Thanks for the link but this post really seems more like a rant. Its incorrect to simply look at the pharma industry as one. I will try and give my perspective on Indian pharma.

During the recent downturn (starting in 2015), there were four large factors which impacted large generic companies.

- Consolidation of distributors into 3 main companies controlling more than 80% of US market resulting in loss of pricing power for large Indian pharma companies as most Indian companies do not have their own frontend

- Stricter FDA compliance with FDA setting up their offices in India. This was because more than 40% of drugs in US (by volume) come from India

- Implementation of GDUFA in 2012-13 with FDA’s focus on faster approvals to smaller generic companies to reduce generic drug pricing. This resulted in delays in approval for large generic pharma companies at the cost of smaller companies which were just getting into US. Net beneficiaries were smaller pharma companies like Alembic.

- The opioid crisis in US which took the sheen away from large acquisitions from Indian generic companies (eg: Lupin acquisition of GAVIS which made money by selling opioid drugs)

- The large generic pharma companies were trading at very rich valuations reflecting a lot of optimism

I divide Indian pharma companies into the following categories:

- Pure Generic companies: With faster ANDA approvals, the price erosion has increased to such an extent that the incremental ROE has gone below 10%. This is the cyclical aspect of the generic business and depends on the number of drugs going off-patent in a given year. The lowest cost producer and the most efficient player will win this battle. In the 2010s, companies like Lupin and Sun gained a lot by milking this market. Now, its Alembic and Ajanta Pharma winning this game because of their smaller exposure to US market. In a few years, Alembic and Ajanta will land up in a similar position as Sun/Lupin if they do not invest in their specialty drug pipeline.

- Specialty/hard-to-make drugs: The large companies (Sun/Lupin/Reddy) have invested a lot in this business. Returns are yet to come making it hard to estimate the ROCE of this business. On the face of it, it looks better than the pure generic business. Smaller companies like Natco feature here with them making most of their money from 1 to 2 specialty drugs.

-

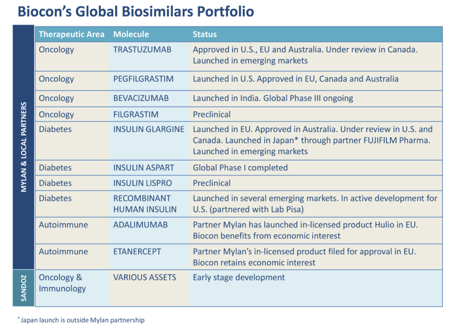

Biosimilars: There is only one company (Biocon) with a sizeable biosimilar pipeline. You can see their pipeline below (taken from FY19 AR). They have commercialized two molecules so far for the US market and EBITDA margins are >30% reflecting low price erosion. Lupin has a pipeline of 2 drugs (ethanercept, pegfilgrastim). Dr. Reddy has 2 drugs (pegfilgrastim, adalimumab), however Biocon has a time edge on both these drugs.

- API manufacturers: This is a scale business and the lowest cost manufacturer will always win. China is way ahead of India in this and is the lowest cost provider of bulk APIs. In the Indian context, Divis is the only Indian company with a large market share in certain APIs. There are other smaller players like Granules.

- Contract research: This is like the IT of the pharma sector where research is outsourced from innovator companies to India because of labor cost arbitrage. This is a reasonably predictable business with Syngene being the market leader. Other companies like Suven also get sizeable revenue from this segment.

- Indian pharma: This is a high ROCE business with limited growth prospects. Its mostly a branded drugs game, where branding gives pricing power to companies (eg: Zydus, Cadila, Sun, etc.). However every few years there is pressure from government to reduce drug prices (eg: categorizing drugs into National List of Essential Medicines). Large generic pharma companies like Sun, Lupin, Cipla now derive about a third of their revenue from this segment and use this cash to invest for growth in foreign markets. MNC companies also operate in this space. Its a reasonably predictable business.

I will love to get into more detailed discussion about the specialty/biosimilar pipelines of listed Indian companies as that can be a large value driver.

Some additional resources:

The thread on biocon is a treasure trove for learning about biosimilars (link)

Disclosure: Invested in Ajanta, Lupin, Natco, Divis, Biocon