NII number for this quarter has been impacted may be by 25-30 crs due to reversal of interest on proforma GNPA accounts. Very Positively surprised on growth in core other income

A lot of opex has been frontloaded till now to acquire CASA(in the form of Rs 3000 Amazon,Flipkart Vouchers) and branch expansion. C/I of 79% in Q3 shows a huge operating leverage playing out in FY22,FY23 and FY24 with a targetted C/I of 55% FY FY24.

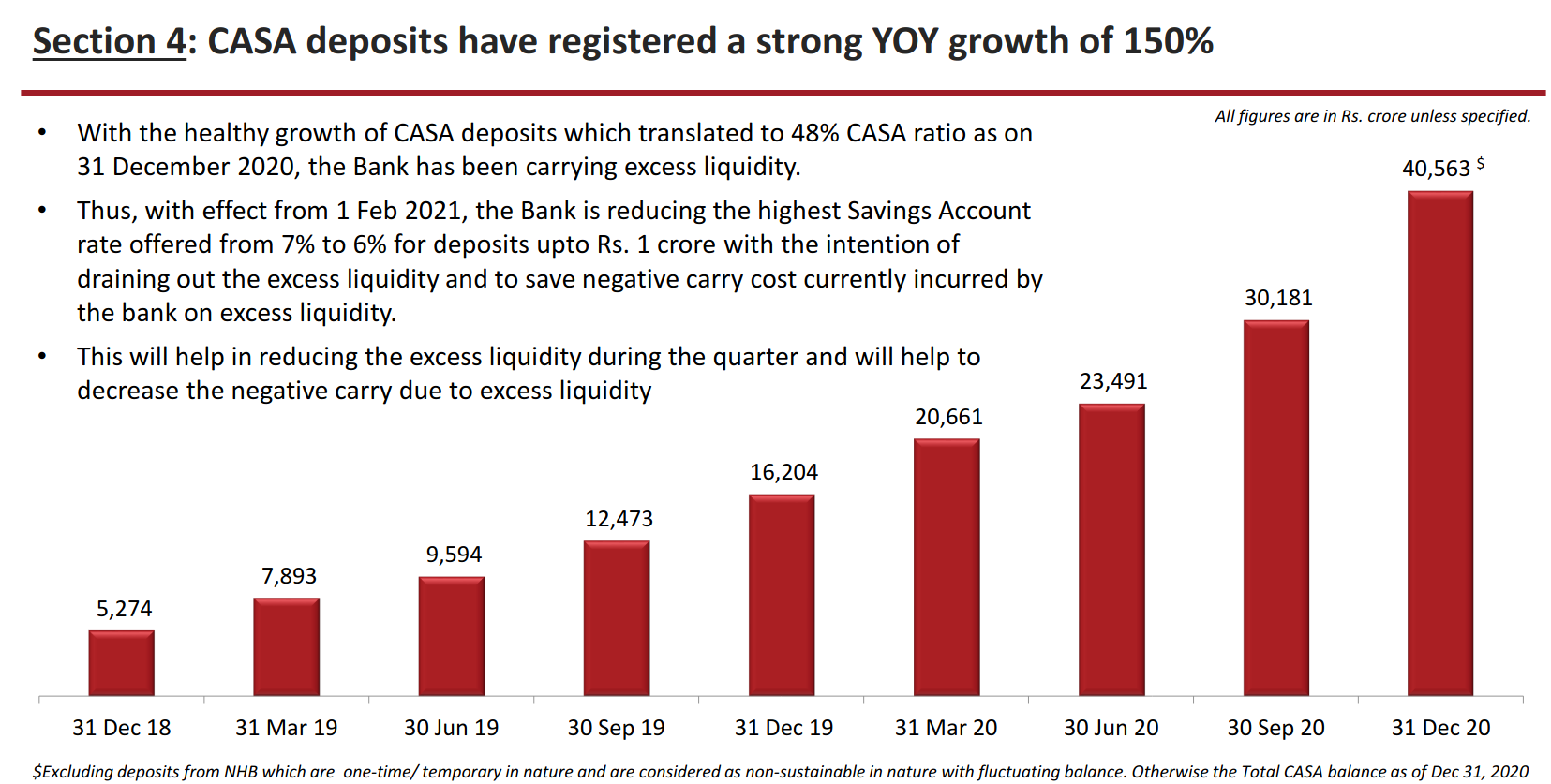

Reduction in SA rate of 7% at this juncture indicates that management underestimated the pace of CASA accounts opening and was overwhelmed by the demand. Good and timely move to reduce SA rates and will impact PAT by 500 crs in FY22(Considering Avg CASA for FY21-22 of 49000 crs).

My C/I and RoE projections for FY22 are 66.9% and 7%. Profitability is now on a J-curve growth in my view.

Hindrances on Stock Price jump can be:

Manner of reverse merger between IDFC and IDFC First

Just wanted to post a correction to my earlier post:

I had calculated this CASA on customer deposits, excluding certificate of deposits but that is not correct. CASA actually did increase by 10000 Cr this quarter, which I expected but still surprising.

Could the bank sell some of the chunky wholesale loans (which also have relatively low yields) to improve the ratio without raising funds? Adding those funds to reserves would decrease the denominator and increase numerator. Is something like that allowed by regulations?

After retail segment become profitable the bank could afford to sell the under-performing wholesale loans at some loss.

Reducing of cost of funds by decreasing SA rate allows bank to reduce the interest rate given on a loan while maintaining the NIM. Reduction in the SA rate won’t result in the saved interest cost for shareholders but it will flow to borrowers in terms of the reduced interest rate.

Reducing interest rate for borrowers is required by competition dynamics within the market. When a customer is taking a loan with 12-15% interest rate from a Bank, it is likely that the customer has shopped around with numerous competitors, offering loans within few clicks and seconds. Choosing to lend money to a borrower at a lower rate of interest than competition is also risky proposition for a bank.

Why does IDFC First bank want to increase CASA ratio? CASA is usually beneficial for banks as it is a source of lower cost of funds vs TD/borrowing. Looking at the IDFC First Bank’s interest rate, increasing SA comes at a greater interest rate than a TD and hence less useful for economic earning of the business but good for ratio based cursory

analysis.

This is a good strategy for a new bank competing with established player but it is also risky (asset quality/ephemeral deposits) and expensive (higher cost/reduced NIM/ROA/ROE).

For valuation point of view, bank is available at ~1.5 P/B ratio. Doesn’t seem attractive enough entry point but playing in the right direction going forward.

Any increase/decrease of interest rates in SA becomes effective on the entire stock of the deposits ie both existing as well as fresh deposits. In case of TD it is effective only on fresh deposits. Therefore it is the most preferred way to get the deposits from retail customers.

In my opinion, 6% saving rate is also high and the bank would have to reduce it further to moderate deposit increases. Maybe within a year.

The bank is doing very well. They have handled Covid crisis very well by taking adequate advance provisioning action and continuous monitoring of accounts. It has become very difficult to predict Supreme court decisions in advance, even if one knows most of the facts but one can presume that by March end, the SC would withdraw the restrictions put on banks and allow them to have normal interactions with their borrowers and recognition of NPAs.

The results over the past few Q’s have consistently moved in the right direction on all parameters, IMO. The one big concern is the amount of provisioning required for COVID, and how long that will continue.

I recall VV mentioning total no. of NPA’s at Q4 end at around 2-2.5%. However, GNPA seems to already be >4%, and we’re still in Q3, with VV himself saying the real pain will come in Q4. With NNPA being ~2%, there is around 2000 cr that remains to be provisioned, for Q3 NPAs itself. Q4 is yet to come.

Is this not significantly worse than guided by VV a few months ago? I could be wrong, happy to be corrected by more knowledgeable people. I think the NPA’s are really the big albatross that can undo all the good work for the next 1-2 years.

As an aside, a lot of us perhaps read the investor presentation in detail and base our conclusions on that. However, this ignores the fact that that contains data exclusively chosen to please investors, and then designed specifically to look appealing to investors. It’s important to read between the lines for the conclusions all companies try to downplay.

Something for us investors to cheer for after a below par q3.

One thing I want others to also talk about is:

Is this lowering of interest rate even after promising that they will keep the rates at 7 for sometime and giving reasons for the same due to:

Management getting defensive/cautious given the rising GNPAs.

Or the large increase in CASA as the management is saying.

Personally I think the sudden change in strategy is due to the first reason. Though obviously 10000 Cr of CASA last quarter would have made them do this with higher urgency.

From what I understand, the interest rate being the cost of capital is only important to enable a healthy NIM. Given that IDFCB’s NIM is near industry highs due to the higher rate of lending, I don’t think we need to be too concerned about the deposit interest rate, whether it’s 6 or 7. CASA ratio also being at industry high levels, it makes sense to rationalise the deposit interest rates to further boost the NIM.

The main concern, as I understand it, is the consequence of lending at such high interest rates i.e. riskier loans which further lead to NPA’s, provisioning etc. Provisioning is what has been holding the BV back for the past year and doesn’t look like reducing anytime soon.

VV mentioned Q3 & Q4 is where we can see real NPA numbers. I think he is aware of this 4 months back itself. He predicted all the banks will be showing covid NPA’s around Q3 and Q4. He mentioned this in an interview with CNBC or ET post Q2. One comforting factor is in q3 presentation collection is almost returned to pre covid levels (98%) and improving. I feel next few quarters will see real growth and real profits ( Not the trading gains). I am hopeful …

Disc: Fully Invested

I am having trouble assessing the asset quality. The write-off numbers are not mentioned anywhere. And how does write-offs or sale of loans to Asset restructuring companies affect the balance sheet? Like how many provisions can be reversed? Does it affect the top line or bottom line?

As I have been saying before, it is important to focus on total customer deposits (TD+CASA) as a percent of total operational liabilities since it is this part of the book on which bank has a lot more control and a lot more ability to maneuver. Let us compare IDFCF to some other leading banks (All figures are in cr):

Bank name

Total Customer TD

Total Customer CASA

Total borrowings

Customer TD +CASA + borrowings

(Customer TD+CASA) / total borrowings

Data from

IDFC First Bank

37058

20661

64508

122227

0.472

Q4FY20

IDFC First Bank

36726

40563

47478

124767

0.619

Q3FY21

Bandhan Bank

36052

21029

16379

73460

0.777

Q4FY20

Bandhan Bank

40640

30540

12667

83847

0.848

Q3FY21

HDFC Bank

662,877

484625

144,628.00

1,292,130

0.888

Q4FY20

Kotak Bank

109,130

156174

48,223.00

313,527

0.846

Q3FY21

ICICI Bank

461000

340500

164900

966400

0.829

Q2FY21

What we can see is that most good banks have this ratio 82%+. They have very good control on their cost of funds as well as the liquidity situation. IDFCF has a significantly worse position right now. An anti-thesis would point this out as a negative. An investment thesis would see this as an opportunity for metamorphosis. Good news is that this position is moving in the correct direction. For some reason they do not want to seem to retire their total (market) borrowings**, which makes me think that they might be at a low cost of funds. IMO the current reduction of SA rate will definitely cause a slow down in growth of CASA. IDFCF growth in this regard might slow down to that of bandhan bank (which has been offering 6% CASA+TD rates for few years now).

Please go through the thread. Someone has posted a good video explaining asset quality. TL;DR is we do not know the write-offs right now. GNPA+Write-offs will leave a hole in the book unless provisions cover those.

Disc: Invested.

**: Makes me wish that they held a concall, would have loved to understand management reasoning here instead of second guessing.

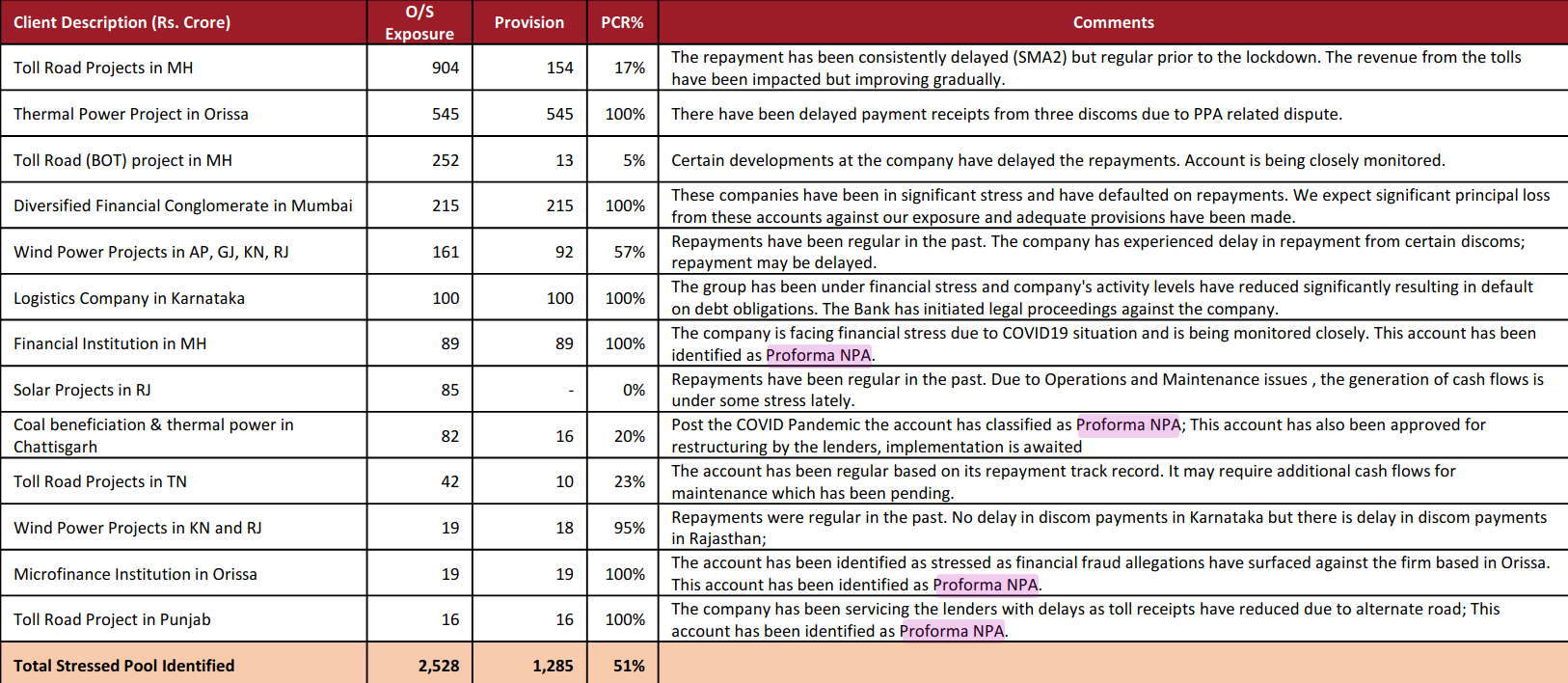

Not sure if all the numbers can be taken at face value here, I think there will be overlap between proforma GNPA, stressed book and (eventual) restructured book, leading to double or even triple counting some loans if looked at this way.

Yes your reasoning is correct thanks to the SC order. Basically no account that was standard in March can be declared as NPA, but if you see the RBI announcement it is these very same accounts that are eligible for restructuring. As a result it is very likely that the 2% of the accounts that might be restructured are also a part of the pro forma NPA, we just won’t know for sure without a confirmation from the management.

Secondly,the chart you have posted shows accounts that are stressed but not NPA. If you see the chart from March then the list of accounts mentioned there were stressed but not NPA in March, as a result logically speaking they should have been eligible for both being restructured (unless already done) and being a part of the pro forma NPA announced by the bank. Hence we should be careful when just simply adding all these numbers to come to the stressed assets as its very likely there is an overlap.

yeah sahil, they might be getting money at low cost, as the interest rates are low now. That is the reason they are going with borrowings. There won’t be much difference for big banks since they already offer low interest cost to deposits and CASA. So it does not make much sense for big banks to borrow.

They can’t get rid of those borrowings as those are long term bonds from IDFC days. They will be retired when they mature. A big chunk retires next year.

I was wondering why the Opex is so high. Is it investment in branches, technology etc or is it the nature of the retail financing business.

I was feeling pretty good about the results. Then I saw Morgan Stanley target of 20. Their logic seems to be low ROE but that is clearly a matter of next year or 2.

Can’t they prepay those bonds? I think they were already doing that for other bonds. Is there any way that I can read the raw data of those bonds (number of bonds, duration, terms like prepayment, quantum of interest and principal)?

Morgan Stanley

If I had a penny for every time Morgan Stanley gave a bearish report on idfc first bank, I’d be a billionaire. They, are clearly biased. Check their previous reports including from last year beginning. Earlier the logic was that idfc first won’t be able to build CASA. I generally treat the opinions in these research reports as garbage in garbage out. The facts and figures are what I generally rely on.

This budget had 2 ways in which it benefits idfc first bank.

Banking sector related: creation of bad bank which enable all banks to dispose off of their toxic assets in a much more efficient way. Think of all loans where idfc first has 100% provision, someone that thinks they are skilled at stressed asset reconstruction or recovery might be willing to pay some money for such an asset (this is the business model of bad banks). This would benefit all banks. Of course idfc first would still suffer haircuts but those haircuts are expected to come down.

Idfc bank specific: with this huge gush of liquidity into the infra sector (depending on timelines of course), idfc’s infra asset quality could possibly improve as the entire eco-system becomes liquidity surplus and also revenues increase from higher infra capex by government. This is more like a possibility (hard to quantify) so I am treating this more like an optionality. The creation of DFIs (public + private) would enable better infra financing.

.

On one side Morgan Stanley was giving targets like 13 and 20 for IDFC First Bank, on other side they are buying shares of its holding company IDFC Limited at price of 38.7…am I missing something here…