IEX earns 20paisa from both the buyer and seller, with an operating margin of approx 80% as per screener. Why isnt PXIL charging lower transaction charges, say 15p from each side to try and attract buyers and suppliers?

Does IEX’s platform provide the ease/convenience/features that are actually worth 10-20% of the tota value of transaction? (IEX earns 40 paisa per transaction, so assuming per unit cost is 2-4rs, it’s “commission” would be 10-20% of total transaction value)

If IEX truly does offer these features, what’s stopping PXIL from copying these?

2 paise, not 20 paise.

2 Likes

point still stands. they’re operating at 80% margins. could PXIL offer the same service at 1.5 paisa? margins would go down to 70% or so in that case… why hasnt PXIL been able to do this?

Go to post no. 58 on this thread.

The first mover is always the winner in the Exchange & Auctions Businesses. Buyers will flock to where the sellers are. Take eBay for example, no one has been able to displace them over 20+ years of e-commerce. Take Sotheby’s & Christies for example when it comes to Auctions, they have been around for 300+ years. First mover is the winner!

The only exception I have seen to this, is BSE losing out to NSE. BSE appears just lost their way when it comes to competition in the equity segment.

Btw…BSE has also either obtained or applied for license from CERC for power trading.

1 Like

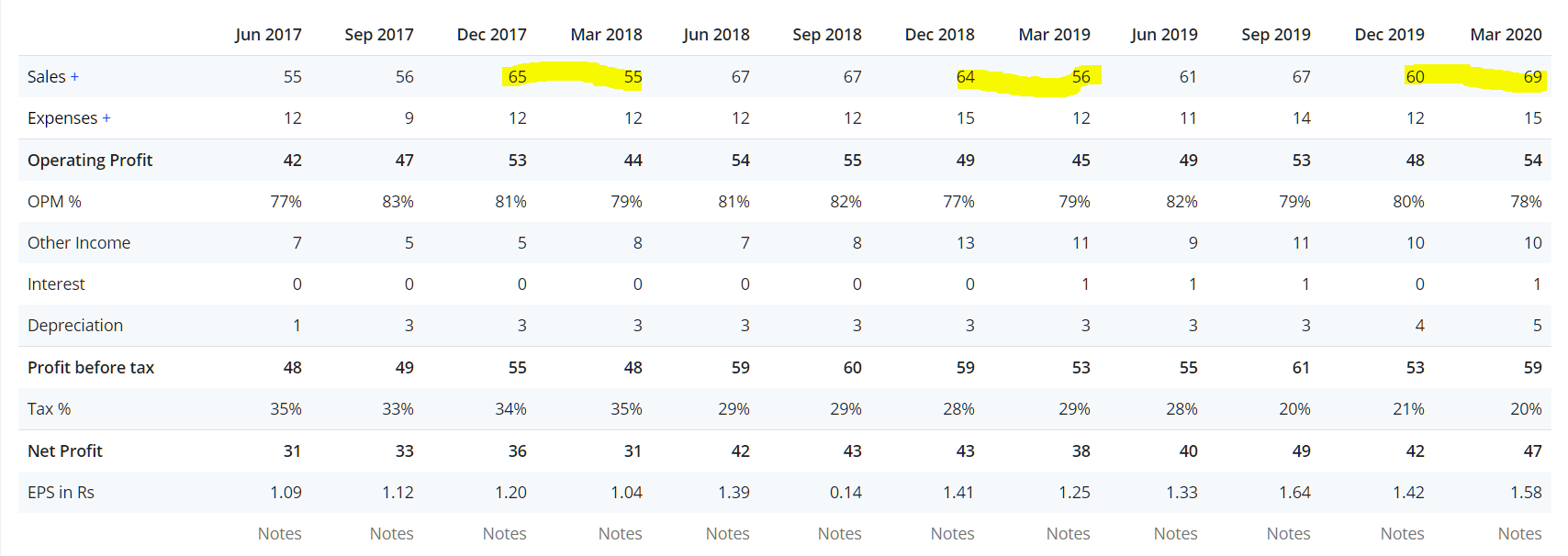

Results are out and the numbers look very good - 23% growth in topline and 23% growth in bottomline.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/118f58f8-6c33-426e-8c37-ead9e0987f2c.pdf

Looking back at the last few years’ numbers, looks like March is generally a weak quarter QoQ but this time the numbers are better.

Is there anything to be read here?

Update: The company just came out with a presentation. This might explain the jump in a seasonally weak quarter.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/642af8d4-4cc4-47ae-a560-597c967cd5ff.pdf

1 Like

FY2020 - Consolidated Results and observations to look out :

PBT: 225 v/s 231 cr FY19.

Employee benefits up by ~33% to 33 cr from 24cr where total operating income has been flat YoY at 297 cr.

FY18 was also at 24 cr.

Cash flow from operations declined to 175 crores majorly due to a spike in other financial liab which mainly comprises Deposits towards settlement guarantee fund. Taking that factor out, CFO also remains at the same level.

69 crores was allotted for buyback at Rs. 185/share(last price:155) which seems expensive at current market conditions and valuations. We will need to wait to hear management’s opinion on such policies going forward.

Q3 to Q4 revenues have spiralled upwards of 9% and compared to FY19Q4, they stand north of 12%.

Employee expenses have gone up this quarter by 25% compared to q3 and almost 50% from fy19q4.

Salary & Bonus includes a major portion of employee expenses which was at 21 cr out of 24 in fy19. MD & CFO were getting around 2.8 cr. (2+0.8).

There were 126 employees as on March 31, 2019, avg salary being at 15 lakhs/an.

2 Likes

Major contributor to IEX’s revenue is volume of electricity transaction on the platform, which in my view is factor of two things, one is obviously overall electricity demand and other is the price attractiveness of IEX as compared to others (PPA and Direct buying). Price at IEX has been at all time low for some time (Average Monthly Market Clearing Price is less than Rs 3 from September 2019)

| DAM | 2018 | 2019 | 2020 | |||

|---|---|---|---|---|---|---|

| Month | Volume (in MU) | Average MCP | Volume (in MU) | Average MCP | Volume (in MU) | Average MCP |

| Jan | 3382 | 3.2 | 3281 | 3.33 | 4791 | 2.86 |

| Feb | 3316 | 3.23 | 2794 | 3.08 | 4289 | 2.91 |

| Mar | 4.02 | 3356 | 3.12 | 3971 | 2.46 | |

| Apr | 4055 | 3.98 | 4005 | 3.22 | 3692 | 2.42 |

| May | 4916 | 4.67 | 3722 | 3.34 | ||

| Jun | 4965 | 3.73 | 4207 | 3.32 | ||

| Jul | 4028 | 3.46 | 4800 | 3.38 | ||

| Aug | 3976 | 3.34 | 4675 | 3.32 | ||

| Sep | 5725 | 4.69 | 3488 | 2.77 | ||

| Oct | 6505 | 5.94 | 3391 | 2.71 | ||

| Nov | 3404 | 3.59 | 3389 | 2.85 | ||

| Dec | 3059 | 3.3 | 4333 | 2.93 | ||

| Total | 40632 | 45441 |

As price remains lower than Rs 3, the incentive for open access customers (industries) to buy from exchange is higher.

In short, seasonality matters, but price of electricity at exchange is crux. In my opinion, the price should remain at this level for some time in future, due to higher supply as compared to demand of electricity.

4 Likes

I believe this the key reason why exchange volumes are up

There was similar article I read related to MSEDC (Maharashtra) … Not able to get link now.

This could be potential “JIO” moment for state electricity boards and they might get habituated on relying more power exchanges for cheaper and flexible electricity.

IEX also claims the same reason on how exchanges are adding value

Next few quarters would be interesting to see if this trend could be maintained or seasonality or old habits prevail

1 Like

Detailed presentation is available in this tweet. Hope it will be useful to the community.

1 Like

Anybody has access to the Elara capital coverage report on IEX ?

Possible future opportunity for IEX with opening up of commercial mining.

Management Concall- Coal India

2 Likes

there are some developments happening on storage of electricity in solar/ wind projects. Isnt this disruptive for power exchanges or its too far fetched ?

It is very expensive and hard to store bulk electrical energy…It is possible to store energy to run a car not a Plant. Future may change not in near term 5yrs…

Real-time power trading may lead to large savings for discoms

Is this going to be game changer for IEX ? Experts out there please comment on it.

1 Like

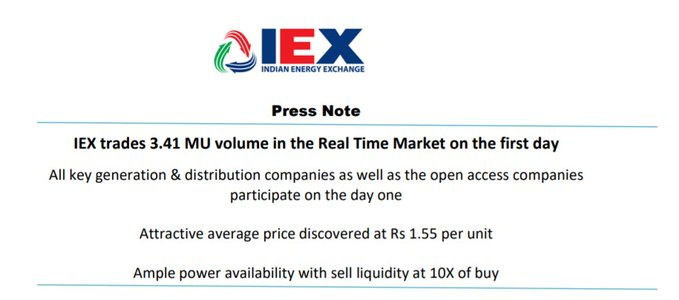

It seems that the power generators are under liquidity stress as the price discovered in the recently launched real-time power trading market was at Rs. 1.55/unit with prices going down to Rs. 0.10/unit at one point in time. This contrasts with an average settlement price of 2.42/unit in the month of April. Anyway, IEX seems to be off on a strong footing in the real-time power trading market.

IEX RTM saw 3.41 million units traded on 1st day itself.

Current DAM volumes are averaging 150-180 million units daily. So this adds another ~2% to growth

Multiple levers for the company in terms of new products, IGX itself is a Rs160-180 crores opportunity.

1 Like

Q4FY20 CCT Notes

Financials, Volumes, Other Metrics

40% Q4 yoy Volume growth, from 9.9 BUs to 13.84 BUs. Price declined by 14% in Q4. OAC volume went up by 41%. FY20 volume growth of 3.2% from 52.2 to 53.9 BUs. Lack of sell side inventory in RECs. Revenue growth of 1%, PAT up by 6% and PAT margin at 59%.

Power Industry

Total installed capacity increase 4%, 12% increase in renewable and 2% in thermal.

We know that COVID-19 has thrown up a huge range of challenges, but more than that we see ourselves as steering on the range of opportunities for the power sector. Clearly life is not easy. We will need to assess every single element of the electricity value chain, generation, transmission, distribution, the structure around that and networks, we will have to assess which business models delivered in the electricity business. Clearly an overemphasis on a 25-year long term rigid contracts may or may not be the most useful way forward and there has to be a certain amount of work done on that topic as well. Strategic involvement of financial institutions, how does the whole funding mechanism work between the financing institutions, the generating companies, the distribution companies and the transmission companies and regulatory environment, which is working right now or trying to make sure that things become streamlined. Operational efficiencies which is reducing the losses in transmission and distribution are just few steps which will help us to accomplish the objective of power for all on a 24/7 basis in a very sustainable way and in a very cost effective way. Collectively, we would need to find out a way out of these issues and we are working very strongly with all the stakeholders and the Ministry of Power and the Regulatory Commissions to play our part, very strong part. We need to bring in more efficiency and flexibility in terms of structure, operations, financials into the system and that is a key priority. Cost of power needs to be optimized for industry as well as at homes. With the Make in India program, that needs to really take shape for both getting self-reliant and also for generating a huge amount of employment into the country, will happen and will be facilitated on the back of power being optimized for the industry as well as at homes and then we need huge amount of efficiency in the whole network and the value chain because India has set itself on a path of rapid growth for the foreseeable future. In my opinion, this is a perfect time to make some very fundamental progressive shifts and also because most of the world has already solved for these issues, there is no reason for us to not solve them for ourselves in a very nice and a very progressive way. We believe the sector will require a lot more automation and solutions that enable all of these elements of transformation and that we are standing at the forefront to deliver around the solutions that the industry requires right now. The technology driven energy markets will have a very key role to play to enable this transformation.

COVID Update

During the lockdown period, power procurement by distribution utilities is some southern, western, northern states such as Andhra Pradesh, Telengana, Tamil Nadu, Maharashtra, Gujarat, UP, Bihar, Punjab, and few others has increased because there is ample power availability on the exchange with extremely attractive prices, which is helping the utilities make significant savings in the procurement cost and several utilities have shared their success stories on how much they have been able to optimize on cost through exchange led procurements in the media, so that has been a good story so far.

Regulations

Additionally, on the policy and regulatory front, the Ministry of Power recently issued the Draft Electricity Bill, 2020 with a focus on (a) abolishing of cross subsidy charges & cost reflective tariffs (b) sub-licensing/franchise of distribution areas © a separate authority to adjudicate PPA obligations to augment capacity of the Appellate Tribunal (d) promotion of renewable energy (e) allowance of cross border trade of electricity (f) payment security mechanism.

Demand Supply Mix

Q4 is a peculiar quarter when you do not have high demand in most part of the country. So if you are following demand pattern, normally you see high demand coming in Q2 particularly in the later part of Q2 and early part of Q3 and Q4 we see demand start to pickup only in the month of March. So the pattern that we observed in Q4 was we were, our volume growth in Q4 was about 40% and 34% of the total volume came from open access and there was tremendous growth in the open access buyer as well. So there are couple of things which happened on the sell side. There was participation from distribution companies as many states who were surplus during those three months, they were selling very aggressively, prices were low and since the prices were low, there was huge participation coming from open access side also. So I would say on the buyer side it is state participation and also open access, state participation was little limited because there are few states where they have good demand in Q4 and on the sell side mix was very healthy, there was IIP participation close to about 40% to 45% and states were also selling and their overall sell was little above 50%. So that is how mix was.

So year on year basis, the open access when we started last year in the month of April, open access contribution was just 20% of the total buy, but gradually it started to build up, there were some favorable regulatory orders which came couple of them, particularly one from Gujarat, also there was so much consumer addition happened from Tamil Nadu. So it started to change from start of Q2 and up to end of Q4, it was almost 35% of our total buy. Distribution company buyer pattern is dependent on their procurement cycle, their agriculture season largely. So we see participation coming from northern state in Q2 and Q3 and then in Q4 there were very few states where you had high demand like Telangana, AP, then some demand came from Rajasthan, MP also hds good demand during those times. So it keeps on changing. It varies from time to time, but on an average, this is for the last year 30% from open access and 70% from Distribution Company.

So to answer first one, which was essentially around two big states, Maharashtra and Gujarat, so as we know Maharashtra is the biggest consumer in the country today and Gujarat is also number three or number four, so what we are seeing is Gujarat, your question was about balance between open access and discom buy. So this is undoubtedly a state where there is an absolutely no deficit so in fact if I recall correctly Gujarat was one state which declared it as a surplus state about five to six years back and if you see their participation at exchange, in terms of distribution company buy they are in top three most of the years and in terms of open access buy also they are in top three. So this is one state where industries as well as distribution company themselves, they are super-commercially sensitive, they do not want to leave any opportunity of doing optimization on any cost. They are making money by selling surplus power which is not the case with most of the distribution companies in the country. So, in terms of overall balance, open access and discom, on both sides their participation is very high. On the other hand, Maharashtra, their participation at exchange is extremely high in fact if you ask me in the last two months, they were most proactive and they in fact did a lot of replacement and saved Rs.100 Crores by doing that. But open access buy, they are not so active. The charges in the state, open access charges, which is additional surcharge and other surcharge are on the higher side and then they are giving subsidies also in some parts of the state, so we do not see participation coming from there as well. So open access that is little limited but as a state they have been very proactive in doing replacement and coming to exchange as and when there is an opportunity to save on the cost.

On the total buyer side, above 30% was done by open access consumers and 70% was done by Distribution Company.

RTM

Introduced on 1st June 2020. Fully ready for it. DSM - 20-22 BUs should shift to RTM. In a couple of years we estimate majority of it to shift. We expect DISCOMs to optimizing their cost through RTM. They have become very cost sensitive. Charges will be 4 Paisa.

In touch with all DISCOMs, most of them are fully prepared to participate in RTM. No impact of COVID as of now. today all of them have installed our software on their platform and they are doing it, that is one part. Second is we are also helping them in creating capacity to ensure that they are in a position to optimally utilize this new platform. See there are two parts of it as I earlier explained, one is meeting your deficit, which is a very simple thing because you are so near to real time, you will immediately calculate what sort of deficit is there and you can place your bet. Large part of volume we are expecting from optimization as well. So we have created a tool which we have shared with couple of Discoms now and in next one week time we are reaching out to all of them and there is so much excitement in distribution companies. This is one of the game changing market models that they are looking at and particularly all those states where there is high renewable, they are also very, very excited about it because this gives them another opportunity to address the variability in generation that they see, which is a great problem for them on account of high variable charges in their particular state. So I would not say everybody is ready but I think 85% of the states are directly dealing with us and creating capacity to participate on this platform immediately.

We are seeing major enquires coming from all the states who are rich in renewables. So, states like Tamil Nadu, Gujarat, and Maharashtra, AP, and Telangana. These are some of the states but yes there are some more states who are heavily overdrawing from grid where their DSM bill is very very high. These states are Odisha and then UP, Bihar also in some of the months the rate is very high. These are seven, eight big states and they also contribute to almost 60-70% of the total consumption in the country. So, all big states we expect them to come to our platform to make use of this new platform.

LDC - Long Duration

50 BUs in banking and bilateral transactions in country today. 20 BUs is direct bilateral and 30 BUs is banking transactions. This is the total potential, it will take time to convert. Charges should be similar to RTM but it is a bit far and not finalized yet.

Petition - This is in the Supreme Court. All litigants want the disposal of that petition as of yesterday. Everybody wants to get on with doing something more active and meaningful versus trying to chase a petition. Unfortunately, right now you understand it as much as I do, there are ton of very significant and very important litigations which Supreme Court is dealing with, the matters of great, great national importance Supreme Court is dealing with and also they are taking cases only which are extremely priority case. So the hearing which was meant to happen on May 7, 2020 has been deferred to July 8, 2020. What the CERC, the regulator and the Ministry of Power have done, they have sort the opinion of the Solicitor General of India, day before yesterday whether they can move on this without Supreme Court disposing off the petitions. So you can just see the urgency in the ministry from all sides, to make this happen and our view is it will happen very very soon. So there is nothing which is holding it up, it is just inline, it is a procedural thing that is stuck with the Supreme Court otherwise every party engaged and involved wants to make it a reality because it will help not only the market, it will help a lot of customers as well just because it optimizes everyone.

IGX

Manikaran Power also a member of IEX became 1st member of IGX. Added 6 more members and 75 clients. No derivatives on the gas exchange currently.

Thanks for asking that question, let me give a bit of preamble about what the intent of the government is and where the country is headed. The country is very rapidly moving towards everything possible to do with the clean sources of energy, and gas falls in that bracket. So the stated objective of the government has been, shift the adoption of gas in the overall energy mix, from a 6% point of today to 15% points over the next couple of years and that is 2.5 times shift of today in a growing market because gas economy is growing. So gas is going to be finding a lot, lot more favor as part of shift of energy mix and clean energy desire of the government that is one and you know gas is produced in multiple location in the country, whether it is western India or it is south eastern India and southern India or in those zones, we would be trying to play in all of those areas. Just to get you a flavor of numbers, the spot market of gas already is about 30% today. So of all the gas that is getting it is about 30% today and we will aspire to be a couple of percentage points on that spot market.

The gas exchange technology comes from a company in UK called as GMEX Technologies, they are one of the leading pioneers in gas technology business across the world and they are helping us to develop. It is not revenue share. We are buying it out right. So, it will have not an impact in the subsequent years. On the manpower cost, we are building the business. So, we will obviously keep adding head count to the gas business as we go forward. Right now the head count was very small, we have to get rest of the operational infrastructure in place, which is what we have got now and we have got a few business, and that is the place where we will hire the most to make sure we get more business, we are getting more strategic people and we are getting more operational people in the business.

OAC

So in fact throughout the last year we have seen many favorable orders and in fact as I said 20% increased to 34% and overall volume was also very good in Q4. So many orders came and most of them were favorable, but you are right, every year in the month of March and April we get to see new tariff orders and in new tariff order, you have new tariff, new cross subsidies are charged, new additions are charged. All these elements which are important for any open access consumer to source power from exchange, there is some change in that. So we are in middle of May, we have seen many of these orders and none of these order which came in the month of March and April except for one there has been any increase in the open access charges. So in fact before the lockdown, our mix was very healthy, the open access was, it is ever increasing. So what started from last year Q1, it attained very good high in Q4 and when we started this year it was low because of lockdown, but we have not seen any adverse order so far.

Renewables

For the green market, we expect the launch to happen sometime in Q2. We are awaiting for issue of the regulations from CERC and we are getting extremely positive feedback on the whole requirement of the green market, very keen interest from participants who have surplus high energy available say like Tamil Nadu for instance and also the recent change in the transmission regulation, which puts exchange and power with the intrastate transmissions on equal footing, so that is one thing which is helping us. From a sizing perspective, we won’t provide the guidance, but the whole green trading should become a reality over the course. This is a very positive thing from green perspective.

Cross Border

On cross border we are awaiting final regulations from the Ministry of Power. There is a huge amount of work required, the regulations are drafted and there is a bit of back and forth because they wanted some clarification and because it is cross border, Abhishek, it needs a bit of a vetting by the Ministry of Commerce as well. So, between Ministry of Power and Ministry of Commerce in my opinion they are working together, it is almost at the last leg and we should hear of it very very soon.

COVID Response

A lot, COVID is just going to force us to change. A lot of companies have changed, you will see us also getting a huge amount of change on account of COVID. The manner in which you engage and interact with the customers is going to change. So the customers who used to come in to your office and dealing with you or you used to be going to their office and dealing with the customers and showing them a few things, I think that needs to change and that has a very profound impact on what we do. If the customers are not going to be engaging with you physically in your premises or our premises, then our tech has to step-up to make sure that you are able to handle customers remotely in an extremely seamless way and in a very user friendly manner. So that is one big change and I talked to you about how IEX is taking this whole point up so we are getting whatever is possible, doing whatever is possible to make sure that our infrastructure is absolutely pretty much the best in class in the world and from a tech perspective and counting because tech has no boundaries and we want to make sure that that our infrastructure or technology is the best in the world. That is one thing that we are very very keen in terms of doing. So that is external aspect. The second is internal aspect is about our own employees, we are going to make sure that safety and health of our employees are managed but you also realized that when you do a huge amount work from home, there is a need to engage with your employees in a very different manner. The social aspect is missing right now, but we want to make sure that whatever we can do, to engage with the employees is then absolutely in a good way. We are carrying out many such activities including training of people including fun and games with them including all kinds of regular webinar and engagement outreach so that our employees are motivated and employees are taken care of and we continue to do regular engagement with them. The third thing which is beyond employee engagement is a huge range of new products that we need to have because post COVID world will make it almost imperative for customers to start to come back and demand different kinds of features and functionalities, which you believe will be absolutely a right thing to do from their perspective, but it make sense for us to make sure that we are providing that. So that would be the other thing that our investment and product development people, new product initiatives has to do that much notch higher. So there has got to be a very strong pillar in the company now on innovation and innovation around creating new products, developing new products which makes sense for the customers. Earlier we did a broad based release of new products, sort of releases which really makes sense for our range of customers, but for a whole range of customers that strategy has got to change, instead of trying to sell yourself across the broad range of customers, only one or a few require a new feature, functionality or product, we have to be agile enough and sharp enough to make sure we are providing them. So, there is a bit of innovation angle which is coming in. There is an external angle of customer user interface and customer sensitivity or making sure that you can deal with them remotely in a secure manner, very user friendly manner, there is an element of internal technology, there is an element of new product innovation and new product development and the fourth element is element of employee engagement. We are very focused across each four dimensions to make sure that our company is reorienting itself to make the best of this scenario. In the other way, I mean we know in the industry, there will be liquidity challenge and there will be a liquidity crunch and so how can we help to step up that, that is part of my regular business because what we do is we provide energy at the cheapest cost in the most flexible manner. So people want to buy through us at the shortest duration of time, today, tomorrow whenever they want over the course of next 11 days. So, their financial distress can be relieved right now, through exchange because a lot of customers or a lot of states are doing replacement buying right now. They are putting to sleep their costly generation and they are coming to the exchange and by virtue of that they are saving money and I can tell you one discom in south, saved 60 Crores by doing such a thing with the exchange for the month of April. That is a great story. So those are the things in which the financial liquidity that we are helping with. And our communication had also stepped up. We are engaging a lot more from a communication perspective, written communication with our customers and our partners to let them know what is happening with exchange on a daily basis. So exposing them to liquidity availability, exposing them to saving that they can get through buying on exchange and the price trend because it is at all time low and I am just assuring this that do not worry, whatever and whenever you require, IEX is standing behind you absolutely solidly to give you anything that you need. Okay so long answer but there are about five or six dimensions on which we believe post COVID will happen.

5 Likes