I agree with your assessment.

As regards provisioning, I feel VV is purposely over provisioning to avoid the possibility of showing a loss even if there are negative surprises in a future quarter.

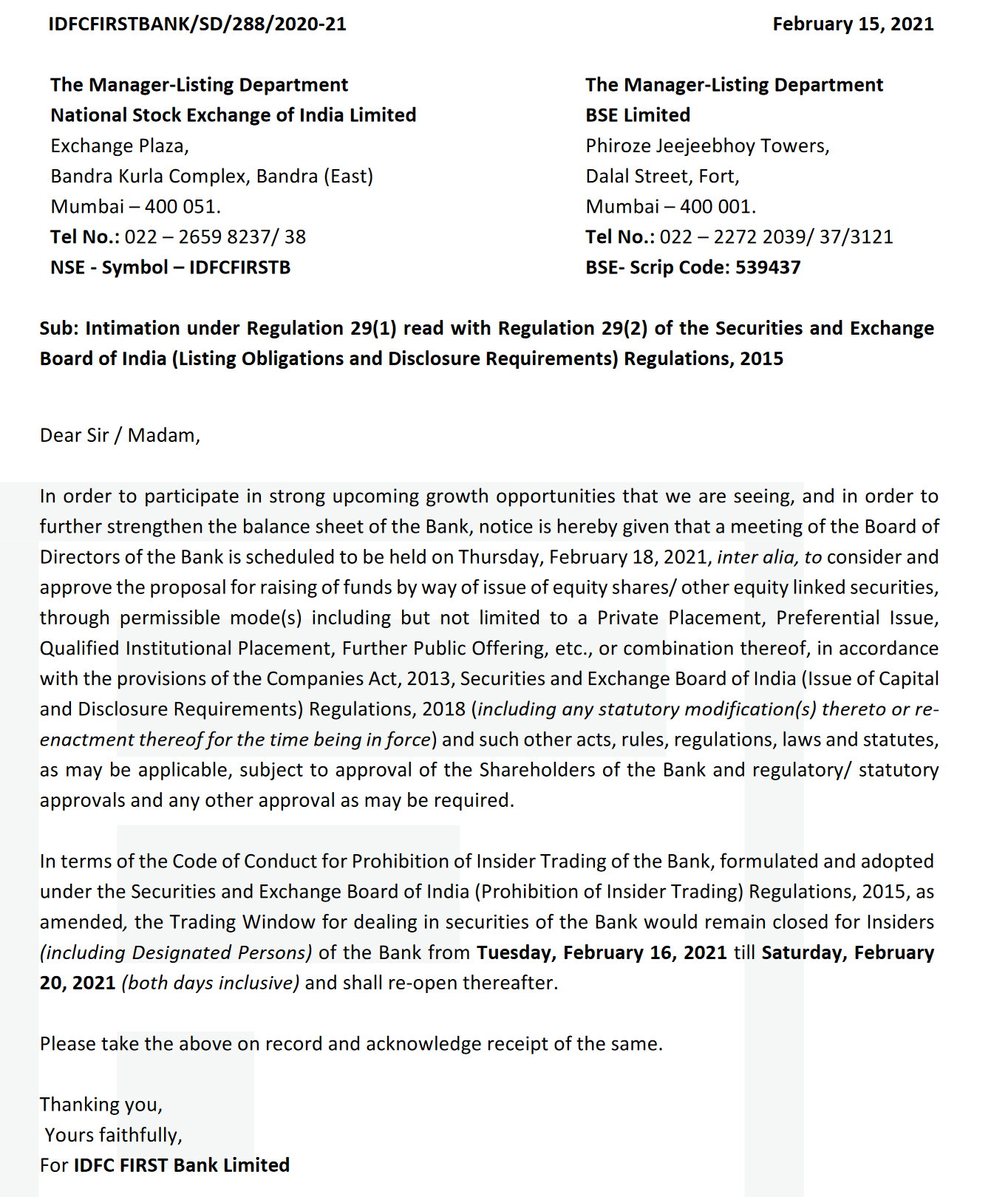

A good stock price would help them in raising capital with less equity dilution.

There is very little uncertainty now. The moment all remaining fog clears, the price would become too high in no time.

Disc- Invested

1 Like

My takeaway is slightly different. It seems like the provisioning has been based on what’s possible while maintaining a profit. The bank wants to show consistent profitability and therefore doesn’t want to increase provisions at the risk of slipping in the red. Which leads me to fear that the provisions may be lower than ideal, given the rising NPAs.

3 Likes

About the provisioning-

We have to look at a few points-

-

Bank already has 2% of book as covid provisions. That is a sizeable amount

-

I don’t mind the management trying to show tepid profits. The markets are extremely moody and price drives perception. To see this play out check any thread on the forum. As the price moves up people start discussing, even though this is a value forum.

If slight losses are shown versus slight profits the markets might lose all sense of logic and give Morgan Stanley eske targets. This causes real problems for capital raising for the bank. And management would be acutely aware of this. Mr Vaidyanathan has dealt with PE investor for the larger part of the last decade. -

Covid is a black swan and management needs to be trusted on their word for their assessment- with banks we need to trust the jockey

-

Mr Vaidyanathan seems to me to be the type who would not like the formality type procedure of concalls.

I think he knew there would be 10 questions about CASA about a year back and even now 20 questions on the provisions going up.

I think they will start these once the bank stabilises.

3 Likes

I fully agree with your views. Keeping in view the past track record of Mr Vaidynathan in ICICI and Capital First, he deserves the time to prove himself. Frank and transparent approach of the management of this company is rarely seen in others. I am sure he will prove Morgan Stanley wrong in the near future.

Disc :Invested

2 Likes

If the NPAs keep rising then you are right but logically one would imagine that most of the stress must already be out in the open. A person / business who was able to make payments regularly upto 31st Dec will probably not suddenly default in the January-March quarter and become a fresh NPA. If the worst is behind us then the current provisions should be more than enough. Also one needs to remember the restructured book of 2% that some folks are treating as entirely stressed is actually a book that was standard on 1st March and a book that the RBI only needs a PCR of 10% on. So for a 2000cr book only 200cr provisions are regulatory required.

I feel that VV is once again being overly conservative and providing the maximum amount to provisioning that he possibly can while maintain a positive trend in the profitability of the bank.

2 Likes

I completely agree with you. Based on my limited understanding, the moratorium ended on Aug 31, so 90 days after that have elapsed in the quarter gone by i.e. Q3. Therefore, the pain that was hidden by the moratorium should be entirely visible in Q3, and Q4 onwards the process of recovery / writing off should commence. While this is my understanding, VV was quite categorical in interviews at the end of Q2 that the real pain will only show at the end of Q4 - I do not understand the reasoning behind this. Taking it at face value, my fear is that the current ~4% number is only going to rise in the coming quarter.

Also, while the RBI mandated PCR is 10% on the restructured book, I’m not sure that level is the most prudent. If other banks have much higher PCR’s, then IDFCB’s valuation will suffer in comparison. My personal preference would be to have higher provision, much like VI. If not necessary, it can always come back into profits. It would be a sign of the conservatism that has drawn a lot of us to VV and IDFCB.

Would be more than happy to be proved wrong or corrected. Invested.

1 Like

Point taken though, that excessive provisioning has to be balanced with showing profitability. As someone pointed out above, a higher share price makes it easier to raise equity with lesser dilution.

1 Like

Yes but when he gave that interview in Q2 we were probably in the worst phase of the Covid crisis and everybody was expecting the worst. I think it was the same interview where he said there would be no loan growth in FY21 and it would be a standstill sort of a year. Both the IMF and RBI were expecting a -10% GDP degrowth etc. Fast forward one quarter and things have turned on a dime, GDP forecast upgraded to -7% with a positive Q4 expected and even IDFCB witnessed excellent growth in their retail book. Commentary from most banks and NBFCs has been generally positive with most saying the worst is behind us and expecting a good Q4. Would be great if we could hear from VV on this but I guess their guidance on the pro forma NPA must be based on a similar experience.

2 Likes

Equity getting diluted with small esops

https://www.google.com/amp/s/wap.business-standard.com/article-amp/news-cm/idfc-first-bank-allots-6-32-lakh-equity-shares-under-esos-121021001306_1.html

Why do IDFC First Bank share holder prefer to hold bank directly instead of indirect exposure via IDFC’s 40% holding?

With IDFC there is 35% discount to the value of IDFC First Bank stake + IDFC MF 100% ownership.

1 Like

The reason could be uncertainty.

Holding companies typically have discounts that may be due to the perception that they don’t have access to the operating asset cashflow directly, mis allocation of capital is possible etc. That is a likely reason

2 Likes

@Shankar, are these reasons for you as well?

I understand these are typical concerns about holding company structure.

IDFC is a different story since management has communicated their desire to get rid of the discount. Laid out and executed plan for divestment of assets. Paid for cash flow from divestment of assets except for unexpected fund raise from IDFC First Bank and regulatory requirement to maintain 40% stake.

IDFC would like to get rid of the discount to NAV but that is derived mostly from RBI/Govt action on NOFHC structure and tax treatment to exit from the structure.

Since underlying assets such as IDFC First Bank and MF business are growing, even if they distribute shares of these holdings to IDFC share holders, mostly the share holders on this forum might want to hold on to the distributed shares.

4 Likes

IDFC First bank has given 56799 credit cards by end of Dec 2021 as per RBI data. ATM1220208E8C93801C6D4F2399EF31C19A0805A9 (1).XLSX (21.5 KB)

2 Likes

Which might be a dampener on growth given the GOI push on Infra,no? I get it that Infra loans lock up large amount of capital and you get hit if there’s delay but at least they should be looking at projects that are 75% done or higher and looking for last mile capex especially low default industries like chem,pharma and oil

IDFC First bank is going to get indirect benefit of infra push by way of buying/spending power of the people involved in the infra built up. I think VV has an excellent experience and strategy of increasing retail loan book.

1 Like

Post-conference notes published by Edelweiss gives IDFC First a 12-month target of 46/- . Conference attendees from IDFC First were CEO, CFO and Head, IR. The key takeaways published by them are

-

‘Retailisation’ of loan book using AI/ML

-

Funding Cost - reducing rates will not impact due to goodwill of bank and better than competitor rates

-

More points around asset quality (collection efficiency at 98% in retail loans, pretty much back to pre-covid levels), branch expansion (tier-1 on priority followed by other cities), use of tech and capital raise needed when growth picks up.

Honestly, I was trying to understand the logic behind the price target given that most of the published takeaways are already captured in my thesis and the only two points which seemed to clarify this was

- “High growth in MFI/MSME consumer segments, where our prognosis of systemic asset quality remains bleak”

- “A wide gap between reported net worth and true residual equity remains a concern”

5 Likes

Concall of IDFC Limited happened today and according to management, IDFC First Bank would have reported a loss of 626 in Q3 if they had reported their numbers according to IndAS instead of IGAAP…

.

Can someone please explain this…what is the specific difference between two accounting standards which is causing this deviation and what could be the reason for IDFC First bank to stay with IGAAP instead of reporting according to IndAS…do other banks also use IGAAP…

2 Likes

Any specific standard mentioned? Because there are various standards in IndAS. So if any specific standard due to which this deviation is there.

1 Like