Link to the interview of IDFC Bank’s Mr V Vaidyanathan to Zee Business:https://www.facebook.com/zeebusinessonline/videos/861798184598332/

What is the reason for the reduction in provisioning?

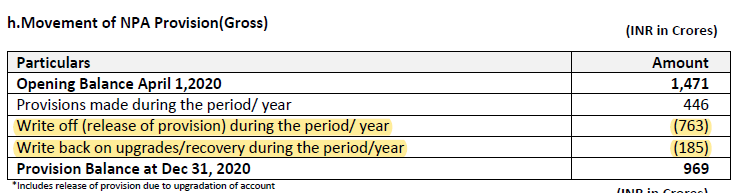

Have already made provisions for Covid over the last 2 quarters and thus incremental provisioning is now much lesser,Have sufficient provisions as of now.

Asset Quality outlook?

Declared NPA is at 1.33% Gross and 0.33% Net NPA.

This is not representative due to standstill as per Supreme Court order.

Long term Retail Gross NPA used to be 2.27% now after Covid it is 3.88%,

Net NPA is 2.35% on proforma basis.

So about 1.6% NPA rise is purely due to Covid.

Collections have recovered strongly,improving every month steadily.

Touched 98% of the pre-covid levels(Jan-Feb 2020).

Expect the Gross NPA and Net NPA to get back to the long term average of 2.2% and 1.2% respectively in 2-3 quarters.

Bank has unique capability to lend to small businesses/entrepreneurs

with small ticket sizes ranging from 20k to 2-300k and managed to do this keeping good credit quality.

Have 9-10 million customers,3 million MFI customers.

Have given 1.6 lakh toilet loans which has been performing very well.

Lending for cattle,goats etc.

Category has huge potential in India and will surpass the guidance for retail loan book of 1 lakh Crore in 4-5 years.

Response to Credit card launch extremely good.

Have launched initially for own customers.

Huge number have applied in advance even before we have opened the applications to new to bank customers.

Overwhelmed by the goodwill for the bank amongst the people.

Have broken the barrier by offering cards from 9-36% when industry was offering at 35-40%.

9% will be for very few select good customers.

Vodafone Idea:exposure of 3244 Crores.

Provision of 800 Crores already done.

Latest update as per management of Voda idea is that there fund raising plans are on track.

Hoping that they will be able to raise the money needed given the improvement in general market confidence.

So, recovery of this 800 Cr. will get added back to the bank’s profits.

In MSME category Bank gives millions of loans.

Give loans based on the Bank Statement rather than ITR.

Budget is bold especially talking about privatization of PSU banks.

On Morgan Stanley giving low targets for the stock.

When stock was 40 they gave a target of 20

when Covid came they said target is 10.

Even in their latest report there are some mistakes(in their logic and on counting of stressed exposures)

They are not able to understand the business model,looking at the numbers very mathematically that exist as of now not understanding the potential.

The true picture of the bank will emerge after 2-3 years and expect them to change their opinion at that time.

Mr. Vaidyanathan got emotional in the last part of the interview while talking about

those who helped him.