Bulk deal between AGRI POWER AND ENGINEERING SOLUTIONS PRIVATE LIMITED and AMANSA HOLDINGS PRIVATE LIMITED.

| Deal Date | Client Name | Deal Type | Quantity | Price | % of total share |

|---|---|---|---|---|---|

| 13 Sep 2019 | AGRI POWER AND ENGINEERING SOLUTIONS PRIVATE LIMITED | S | 9378396 | 115.30 | 1.89% |

| 13 Sep 2019 | AMANSA HOLDINGS PRIVATE LIMITED | P | 10941482 | 115.18 | 3.6% |

AGRI POWER AND ENGINEERING SOLUTIONS PRIVATE LIMITED earlier held 4.99% stake at company. Did this cause price to fall by approx 9% (from Rs 130 to 118) on Friday?

The opportunities in exchange market for electricity is abound like latest CERC draft regulations for Real Time Market, Market based economic dispatch, cross border trade esp with Bhutan, Nepal etc and India will move slowly away from long term PPA to market based power procurement. Apart from this, there are REC and now GOI will introduce HPO and therefore DISCOMs can trade on HECs too(Hydro Energy Certificates). But all these opportunities takes very long time to materialize since the whole chain in the electricity market is regulated and controlled by the Government. The traded volume has again come back to 120-130 MUs every day in DAM market. This volume will only fetch the similar kind of revenues and there may not be much growth in the IEX. There are no new products other than TAM and DAM. CERC and Govt has to break the shackles to bring more products into the market. There is long pending case in SC where CERC and SEBI were fighting to control who decides on the forward markets. Therefore In exchange we cannot buy electricity for more than 11 days, like say 3 months or 3 years. Settlement was an issue. Now i understand this case may come to an settlement where physical delivery will be done in the exchange by CERC and financial settlements will still be under SEBI. This is pending for the last 8 years or so.

CERC though quasi judicial but behaves like a govt entity where everything moves very slow. IEX is there from 2008 -09 but the volumes getting traded has not seen a significant incease. every unit traded or i would say bought or sold they get a trading margin which is not regulated and that is good for IEX to increase its margins but too much high margin customers will move away.

we also have the Discom’s poor financial health leading to increase in CSS and Addl surcharge resulting in open access customers moving away from exchanges thereby reducing the volume. The major customers are only DISCOMs. The govt indirectly supports the discom’s and we all know the power sector is in a mess due to majorly being fully regulated and controlled by the Govt.

unless and until they can increase their volumes IEX will continue to be traded in the narrow band or even lower as there is no visibility of growth in volume as well in different markets or geographies.

IEX plan to have an exchange for a GAS hub also is a non starter as govt has not done anything on this front. they have been talking for the last 3 years but nothing much has moved

yes, Amansa got lucky.

Almost 10% of shares were traded on Friday. Agri Power holds only 5% so who sold the remaining 5%. Also, why didn’t Agri Power and Amansa do a block deal? Is Agri Power really desperate for money that they had to sell at a discount to market price (last I checked they were BB rated).

Also there is some progress in the gas exchange as per the article below but I don’t know how IEX will be involved in this (if it is). Green contracts and derivatives would be near term trigger as gas exchange would take some time to get started.

Intimation for Incorporation of a wholly owned subsidiary company in India to undertake the business of developing a gas exchange for transacting, clearing and settling trades in various types of gas based contracts including all other forms/types of energy, with an initial investment up to Rs. 10 crores in the form of subscribed and paid-up capital.

I am sorry to say but this has completely ignored many aspects of businesses and assumed growth will come from growth in power demand ( which doesn’t explain last 10 years 15% CAGR growth in businesses).

I think a lot more effort could have been put in explaining it.

Hi Amey,

Very nicely explained all scenarios. I think we sometime get into lot of lengthy calculation missing bigger picture. Thanks for explaining in simple manner.

thanks for the clarification, I thought it was for stock recommendation.

You may find this more value-adding -

@amey153 is the author I presume.

Impact of UDAY - to improve the health of distribution companies - has not been as expected.

Hi, can anyone share light on the fixed asset, up from 7-8 crore in Fy17 to 120 crore in Fy18 (largely intangible)? See, a 120 crore cash outflow towards purchased of fixed asset too, what is it regarding? Thanks.

I think they bought out the company and IP of the trading software which they were using. This was a very wise move.

![]()

I’m protected online with Avast Free Antivirus. Get it here — it’s free forever.

I tried doing some broad work on IEX while researching this business. So this is going to be a mixed bag post.

I found some reverse auction data on the DEEP portal website. The information on DEEP is really scant, and we have to work with what we have. The idea behind this was to answer the question that many in this forum and other blogs have been asking, how big of a regulatory disruption risk DEEP is to IEX.

DEEP Portal Link: DEEP Portal RA Result

I transferred all these RA data to the excel below and used a weighted average method to calculate the price discovery being done on DEEP. A few caveats before you go through the data,

- I am not sure whether this data-set is complete.

- I have tried to aggregate data from 200+ excel sheet and a few PDFs, there could be human errors in the process.

- The weighted average was the simplest/easiest operation I could think that was the least time-consuming. The average we get is a blended figure from auctions held since 2016.

- I am still working on the comparison data from IEX, though I am really not sure at this juncture what to use. So this blended figure has aggregated years, months, hours of seasonality, peaks, troughs and should not be compared with any single price discovery figure from IEX.

- The DEEP portal data consists of 30 days, 15 days blocks while IEX has shorted timeframes.

- The data also consists of price discovery from the IPO method. I am not sure what this is.

- I have tried to maintain some chronological aspect in the data, but since the excel sheets were state-wise, and the trading volumes differ from state to state the data is mixed. I doubt anyone here will have the time to sort through the data and come out with annual price discovery figures.

DEEP Portal Data: DEEP RA Data.xlsx (423.8 KB)

The blended price discovery through a weighted average method comes out to be 4.51 from 2016 to now. The total demand during this period was 421 BUs while the allotted units or supply were 372 BUs.

During the same period IEX has done volumes of 139 BUs:

A few price discovery data points from IEX that I think will be somewhat relevant to compare with DEEP:

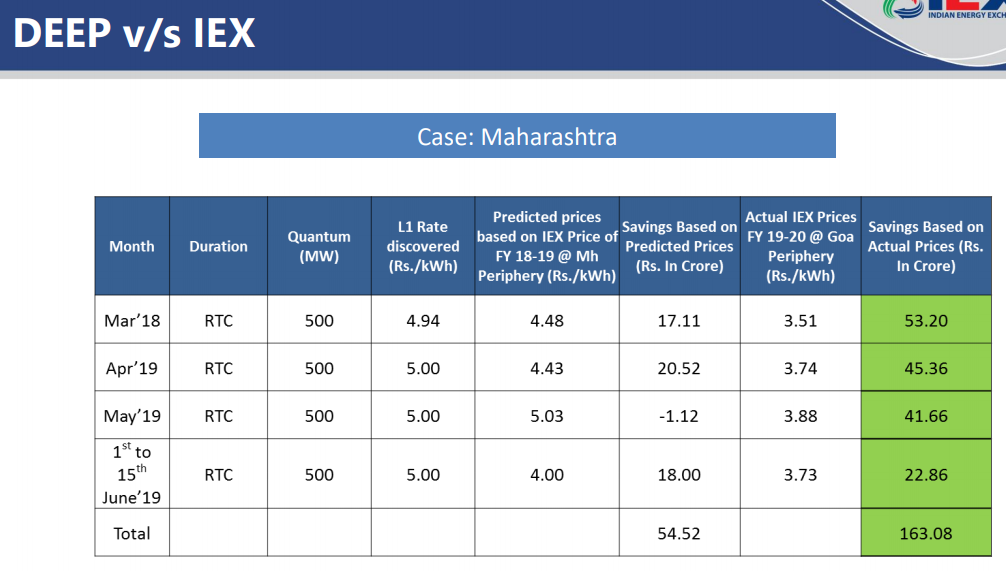

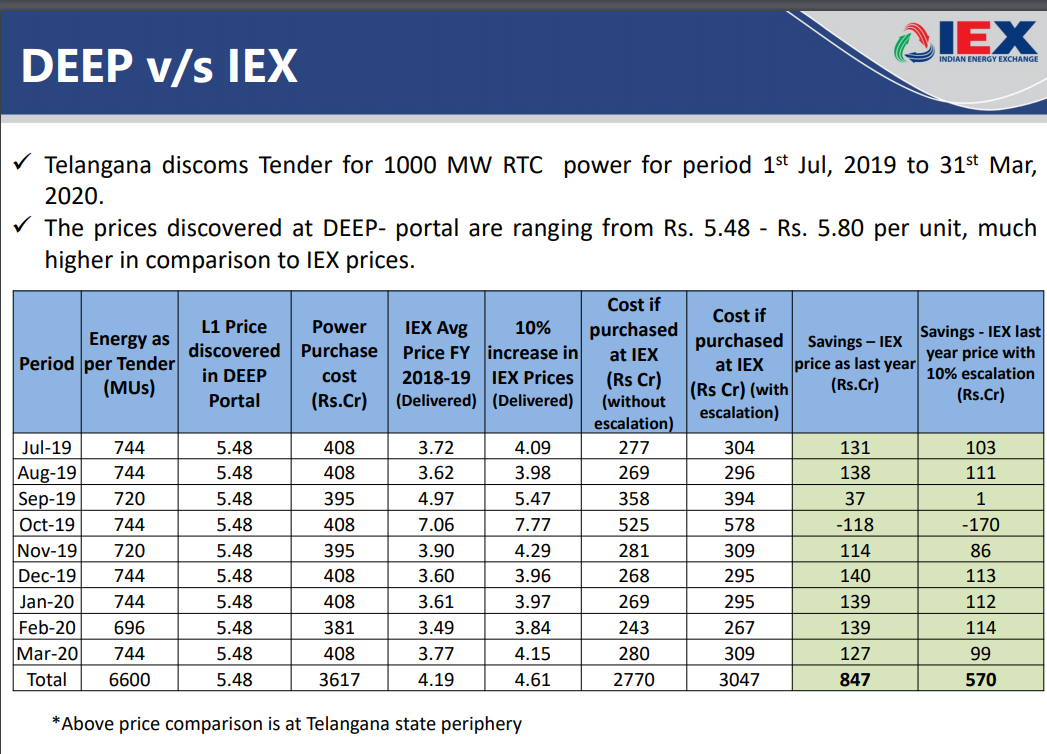

I thought of looking for DEEP data after I saw a few comparisons done by IEX in their Q1FY20 presentation.

I am not convinced with this comparison that they have done, firstly, in the case of Maharashtra they use Goa periphery prices to highlight actual savings when comparing to MH predicted prices the saving is much smaller.

As you will see in the DEEP portal data and even in IEX trade data, it is really tough to pick and compare any two data points. In the comparison, they use the average price of the entire FY for themselves and pick certain block-based prices for DEEP which is not fair. Another point is in today’s day and age of information tsunami, it is hard to believe that such big players will leave savings of 850 cr on the table.

A few other aspects I want to highlight and share with the forum members:

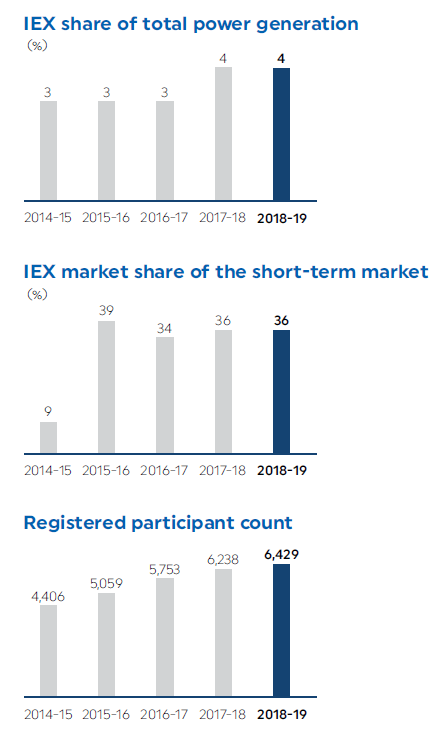

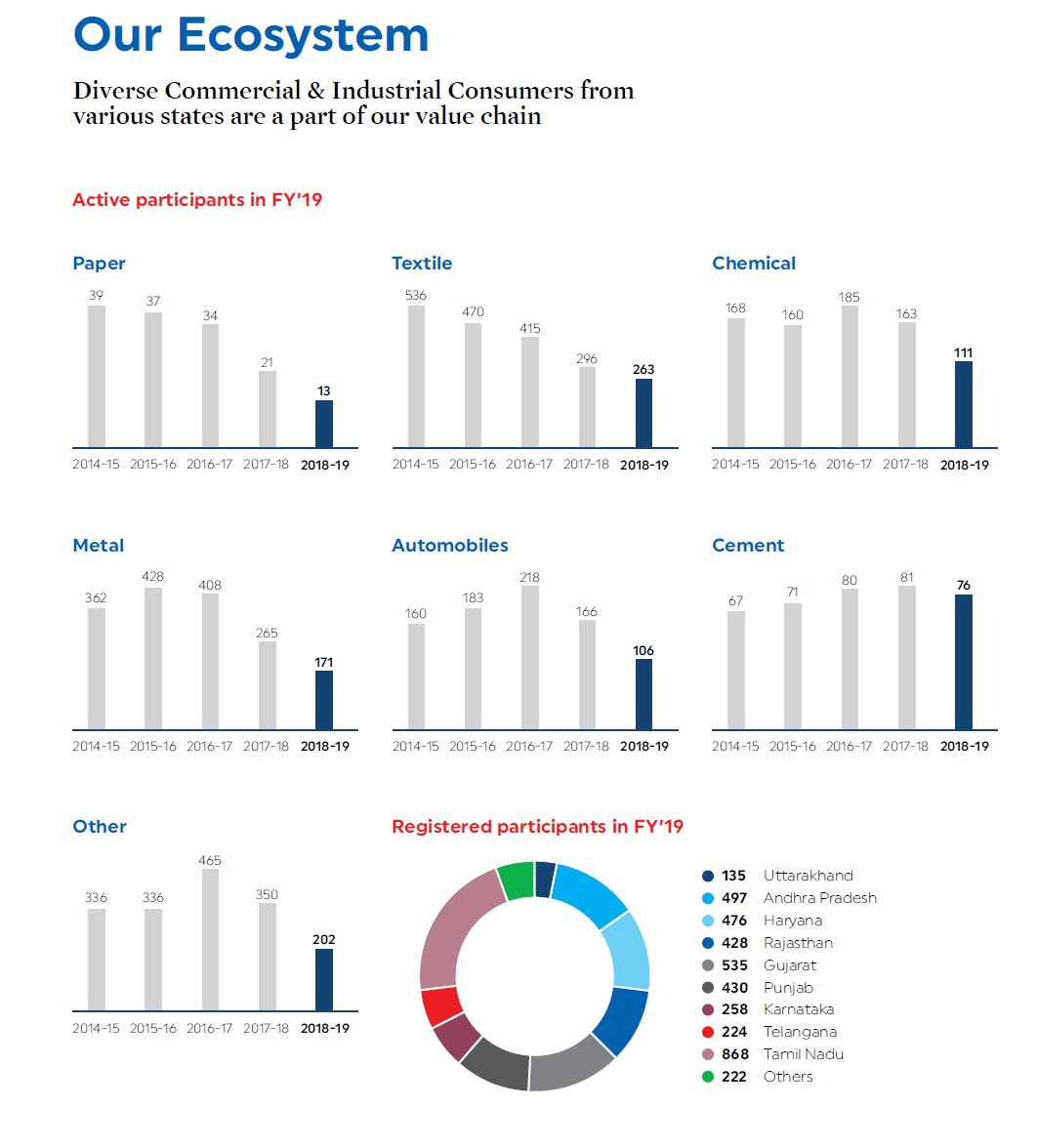

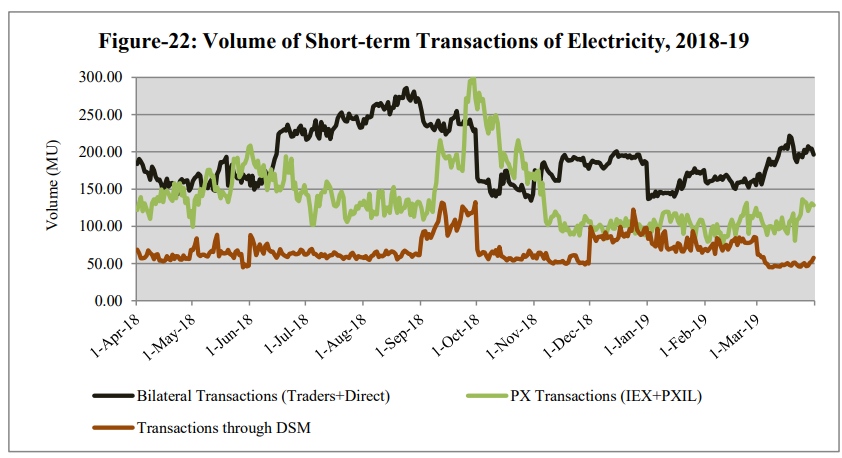

1.IEX’s market share in the ST market has reduced and if I am not mistaken this is from the same time DEEP started in 2016. What else explains this downtrend?

- Active participants in all industries have gone down since FY15, what explains this trend? Wasn’t open access cross-subsidy surcharges prevalent throughout this time period?

A few resources for further investigation:

- CERC market Monitoring Reports: http://www.cercind.gov.in/report_MM.html

- CERC Regulations: http://www.cercind.gov.in/Draft_reg.html

Have a query on this part-

“Here, “short-term transactions of electricity” refers to the contracts less than one year for the following trades:

(a) Electricity traded under bilateral transactions through Inter-State Trading Licensees (only inter-state trades),

(b) Electricity traded directly by the Distribution Licensees (also referred to as Distribution Companies or DISCOMs),

(c) Electricity traded through Power Exchanges (Indian Energy Exchange Ltd (IEX) and Power Exchange India Ltd (PXIL)), and

(d) Electricity transacted through Deviation Settlement Mechanism(DSM).”

These are the participant in the which facilitate short term transactions in electricity as per CERC. So where does DEEP fit into all this? Or does DEEP does not participate in short term transactions and its PPAs are classified as long term?

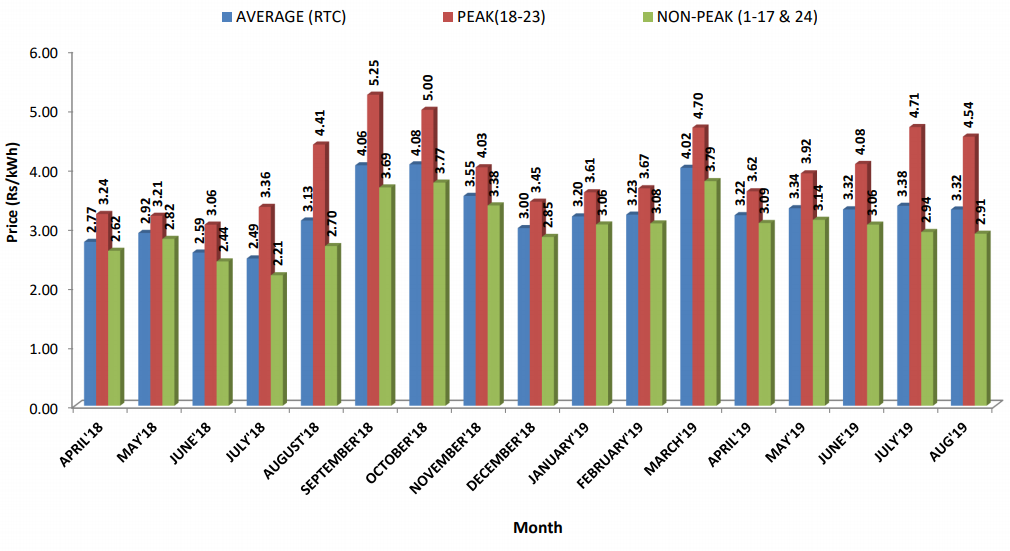

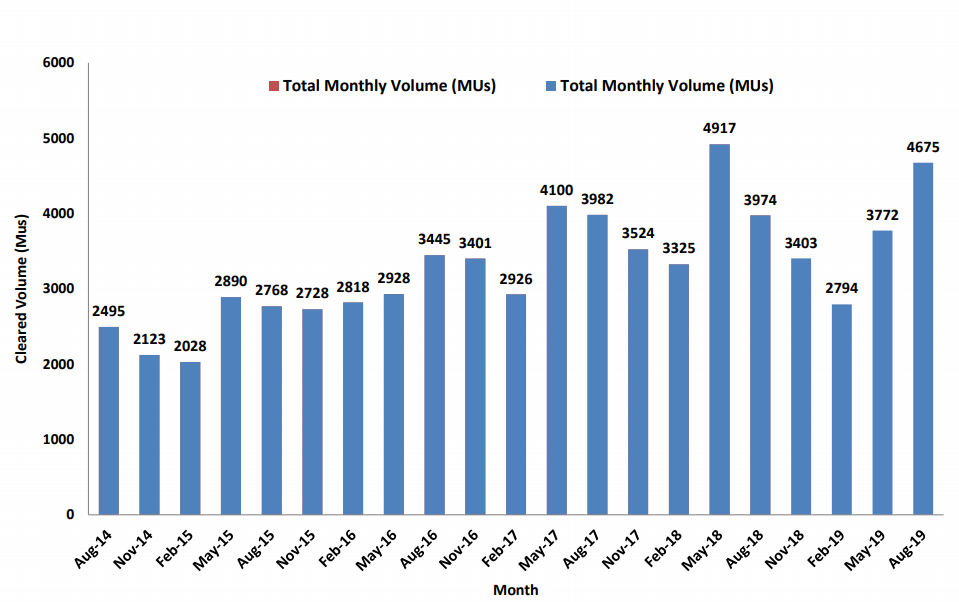

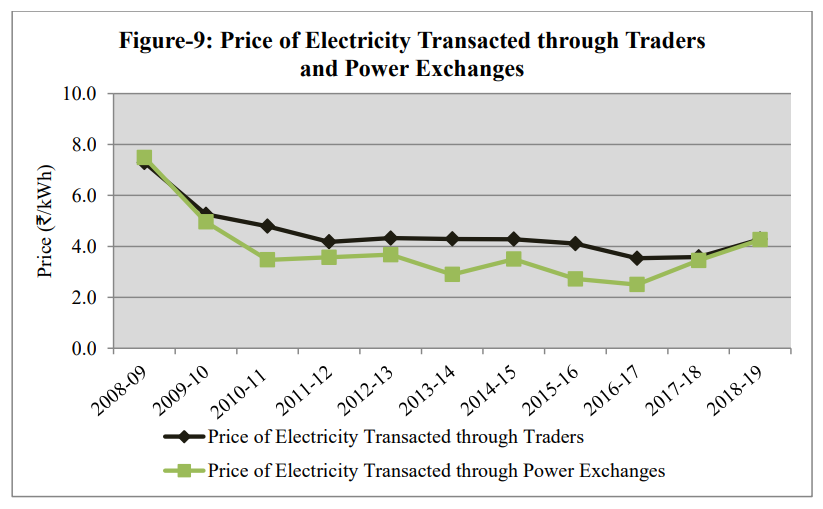

The price discovery on exchanges has gone up since 2017, any reason for this? As per the CERC report, traders are giving good competition to exchanges both in volumes and price while the DSM market has stagnated since 2010 and CERC wants that though the price in DSM is significantly lower than that of traders and exchanges.

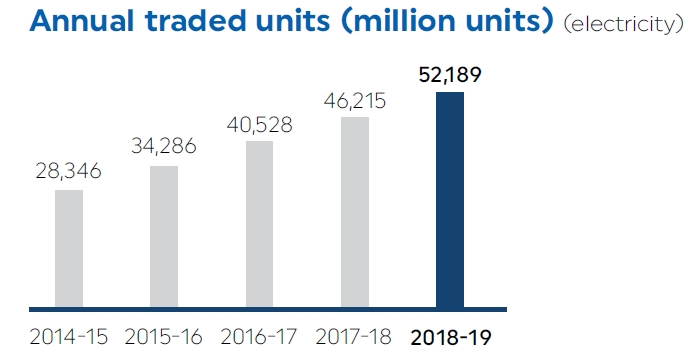

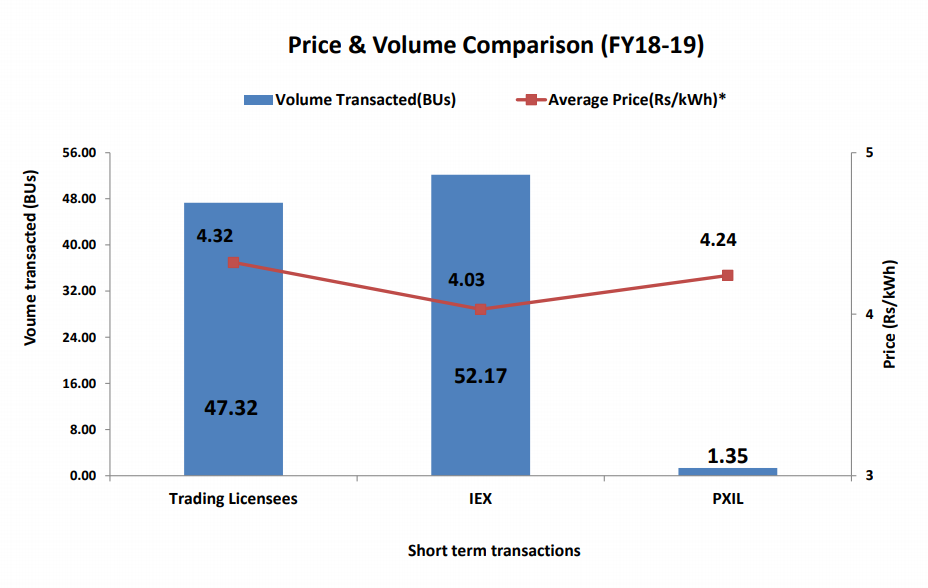

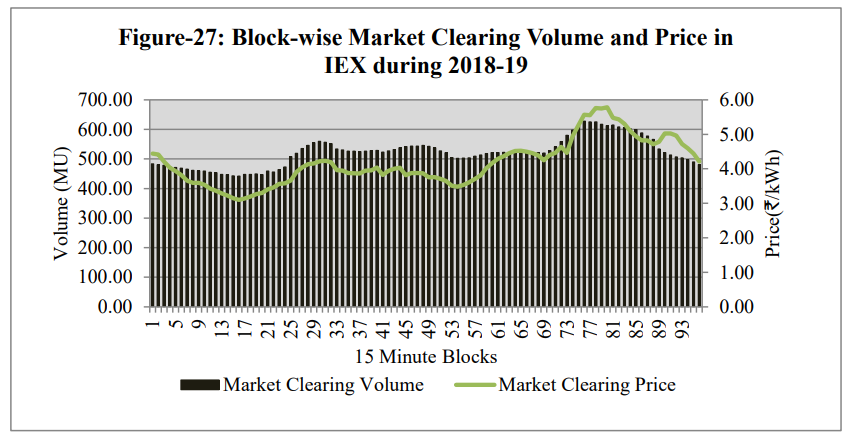

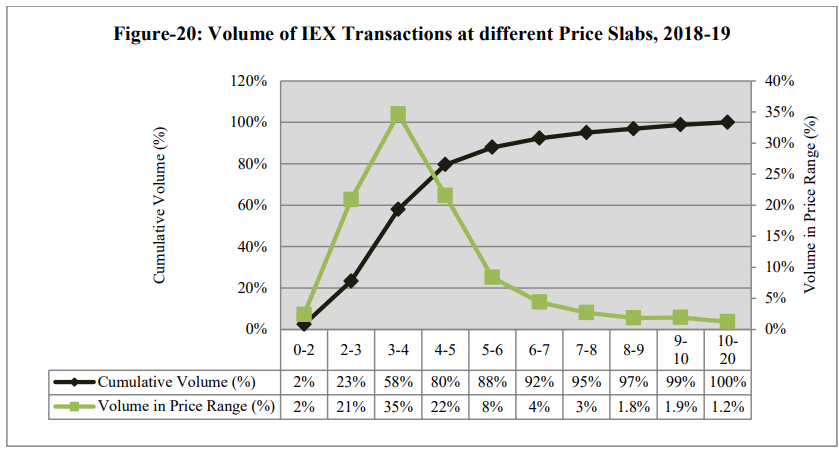

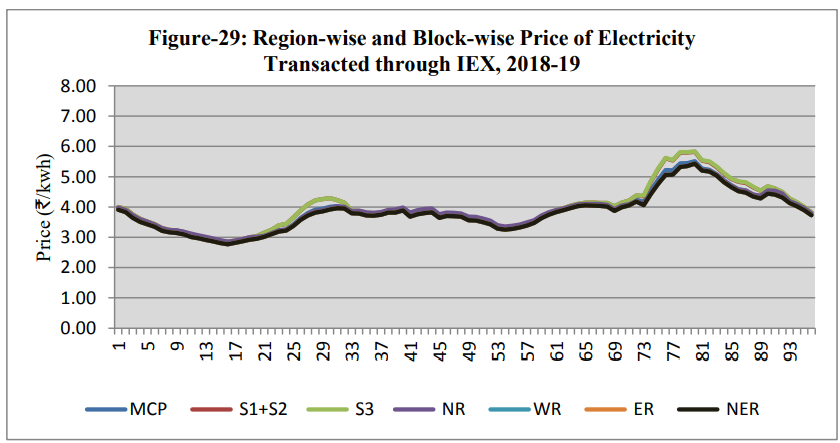

A few charts on IEX’s Price Discovery, volumes:

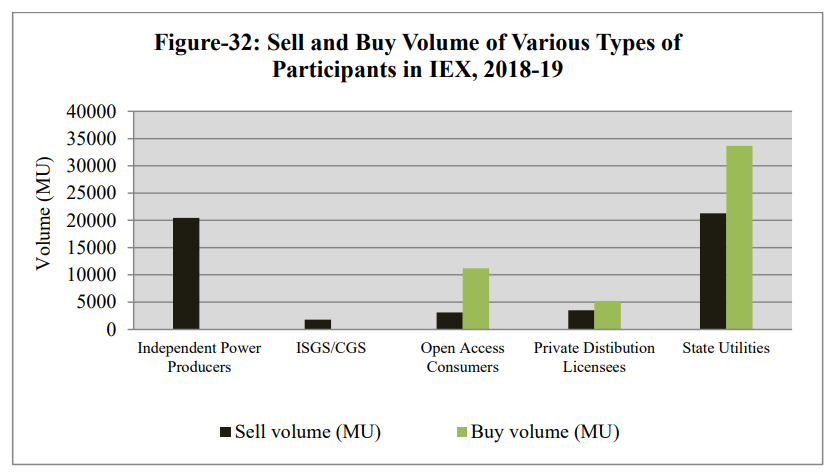

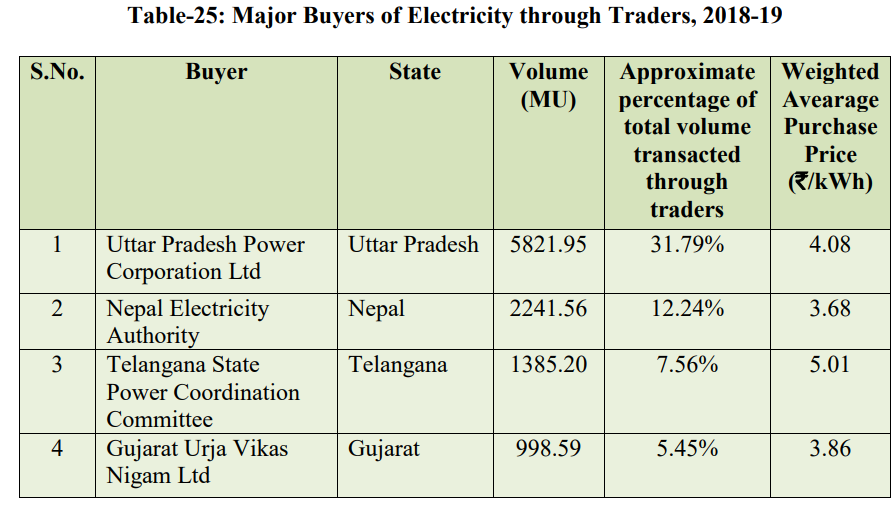

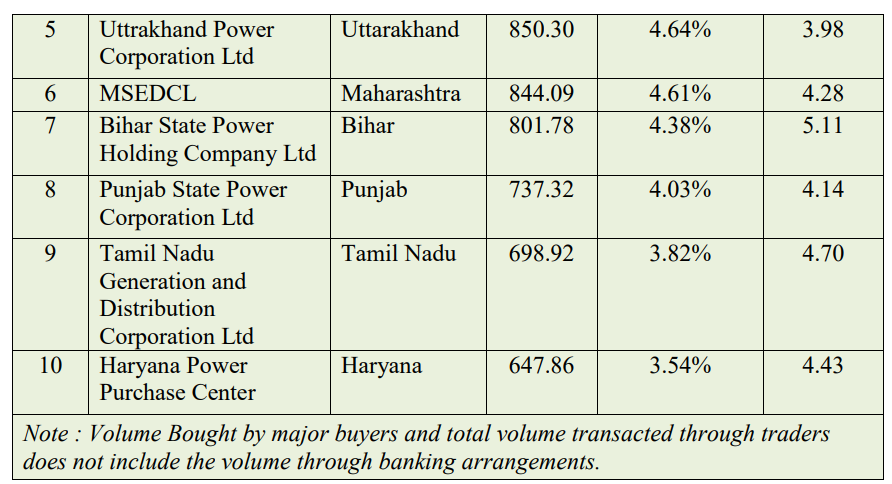

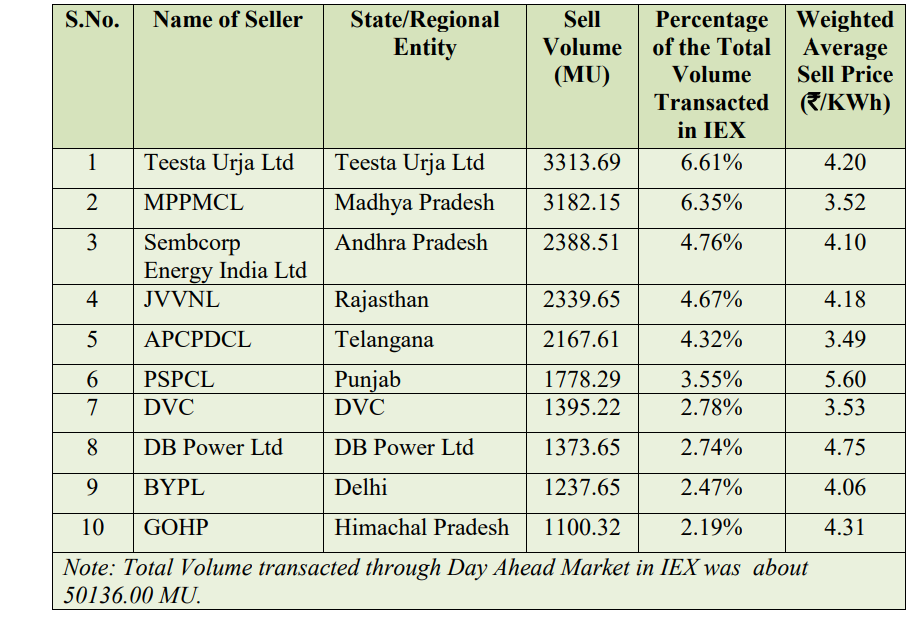

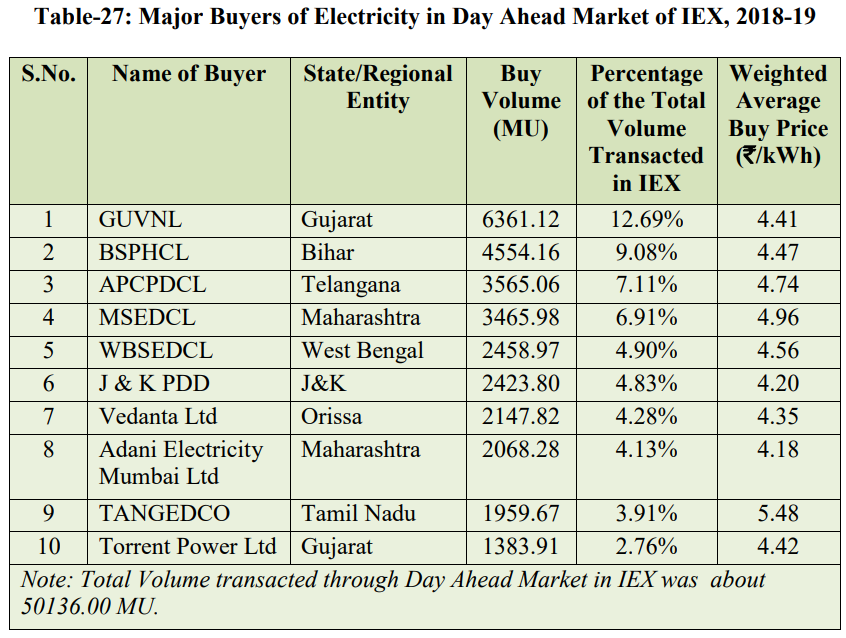

The majority of volumes (demand and supply) in IEX come from DISCOMs.

Contribution of OACs to Exchange Volumes -

Misc. Fact:

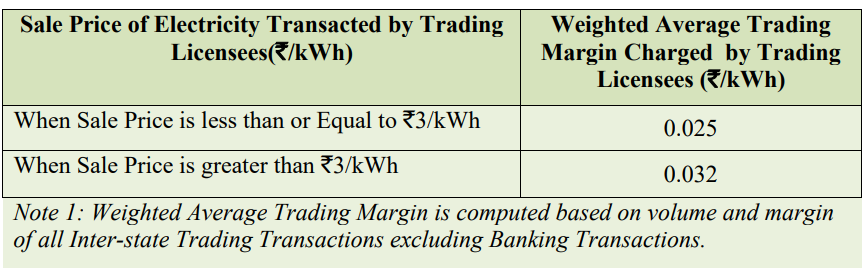

Trading licensees used to charge trading margins up to 10p/KWh in 2005, after that CERC reduced their trading margins to 4p/KWh in 2006 and now allows up to 7p/KWh if the sale price exceeds 3 Rs/KWh and 4p/KWh if lower than 3 Rs.

The weighted average price of electricity bought by OA consumers at IEX was lower (3.48/kWh) when compared to the weighted average price of total electricity transacted through IEX (4.22/kWh).

The volume of electricity bought or sold on the exchanges or through traders by any entity has little effect on the price:

An entity buying higher volume during off-peak hours can have a lower weighted price than one with a lower volume during peak hours.

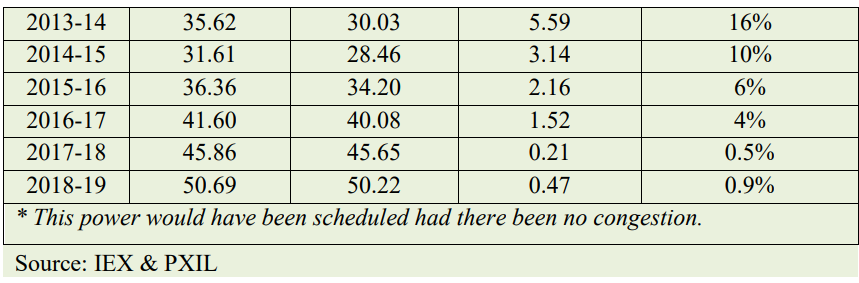

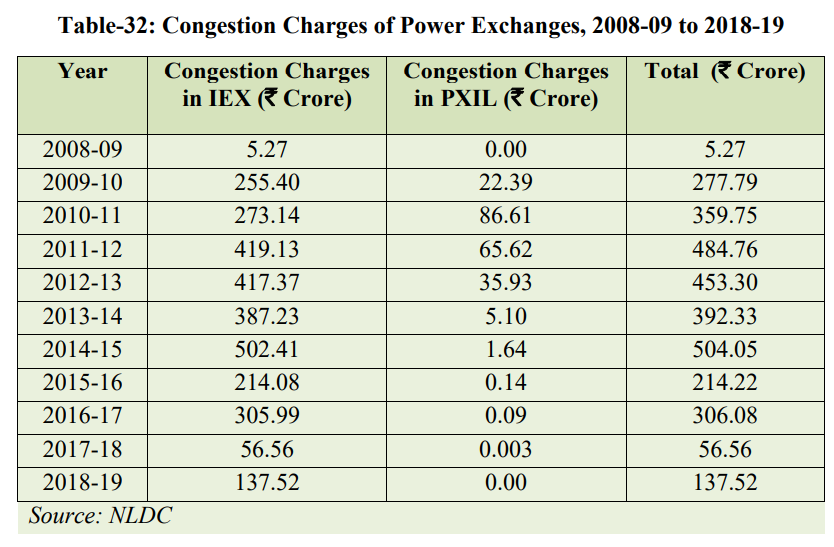

Congestion in the transmission network will be a key monitorable in the future of this business. Here is a chart with historical values:

Congestion has reduced significantly since the 1st half of this decade, though congestion charges are still high.

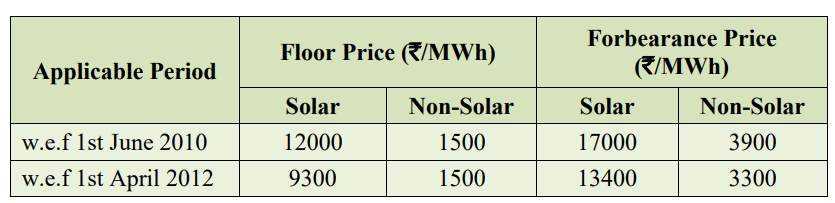

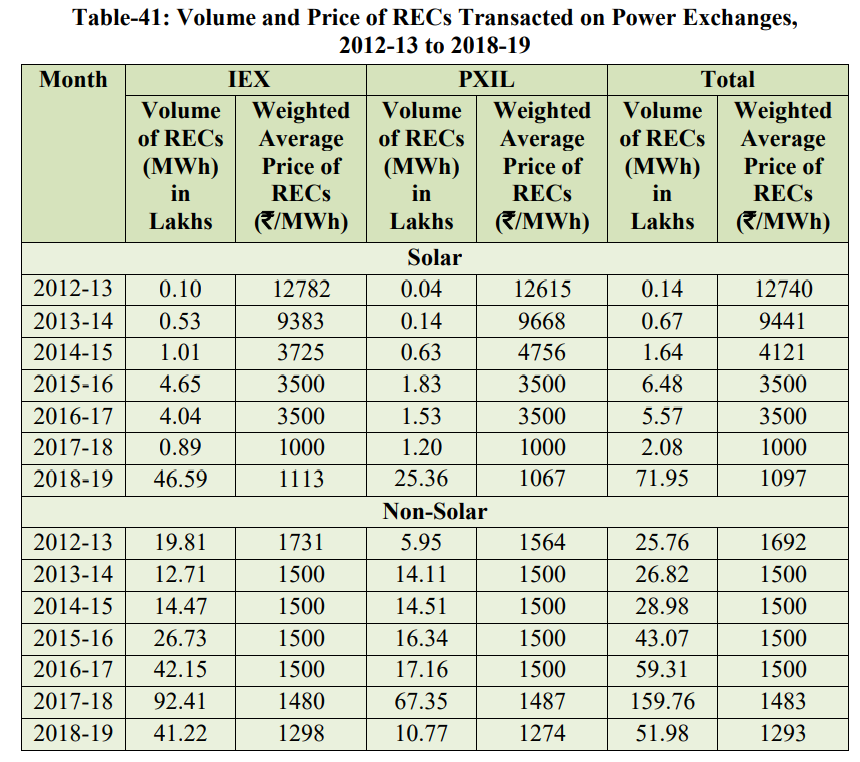

w.r.t. to RECs it is good to see that solar has come on par in terms of pricing to non-solar:

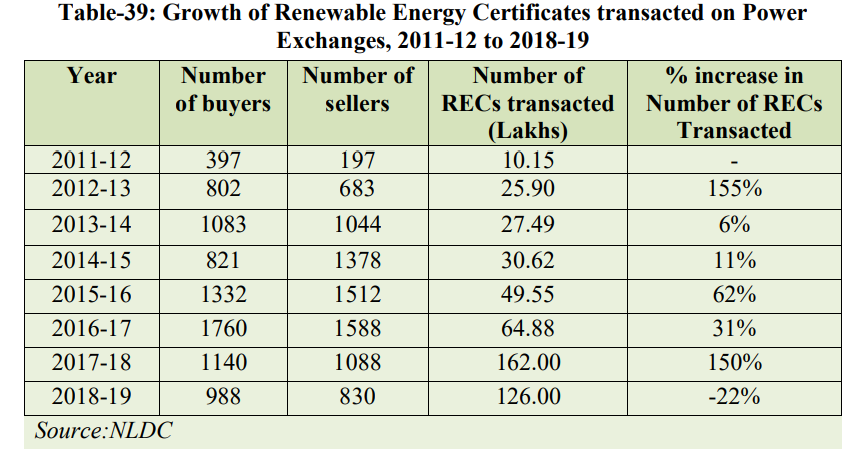

we are seeing good growth in the number of RECs traded:

though, since past few years supply far outstrips demand for RECs:

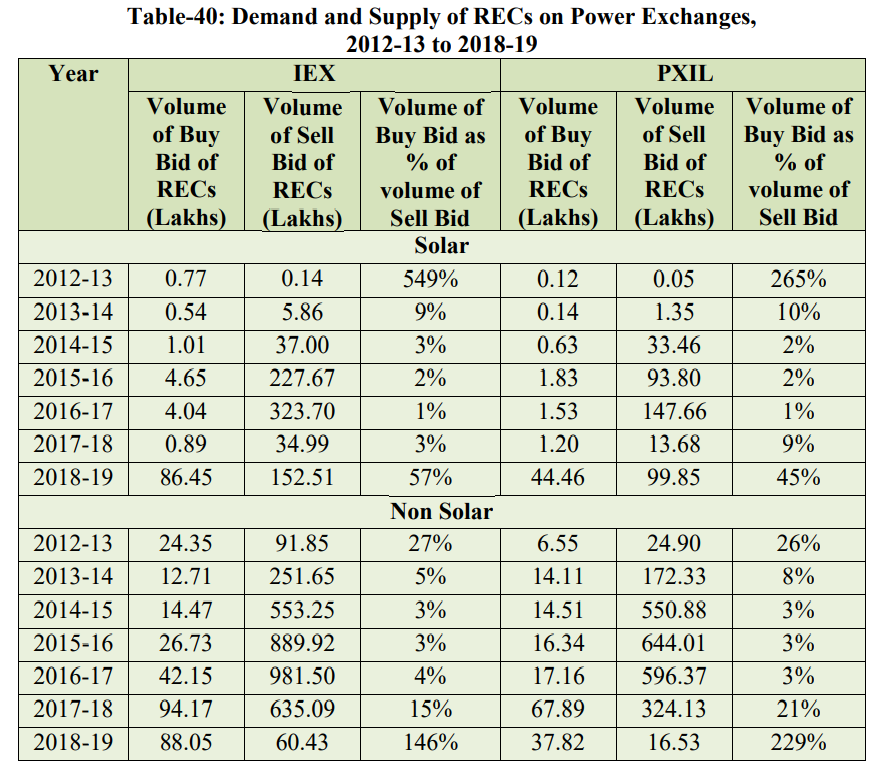

Volumes and weighted price of RECs of exchanges:

REC market is clearly not showing true price discovery as the ceiling and floor prices are regulated by CERC. This is perhaps a protectionist move to safeguard the interests of different groups involved.

The 2019s abnormal increase in solar REC volumes was due to the intervention of SC in halting trading of RECs. Non-solar RECs were allowed conditionally in 2017 while solar RECs were suspended till March 2018. When trading resumed after one year, the majority of RECs were at or near expiry for which CERC intervened by extending the validity beyond the 1095 days figure.

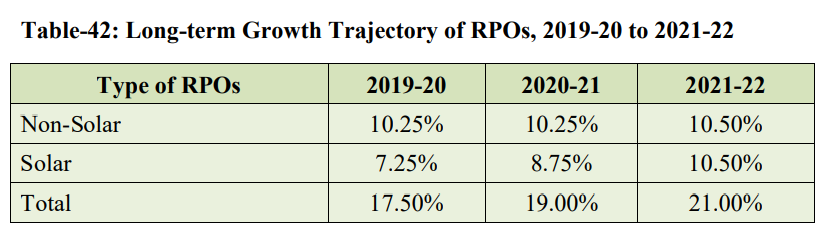

A new RPO compliance cell has been created by MoNRE to ensure compliance. Further growth targets have been given for future years.

We will not see 2019 figures soon, but growth in this market is being actively created.

I am still studying this business and the power sector, I am no expert and all of the above is just conjecture on my part. If you find any discrepancies please do correct my findings.

Disc.: Not Invested.

Hi Abhinav

You have done some detailed worked.

One needs to step back and first analyze the electricity “market-design”

Short-Term power = contract with duration less than 1 year.

DSM (Deviation Settlement Mechanism) is not a “market” - it is used as “balancing power”. Eg. DISCOM predicts demand will be 1000 MW tomo. It buys 1000 MW power from various sources (long-term PPA, DEEP, IEX etc.). Now, suddenly there are torrential rains tomo, demand reduces to 900 MW. What happens to the extra 100 MW?

It gets sold in DSM.

The opposite is also true. If demand for some reason is actually 1050 MW instead of 1000 MW, the extra power is supplied via the “deviation settlement mechanism” (DSM).

The DSM rate is a penalty not a market price of electricity.

Higher volumes of DSM pose a security threat to the electricity grid.

This is the reason why we observe steady decline in DSM volumes over the years since CERC discourages these volumes by charging progressively higher penalty.

DEEP portal is only for price discovery not for settlement (ie transmission allocation)

IEX = price discovery + (guarantee of) delivery.

The drawback of IEX is that one can trade power only 11 days in advance since “forward contracts” in electricity are sub-judice.

This is also the reason why prices on IEX (day-ahead) are typically lower than DEEP portals, since sellers are desperate to sell (electricity cannot be stored). DEEP portal is a few months in advance, there is still time for the seller to make a contract at a higher price than selling that electricity in the day-ahead IEX market.

DEEP portal exists because they can do longer duration contracts.Once forward contracts are allowed on exchanges, DEEP portal may become irrelevant.

DEEP portal was introduced because power trading was completely OTC (negotiated settlement) before. There was huge scope for manipulation and/or corruption. Prices discovered for procurement in Maharashtra would be very different than prices discovered for procurement in Uttar Padesh (the famous UP tax).

I have sold electricity for 4 years myself.

My suggestion is first study a little more on market-structure before putting in too much effort on analyzing the numbers and relative prices and volumes.

Hey Amey,

Seems like you have a pretty good understanding of the company and the business.

So, can you give some idea on the demand and supply side participants; like type of participants and share of volumes contributes by these participants.

And do you think that, PTC posses a risk for IEX since it contributes 25-30% of exchange’s volume and if PTC moves its volumes to another exchange probably the one being setup by BSE+PTC.

There are basically two types of buyers - distribution companies and open access consumers.

Imagine it this way. Suppose I am a buyer (industrial open access consumer). I buy on IEX. I buy 10 MW every day at average Rs 4 per kwh.

Energy Bought = 10 MW * 24 hours * 10^3 = 2,40,000 units (kwh).

Money spent every day = 2,40,000 * 4 = 9,60,000 Rs

I pay 2 paise per unit to IEX as fees

Fees to IEX = Rs 4,800 (Four Thousand Eight Hundred only)

Suppose a new exchange starts. Since from day 1, price discovery is not very efficient as not many sellers/buyers can be persuaded to shift the exchange unless some tangible benefit is guaranteed/highly likely.

So, price settles for Rs 4.20 per unit (5% variation) on the new PTC exchange.

What is the money I spent on buying power from the new exchange.

Money spent = 2,40,000 * 4.2 = 10,08,000 Rs

This is a loss of Rs 48,000 = 10 times the fees I pay to the exchange.

Even if the new exchange offers me free trading like Zerodha, will I switch from IEX to the new exchange?

Plus, as per regulations, a power exchange is a market infrastructure. This is the reason why BSE, MCX, NSE are being listed on stock exchanges - there should be no single promoter who can influence the rules of the game.

PTC can own only 5% of the new exchange

Check this out

The new exchange is not getting permission from CERC till they first sell the ownership to a wide variety of institutions.

The article also mentions that PTC will end up owning only 5% of the stake.

Will PTC for 5% of the stake risk making real and big losses to its customers who trade on the IEX?

If PTC is so interested in the power exchange business, why did they sell their stake in IEX after making something like a 100X returns?

So, lets not worry about things which are really really remote. We are not investing 50% of our portfolio in this stock. If a competitor comes and survives, the market would have sufficiently expanded for 2 exchanges to flourish. And many of the reforms I have mentioned in my article would have already taken place.

IEX is the biggest player in spot energy trading with a share of 97 per cent, and with participation of over 6,500 players

Potential threat to solar roof top targets