It’s kinda hard to tell how things will unfold considering this sector is politically intertwined. Ideally DISCOMS will try to choose the lowest possible rate. For last 2-3 years rates dropped dramatically on IEX due to excess capacity, hence the buying spree on IEX. In recent months rates have picked up on IEX as supply/demand gap is getting adjusted.

In a sense it is possible to buy peak power through IEX if the rates are cheaper than buying through PPA.

Management has stated in the concall that higher prices in the past couple of months is seasonal (happens every year) and prices should cool down now. They had also mentioned that prices above Rs 4.5 would prompt discoms to switch to PPAs. So I would keenly watch this number. At least for this month prices have been below this number but I guess these are low demand months.

I mean to say is YoY month-wise price increase is significant compared to last 2 years. For me at least the current valuations are on higher side for any notable gains.

I think the volume would go up. Currently the output is curtailed incase of excessive supply. Lets say for renewables, the energy can be stored and supplied at peak times.

Although economical storage systems are few years away, I dont think for medium term there is any impact.

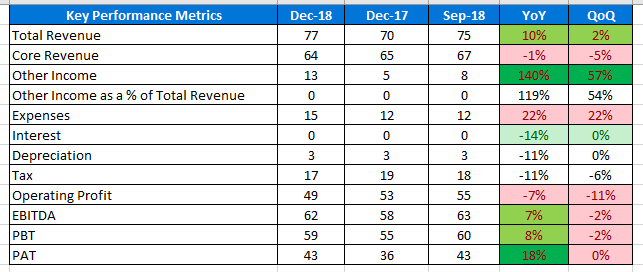

Fairly decent quarter with 10% revenue and 18% PAT growth (some contribution through other income). With proposed buyback, there should be ~1% gain to EPS to existing shareholders.

Not really. But broadly it depends on the renewable energy generation in the country for which the generator gets RECs. These RECs are then bought by SEBs to fulfill their renewable quota.

Anyone done an analysis as to why the volume traded in DAM contracts has been consistently declining YoY basis since last November. Is it likely that this could be structural issue for the short term spot market? While I understand the reasons that the management provides in the monthly power updates, hasn’t one or the reason gone on for a bit of time? It is peak summer and the average monthly volumes for May as well as June have hovered around 130-140 MUs - about 20-30% lower than last year. The company is at almost peak EBITDA margins and any degrowth in volumes could result in operating deleverage being played. Just wanted to know how forum members interested in IEX read this. Many thanks

Bilateral contracts provides better realisation for suppliers and comparatively longer terms (weeks-6months).For discoms it provides stable supply at known fixed rate. IEX DAM is more like a top-up for day ahead short supply or selling excess for suppliers.

The main buyer last year was Gujarat discom due to issue related to tata and Adani umpp. Those have been largely resolved.

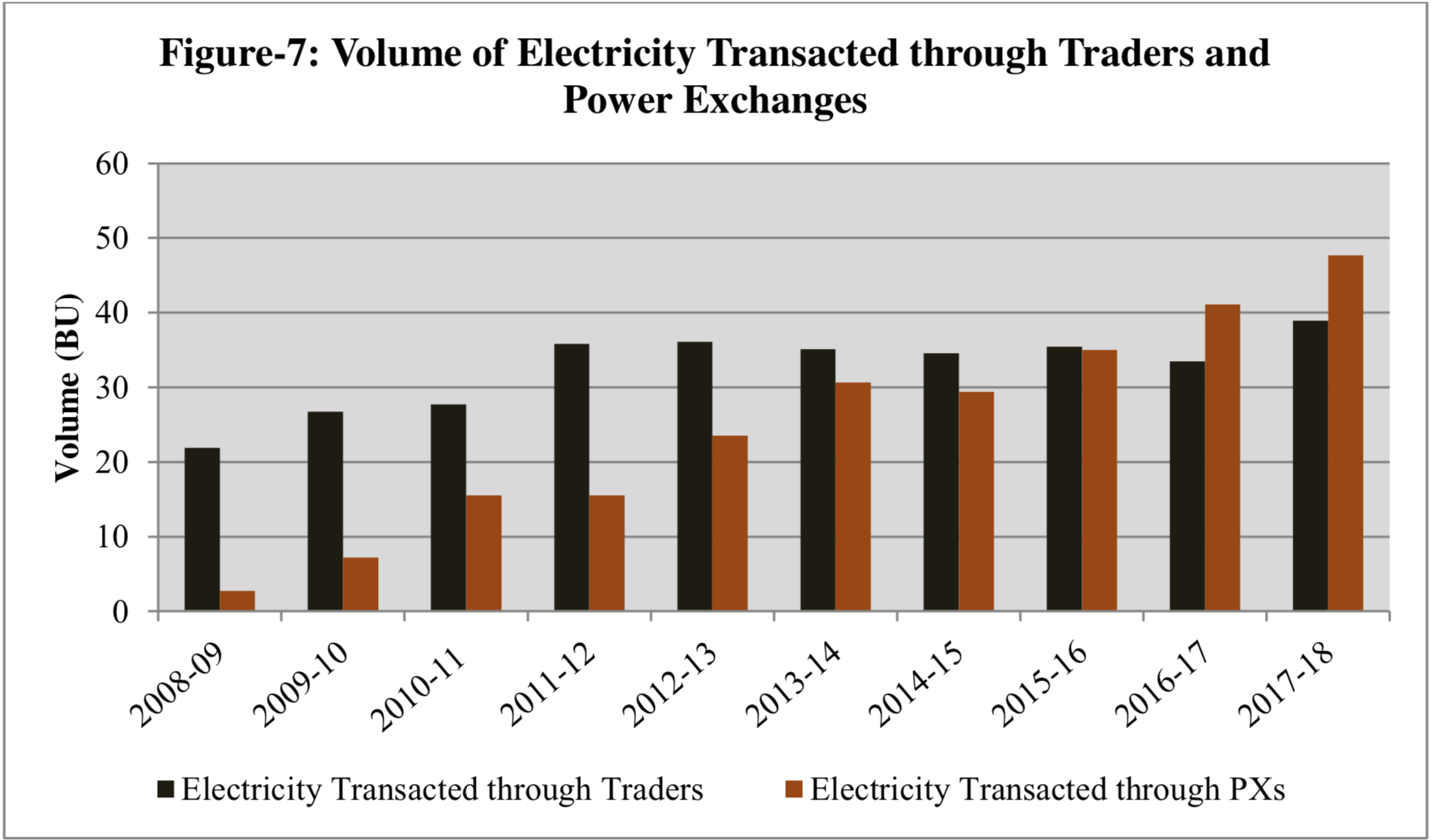

India’s power demand is expected to grow with the government’s focus of providing “24x7” clean and affordable power for all. Of around 1,200 billion units (bu) of electricity generated in India, the short-term market accounts for around 130-150bu. This trade volume has grown by around 10% annually and is valued at around ₹ 22,124 Crore.

This short-term power market is serviced by power exchanges, which function on the lines of commodity exchanges and provides a platform for buyers, sellers and traders of electricity to enter into spot contracts that are for the same day, next day, and on a weekly basis. It also provides a payment security mechanism to buyers and sellers. India, currently has two operating power exchanges—Power Exchange of India (PXIL) and India Energy Exchange (IEX).

There is a need to deepen existing exchanges through more evolved products, clarity on cross border trading along with institutional mechanisms to deal with forward contracts of varying durations.

In this regard, Pranurja Solutions Limited (Consortium of BSE Investments Limited, along with PTC India Limited and ICICI Bank Limited), filed a petition with the power market regulator, CERC (Central Electricity Regulatory Commission) on September 7, 2018 for grant of license for setting up a new power exchange. The final approval of CERC is awaited. Our proposed Power exchange would offer the market participants a world class power trading platform.

AFAICU, existing participants can list on both exchanges. The current market is very much under-penetrated so both exchanges have the chance to gain new participants. So, for a participant, listing on both exchanges means better visibility towards other listed participants.

Disc. I know very little about energy exchanges. And this conclusion is based on the inference drawn from stock exchanges. I can very well be incorrect. Feel free to correct me.

As per CERC Rule 13(5) If Any Exchange has less than 20% market share for 2 consecutive year, it has to merge with other exchange. But for this rule to apply there has to be at least 3 exchanges.

Total revenue 14.87% Up, PBT 15.88% Up, PAT 25.33% Up

Revenue sources

Transaction fees - 92.3% of total

Annual subscription fees - 7.3% of total

Operating profit margin at 82.58%. Net profit margin (51.43% to 56.1%) has increased because of company being in lower tax bracket.

52.2 BU electricity traded volume as compared to 46.2 BU last year. 13% YOY up

Day ahead market: 50 BU electricity traded as compared to 44.8 BU last year. 12% YOY up

Term ahead market: 2105 MU traded as compared to 1373 MU last year. 53.3% YOY up

Renewable Energy Certificates: 89.56 Lakh certificates traded in 2019.

Energy saving certificate: No business. Regulated under PAT (Perform Achieve Trade) scheme of Ministry of Power. PAT Cycle-I was conducted in 2017, Cycle-II is expected to happen in 2019-20.

There is a sharp-increase in finance cost from 22.66 Lakh to 73.42 Lakh. This was due to provision of 50.85 Lakh, towards refund of 70% of the return earned on investment of security deposit by members.

There was a sharp-increase in company’s trade payable and trade receivable YOY. Trade Payable from 84.63 Cr to 133.83 Cr. Trade receivable from 0.22 Cr to 45.89 Cr. This was due to non-clearing days on March 31,2019 due to Sunday.

Key Business growth drivers

Implementation of gate closure time → can help in making power exchanged true real time.

National open access registry and removal of procedural barrier → Can lead to attractive open access transactions.

Introduction of long duration contract on exchange → Can shift volume from bilateral trade to exchange.

Phasing out of 35 GW of old and inefficient capacity will lead to discoms using more of exchange.

Cross border electricity trade on exchanged → PTC India recently signed PPA with Bhutan

Coal linkage to sell in short-term market → Favorable for short term electricity market

Seasonality factors → Hydroelectric potential states (HP, J&K, Sikkim, Uttarakhand) are power-plus in summer but have power deficit in winter months. Some states like Punjab and Haryana have power requirements in the summer and monsoon seasons but are surplus in winters. This diversity provides power trading opportunity.

Questions to explore (Mostly thinking out loud):

There has been systematic downward trend as per number of active participants in commercial and Industrial consumers from 2014-15 to 2018-19.

Paper : From 39 to 13

Textile: From 536 to 263

Chemical: From 168 to 111

Metals: From 362 to 171

Automobiles: From 160 to 106

Cement: From 67 to 76 (Almost constant or slight increase)

Others: 336 to 202

Though I believe above trend is due to surcharges and other non-favorable regulations for open access. Active participation from these industries can provide sustainable growth. A number to look in future specially upon the implementation of National open access registry.

IEX relies on ESOP as compensation mechanism. IEX granted 150,000 shares in last year. 100,000 in Nov 2018 at Exercise price of Rs 160 and 50,000 in Dec 2018 at Rs 166. What is the impact of company’s ESOP policy on retail shareholder?

IEX has been holding some amount of cash approx 475 Cr (267 Cr last year), causing both their non-current as well as current investments to grow from last year. This was after company had bought back shares worth 69 Cr. Company mostly invests money in Debt and Liquid mutual funds (FMP many). As cash amount is supposed to increase, it would be worth watching how they utilize it?

What is the market concentration at IEX and impact of it as client concentration risk? Jan to Dec 2017. Contribution of top 10 seller at IEX - 36%, top 10 buyers at IEX - 48%.

Do major buyers and sellers keep continue doing business on IEX over years? or they switch from IEX to bi-lateral traders very frequently?

Comparing Top 10 buyers and sellers (Jan-Dec 2017) from traders and IEX. There are some unique trends. for example: Punjab state power corporation ltd and Telangana state power bought approx 4BU from traders, but not in top 10 list at IEX. Similarly Gujarat Urja vikas nigam ltd bought 5BU from IEX but not in top 10 list of traders. How does state decide how much to buy and from whom and who is the decision maker? Can the decision be influenced by non-economical reasons like political interference?

In spite of several regulatory uncertainties, Power exchanges (IEX mainly) seems to be doing great.