Business

- [Market position]: Indigo is the fastest growing amongst the top five paint companies in India. They are the fifth largest company in the Indian decorative paint industry by revenue for FY2020. They have achieved this position by introducing differentiated products, building brand equity for the primary consumer brand of “Indigo”, creating an extensive distribution network across 27 states and 7 UTs as of Sep30, 2020, and installing tinting machines across the network of dealers.

- [Business Strategy]: To create demand for their differentiated products, they initially tapped into Tier 3, Tier 4 Cities, and Rural Areas, where brand penetration is easier and dealers have greater ability to influence customer purchase decisions. They subsequently leveraged this network to engage with dealers in Tier 1 and Tier 2 Cities and Metros as well.

- [Brand Building]: They engaged Mr. Mahendra Singh Dhoni as their brand ambassador, to enhance their brand image amongst end customers. They concentrated these branding efforts on their differentiated products and then leveraged these efforts to increase distribution and sale of their complete range of decorative paint products.

- [Product Range]: They manufacture a complete range of decorative paints including emulsions, enamels, wood coatings, distempers, primers, putties and cement paints. They also identify potential product needs from customers and introduce differentiated products to meet these requirements, and create a distinct market for their products.

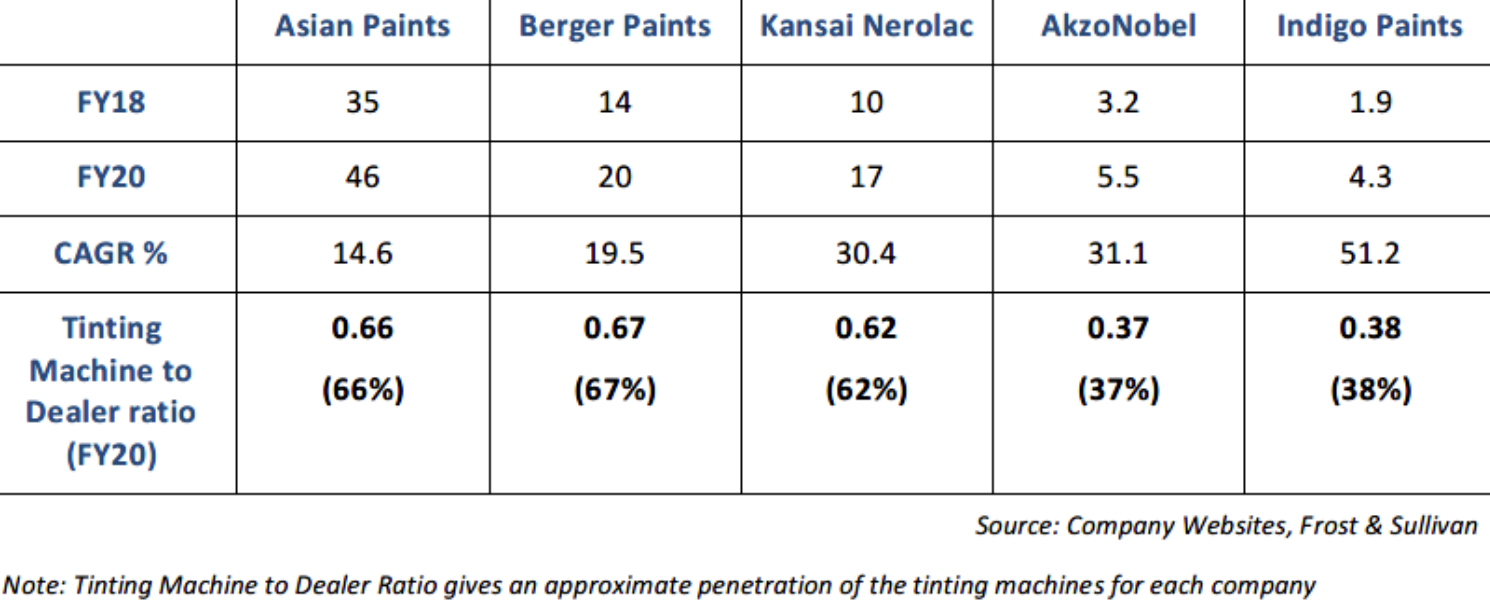

- [Product Innovation]: For instance, They are the first company to manufacture and introduce certain differentiated products in the decorative paint market in India, which includes their Metallic Emulsions, Tile Coat Emulsions, Bright Ceiling Coat Emulsions, Floor Coat Emulsions, Dirtproof & Waterproof Exterior Laminate, Exterior and Interior Acrylic Laminate, and PU Super Gloss Enamel. These products are differentiated based on the end-use they cater to, as well as added properties that they possess. Revenue generated from Indigo Differentiated Products represented 26.68%, 27.58%, and 28.62% of total revenue in FY 2018, 2019 & 2020, respectively. As the first company in India to develop these products, they have had an early mover advantage in the markets we are present in, which has allowed them to realize relatively higher margins for these products compared to the rest of their product portfolio. As of March 31, 2018, 2019 and 2020, the total number of tinting machines that we placed across our network of dealers was 1,808, 3,143 and 4,296, respectively.

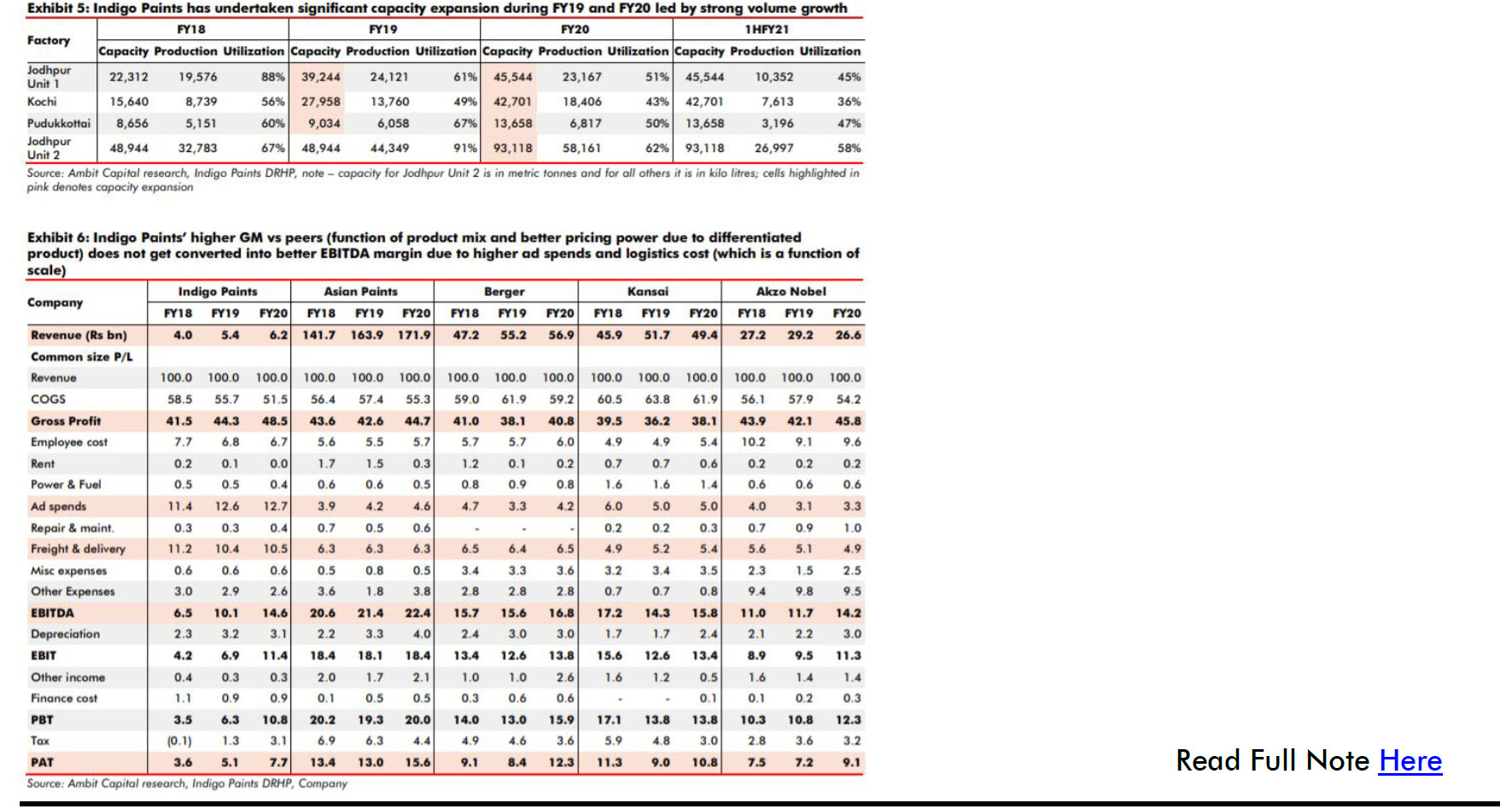

- [Manufacturing]: As of Sep30, 2020, they own 3 manufacturing facilities located in Jodhpur, Kochi & Pudukkottai with an aggregate estimated installed production capacity of 101,903 KL per annum (“KLPA”) for liquid paints and 93,118 metric tonnes per annum (“MTPA”) for putties and powder paints. These manufacturing facilities are strategically located in close proximity to raw material sources that reduces inward freight costs, lowering their cost of raw materials.

- [Capex]: Will expand their manufacturing capacities at the facility at Pudukkottai, by adding capacities to manufacture water-based paints to cater to the growing demand for these paints. The proposed installed production capacity of the expansion unit is 50,000 KLPA and it is expected to be 155 operational during Fiscal 2023. Will be funded through IPO proceeds.

- [Products in the Existing categories]: Dirt-proof & Water-proof Exterior Laminate: Indigo Paints launched India’s first and only paint that gives equally effective protection from dirt as well as water; Acrylic Laminate: Indigo Acrylic Laminate is a premium quality emulsion; PU Super Gloss Enamels: an all-surface enamel paint that delivers superior gloss and protects wood and metal with its anti-fungal and non-yellowing properties; Polymer Putty: A white cement based putty with special polymers that gives double protection to the wall with a smooth and bright finish

- [Unique Products disrupting market]: Metallic Emulsion (Walls): pioneered the Metallic Emulsion segment, which gives a designer finish with glossy metallic texture effect; Tile Coat Emulsion (Roof Tiles): provides unmatched gloss and sheen with excellent protection against algae and fungus; Bright Ceiling Coat (Interior Ceilings): offers unmatched brightness to the ceilings with a smooth matt finish to enhance the brightness of the room; Floor Coat Emulsion (Driveways): s India’s first Floor Coat Paint that offers a glossy finish while also protecting the terrace floor, driveways, walkways and cement surfaces

- [Growth ambitions]: Indigo plans to grow revenues 5x to 3,000 cr in 5 years (by 2025 assuming washout FY21).

Financials

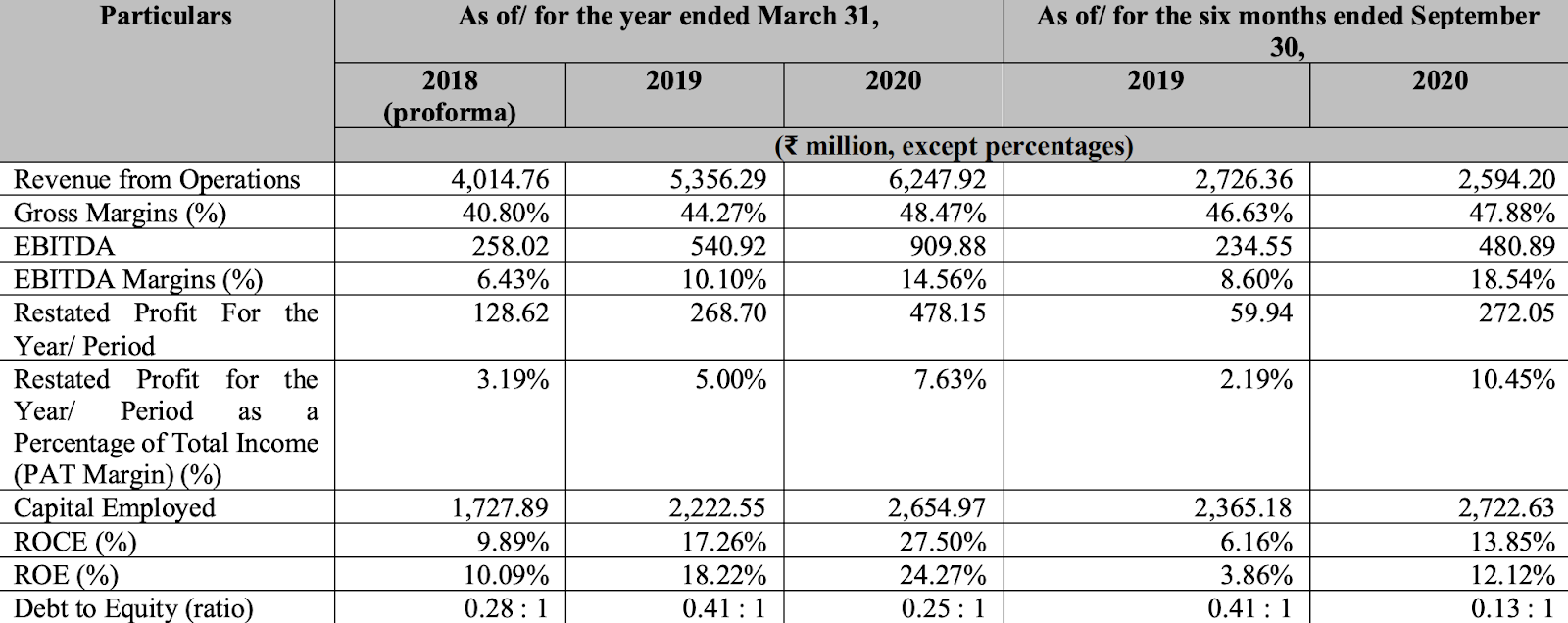

Some observations:

- Revenue is growing well.

- Gross margins are expanding as product mix changes.

- PAT margins are improving.

- ROCE is improving.

- Debt is being repaid, this will further expand PAT margins.

Barriers to Entry

- The Indian decorative paint industry presents significant entry barriers. These market entry barriers include the development of an extensive distribution network through relationships with dealers.

- The ability to set up tinting machines with dealers. Many dealers are unable to install a new company’s tinting machine mainly due to space constraints. As a result, most dealers tend to install tinting machines of only recognized players. The large number of SKUs and product ranges in emulsions renders installation of tinting machines imperative for timely distribution of different shades and products.

- Significant marketing costs and the establishment of a distinct brand to gain product acceptance

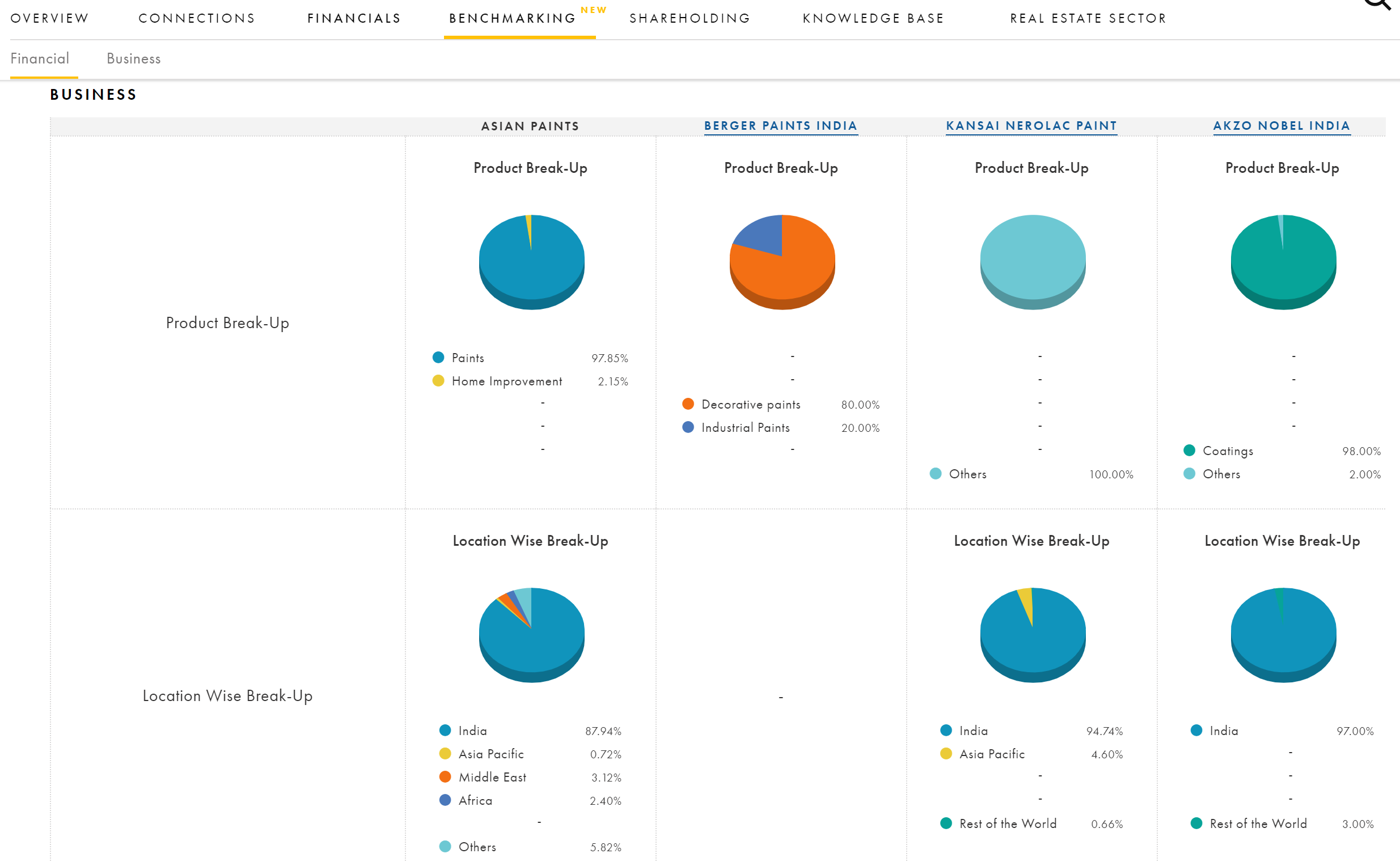

Industry Comparisons

- (Key costs): Raw material sourcing comprises more than 60% of the input costs of paint manufacturing. Around 300 to 400 ingredients are used in the manufacturing of decorative paints, of which, Titanium Dioxide (TiO2), a white pigment, constitutes around 20% to 25%. The paint industry has historically been successful in passing on any significant price increases in inputs to the customers

- (Global paint consumption trend):

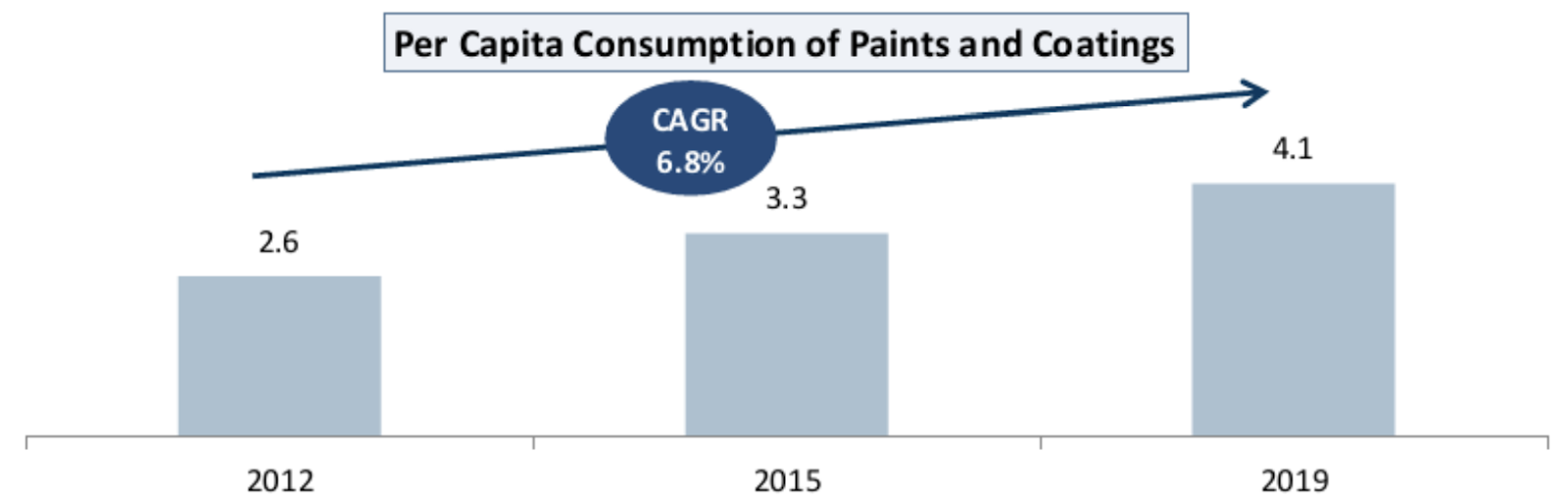

- (India Paint Consumption Growth): Compared to the global average consumption of approximately 14 kg to 15 kg per capita, the per capita consumption of paints and coatings in India is low, indicating a significant opportunity for market penetration in India.

- (Paints Sector): By end user, the sector is split into Industrial and Decorative paints. The decorative paint segment constitutes around 74% of the total paint sales. By technology, there are water soluble, solvent soluble and solid paints. Water soluble paints are 46% of market whereas solvent soluble are 48% of the market. Water soluble paints are higher quality and more eco friendly. Organized sector comprises 67% of the sector versus 33% for the unorganized sector.

- (Decorative paints market): There has been a higher growth of emulsion paints for interiors as compared to distempers, in line with an increase in the use of economy emulsions in place of lower-priced distempers. Seeking better products, consumers are also switching to marginally higher-priced emulsions with more durability and better-looking finishes in a wider range of colors

- (Fresh vs Repainting): As we can see, repainting drives most of the painting demand and painting cycles are also becoming shorter.

Competitive landscape

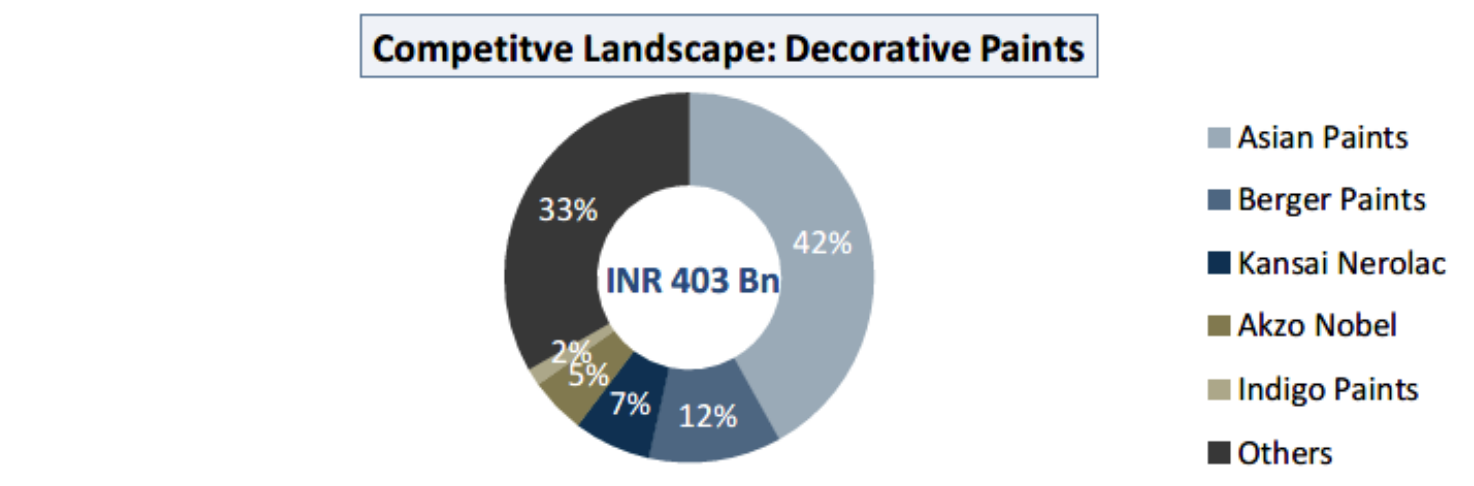

Unlike the major entities, Indigo Paints entered the market of small cities, towns and Rural Areas (Tier 3 – 4) and effectively established itself as a market leader in selected categories within a short period of time, and is now venturing 137 into metros and Tier 1 Cities. Indigo paints only has 2% of the market share. Which demonstrates the opportunity size.

- (Tinting Machine growth and penetration): Before 2000, machines used to cost approximately ₹ 1 million, due to being imported. With local manufacturing, the cost has decreased to ₹ 0.15 million, typically borne by the paint companies at least for Asian Paints and Berger Paints.

- (Manufacturing Capacities and growth): Indigo Paints is doubling capacities in last 2 years which demonstrates strong demand for their products.

- (Capacity Utilization): Due to aggressive capacity additions by Indigo Paints, their capacity utilizations are low, which is good since it leaves more room for growth.

- (Terms of Trade): The companies mainly focus on dealer margins with Asian Paints offering the lowest margins. Berger Paints provides the highest margins among the top four with almost 10% to 15% and up to 18% for specific dealers. Asian Paints and Berger Paints also provide direct cash discounts ranging between 3% to 5% to the dealers in case of early payments. Indigo offers a wide range of incentives to its dealers such as cash discounts, annual turnover rebate, long-term dealer loyalty program, among others.

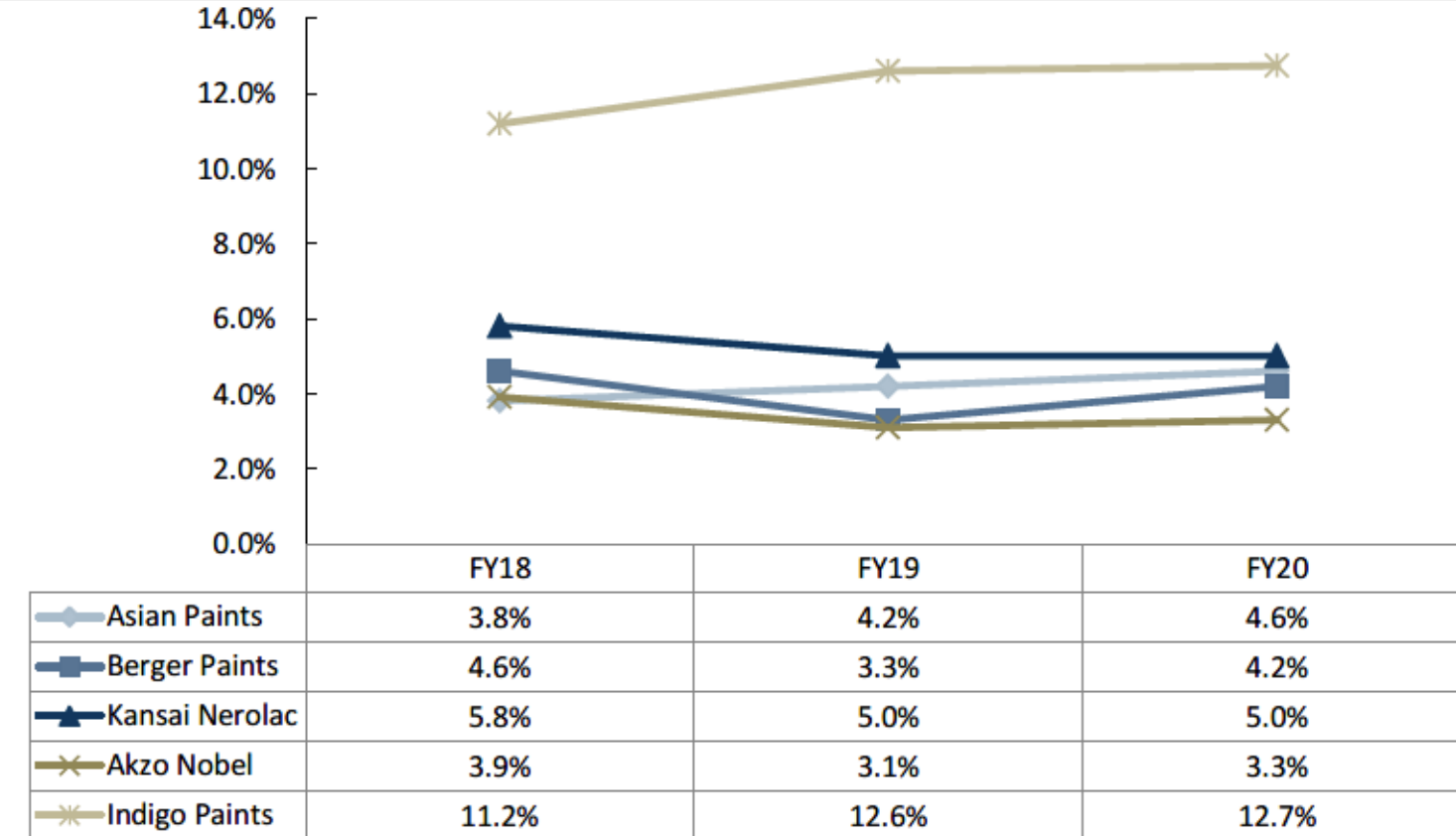

- (Marketing And Ad Campaigns): The paint companies have continuously invested in brand building through increased marketing and sales promotion expenditure.

- (Raw Ads Spends): We can see Indigo Paints spending on Brand building close to what other market leaders (Berger, Kansai Nerolac) are spending, despite being much smaller

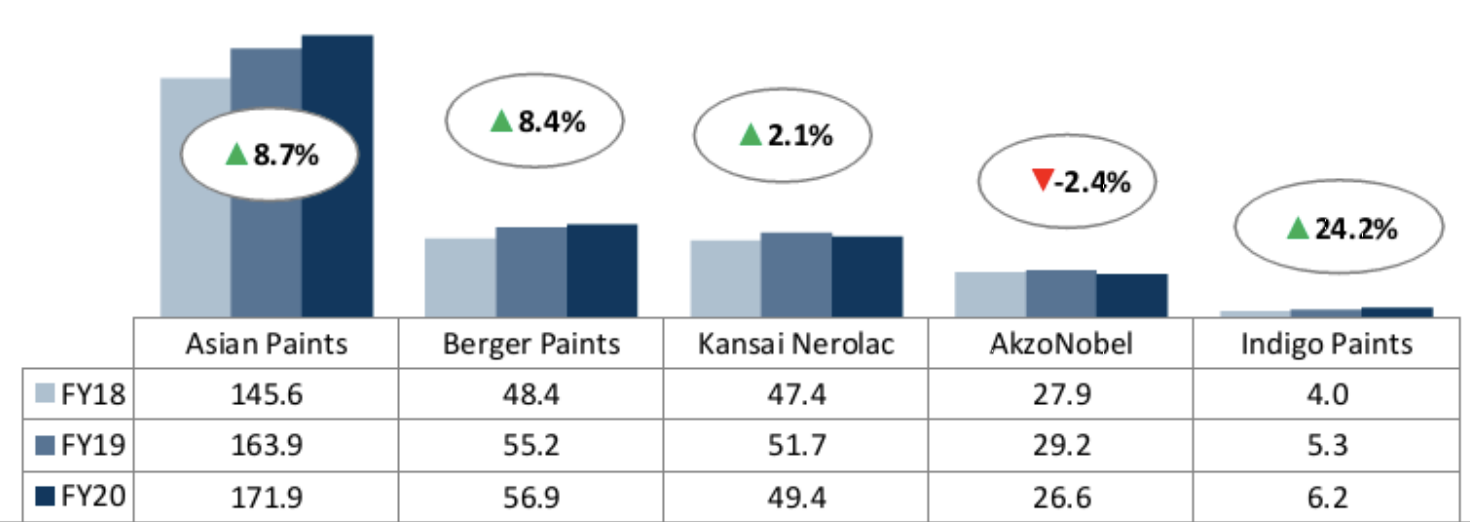

- (Revenue Growth): We can see Indigo being on a clear growth path (Revenue in Billions of Rupees)

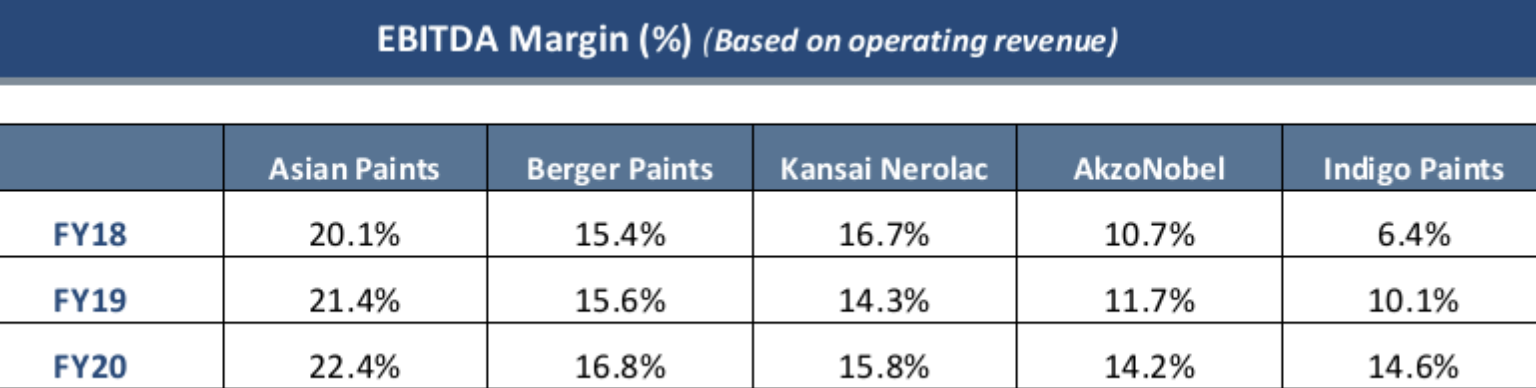

- (Gross, EBITDA & PAT margins): We can see that EBITDA margins for Indigo are at par with other market leaders although lower than Asian Paints. We can also see Gross margins improving over last 3 years as the product mix has changed. While the PAT margins are low right now, they are on the right trajectory and as they pay down debt, PAT margins would go up even more. Same with increasing capacity utilizations.

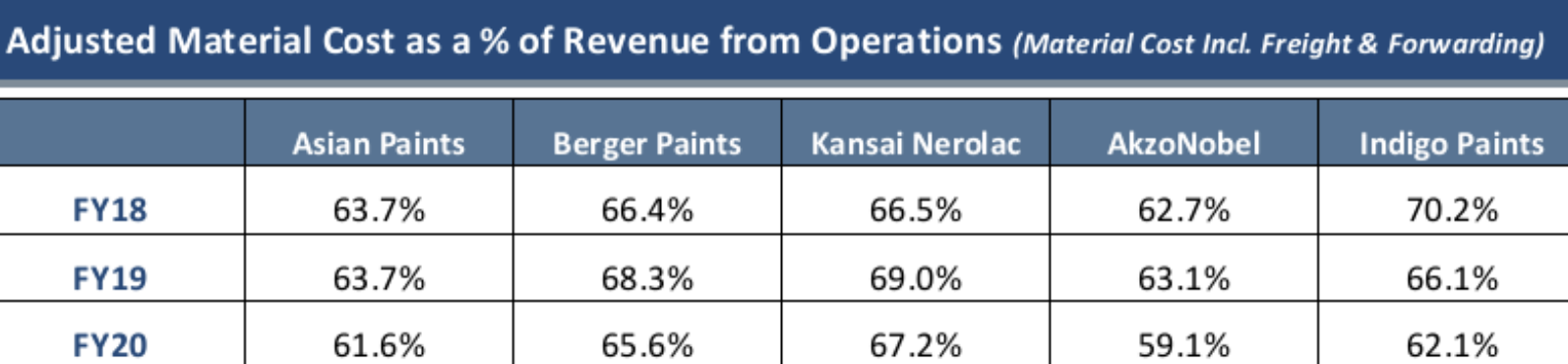

- (Materials Cost): The material cost (excluding the freight cost) as a percentage of operating revenue is the lowest for Indigo Paints as the company is closely located to the source of raw materials. However, this leads to Indigo Paints spending greater amounts on outward freight charges to deliver the products to the consumption centers. The outward freight charges for its peers are comparatively lower as their manufacturing facilities are located close to the consumption centers. On combining the material costs and freight and forwarding charges, Indigo Paints is effectively at par with its peers with the range being comparable to the industry leader – Asian Paints and lower than Berger Paints and Kansai Nerolac.

Valuation

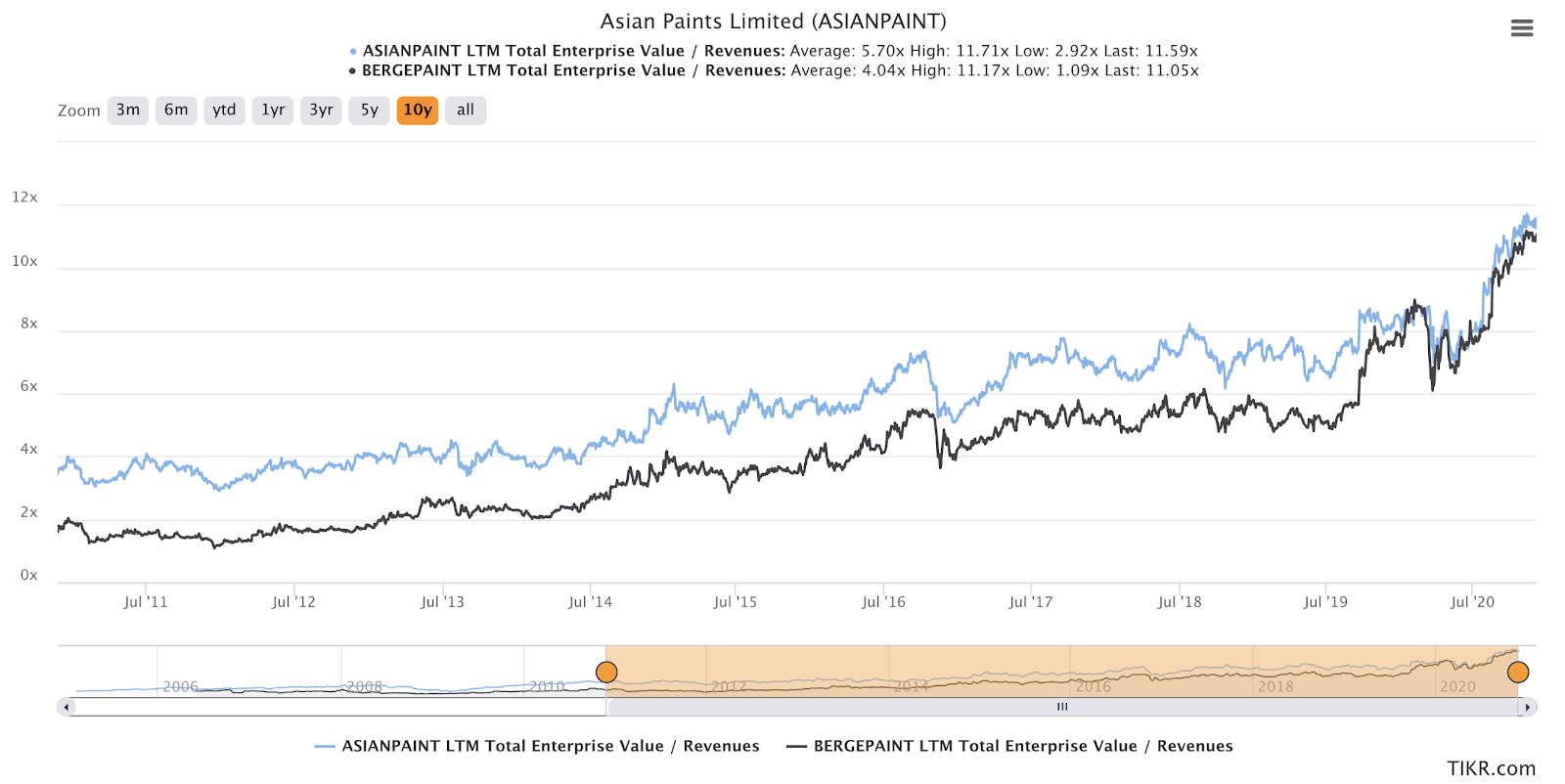

The IPO size is estimated to be 1,000cr as per the news. This includes 300cr of Fresh shares being issued by the company and also 700cr worth of existing shares (mostly belonging to Sequoia Capital) being sold. These are 5.8M shares. Pre-IPO there were 29M shares. This makes Indigo’s market cap to be 700*29/5.8+300 = 3800cr. With 19 cr of debt, EV is 3820 cr. At FY20 revenues of 620cr, it is available at EV/Sales of 6.16. We can see valuations of peers below:

The two market leaders are available at EV/sales of 11 and 12. Average EV/sales has been around 4-5. Relative to current peer valuations, Indigo is definitely undervalued. Relative to historic peer valuations, Indigo is marginally overvalued.

Risks

- An inability to protect, strengthen and enhance the existing brand could adversely affect the business prospects and financial performance. Retail Decorative paint business is based on brand recall and word of mouth recommendations.

- Engages in a highly competitive business and any failure to effectively compete could have a material adverse effect. Some of the competitors have larger business operations, are diversified with operations across India, have greater financial resources than Indigo does, have access to a cheaper cost of capital and may be able to produce paint more efficiently or invest larger amounts of capital into their businesses in terms of strengthening their brands, expanding their distribution networks and expending greater resources to populate tinting machines.

- Ability to grow the business depends on the relationships with dealers and the community of painters, and any adverse changes in these relationships, or their inability to enter into new relationships, could negatively affect the business and results of operations.

- On an absolute basis, valuations are very steep. Specially the P/E ratio is ~100. Entire industry has priced in decades of steady low double or high single digit growth with high terminal value. Any sector level disruption will impact Indigo’s ability to command premium valuations as well.

One para Investment Thesis

Indigo is the fifth largest paints manufacturing company with 2% market share. It is growing at quite a steady and fast pace, based on differentiated and innovative products (metallic emulsions, ceiling and floor paints, cement paints), high brand building & Ads spending, and differentiated business strategy: while top players started with metro cities and are now expanding to tier 3 and 4 towns, indigo has solidified their presence to some extent in smaller towns & villages and are now looking to expand to tier 1 and 2 cities. Company is able to successfully create demand for and sell their products, creating, expanding and utilizing larger manufacturing capacities (in fact all proceeds of Fresh IPO issue will go to capacity expansion). Given the very small size (2%) compared to opportunity size, high industry growth (10-13%) and reasonable valuations (6x EV/sales), Indigo is a reasonable investment candidate as per available information.

Next Steps

Some ways in which community can help is by scuttlbutting the nature of and pull of the end products. Are indigo paints of comparable quality to Asian Paints and Berger Paints? Are they available at attractive prices to Customers compared to other paints? How does Indigo treat their distributors?

Disc: Planning to invest in the IPO and possibly on listing depending on listing price.

Sources:

https://www.sebi.gov.in/filings/public-issues/nov-2020/indigo-paints-limited-drhp_48167.html