Checked the fintech apps.

I don’t have the source with me. I read somewhere, it is an yearly payment schedule and the payment is made in December. Also, Vodafone just made a few crores of payment to Franklin AMC, so they are making payments.

My views:

- Vodafone is a dead company. Nobody in their right mind invests in this company’s equity in the middle of a pandemic. Amazon believes in market leadership and not turnarounds.

Expect it to declare bankruptcy suddenly because it is taken to court by some tower vendor etc.

Declaring to markets that they have an announcement to make and then putting out a new logo is showing their desperation. - IDFC First bank has greater than 10% NPAs. They had 28% moratorium so this is a good conservative measure. IDFC First has a poor loan book so it’s Npas are expected to be worse than industry average.

Dis- Indirectly Invested.

2 Likes

Very recently, in an interview Vaidyanathan said, if they were to calculate moratorium the way SBI calculated, their moratorium would be 15% and not 28%. He is known to be prudent and conservative.

2.28

2 Likes

He also added :

0. As ashish added, if we compute the moratorium part of the book as the definition being used by SBI, then 15% of the book is under moratorium as of June end and not 28%.

- After conservatively promising 0% growth in loan book in the AR, after looking at the lending in June, July, August, he now expects it to grow by 10-15%.

- All industries are not affected equally. The physical contact industries are affected more materially rather than others like Pharma, Chemicals, Agro facing businesses.

- Government is reviewing even with private sector banks, the extent of their lending to MSME enterprises (periodic updates with the ministry).

- There is no reluctance towards lending at all. This is a great opportunity to lend at 9.25% (risk free) guaranteed by the government.

- IDFCF has disbursed 1400 cr towards this end (against an internal target of 2400 cr).

Disc: Invested.

8 Likes

Depends on “Terms & Conditions” agreed with those fin-techs.

can anyone clarify on this?

Hi All,

A leading Fintech named Niyo has collaborated with IDFC First bank for saving account.

Below is the urls

4 Likes

Hi,

Newbie here.

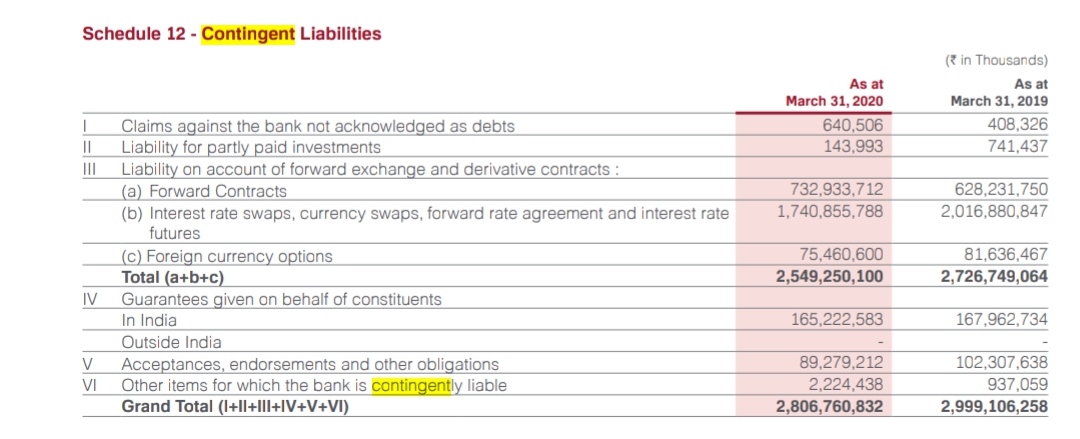

I find the contingent liabilities (schedule 12 of annual report 2019-2020) disproportionately high (₹2,806,760,832,000) to the networth of the bank. Is it a red flag?

3 Likes

I know one instance where they have tied-up to disburse loans to Flipkart’s vendors. The arrangement is such that bank is providing the financing etc but Flipkart has to make good any NPA arising out of it. I heard good reviews about the bank’s tech team working on the project.

4 Likes

IDFC bank has a different business model as compared to other banks. Correct comparison of IDFC first can be done with NBFCs like Bajaj Finance or Credit card companies like SBI cards and Payments.

Along with above, they have some other products which are similar to Banks.

Since they have a lot of unsecured retail lending, GNPA is going to be around 2% most of the time(it will be great if this comes below 2 and stays there). Being a bank they would have certain advantages over NBFCs as lower cost of capital and they can lend more than NBFCs with respect to their equity capital.

You can also compare yield rate and GNPA of other unsecured lenders(SBI cards and payments,Bajaj Finance etc) with IDFC First.

1 Like

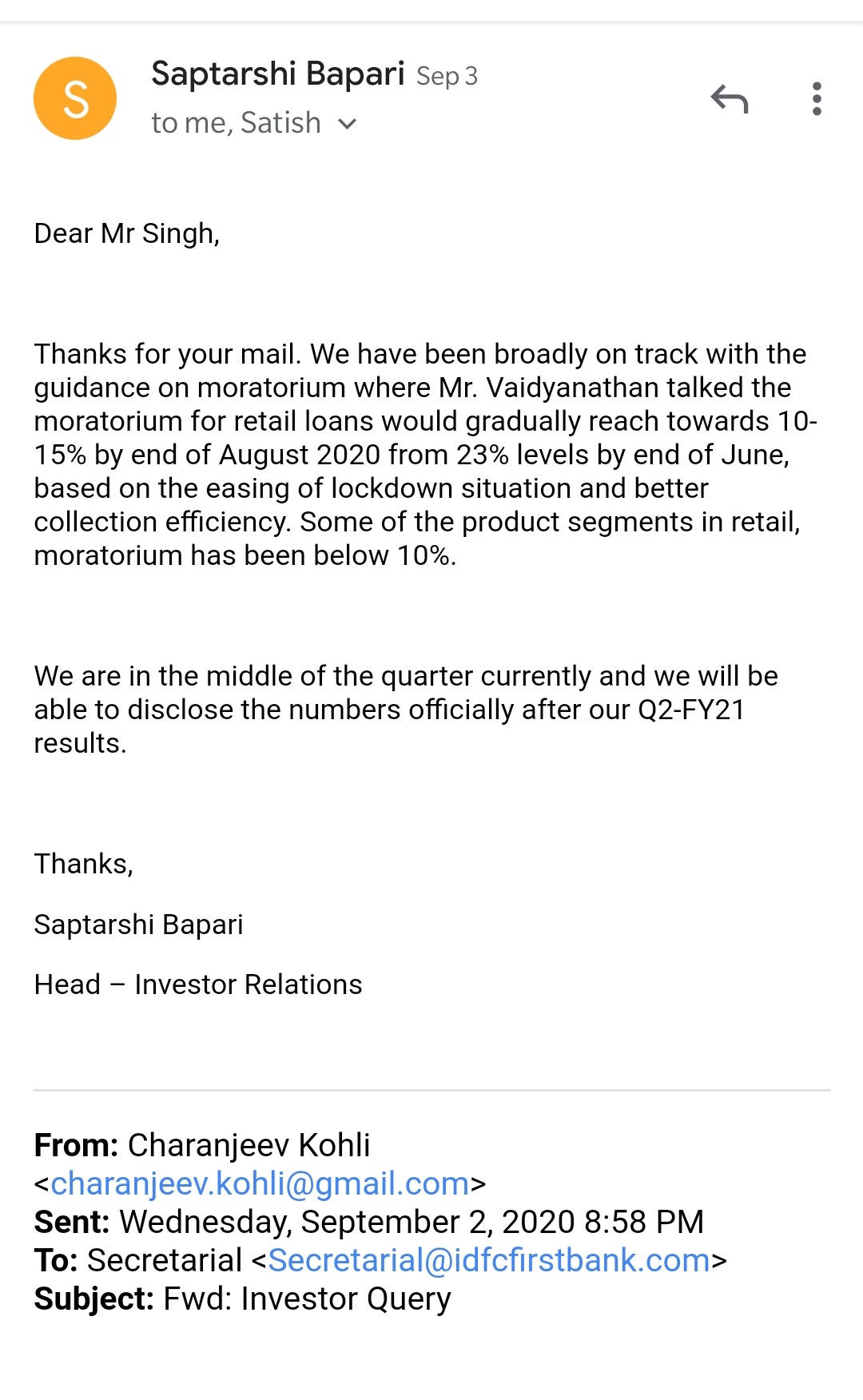

Mr. Vaidyanathan had mentioned that the moratorium book would come down to 10 percent from 28 percent by Aug end. Any updates on this front? Can’t find anything on the net with respect to this.

There is 1 update. Please see my previous comment.

Hi All,

Please have a look at my model and criticise to help improve it.Model- IDFC First Bank.xlsx (415.3 KB)

1 Like

I wrote to the Bank at end of August, followed up for reply & got the response as below.

My take:

They are now talking about retail loans only, means stress in wholesale loans. Also reading between the lines doesn’t give confidence. Segments of retail has been <10%. This means they couldn’t assure uniform <10%.

13 Likes

i get the impression that he is conveying that they are well on target. If the situation was not good, he would have replied that he is not allowed to disclose information to individuals.

4 Likes

Good point, my concern is: he specifically mentioning about retail. This is change of narrative. This indicates some issue in wholesale.

1 Like

Received OneCard Credit Card today. Its a metallic card and looks really good. Reason why I am posting this here is because it is partnered with IDFC First bank. Few things:

-The OneCard app has an amazing UI. Very friendly, attractive and easy to use. It focus on user

experience.

-The onboarding process was really smooth. All I had to do was download the app, enter my details and wait for few days. They grant the credit card only if you have a solid credit score and credit history. Moreover, they have a waitlist before you get the credit card: this, in my opinion, provides as aspirational touch to owning the credit card.

The best feature that I like about it is that you get 5x reward points for top 2 category spends.

Charges:

- Forex Markup is 1% (which I believe is lower than industry benchmark)

- Over the limit charges is 2.5%

- Cash withdrawal charges is 2.5% (which again I believe is lower than industry standards)

- Late Payment charges is 2.5%, with the maximum amount being just 1000/- (much much lower than the industry)

Key Takeaway: Great user experience. Not everyone gets this. The bank is targeting creditworthy borrowers and rewarding them for the trust. Great way to target the right set of customers.

Thoughts and opinions welcome!

4 Likes

1 Like

That seems fine.

If they are able to keep overall Npas to around 10% of book they should be fine.

Assuming 60 percent LGD we can expect the bank to handle this crisis decently.

So around 6000crore of book value loss expected in that case. The bank can handle that well.

Assumption- RBI financial stability report assumes Private banks to have 8% GNPAs.

1 Like

Does anyone know why IDFC does not have ASBA or UPI facility for applying for IPOs? Is it a regulatory issue or is it because they do not have the technology to offer this feature?

Almost all scheduled commercial banks and even several small urban co operative banks offer this facility. Without basic facilities like ASBA, I fear IDFC would have to always offer a much higher interest rate on SB accounts compared to other banks in order to be able to retain customers.

4 Likes