I think RTM market was supposed to start from April 1. Do you know what happened to it?. IEX tried to start Green DAM but CERC didn’t approve it and they are now trying for Green TAM I believe. Up to the regulators now.

IEX updates on current situation

IEX ASSURES THE NATION OF 24X7 ACCESS TO FACILIATE UNINTERRUPTED POWER SUPPLY DURING INDIA’S HOUR OF NEED

In March’20, the electricity market at IEX saw a trade of 4,291 MU - the Day-Ahead Market (DAM) traded 3,971 MU during the month and saw 18% YoY growth while the Term Ahead Market (TAM) traded 320 MU and recorded 30% YoY growth. The southern distribution utilities continued preference for TAM contracts.

Several stakeholders have also been concerned about availability of 24*7 power at this point in time. According to IEX, there is ample electricity available on its platform. The average price for March is currently at INR Rs 2.49 per unit and average price since 22 March at INR 2.15 per unit. The company estimates that rates may continue to be on the lower side as the COVID situation unfolds.

Disclosure:invested

Amey,

RE generators are not allowed to sell on Exchanges?

IGX holding a webinar on 8th.

Register here: https://igxindia.com/webinar/

1 Like

RTM shifted to June due to COVID Issue. SCED is continuing. Ministry is coming out certain policies for freer selling of Power thru exchanges for Thermal power plants having Coal linkage with CIL at notified price. this should increase the volume in IEX though may take 3-4 months

1 Like

Hi Ankush

They are allowed to sell.

But, I understand that since one cannot distinguish if one bought coal power or RE power, the DSICOMs are not able to set-off against their renewable purchase obligations.

Plus, it is not easy to predict exact generation.

If planned Vs actual varies, then RE will have to pay a heavy penalty under the deviation settlement mechanism.

This could be more than the sale price of electricity.

So, we need a separate RE power market with different rules which IEX is trying to come out with in consultation with CERC

5 Likes

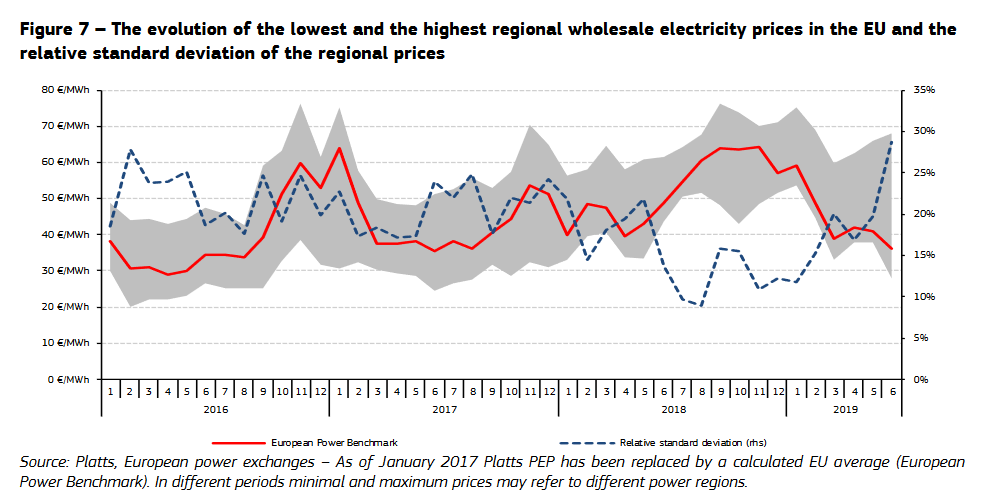

Hi all,

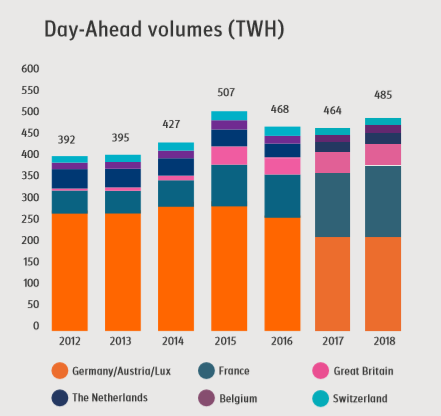

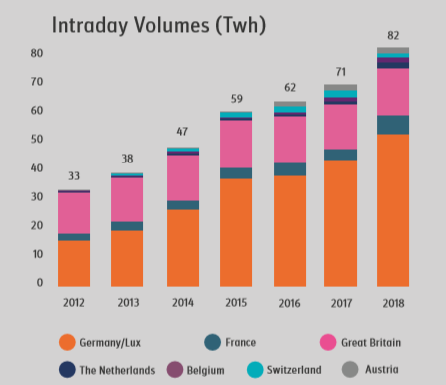

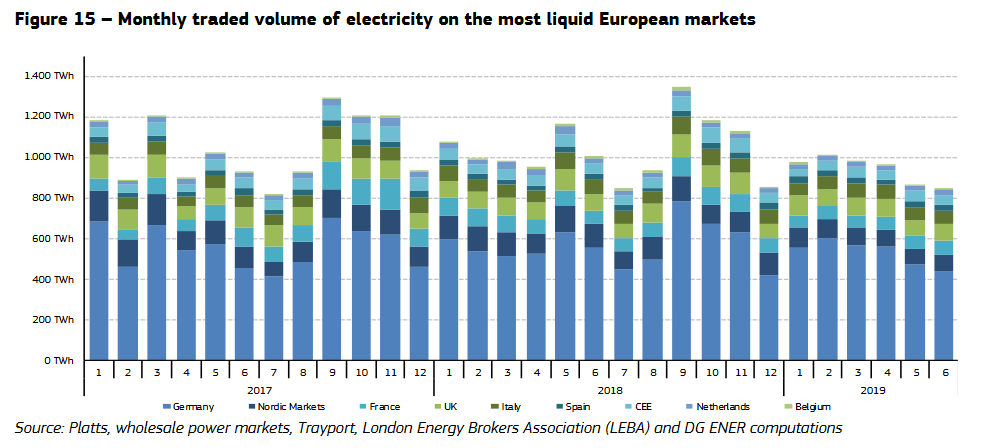

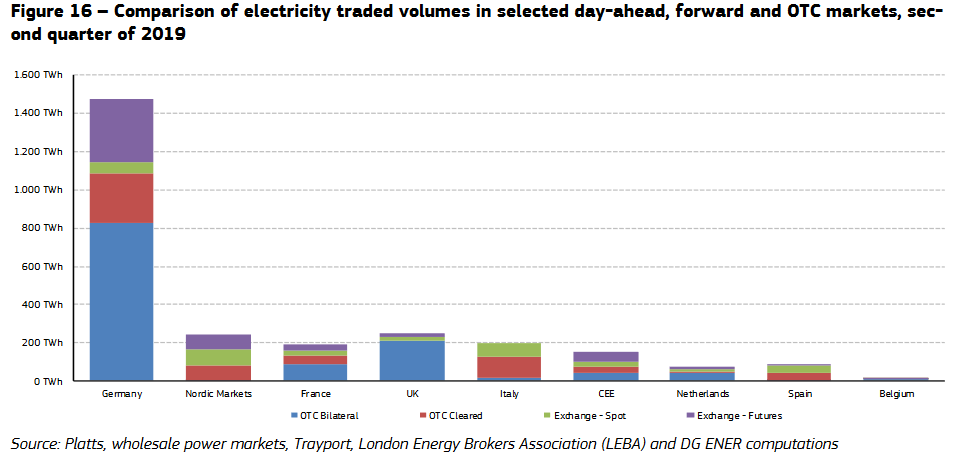

I have been studying the European Power trading scene for last couple of days and would like to share the details. I have mostly reviewed data from EPEX SPOT (part of EEX group) which runs power exchanges in 8 counties in Central and Western Europe and data from European commission. EPEX SPOT seems to be the biggest exchange in the countries they are operating. Firstly, let me admit that I have not read everything in detail and hence there might be some errors in my understanding. Also, I am attaching all the material incase anyone wants to take this further. The reason I was looking at European power exchanges is to see where we might be heading in terms of products from exchanges, opportunity size, growth etc.

The observations are as follows:

-

The growth in day ahead and intra day market for each country is highly non linear. Germany, which is the largest market for power trading has seen de-growth in day ahead and growth in intraday (cannibilisation?). The growth has come from France & UK, which has lower power trading as a whole of their respective market. As per EPEX , about 1/3rd energy supplied in these countries is though EPEX SPOT market.

In the same time from 2012 to 2019, growth in production of electricity in EU is almost NIL.

-

The volume bilateral contracts is still very high in all the countries.

-

There is considerable growth in renewable energy and de-growth in conventional power. Renewables are supported by PPAs.

-

There is a big difference in power trading market in EU. Germany, Austria, Lux have high amount of power procured through day ahead and intra day. Whereas, UK, France and central europe still has long term contracts. The reason is explained well in this report:

The historical challenge has been the move from the long-term bilateral contracts from before liberalisation to the current situation. This has been a long process with discussions between producers, authorities and consumers. The most successful developments have been where voluntary agreements could be found in a common interest to replace or adapt the contracts, as it was the case in the Nordics and Germany. In other countries the process has been long, and regulated prices to secure investments are still in place. This is the case for instance in France, to cover nuclear power plant investments, and in Britain, where the state owned companies were split by law to create competition.

- The physical exchange and financial market for electricity related derivatives go hand in hand. This explains it clearly:

The use of power exchanges gives the flexibility but also a volatility risk that can be difficult to handle, and therefore physical power exchanges are often developed together with financial power exchanges for risk management on i.e. annual financial power products. The financial market takes advantage of the opposite risk profile of producers and consumers in the power markets. Both producers and consumers want to reduce price volatility risk and the financial power exchanges gives transparency in the willingness to pay for reducing the risks.

- The volatility in prices is high even in stable EU market.

Conclusions:

- The growth will be highly dependent on the policy and regulation adopted by the govt. Also from DEEP launch we can see how easily it can capture the market.

- The bilateral market is here to stay.

- Derivative markets need to be developed for full benefit our power trading.

- The growth will come from the need to balance the market with increase in renewables (becasue of generation volatility)

- The volatility will not allow the DISCOMs to depend on power exchanges for major part of their need.

- Germany was able to renegotiate long term contracts to come to this stage. In India, it looks difficult to renegotiate long term PPAs without serious consequences.

Disclosure : Not invested. Still researching if to add.

Attachment:

https://data.europa.eu/euodp/en/data/dataset/european-electricity-market-reports

Epex_factsheet_190117_V2_0.pdf (1.0 MB)

european_experiences_power_markets.pdf (1.0 MB) quarterly_report_on_european_electricity_markets_q_2_2019_final.pdf (1.7 MB)

4 Likes

Presentation from latest webinar on IGX

IGX Webinar Presentation (03-04-20).pdf (1.5 MB)

3 Likes

A discussion on price discovery mechanisms in place for electricity markets.

DAM: Auction

TAM: Continous

Apart from numerous qualitative pros n cons, from a real long term fundamental perspective IEX’s past performance has been very good as far as profit-making abilities are concerned. This has reflected in an excellent return on equity for IEX for last few years :

After the uncertainties arising out of the Covid-19 crisis, this past performance in terms of operating efficiency & minimal leverage should keep long term investors keenly interested in IEX. Volume pick up & successful new product launches should also be the key aspects going forward .

1 Like

The business is sound and strong.

As far as stock is concerned, there is huge supply here as a lot of PE guys wants exit. Every time the stock goes towards old highs, someone come’s and sell.

hi All

IGX (Indian Gas Exchange) held a webinar on Wednesday explaining their business. Following are some of the points that were discussed -

- IGX would act only as an agent and would not be responsible for transmission or infrastructure.

- IGX is ready to go live in May 2020 if the lockdown ends. They have already conducted one mock trading session, and might conduct one more.

- There are strict up front margin rules with buyers depositing 115% of the purchase amount, while sellers depositing 15% margin so that IGX can honor defaults and act as a counter party guarantor.

- Contracts would strictly be spot and thus only those participants with access to infrastructure can participate. Further prices are quoted ex-hub and are on a take or leave basis.

- benefit to sellers - immediate T+3 payment against the current 20 days credit period.

- IMP - currently contracts for only RLNG would be traded on the exchange, not APM domestic gas.

- currently, 30% of NG trading in India is on spot basis. Co. looks to target 5% of total market to come to it. current market size is 1.677 mmscmd (need to recheck this figure)

- Apart from GAIL, co. did not mention any other seller as such. buyers could be industrials, hotels fertilisers cos. etc. with a minimum order size of 100 mmbtu.

- company is looking to charge INR 5 per MMBTU

trust this was helpful.

5 Likes

Presentation from recent webinar on RTM markets-

IEX Webinar RTM Markets (24-04-20).pdf (1.9 MB)

Could be a weird question but what exactly is stopping producers from listing their generation at 2 different exchanges?

Since IEX generates a clearing price, any producer above this price is at a risk of complete loss and since no generator is likely to know the exact clearing price, wont they end up selling power at all available exchanges to hedge their risk?

How does the exchange deal with this?

1 Like

I think most players are listed on both the exchanges IEX and PXIL.

It’s more about the liquidity; IEX has 99% market share in DAM which is the primary market. The DAM volumes of IEX in its first year of operations was more than what PXIL is doing now even after being operational for 10 years.

The reason why double sided closed auction is better for this kind of market is because if you keep continuous trading like in case of stocks wherein everyone can see the bid & asks. Everyone will just try to undercut each other by quoting lower/higher prices which will lead to suboptimal clearance of volumes.

A blind auction ensures that every participant bids/quotes their best price, which is usually their breakeven price. This ensures that the buyer/seller will alteast breakeven if not gain if their volume is cleared.

Also, exchanges have other products which are based on continuous trading method wherein a buy/seller can basically invite/ask for quotation for their volumes at a specific price.

1 Like

Thanks for the explanation but there’s still a doubt. In the double sided closed auction, lets say the discovered price/ clearing price is 3 rs/unit on IEX. A buyer X seeking to purchase 100 units needs to deposit 300 rs with the exchange, binding him to the contract. Is there a similar mechanism in place to bind the seller? Can the seller list the same electrical units on both IEX and PXIL at the same time? And if the clearing price at PXIL is 3.5 rs/unit, what’s stopping the seller from selling his entire supply at PXIL instead of at IEX?

Is there a clause in the contracts preventing this from happening?

1 Like

The following is my 2 cents.

The flow of electricity is via the grid. And for the grid to be stable the system operators enforce strict rules. The generators that inject electricity into the grid, the system operators, the exchanges, the National and Regional Load dispatch centers and the buyer - all are on same page as far the quantity that is being traded and the time block. Deviation from this either by the seller or the buyer will be penalized by the grid operators.

Therefore the seller can’t agree to sell the same units multiple times to different buyers. Such behavior would be penalized by the exchanges and the grid operators. (If traffic cops are strict, people follow rules more sincerely, right.)

The buyers and sellers need the grid more than the grid needs them and therefore discipline is maintained.

3 Likes

Sir, you need to understand that DAM is not like our stock trading window, wherein we put sell orders in both BSE & NSE and if it gets executed in one we will cancel the other.

Timing of both exchanges is the same, so as soon as order matching happens at end of the session, you might get execution in both the exchanges. But the amount of electricity that you have is fixed right. So will end up paying penalty for non-delivery like it happens in stocks.

Also, even if the price is little higher in PXIL, nobody wants to sell there because there is no liquidity. What good is a high price if you cant get an execution at that price.

IGX releasing monthly magazine on the Gas market.

Gas-Connect-IGX-April-2020.pdf (3.4 MB) Gas-Connect-IGX-May-2020.pdf (5.9 MB)

1 Like

Mohnish Pabrai latest shareholdings shows he has decreased 1.86% of IEX holding.