NTPC does sell URS at IEX right?

1 Like

yes after SCED been implemented, i think its very low. Actually i wanted to mention about the 15% unallocated power from all NTPC and other ISGS plants to be traded through DAM. My error.

Hi Folks — Any updates on the natural gas trading license/set up that the management was talking about? Also, do you guys see any impact of commercialization of mining on power generation?

Hi Bozo_investor,

I like the way you put it " If dams were considered temples of modern India (as said by Nehru), the SEBs are its largest gutters, draining India of infinite man hours and resources…"

2 Likes

Gas exchange is a few years in the future.

Changing the law, getting all the enabling regulations in place (after extensive stakeholders consultations) and forming the rules of business is a very time consuming process (years)

And after start of operations, it will take a few years to generate any meaningful revenue.

Gas exchange is a good thing that IEX is trying, however that cannot be a part of valuation/investment thesis.

3 Likes

It does, but the DISCOM can make a recall within 1 hour.

With the introduction of real-time market on the power exchanges, NTPC and other generators will be in a position to trade the URS (un-requisitioned surplus) on the power exchanges.

(Read about the concept of gate closure introduced in RTM regulations)

Introduction of CTT like tax will not be a concern for IEX.

Only buyers and sellers transact on IEX

Speculators are not allowed.

Even of electricity futures are introduced, only the actual sellers/buyers may be restricted to IEX. (regulated by CERC)

Speculative activity may be traded on MCX or some other exchange regulated by SEBI.

In such a case, introduction of a small STT/CTT type tax will not have any impact on IEX volumes

2 Likes

Hello Amey,

My understanding is that RTM market will be market for every 30mins in form of two15min blocks and gate closure for each 30min period will be 1 hour prior.

Is this understanding correct?

And how will this RTM be different from current intraday market?

Thanks

Anyone here gone through the Smartkarma article on IEX by Nitin Mangal? There has been few questions raised on receivables and payables. Smartkarma doesn’t seem to allow retail investors to subscribe for their content, so don’t have much idea what this is all about.

1 Like

Your answers will be in this document

http://www.cercind.gov.in/2019/regulation/1.%20Statement%20of%20Reasons_RTM_12_12_2019.pdf

RTM will make a difference.

Both India Electricity Grid Code and Open Access regulations have been modified to enable RTM market.

DSM (Deviation Settlement Mechanism) power which is not traded/market power, but rather “balancing power” will migrate to the RTM Market

Also, order matching mechanism is different for RTM market and current intra-day market. Price discovery is different.

2 Likes

Quarterly result updates Q3 FY 2020

- Electricity volume traded: 12,472 MU. QoQ 14% down, YoY 9% down. Mainly due to two bad months October and November. Electricity consumption declined by 13% in October and by 4% in November. It has recovered post that (0.4% decline in December).

- Total revenue: 69 Cr. 12% down QoQ and 10% down YoY.

- EBITDA margin - 82% level. Same for last year and recent quarter.

- PAT - 42 Cr, QoQ 15% down and 2% down YoY.

- Average market clearing price was Rs 2.83 Per unit. 34% lower YoY. Due to attractive price, power procurement by open access consumer increased by 64%.

- TAM volume has surged by 47% during due to increasing use of TAM by Discoms. This shows interest of Discoms in longer term contracts within short term market.

- The question which I am puzzled about is, if Discoms are buying, Open access use is increasing, TAM market grew, liquidity is superb and hence price is attractive, why did the volume de-grow? Subdued demand from core sector has some impact. Extended monsoon had caused subdued demand from Agricultural and Industrial sector. but i believe it was also due to higher base of last year October month. There was a record level of electricity trade, 6505 MU of DAM and 620 MU of TAM in October last year despite higher price last year. Average MCP of Rs 5.94 in Oct 2018 as compared to Rs 2.71 of Oct 2019. The power prices and volume remained on the higher side in Oct 2018 due to high demand of power from Western, Eastern and Southern States as well as supply side constraints such as coal shortages, reduced hydro and wind generation affecting the market. So, it seems as liquidity have flooded the market and hence base demand met. So discoms is not buying base demand from market.

- Company is expecting announced pre-paid smart meter in budget to be good for sector.

- Market has high sell side bids as compared to buy sides and hence prices are down quite significantly from last year.

- Company expects liquidity to be in the similar range due to recent government interventions. One of them is Generators not having PPA, can buy coal and sell power on exchange now. Expecting its execution to happen soon.

- RTM should start trading from 1st April 2020. Trial being executed by NLDC, SLDC and others in February and March. Company is getting encouraging response from customers about RTM.

- Cross border trade is in its final phase of regulatory clearance. But no fixed timelines till now. Something Similar was said for Longer term duration contract.

- Company started making investment related to Gas exchange. But no clear cut regulation has been decided. Making preparations early to catch it as and when it happens.

- In REC segments, company has brought down incentives given earlier. Slightly increasing bottom lines, not much effect.

- Real difference between RTM and Intra-day TAM is in the nature of auctions. TAM is based on continuous matching of bids, which maps to a one to one transaction. Due to that price discovery is not very effective. RTM would be similar to DAM, which is double sided closed auction, which means that several buyers and sellers are competing for the same volume and best price is picked in that time slot. So, price discovery should be better on RTM as compared to Intra-day TAM. Apart from that, current intra-day TAM requires bidding to be done 3 hours in advance, which would come to 1 hours in case of RTM.

- Open access contributed 38% in Q3 as compared to 22% last year for Q3. 30% for 9 months FY 2020.

- Company’s strategy

1. Increasing customer base: Sales team reaching to Discoms and Open access consumers. They are also tweaking some of their products for easier access and integration by end-customers.

2. Ensuring High liquidity and hence better prices.

As prices are pretty low and if demand re-covers, we may see a significant increased in volumes of exchange in recent quarters. Volume in January has increased by good number.

2 Likes

Energy exchanges are relatively new to India with liberalization in regulations allowed to take its course only in the last decade and a half. And with 98% market share, Indian Energy Exchange does provide a structural long term growth opportunity. Although there would always be some short term hiccups every now and then due to uncertainties on environmental or macroeconomic fronts, such as recent fall in quarterly earnings can be attributed to the prolonged monsoon & subdued economic growth as rightly pointed out by one of the fellow boarders :

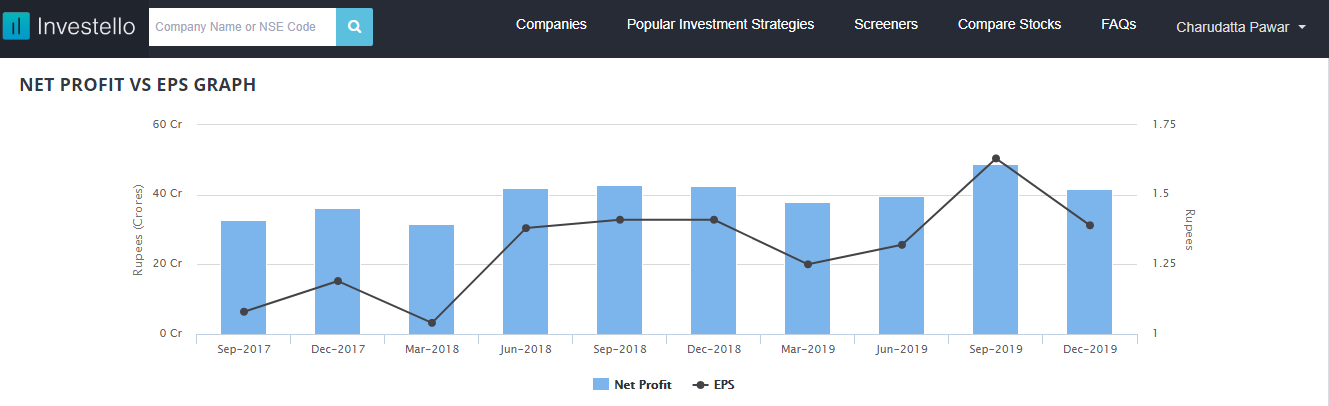

But when we consider past track record from an investor’s perspective what’s more enticing is the consistency maintained by Indian Energy Exchange in the growth of its topline as well as of net profits. The following chart should enunciate that the company was able to maintain healthy profit margins during all those years of revenue growth :

However, given the complexities on the regularity front, it would be noteworthy to see that if these earnings can be sustainable over the long term or not. The recent significant slowdown in the economy has probably taken a toll on stock price as a result of declining volume growth and weak power demand in India. But few of the points which can underpin the argument in favor of Indian Energy Exchange to justify its potential for attaining a structural long term growth can be enlisted as follows :

#Growth potential for IEX should come from power demand growth in India with its GDP to grow at 6-7% in the coming decade or so. Technically demand growth should be more than the GDP growth due to relatively low power consumption per capita India has had over the years.

#Some of the government initiatives (such as UDAY & other schemes) has helped state discoms to narrow their losses in recent yers & the trend should continue due to dropping AT&C losses and the procurement of cheaper power from short-term markets like exchanges.

#IEX gain from the reluctance of discoms to signing new long term PPAs with new gencos due to their financial positions & availability of cheaper prices on the exchange markets.

#Going forward, gencos will look to completely switch to short term sources such as Indian Energy Exchange to meet the seasonal variation in demand.

#India has been aggressive in its plans to add renewable energy to fulfill its energy needs. Currently renewables is about 20% of the current capacity and about 10% of the power consumed.Though these renewable energy capacities are tied with long-term contracts, they will free up existing thermal capacities contracted by the state discoms and cause supply fluctuations which will benefit the volumes on the exchange.

#India has been phasing out thermal gencos(most of which are under PPA) which are over 25 years old. This pursuit will lead to decommissioning of a huge capacity . Discoms will most likely look to replace this demand from the short-term market, a definite gain for exchanges like IEX.

2 Likes

- is it possible to see more than 10% growth in any of exchange businesses over long run?

- If we look at similar business track record, All the opportunity theories have not worked out so far (BSE, MCX etc.)

- Plus always the regulatory risk - evolving and changing

1 Like

This is encouraging.

Government is thinking for reforms. This step will be massive, will pave the wave for deepening of power markets and a significant increase in volumes traded on power exchanges in the next 3 years

1 Like

Q3FY20 CCT Notes:

Clearing Price 2.83 34% down yoy. Management says attractive for buyers.

MOP has finalized allocation of coal for sale of power in the ST market. Will enable coal linkage for plants without PPAs and increase supply in the exchanges with decreased input costs for generators.

Standalone Revenue down 9.8% yoy, PAT flat with PAT margin at 61% against 56% last year.

Consolidated revenue down 9.7% yoy, PAT was down 2.2%.

RTM - 1st April Onwards. Will get updates on LT and cross border at the end of Q4. Cannot share gas launch date.

RTM will be a double sided closed auction, trading in 15,30 min. blocks. Delivery in 1 hr. Intraday is 3 hrs in advance. RTM is similar to DAM. Intraday is a matching concept, you place the best bid and matching is done with multiple buyers and sellers.

99% MS in DAM but in TAM 60% MS. TAM is a one to one transaction and competition exists. The way the day ahead market works is on closed auctions which involves all the players bidding in the system and TAM survives on one-to-one. Closed auctions and one to one matching differs in the way in which transactions come, the way the liquidity is available on the exchange and the way the prices are optimized, and that works best in the day ahead market and that is the reason why you will find that world over the DAM market is really the market usually every player is trying to get market share of.

Yes, so is it okay to assume that once the long-term contacts are in place the market share would be similar to that of TAM and not DAM?

Tough one to answer because you will have to figure out what discovery mechanisms discover prices, what kind of sales outreach you will build and I can only tell you one thing, we are extremely conscious of that and making sure that our engine continues to improve and get more optimized, our sales outreach continuously become stronger all the time and so that is how we are going to play. We would love to believe that we will continue the way we are continuing.

I wanted to confirm one data point on the regulations which came in after the intraday norms were approved by CERC. When I am looking at one of the provisions it says that the allocation of transmission corridor between the power exchanges for real time transactions will be in the ratio of their shares in the DAM market. So that means that you will get the lion’s share even in the intraday market?

Yes, for real time market this is the provision and we will get lion’s share transmission capacity

Exactly, RTM because the model of price discovery is also same so liquidity will play important role in RTM market and second is the transmission capacity allocation is in favor of those who already have share in their market.

Competition

One thing is good that they have launched this, and you heard me talk about our views on competition in every single call over the last three quarters since I have been here. We really need more competition in our space because more competition allows companies to work to develop the market which is always going to be healthy for all of us here. So, I really want PXIL to ramp up and whoever else wants to should ramp up. To your point whether they are getting more volumes or not I think that really depends upon a couple of other things. One, on the fundamental design of the whole engine and mechanism of trading, two, the user experience that customers get out of us versus anybody else, three, the manner in which our teams are in touch with the customers across country, the familiarity in the way in which we enable trade and we do an end-to-end settlement so I think there is goodness to our end-to-end mechanism right now which is helping and the fact that PXIL is launching tells us one very good thing that they see the market from a very buoyant perspective just the way we believe it will be over the next couple of years. So, in that buoyant market more people coming in, is an absolutely great thing but like I said you must play to the fundamentals of exchange.

Volume Trends

Sir I want to understand what exactly has gone wrong in this quarter because on one hand you said electricity consumption is down by 6% but then, we are down 9% in terms of volume and then in your press release you have said that there are some states which have got double digit growth, then somewhere you have said that the industrial customers have got a 64% increase, so what exactly went wrong for us to have such a dismal performance on the volume side?

First of all, if you have been tracking the electricity market there is a very close relationship between drop and recovery both sides on IEX volumes, while the electricity market has not recovered in the month of December and is down about 0.4% points year-on-year but the electricity peak demand goes up 4.8% you see the exchange performing 53 points better but when the electricity market is down like 13 points in the month of October it was a significant drop year-onyear. In the month of October, a couple of things happened, one across two big types of customers that we have, we have agriculture and we have commercial and industrial customers. The industrial activity in October was very down, you see the IIP numbers for the month of October being extremely low and the core sector per se whether it is coal or fertilizers or refinery or electricity or steel everybody was down in the month of October significantly. So, the industrial activity was one part of the whole story. The other thing that happened in October was that we had a very serious change in the weather pattern. Climate activity in the month of October or monsoon activity in the month of October was very high and this year was a delayed withdrawal of the monsoon. So, when we have delayed withdrawals of monsoon then the agriculture consumers do not buy enough electricity and hydro is very active then. So, both of our two most potential sectors segment, C&I as well as the agriculture customers had reduced dependence and reduced requirement of electricity. Now you are seeing the recovery bounce back much faster in the months of December and January and that is also because hydro is no longer an option right now because it has gone down and the industrial activity happens to be coming back on track. The IIP was positive in November and some other core sectors are becoming much positive in December and that is the reason you are seeing the electricity demand go up across specifically in the month of January, electricity has gone up by 2.5% points. So, there are some factors which are in the larger alignment with the economy, GDP and IIP and some factors which are again in the domain of climate change that is happening. Now, the way we are trying to buffer ourselves is on two fronts. One is clearly what is the exchange doing? One thing we are doing is we are spanning our offerings to more customers to make sure that whenever there is a demand, we are there to fulfill that demand. The fact that there is liquidity on the exchange allows for the prices to be lower. The government has announced two other things. One, all plants that are beyond the emission control norms will have to be phased out and shut down, so that will require more electricity to be provided to some other resources and that demand should get fulfilled on the exchange and the second thing is provisioning of Coal to Commercial Power Plants and you will find that the price on the exchange will continue to be competitive and attractive to open access consumers across the country. So, one activity is very clear: Go across to as many distribution companies and as many open access consumers through our sales efforts and convert those customers for buying on the exchange, hat is one thing. The second thing which is our effort again is making sure that the new products that we are launching, like Cross Border or Real Time Market or Longer Duration Contract, those should also get launched but we are also tweaking new products and engaging with our distribution and open access customers to customize products from their requirement perspective. So, we are expanding our portfolio. Expansion of portfolio allows us to serve the same customers in a deeper way and allows us to find new customers. So those are the two things that we are doing. It is a longish thing, electricity per se is subject to a huge shift in vagaries and that is what has happened over the course of this last quarter. That is the reason I said fiscal Q3 or calendar Q4 was a tail of three different months for us.

OAC

The open access right now is 38% in our overall mix. It has gone up. If you see last year it was 22%, it has gone up to about 38% right now and open access is one which has grown significantly, it grew 64% points in Q3 versus the same period last year. Open access is a good story. The proposition that we have been taking very strongly to the government is open access which allows customers across industries which consume more than one megawatt of installed capacity to buy cheap power from the exchange. Now that is a great thing because it allows their input cost to reduce but a lot of states impose open access charges and some other subsidies on open access consumers and that deters them from buying that makes all value proposition of exchanges uncompetitive. The reason for an increase in open access despite all of the charges in Q3 was because the prices were very stable and low and as long as we continue to see such kind of prices on the exchange, you will find that the open access consumers will continue to find favor with the exchange. The good thing is that our engagement with the ministry and with other ministers of power and the regulatory bodies already suggest that we are focused on this problem, we are focused on making sure that industry becomes competitive and one of the factors in industry becoming competitive is reduction of open access cross subsidy so that the power becomes cheaper which again is going to be really helpful for the exchange

In a way what you are suggesting is the conflict of interest from a SEB perspective to actually lose their most profitable customers is probably the limiting aspect even now?

Yes. What you are saying is the way it is understood right now but let me give you a proposition. Assuming power is about 20% points of input cost to any product manufacturer. It is more in cases of some industries like metal industry, it is less in case of some other industries which are knowledge or service industries, but on an average, it is in the range of 15%. Now assuming the power cost can be reduced by 20% points at least through the exchange. Now in this manner about 4% points of their combination of input cost of power and consumption of power purchase can add about 4% points to the bottom line if you do the math’s right. So that 4% points really adds 1% to the corporate taxes (assuming a 25% tax slab). Now that is like a wonderful proposition and is one of many different ways I think the country can to step up to find very solutions to the whole DISCOM distress problem and this in our opinion is one of the more brilliant solutions that the industry can get, in this game everybody gains. There is not a single loser because 4% points you add to the bottom-line and you use that for corporate tax and the gain on the four points on the bottom line is used for capacity expansion, for job creation, and every problem that we are going through and trying to solve for today. So there are various means and ways we can solve today and that is the reason I said at one level your question is a very straightforward one but the solutions are unique and different and I think all of us need to step up and find those unique solutions.

LT Markets

Just to understand longer duration contract which we will have, will be designed like the day ahead contract or term ahead contract?

what happens in longer duration contract, you cannot have matching. In fact, if you see our weekly contract that we have today, there is open auction which happens. So, we are looking at it from every direction, in fact we are thinking of contracts which would be in similar lines to DEEP tender that is there today. We are also working towards creating standardized contracts which would be like our weekly contract. So, in none of the cases, it would be matching. It could be auction, it could be reverse auction, or it could be open auction, both may be done.

Sir, my question is with respect to the longer duration contract. Sir, if you could help us understand some of the contract specifications in terms of what sort of upfront margin would you be looking for and how will the payments cycle go?

As far as payment cycle goes, we are going to create a product where we are going to give comfort to both buyer as well as sellers. This is what exchange is known for. So, when you are doing long duration contracts through exchange, we would be absorbing counterparty risks which means that as a seller, you will get paid. So what we are doing in case of our weekly transactions where settlement is done on daily basis, similarly we are going to adopt for longer duration contracts where we will have some BGs and LCs in place which will take care of guarantees and then every day the power that is being traded will be settled. So, this is what we are thinking. To answer your second question about transaction margins that is still under consideration. We will be taking call in due course of time.

TAM vs DAM

on the TAM market, we do not see any industrial consumers coming there and in the weekly markets given the prices are so low, you freeze a price for ten days at least, why are people buying in the day ahead market, why do not they come in the TAM market, is there some issue there?

Normally, if you see, TAM market prices are higher than day ahead market. So whether it is a weekly trade or it is a daily trade, normally the prices are on the higher side. Second is, we have seen some participation of open access consumers in the past. All those consumers who are availing 100% open access which means that they do not have an option to fall back on distribution companies, they are coming and participating in the TAM market. If the consumer is availing partial open access, which means that whenever there is increase in demand, he is eligible to buy from a distribution company, they are not participating here.

Okay. Can you indicate how the prices are in the TAM market versus the DAM market say DAM is around Rs.3, what would be the TAM market?

There would be some premium. So, if you are going for weekly trade, people will take reference of day ahead market and then there would be some 10, 15, 20 paisa premium over that in the weekly market. Similarly, in daily also again they would command some premium depending on the day of delivery whether it is weekly or weekend. Considering all those factors normally there is something else over the day ahead market.

Volume Growth Guidance

Q3 was a 9% drop on volumes and they picked up in December, they have picked up in January, so hopefully in these couple of months which are left for rest of the year we will continue to see a similar momentum as we are right now. We are going to calibrate our next year very soon and let me explain as to why I say this. There are many new contracts that we are trying to launch now which can have a very significant impact. So that is the new market that we are trying to create. We are in the process of assessing the sizing and our capability to how much of the market we can capture and that is the reason we are little cagey in trying to tell you right now about how the next year can look like. But those are new products which we are extremely enthusiastic and encouraged by, and it will open up new markets for us. we are sizing it up and we are sizing it up across the country in every state and it is a fairly complicated exercise and so we are sizing up on business plan for next year and we will get back to you shortly.

Volume Revival in Dec, Jan

Like I said couple of things changed, clearly, one link to the climate like I said, the Hydro-generation has gone down very clearly. Second the fact that the liquidity on the exchange is better because coal allocation is better, the prices of coal has gone down, both domestic as well as imported. When the coal price has gone down which is the input price has gone down, the output electricity cost is lower and whenever the cost is lower on the exchange it is beneficial because then people can see the discovered price on the exchange being too low and all the open access as well as the DISCOMs can come and buy and DISCOMs can replace their more costly generating stations through the cheaper power on exchange and you are seeing all of this play out. The other thing which happened is that there is a pickup in activity in December and January. In January, we have seen some of the core sectors come back like fertilizer, refineries, steel, coal, all these four core IIP sectors have come back to a reasonable level of activity in the month of January. So, both, the climate which is helping us and the prices of coal and the liquidity, the prices being low on the exchange that allows people to buy more on the exchange and the demand going up. So, both of those are helping us here.

Affect of Peak Demand on Volumes

The peak demand is a demand at a point, and that demand happens to be the highest demand. Now, when peak demand happens then there is an imbalance between generation and demand, so there is an imbalance between what is being generated and in that location. The electricity market runs highly localized assuming there is demand which are high up anytime in Tamil Nadu and generation is not in Tamil Nadu they would buy from somewhere and exchange becomes more logical place. So the more the mismatch it is better you will find that the exchange fundamentals will play out and get highest benefit of those demands.

Changes to Block Bidding Mechanism

Sir my second question is, believe you have got an approval for some new block bids which is the minimum quantity and the profile one, could you throw some light on that and how does that help us in the DAM market?

Yes. What happens is today we have a block bidding mechanism where either all is selected, or none is selected. So, it is complete selection or 100% rejection. So, what we are saying is now with the new bid type, if you want to buy a 50 MW and you place minimum bid quantity as 5 MW which means if minimum 5 is selected, it will be cleared. So this is what this first thing is all about. Second is considering the requirement of RE market and also conventional market where they want to bid for complete profile which means that let us take example of solar, right from 9 to 5, every hour generation would be different. So, you can create one block where the quantity in every time block would be different and then this would be considered as one block. At present it is not there and now the approval has come, we are going to introduce in week to ten days’ time. This is going to help us increase the cleared volume. So certain quantity gets rejected today, that rejection quantity will come down.

IEX vs DEEP

With regards to the DEEP versus IEX price parity, that seems to be narrowing over the last few quarters and you in fact generate some data with regards to how there is some gap and why it is beneficial for executing the contracts on IEX, apart from the usual counterparty benefits that we get, is there any other reason why participant would use IEX over DEEP?

See counterparty benefit is a huge benefit. So, if you are following DEEP market, you will find that the price varies with the states DISCOMs. Some DISCOMs in Southern region when they are going for bidding, price discovered is Rs. 5.20 paisa. For some other DISCOMs it is same, generators are willing to supply us at Rs. 3.60 paisa. So that difference is there because they are not confident that they would be able to recover money from exchequer or the past trend this payment is getting delayed for over a year also in certain cases. So, we feel that the value that we bring to the table, has many takers. In fact, we already have discussions with most of these distribution companies, we have shared our contracts with them, and people are waiting keenly for that.

Transmission Capacity Helps OAC

If you have seen with more transmission line coming in, we have got huge network today i.e more than 80 megawatts of inter-regional capacity is there, and congestion is virtually zero. So, 99.5% of the time, we have one nation, one grid, one price which means that wherever there is a customer, this power can be generated somewhere else and can be transported to that particular place. This infrastructure was not there three to four years back but in the last two to three years, we have seen that we are very comfortable as far as the transmission infrastructure is concerned and it is helping in taking the market forward.

MISC

Tax is at 21% because of treasury operations.

PXIL has relaunched their DAM platform.

–

Relevant notes from MCX Q3FY20 CCT for competing products:

Gas & Electricity Products

Now on the new products, electricity futures, again the matter is between the regulators before Supreme Court. Supreme Court has to pass the consent terms and then approve the order, then the rest of the regulatory work will start on the electricity futures. Then comes the gas spot market and there is a lot of, I would not use the word noise but there is a lot of excitement I would say around the spot gas project but then without GST being sorted out without gas grid is being segregated or hived off I do not think these things will happen soon. So, let us see because our job or objective is to keep ourselves geared up to seize any opportunities that comes in our way and we will not miss any opportunity.

11 Likes

Indian energy exchange might have better result in this coming quarter. Total volume traded during Jan, Feb, March 2019 was 9863 MU and Volume traded in Jan and Feb 2020 itself is 9577. Average price at Rs 2.91.

2 Likes

@amey153 can you tell what happens in case a discom is unable to pay/defaults on payment? the exchange takes on the risk of payment to gencos, so in case of default, it could be a crippling risk right?

3 Likes

Hi Priyank

Sorry for the late reply

The exchange does not take the payment risk

They have an elaborate process of margin requirements and other mechanisms to ensure that payment default does not happen on either side.

It is very similar to a stock market - NSE/BSE

The clearing mechanism takes care of the payment defaults without the exchange having to pay from its pocket.

6 Likes

Result of bad policy

When “must-run” status of RE projects means HUGE losses for DISCOMs, they will find innovative ways to avoid payments

The electricity sector keeps getting into deeper troubles without anyone having the bandhwidth/capability to suggest & implement simple solutions.

Allow all these generators to sell electricity on the power exchanges if the DISCOMs don’t want their power.

This will need modification of India Electricity Grid Code (IEGC) and introduction of Real-time markets (RTM) at the earliest.

2 Likes