; supply-creates-its-own-demand has there own set of limitations …

3 Likes

I shared; decorative as that’s the major revenue contributor…i have data for other categories …but all data pointed similar conclusion…hence to save time (of both reader and author) chose to share only decorative.

5 Likes